Nan Ya Plastics PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, raw-material price swings, and sustainability regulations are reshaping Nan Ya Plastics’ outlook—our concise PESTLE highlights the key external forces affecting strategy and margins. Purchase the full analysis for a comprehensive, actionable report you can use in investment models, strategic plans, or boardroom decks—downloadable and ready to deploy.

Political factors

Geopolitical instability and trade wars

The US–China tech rivalry in late 2025 pressures Nan Ya Plastics as tariffs and export controls, which rose 18% in affected chemical and plastics trade in 2024–25, cause sudden supply-chain reroutes and cost increases. Cross-border operations face higher compliance expenses—Nan Ya’s regional exports to North America and China comprised over 40% of group sales in 2024—forcing scenario planning and supplier diversification. Strategic risk models must incorporate tariff shocks and restricted tech transfers to protect market access.

Reciprocal tariff barriers

Reciprocal U.S. tariffs on select plastics and chemical products raise Nan Ya Plastics’ export costs, with U.S. duties on some polymer categories reaching up to 25% in 2024, pressuring margins and pricing for downstream customers.

Higher duties have driven more conservative purchasing and a 12% decline in U.S.-bound trade volumes for Taiwanese petrochemical exporters in 2024, reducing short-term demand for Nan Ya’s products.

To stay competitive, Nan Ya must absorb or pass on tariff-driven costs while countering regional rivals—some benefiting from lower or no tariffs—threatening market share in key export corridors.

Cross-strait relations and regional stability

As a Taiwan-based corporation with significant investments in mainland China, Nan Ya Plastics is highly sensitive to Taipei-Beijing political dynamics; in 2024 its 34 China plants accounted for nearly 50% of overseas operations and contributed roughly 28% of consolidated revenue.

Escalation in cross-strait tensions risks supply-chain disruptions, regulatory restrictions, and asset-operational constraints that could impair EBITDA margins and capex plans.

Operational continuity therefore hinges on geographic diversification, contingency inventory, and localized risk management, including local senior staffing and insurance, to protect revenue streams and mitigate potential losses.

International plastics treaty negotiations

By end-2025 negotiations for a legally binding UN plastics treaty are in a critical implementation phase, targeting up to 30% cuts in virgin plastic production in some proposals and mandatory corporate reporting on polymer flows.

This political push increases regulatory risk for Nan Ya Plastics, which reported NT$475.6 billion revenue in 2024 and may face higher compliance costs and asset retooling to meet production caps and extended producer responsibility rules.

Shareholder and consumer pressure for accountability grows as over 175 countries back the treaty framework, forcing strategic shifts in global production allocations and circularity investments.

- Negotiations target ~30% virgin plastic cut proposals

- Nan Ya Plastics 2024 revenue NT$475.6B — exposure to compliance costs

- 175+ countries support treaty framework increasing regulatory risk

- Requires cap-aligned production adjustments and circularity investments

Governmental energy and security policies

The Taiwanese government’s push for economic security and a net-zero 2050 target shapes Nan Ya Plastics’ long-term strategy, directing R&D and capex toward low-carbon processes; Taiwan aims to cut emissions 50% by 2030 vs 2005 and reach net-zero by 2050. Policies favoring trustworthy industries (semiconductors, AI) bolster Nan Ya’s electronic materials unit—critical as Taiwan allocated NT$1.07 trillion in 2024 for strategic industries—while imposing strict sustainability and reporting requirements. Compliance with these national goals is essential for accessing subsidies, land/energy allocations and preserving operating licenses.

