NSC-Tripoint Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

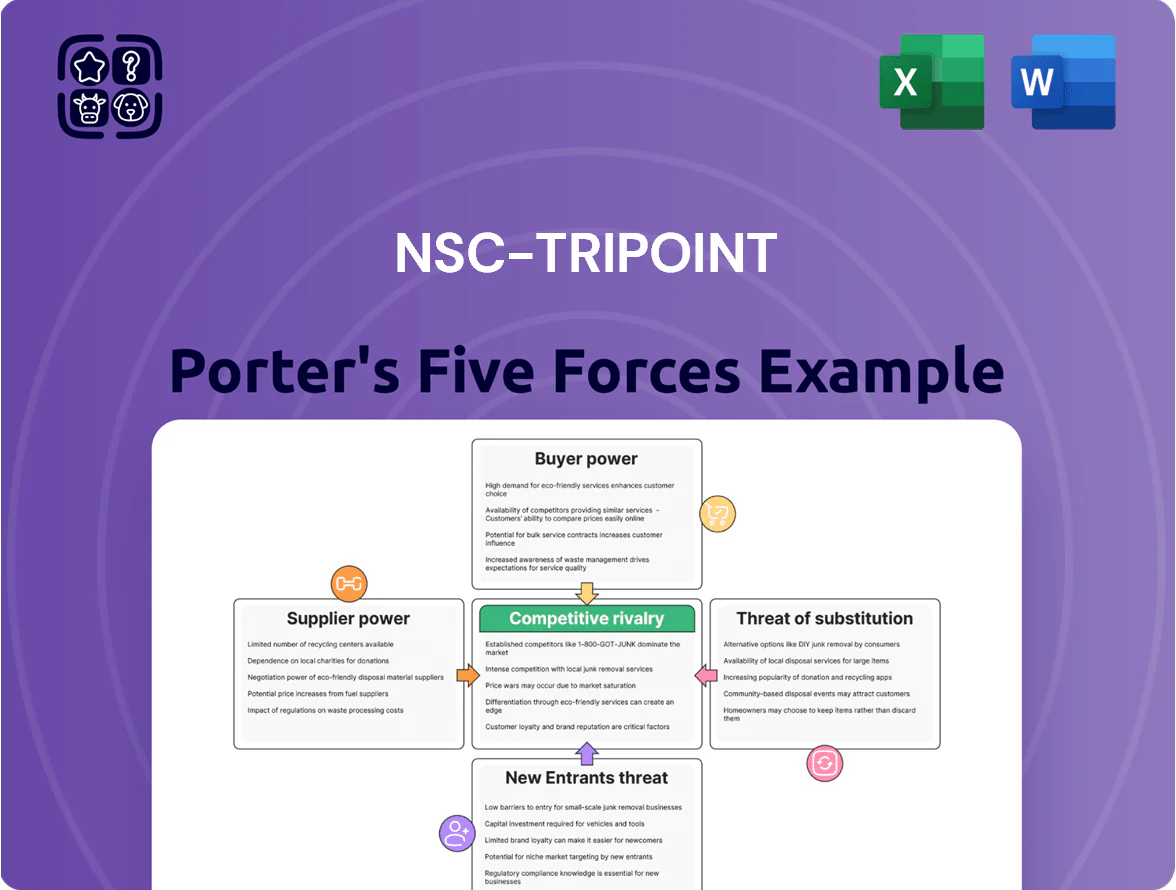

NSC-Tripoint faces moderate buyer power, concentrated suppliers, and evolving substitute threats in a capital-intensive logistics niche—regulatory shifts and scale advantages shape its competitive edge.

Suppliers Bargaining Power

Raw Material Price Volatility

High-grade steel and specialty alloys—making up ~60–70% of raw-material costs for rod pumps and plunger lifts—face global commodity swings; stainless and chrome alloys rose 8–12% in 2024 and remained 4–6% above pre‑2020 prices by late 2025.

Supply chains stabilized in 2025, yet premium-metal suppliers retain pricing power, often imposing minimum order premiums of 5–10% that squeeze small OEMs.

NSC-Tripoint must hedge and renegotiate long‑term contracts; a 3–5% procurement cost cut is needed to protect operating margins near current industry EBITDA of ~12–15%.

