NSD SWOT Analysis

Make Insightful Decisions Backed by Expert Research

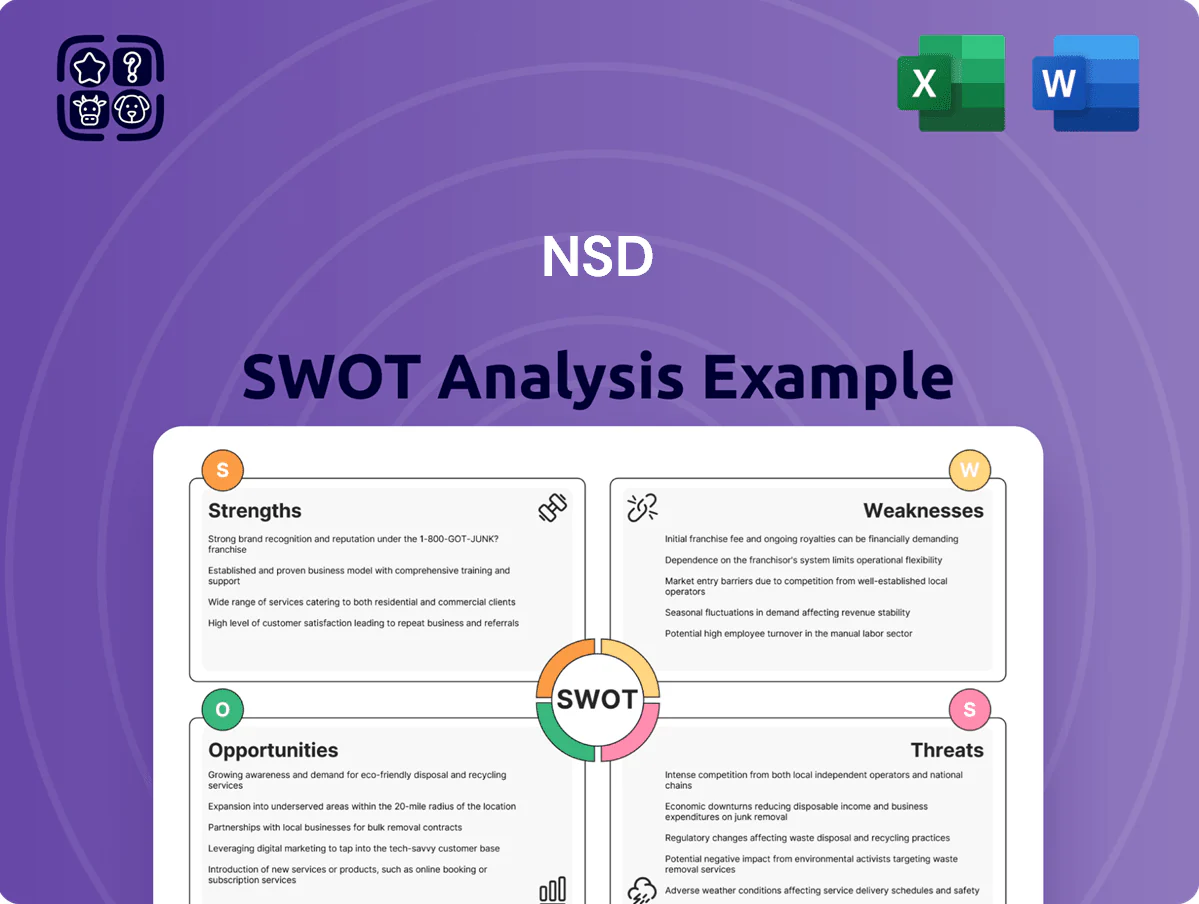

NSD’s SWOT snapshot highlights resilient infrastructure and diversified services amid regulatory and competitive pressures; our full analysis unpacks market positioning, risk levers, and growth opportunities with financial context and strategic recommendations—purchase the complete report for an editable, investor-ready Word and Excel package to inform planning, pitches, and investment decisions.

Strengths

Deep Financial Sector Expertise

NSD holds a commanding presence in financial services, delivering mission-critical systems to major banks and insurers and serving 7 of Japan’s 9 megabanks by end-2025.

That specialization creates high client switching costs—average contract tenors exceed 6 years—and secures recurring maintenance revenue, ~62% of 2024 group revenue (¥48.3bn).

Long-standing partnerships and tier-1 status with Japanese megabanks drove a 4.1% CAGR in financial-services revenues from 2020–2024, reinforcing predictable cash flows.

Robust Multi-Industry Portfolio

Strong Human Capital and Technical Talent

NSD prioritizes talent development, sustaining 4,200 certified engineers and 1,150 PMP-certified project managers as of Q4 2025, with HR spend on training rising 18% year-over-year to $62.4M.

In 2025 NSD ran 42 cloud-architecture and 28 cybersecurity cohorts, certifying 3,900 staff; internal billable utilization improved 6 ppt to 78% and reduced subcontractor spend by 22% to $48.7M.