- Taiwan net-zero 2050; 2030 ~50% reduction (vs 2005)

- NT$1.07 trillion 2024 strategic industry funding supports electronics materials

- Sustainability compliance required for subsidies, energy allocations, license to operate

Nan Ya braces for tariffs, China exposure and green capex amid global tech tensions

Geopolitical tensions, US–China tech restrictions and reciprocal tariffs (up to 25% in 2024) raised compliance and export costs; 40% of Nan Ya’s 2024 sales were to North America/China, and China plants contributed ~28% revenue. UN plastics treaty backing by 175+ countries and Taiwan’s net-zero/50%‑by‑2030 target force capex and circularity investments.

| Metric | 2024/2025 |

|---|---|

| Revenue | NT$475.6B |

| US tariffs | up to 25% |

| Export share | ~40% |

| China plants | 34 (~28% revenue) |

What is included in the product

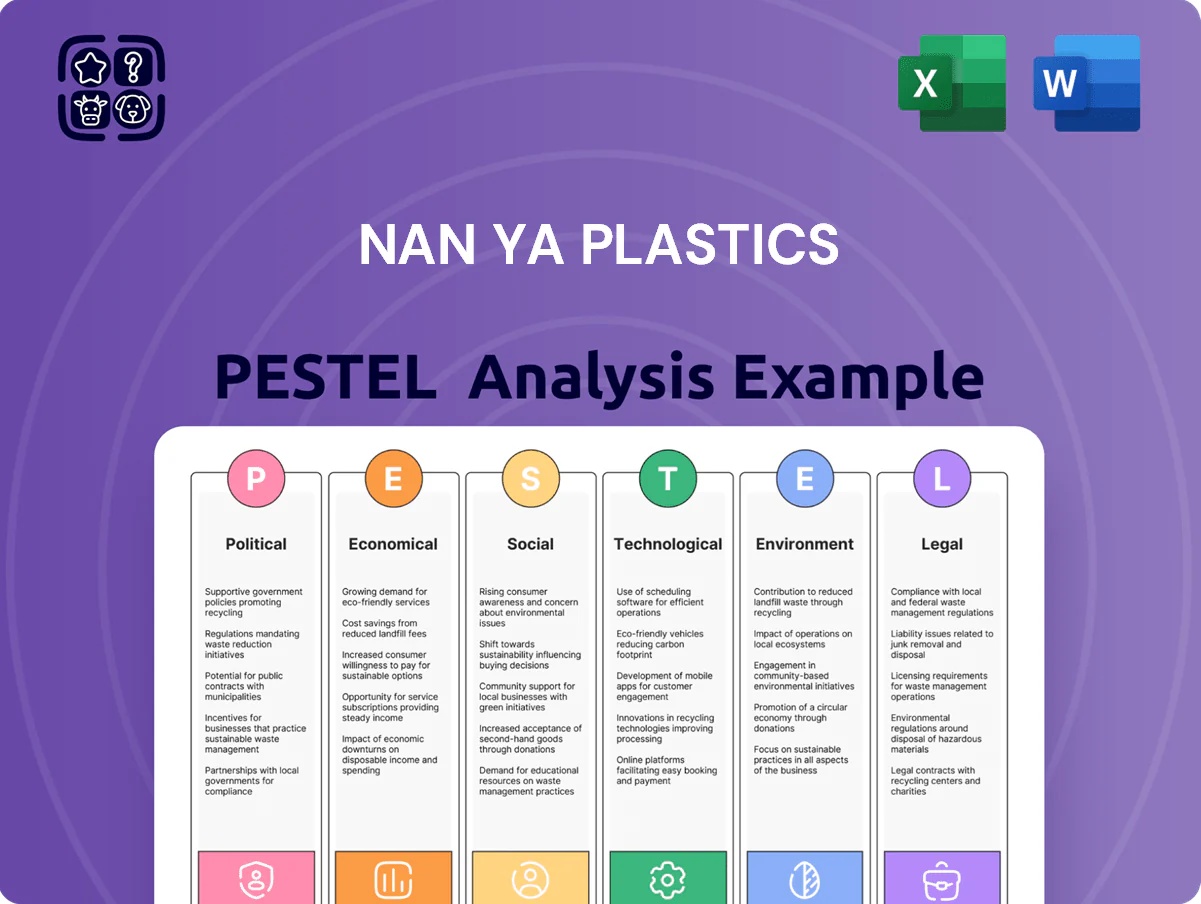

Explores how macro-environmental factors uniquely affect Nan Ya Plastics across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking scenarios to identify threats and opportunities for executives and investors.

A concise, visually segmented PESTLE summary for Nan Ya Plastics that can be dropped into presentations or shared across teams to streamline external risk discussions and support quick, context-specific note-taking during strategic planning.