Specialized Component Dependency

Energy and Utility Costs

The energy-intensive manufacture and refurbishment of heavy oilfield equipment needs steady electricity and gas for heat treatment and CNC machining, and energy can be 15–25% of COGS for such plants; regional industrial utility providers function as monopolies or oligopolies, leaving NSC-Tripoint with minimal rate leverage; this raises exposure to policy shifts and price hikes—Europe gas rose 65% in 2022 and global industrial power tariffs climbed ~9% in 2024—pressuring margins through 2025.

Labor Market Tightness

Suppliers of certified welders and petroleum engineers exert strong bargaining power for NSC-Tripoint due to chronic shortages in oilfield services; BLS data show oilfield employment declined 8% since 2019 while specialized roles remain 20–30% understaffed in 2024.

Demand for precision-driven refurbishment raises pay: NSC-Tripoint must match market premiums—average wage premiums for certified technicians rose 15% in 2024—raising labor cost per refurbishment by an estimated 6–10%.

- Certified welders scarce: 20–30% understaffed (2024)

- Wage premium for specialists: +15% (2024)

- Labor lifts refurbishment cost: +6–10% per job

- Retention spend up: signing bonuses, benefits

Logistics and Transportation Constraints

- Only ~15–25% of carriers handle oversized oilfield loads

- Specialized hauling rates rose 18–30% during 2024 drilling peaks

- Fewer permits/equipment = higher supplier bargaining power

- Concentrated providers increase schedule and cost volatility

Suppliers wield high leverage: input costs, energy, wages and switching risk spike project costs

Suppliers hold moderate–high power: 60–70% of precision parts from top‑5 vendors (2024), steel/alloy costs +8–12% in 2024 and +4–6% above pre‑2020 by late‑2025, energy =15–25% of COGS with industrial power +9% (2024), certified technician wages +15% (2024); switching raises CapEx ~3–5% and missed deliveries can delay $12–25M projects.

| Metric | Value |

|---|---|

| Top‑5 vendor share | 60–70% (2024) |

| Steel/alloy change | +8–12% (2024) |

| Energy share COGS | 15–25% |

| Tech wage premium | +15% (2024) |

| Switching CapEx impact | +3–5% |

What is included in the product

Tailored Porter's Five Forces analysis for NSC-Tripoint that uncovers competitive drivers, buyer and supplier power, entry barriers, substitute threats, and strategic levers to protect market share and enhance profitability.

Compact Porter's Five Forces snapshot for NSC-Tripoint—quickly spot competitive pressures and prioritize strategic moves to reduce risk and protect margins.

Customers Bargaining Power

Consolidation of E&P Companies

By end-2025, E&P consolidation left the top 20 firms controlling ~62% of global upstream production, shrinking the buyer base and boosting customer bargaining power.

These mega-customers demand volume discounts of 10–25% and strict SLAs tied to penalties, pressuring NSC-Tripoint margins on high-volume contracts.

NSC-Tripoint must now compete for a smaller set of contracts—loss of a single mega-client (≥15% revenue) would cut revenue materially and raise concentration risk.

Low Switching Costs for Equipment

Standardized parts for rod pumps and plunger lifts mean switching vendors is cheap; industry surveys in 2024 show 62% of operators cite parts compatibility as top switching reason. If NSC-Tripoint fails to match uptime (target >98%) or same-day turnaround—key metrics—customers will choose lower-cost suppliers. That ties loyalty to immediate performance and price, pressuring margins and forcing continual operational excellence.

Focus on Total Cost of Ownership

Sophisticated financial teams at E&P firms now evaluate Total Cost of Ownership (TCO) over upfront capex, driving demand for NSC-Tripoint data on pump longevity and maintenance intervals; 68% of operators surveyed in 2024 said TCO influenced supplier selection, and buyers expect MTBF (mean time between failures) and lifecycle maintenance forecasts covering 5–10 years. Providing integrated well monitoring and field support is a purchase requirement, not a premium add-on, to win these data-driven contracts.

Price Sensitivity in Mature Fields

Operators use artificial lift mainly in mature fields where EBITDA margins often fall below 20% and lifting costs per barrel rise; that drives high price sensitivity and hard negotiations on new systems and refurbishments.

NSC-Tripoint must show clear ROI—e.g., a <10% lifting-cost reduction or 5–15% production uplift within 6–12 months—to win contracts against low-price competitors.

- Customers: mature-field operators, thin margins (~<20%)

- Price pressure: strong on equipment and refurb

- ROI needed: <10% cost cut or 5–15% production gain

- Selling point: payback ≤12 months

Access to Alternative Lift Methods

Customers can switch among Electric Submersible Pumps (ESP), Gas Lift, or rod pumps based on well depth, flow rate, and gas/oil ratio; global ESP market grew 6.1% in 2024 to $3.9B, showing strong adoption where efficiency matters.