Economic factors

High-growth demand from AI and semiconductors

Surging AI and HPC demand is a key economic driver for Nan Ya Plastics toward 2026, with electronic-materials revenue—copper-clad laminates and IC substrates—growing strongly; company electronic materials sales rose ~18% YoY in 2024, outpacing overall revenue growth of ~6%.

Petrochemical market oversupply

China added roughly 6–8 million tonnes/year of polyester capacity from 2020–2024, contributing to a global chemical/polyester glut that cut average PTA/MEG margins by about 20–30% in 2023–2024; this oversupply intensifies price competition and depresses commodity-grade resin margins for Nan Ya. As a result, the firm faces margin erosion in standard products and increased inventory turns pressure. To protect profitability, Nan Ya is shifting R&D and capex toward differentiated, high-end polymers and specialty resins that command 10–30% price premiums versus commodity grades.

Volatility in raw material and energy costs

Fluctuations in international crude oil—which averaged about $78/bbl in 2025—and periodic ethylene feedstock shortages have increased Nan Ya Plastics’ input costs, lifting resin production cash costs by an estimated 6–9% in 2024–25; a sudden oil spike could shave several percentage points off margins for its Taiwan and Texas chemical plants.

Global inflationary pressures and interest rates

Persistent inflation and elevated policy rates—US CPI at 3.4% (2024) and ECB refinancing around 3.5%—have suppressed consumer spending on durable, plastic-intensive goods, reducing volumes for Nan Ya Plastics.

Higher borrowing costs and cautious construction activity cut demand for packaging and building materials, shortening customer ordering cycles and pressuring sales visibility.

Nan Ya must tightly manage capex and preserve liquidity; for context, corporate borrowing spreads and liquidity buffers tightened across APAC in 2024, elevating refinancing risk.

- US CPI 2024: 3.4%; ECB rate ~3.5%

- Shorter ordering cycles → lower sales visibility

- Reduced demand in construction & packaging

- Capex restraint and liquidity preservation prioritized

Foreign exchange rate fluctuations

As a major global exporter, Nan Ya Plastics is highly sensitive to New Taiwan Dollar moves versus the U.S. Dollar and Renminbi; a NT$ appreciation of 5% in 2024 reduced export competitiveness and compressed gross margins reported in FY2024.

Favorable FX gains can lift net income—NT$300–500 million one-off gains were noted in 2023 when USD/TWD weakened—yet volatility complicates pricing and quarterly guidance.

Effective hedging is central: Nan Ya reported covering roughly 60–70% of anticipated FX exposure in 2024 through forwards and options, reducing earnings volatility.

- USD/TWD and CNY/TWD swings directly affect margins and revenue translation

- One-off FX gains/losses have reached several hundred million NT$ in recent years

- Hedging coverage ~60–70% in 2024 to stabilize results

AI/HPC materials surge 18% in 2024 as polyester margins slump and costs rise

AI/HPC-driven electronic materials grew ~18% YoY in 2024, outpacing total revenue (~6%); polyester oversupply cut PTA/MEG margins ~20–30% in 2023–24; feedstock/oil raised resin cash costs ~6–9% in 2024–25; US CPI 2024 3.4%, ECB ~3.5%; FX volatility: NT$ appreciation ~5% in 2024 reduced competitiveness; hedging ~60–70% coverage in 2024.

| Metric | Value |

|---|---|

| Electronic materials growth (2024) | ~18% YoY |

| Total revenue growth (2024) | ~6% |

| PTA/MEG margin drop | 20–30% |

| Resin cash cost rise (2024–25) | 6–9% |

| US CPI (2024) | 3.4% |

| Hedging coverage (2024) | 60–70% |

Preview the Actual Deliverable

Nan Ya Plastics PESTLE Analysis

The preview shown here is the exact Nan Ya Plastics PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, raw-material price swings, and sustainability regulations are reshaping Nan Ya Plastics’ outlook—our concise PESTLE highlights the key external forces affecting strategy and margins. Purchase the full analysis for a comprehensive, actionable report you can use in investment models, strategic plans, or boardroom decks—downloadable and ready to deploy.