If NSC-Tripoint’s rod pumps lag on lift efficiency or mean time between failures, buyers can retool to ESP/Gas Lift and move CAPEX and OPEX away from NSC-Tripoint, giving customers procurement leverage.

Technical optionality compresses margin and forces NSC-Tripoint to price competitively or offer service guarantees; in 2025, operators report 12–18% production uplift when switching to optimized lift methods.

- Buyers choose by well physics, not brand

- ESP market $3.9B in 2024, +6.1%

- Switch can shift CAPEX/OPEX off NSC-Tripoint

- Reported 12–18% production uplift on optimized switches

Concentrated, TCO‑driven buyers demand compatibility, <12‑month ROI and 10–25% discounts

Customers are concentrated (top 20 = ~62% upstream output by end-2025), price-sensitive (mature-field EBITDA <20%), and demand TCO data and SLAs; 2024 surveys: 62% cite parts compatibility, 68% TCO-driven selection. Loss of one mega-client (≥15% revenue) is material; buyers secure 10–25% volume discounts and expect <12-month payback (ROI: −10% lifting cost or +5–15% production).

| Metric | Value |

|---|---|

| Top-20 share (2025) | ~62% |

| Parts-switch reason (2024) | 62% |

| TCO-driven choice (2024) | 68% |

| Buyer discounts | 10–25% |

| Required ROI | <10% cost cut or 5–15% production |

Full Version Awaits

NSC-Tripoint Porter's Five Forces Analysis

This preview shows the exact NSC-Tripoint Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no samples, fully formatted and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

NSC-Tripoint faces moderate buyer power, concentrated suppliers, and evolving substitute threats in a capital-intensive logistics niche—regulatory shifts and scale advantages shape its competitive edge.

Suppliers Bargaining Power

Raw Material Price Volatility

High-grade steel and specialty alloys—making up ~60–70% of raw-material costs for rod pumps and plunger lifts—face global commodity swings; stainless and chrome alloys rose 8–12% in 2024 and remained 4–6% above pre‑2020 prices by late 2025.

Supply chains stabilized in 2025, yet premium-metal suppliers retain pricing power, often imposing minimum order premiums of 5–10% that squeeze small OEMs.

NSC-Tripoint must hedge and renegotiate long‑term contracts; a 3–5% procurement cost cut is needed to protect operating margins near current industry EBITDA of ~12–15%.

Specialized Component Dependency

Energy and Utility Costs

The energy-intensive manufacture and refurbishment of heavy oilfield equipment needs steady electricity and gas for heat treatment and CNC machining, and energy can be 15–25% of COGS for such plants; regional industrial utility providers function as monopolies or oligopolies, leaving NSC-Tripoint with minimal rate leverage; this raises exposure to policy shifts and price hikes—Europe gas rose 65% in 2022 and global industrial power tariffs climbed ~9% in 2024—pressuring margins through 2025.

Labor Market Tightness

Suppliers of certified welders and petroleum engineers exert strong bargaining power for NSC-Tripoint due to chronic shortages in oilfield services; BLS data show oilfield employment declined 8% since 2019 while specialized roles remain 20–30% understaffed in 2024.

Demand for precision-driven refurbishment raises pay: NSC-Tripoint must match market premiums—average wage premiums for certified technicians rose 15% in 2024—raising labor cost per refurbishment by an estimated 6–10%.

- Certified welders scarce: 20–30% understaffed (2024)

- Wage premium for specialists: +15% (2024)

- Labor lifts refurbishment cost: +6–10% per job

- Retention spend up: signing bonuses, benefits

Logistics and Transportation Constraints

- Only ~15–25% of carriers handle oversized oilfield loads

- Specialized hauling rates rose 18–30% during 2024 drilling peaks

- Fewer permits/equipment = higher supplier bargaining power

- Concentrated providers increase schedule and cost volatility

Suppliers wield high leverage: input costs, energy, wages and switching risk spike project costs

Suppliers hold moderate–high power: 60–70% of precision parts from top‑5 vendors (2024), steel/alloy costs +8–12% in 2024 and +4–6% above pre‑2020 by late‑2025, energy =15–25% of COGS with industrial power +9% (2024), certified technician wages +15% (2024); switching raises CapEx ~3–5% and missed deliveries can delay $12–25M projects.

| Metric | Value |

|---|---|

| Top‑5 vendor share | 60–70% (2024) |

| Steel/alloy change | +8–12% (2024) |

| Energy share COGS | 15–25% |

| Tech wage premium | +15% (2024) |

| Switching CapEx impact | +3–5% |

What is included in the product

Tailored Porter's Five Forces analysis for NSC-Tripoint that uncovers competitive drivers, buyer and supplier power, entry barriers, substitute threats, and strategic levers to protect market share and enhance profitability.

Compact Porter's Five Forces snapshot for NSC-Tripoint—quickly spot competitive pressures and prioritize strategic moves to reduce risk and protect margins.

Customers Bargaining Power

Consolidation of E&P Companies

By end-2025, E&P consolidation left the top 20 firms controlling ~62% of global upstream production, shrinking the buyer base and boosting customer bargaining power.

These mega-customers demand volume discounts of 10–25% and strict SLAs tied to penalties, pressuring NSC-Tripoint margins on high-volume contracts.

NSC-Tripoint must now compete for a smaller set of contracts—loss of a single mega-client (≥15% revenue) would cut revenue materially and raise concentration risk.

Low Switching Costs for Equipment

Standardized parts for rod pumps and plunger lifts mean switching vendors is cheap; industry surveys in 2024 show 62% of operators cite parts compatibility as top switching reason. If NSC-Tripoint fails to match uptime (target >98%) or same-day turnaround—key metrics—customers will choose lower-cost suppliers. That ties loyalty to immediate performance and price, pressuring margins and forcing continual operational excellence.

Focus on Total Cost of Ownership

Sophisticated financial teams at E&P firms now evaluate Total Cost of Ownership (TCO) over upfront capex, driving demand for NSC-Tripoint data on pump longevity and maintenance intervals; 68% of operators surveyed in 2024 said TCO influenced supplier selection, and buyers expect MTBF (mean time between failures) and lifecycle maintenance forecasts covering 5–10 years. Providing integrated well monitoring and field support is a purchase requirement, not a premium add-on, to win these data-driven contracts.

Price Sensitivity in Mature Fields

Operators use artificial lift mainly in mature fields where EBITDA margins often fall below 20% and lifting costs per barrel rise; that drives high price sensitivity and hard negotiations on new systems and refurbishments.

NSC-Tripoint must show clear ROI—e.g., a <10% lifting-cost reduction or 5–15% production uplift within 6–12 months—to win contracts against low-price competitors.

- Customers: mature-field operators, thin margins (~<20%)

- Price pressure: strong on equipment and refurb

- ROI needed: <10% cost cut or 5–15% production gain

- Selling point: payback ≤12 months

Access to Alternative Lift Methods

Customers can switch among Electric Submersible Pumps (ESP), Gas Lift, or rod pumps based on well depth, flow rate, and gas/oil ratio; global ESP market grew 6.1% in 2024 to $3.9B, showing strong adoption where efficiency matters.

If NSC-Tripoint’s rod pumps lag on lift efficiency or mean time between failures, buyers can retool to ESP/Gas Lift and move CAPEX and OPEX away from NSC-Tripoint, giving customers procurement leverage.

Technical optionality compresses margin and forces NSC-Tripoint to price competitively or offer service guarantees; in 2025, operators report 12–18% production uplift when switching to optimized lift methods.

- Buyers choose by well physics, not brand

- ESP market $3.9B in 2024, +6.1%

- Switch can shift CAPEX/OPEX off NSC-Tripoint

- Reported 12–18% production uplift on optimized switches

Concentrated, TCO‑driven buyers demand compatibility, <12‑month ROI and 10–25% discounts

Customers are concentrated (top 20 = ~62% upstream output by end-2025), price-sensitive (mature-field EBITDA <20%), and demand TCO data and SLAs; 2024 surveys: 62% cite parts compatibility, 68% TCO-driven selection. Loss of one mega-client (≥15% revenue) is material; buyers secure 10–25% volume discounts and expect <12-month payback (ROI: −10% lifting cost or +5–15% production).

| Metric | Value |

|---|---|

| Top-20 share (2025) | ~62% |

| Parts-switch reason (2024) | 62% |

| TCO-driven choice (2024) | 68% |

| Buyer discounts | 10–25% |

| Required ROI | <10% cost cut or 5–15% production |

Full Version Awaits

NSC-Tripoint Porter's Five Forces Analysis

This preview shows the exact NSC-Tripoint Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no samples, fully formatted and ready for use.