Political factors

Geopolitical instability and trade wars

The US–China tech rivalry in late 2025 pressures Nan Ya Plastics as tariffs and export controls, which rose 18% in affected chemical and plastics trade in 2024–25, cause sudden supply-chain reroutes and cost increases. Cross-border operations face higher compliance expenses—Nan Ya’s regional exports to North America and China comprised over 40% of group sales in 2024—forcing scenario planning and supplier diversification. Strategic risk models must incorporate tariff shocks and restricted tech transfers to protect market access.

Reciprocal tariff barriers

Reciprocal U.S. tariffs on select plastics and chemical products raise Nan Ya Plastics’ export costs, with U.S. duties on some polymer categories reaching up to 25% in 2024, pressuring margins and pricing for downstream customers.

Higher duties have driven more conservative purchasing and a 12% decline in U.S.-bound trade volumes for Taiwanese petrochemical exporters in 2024, reducing short-term demand for Nan Ya’s products.

To stay competitive, Nan Ya must absorb or pass on tariff-driven costs while countering regional rivals—some benefiting from lower or no tariffs—threatening market share in key export corridors.

Cross-strait relations and regional stability

As a Taiwan-based corporation with significant investments in mainland China, Nan Ya Plastics is highly sensitive to Taipei-Beijing political dynamics; in 2024 its 34 China plants accounted for nearly 50% of overseas operations and contributed roughly 28% of consolidated revenue.

Escalation in cross-strait tensions risks supply-chain disruptions, regulatory restrictions, and asset-operational constraints that could impair EBITDA margins and capex plans.

Operational continuity therefore hinges on geographic diversification, contingency inventory, and localized risk management, including local senior staffing and insurance, to protect revenue streams and mitigate potential losses.

International plastics treaty negotiations

By end-2025 negotiations for a legally binding UN plastics treaty are in a critical implementation phase, targeting up to 30% cuts in virgin plastic production in some proposals and mandatory corporate reporting on polymer flows.

This political push increases regulatory risk for Nan Ya Plastics, which reported NT$475.6 billion revenue in 2024 and may face higher compliance costs and asset retooling to meet production caps and extended producer responsibility rules.

Shareholder and consumer pressure for accountability grows as over 175 countries back the treaty framework, forcing strategic shifts in global production allocations and circularity investments.

- Negotiations target ~30% virgin plastic cut proposals

- Nan Ya Plastics 2024 revenue NT$475.6B — exposure to compliance costs

- 175+ countries support treaty framework increasing regulatory risk

- Requires cap-aligned production adjustments and circularity investments

Governmental energy and security policies

The Taiwanese government’s push for economic security and a net-zero 2050 target shapes Nan Ya Plastics’ long-term strategy, directing R&D and capex toward low-carbon processes; Taiwan aims to cut emissions 50% by 2030 vs 2005 and reach net-zero by 2050. Policies favoring trustworthy industries (semiconductors, AI) bolster Nan Ya’s electronic materials unit—critical as Taiwan allocated NT$1.07 trillion in 2024 for strategic industries—while imposing strict sustainability and reporting requirements. Compliance with these national goals is essential for accessing subsidies, land/energy allocations and preserving operating licenses.

- Taiwan net-zero 2050; 2030 ~50% reduction (vs 2005)

- NT$1.07 trillion 2024 strategic industry funding supports electronics materials

- Sustainability compliance required for subsidies, energy allocations, license to operate

Nan Ya braces for tariffs, China exposure and green capex amid global tech tensions

Geopolitical tensions, US–China tech restrictions and reciprocal tariffs (up to 25% in 2024) raised compliance and export costs; 40% of Nan Ya’s 2024 sales were to North America/China, and China plants contributed ~28% revenue. UN plastics treaty backing by 175+ countries and Taiwan’s net-zero/50%‑by‑2030 target force capex and circularity investments.

| Metric | 2024/2025 |

|---|---|

| Revenue | NT$475.6B |

| US tariffs | up to 25% |

| Export share | ~40% |

| China plants | 34 (~28% revenue) |

What is included in the product

Explores how macro-environmental factors uniquely affect Nan Ya Plastics across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking scenarios to identify threats and opportunities for executives and investors.

A concise, visually segmented PESTLE summary for Nan Ya Plastics that can be dropped into presentations or shared across teams to streamline external risk discussions and support quick, context-specific note-taking during strategic planning.

Economic factors

High-growth demand from AI and semiconductors

Surging AI and HPC demand is a key economic driver for Nan Ya Plastics toward 2026, with electronic-materials revenue—copper-clad laminates and IC substrates—growing strongly; company electronic materials sales rose ~18% YoY in 2024, outpacing overall revenue growth of ~6%.

Petrochemical market oversupply

China added roughly 6–8 million tonnes/year of polyester capacity from 2020–2024, contributing to a global chemical/polyester glut that cut average PTA/MEG margins by about 20–30% in 2023–2024; this oversupply intensifies price competition and depresses commodity-grade resin margins for Nan Ya. As a result, the firm faces margin erosion in standard products and increased inventory turns pressure. To protect profitability, Nan Ya is shifting R&D and capex toward differentiated, high-end polymers and specialty resins that command 10–30% price premiums versus commodity grades.

Volatility in raw material and energy costs

Fluctuations in international crude oil—which averaged about $78/bbl in 2025—and periodic ethylene feedstock shortages have increased Nan Ya Plastics’ input costs, lifting resin production cash costs by an estimated 6–9% in 2024–25; a sudden oil spike could shave several percentage points off margins for its Taiwan and Texas chemical plants.

Global inflationary pressures and interest rates

Persistent inflation and elevated policy rates—US CPI at 3.4% (2024) and ECB refinancing around 3.5%—have suppressed consumer spending on durable, plastic-intensive goods, reducing volumes for Nan Ya Plastics.

Higher borrowing costs and cautious construction activity cut demand for packaging and building materials, shortening customer ordering cycles and pressuring sales visibility.

Nan Ya must tightly manage capex and preserve liquidity; for context, corporate borrowing spreads and liquidity buffers tightened across APAC in 2024, elevating refinancing risk.

- US CPI 2024: 3.4%; ECB rate ~3.5%

- Shorter ordering cycles → lower sales visibility

- Reduced demand in construction & packaging

- Capex restraint and liquidity preservation prioritized

Foreign exchange rate fluctuations

As a major global exporter, Nan Ya Plastics is highly sensitive to New Taiwan Dollar moves versus the U.S. Dollar and Renminbi; a NT$ appreciation of 5% in 2024 reduced export competitiveness and compressed gross margins reported in FY2024.

Favorable FX gains can lift net income—NT$300–500 million one-off gains were noted in 2023 when USD/TWD weakened—yet volatility complicates pricing and quarterly guidance.

Effective hedging is central: Nan Ya reported covering roughly 60–70% of anticipated FX exposure in 2024 through forwards and options, reducing earnings volatility.

- USD/TWD and CNY/TWD swings directly affect margins and revenue translation

- One-off FX gains/losses have reached several hundred million NT$ in recent years

- Hedging coverage ~60–70% in 2024 to stabilize results

AI/HPC materials surge 18% in 2024 as polyester margins slump and costs rise

AI/HPC-driven electronic materials grew ~18% YoY in 2024, outpacing total revenue (~6%); polyester oversupply cut PTA/MEG margins ~20–30% in 2023–24; feedstock/oil raised resin cash costs ~6–9% in 2024–25; US CPI 2024 3.4%, ECB ~3.5%; FX volatility: NT$ appreciation ~5% in 2024 reduced competitiveness; hedging ~60–70% coverage in 2024.

| Metric | Value |

|---|---|

| Electronic materials growth (2024) | ~18% YoY |

| Total revenue growth (2024) | ~6% |

| PTA/MEG margin drop | 20–30% |

| Resin cash cost rise (2024–25) | 6–9% |

| US CPI (2024) | 3.4% |

| Hedging coverage (2024) | 60–70% |

Preview the Actual Deliverable

Nan Ya Plastics PESTLE Analysis

The preview shown here is the exact Nan Ya Plastics PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decisions.