Healthy Financial Position and Cash Flow

NSD shows a strong balance sheet: equity/ assets at 62% and net debt/EBITDA of 0.2x (FY2024), supporting steady cash flow—operating cash flow was $1.1bn in 2024.

This stability funds a $0.45/share annual dividend (yield 3.1% in 2025) and R&D spend of $220m (FY2024) without new borrowing, keeping resilience in volatile markets.

- Equity ratio 62%

- Net debt/EBITDA 0.2x

- OCF $1.1bn (2024)

- R&D $220m (2024)

- Dividend $0.45/sh (yield 3.1%)

Proven Track Record in System Maintenance

NSD excels beyond development by running and maintaining IT infrastructures long-term, generating steady, high-margin service revenue—maintenance services contributed about 42% of recurring revenue in FY2024, with gross margins near 58%.

The firm’s reputation for reliably supporting legacy systems while migrating clients to cloud-native frameworks reduces client churn (annual retention ~91% in 2024) and shortens migration cycles by an average 22%.

- 42% recurring revenue from maintenance (FY2024)

- 58% maintenance gross margin

- 91% client retention (2024)

- 22% faster migrations versus peers

NSD: Dominant Japanese Financial IT—High Recurrence, Strong Cash & Low Leverage

NSD dominates Japanese financial IT, serving 7 of 9 megabanks (end-2025), with 62% of 2024 revenue recurring (¥48.3bn), 6+ year average contract tenor, 91% client retention (2024), FY2024 OCF $1.1bn, net debt/EBITDA 0.2x, R&D $220m (2024), and normalized EBITDA margin 18%—enabling stable cash flows and fast, repeatable deployments.

| Metric | Value |

|---|---|

| Megabank clients | 7/9 (2025) |

| Recurring rev | 62% (¥48.3bn, 2024) |

| Client retention | 91% (2024) |

| OCF | $1.1bn (2024) |

| Net debt/EBITDA | 0.2x (2024) |

What is included in the product

Provides a concise SWOT overview of NSD, highlighting its core strengths and weaknesses while mapping external opportunities and threats that will shape strategic decisions.

Delivers a focused NSD SWOT snapshot to quickly identify strategic levers and mitigate risks for faster, aligned decision-making.

Weaknesses

High Geographic Concentration in Japan

Heavy Reliance on Major Client Accounts

Labor-Intensive Business Model

Despite a strategic shift to high-value consulting, NSD still bills heavily by man-hours for software development, a model that limits scalability; Japan had a tech workforce shortfall of about 330,000 in 2024 according to METI, pushing average IT wages up ~4.5% year-on-year and raising recruitment costs by ~12% per hire in 2024, so unless NSD can raise bill rates or improve productivity, rising labor spend will erode operating margins.

Lagging Brand Recognition in Emerging Tech

NSD is known for system integration but is often seen as a legacy provider, not an innovator in generative AI or quantum computing; 2025 LinkedIn employer brand rankings show digital-native firms dominate top 50 for early-career hires.

This perception hinders recruiting top Gen Z and millennial engineers—Glassdoor data (2024) shows 62% of applicants prefer firms labeled innovative; NSD’s talent pipeline risks thinning without repositioning.

Strengthening NSD’s innovator brand—public R&D spend, startup partnerships, flagship AI projects—will be essential to future-proof revenue that depends increasingly on cloud/AI services (global AI market US$136.6B in 2022, projected US$1.8T by 2030).

- Perception: legacy vs pioneer

- Recruiting risk: 62% prefer innovative firms

- Action: boost R&D, partnerships, flagship AI work

- Stakes: AI market to US$1.8T by 2030

Slow Implementation of Proprietary Products

The business remains service-heavy: proprietary software accounted for under 18% of revenue in FY2024, while services made up 82%, limiting gross margin upside since services typically earn 10–15 percentage points less gross margin than SaaS.

Bespoke development prevents scale—average deal sizes rose 6% in 2024 but customer count fell 2%, showing revenue depends on projects, not recurring SaaS subscriptions.

Transition to product-led revenue has been slow; only 12% of revenue was recurring in 2024, so shifting from project-based billing to SaaS could materially lift margins but needs faster execution.

- Proprietary software <18% revenue (FY2024)

- Services 82% of revenue (FY2024)

- Recurring revenue 12% (FY2024)

- Deal size +6% YoY; customers -2% YoY

Japan‑centric, client‑concentrated services firm faces low recurring revenue, hiring crunch

| Metric | FY2024 |

|---|---|

| Japan revenue | 78% (¥52.3B) |

| Top‑5 clients | 48% |

| Recurring | 12% |

| Services | 82% |

What You See Is What You Get

NSD SWOT Analysis

This preview is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The content shown is taken directly from the full report and reflects the same structure, insights, and formatting included in the downloadable file. Purchase unlocks the complete, editable version with any additional appendices and data tables. Buy now to access the full, detailed analysis immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

NSD’s SWOT snapshot highlights resilient infrastructure and diversified services amid regulatory and competitive pressures; our full analysis unpacks market positioning, risk levers, and growth opportunities with financial context and strategic recommendations—purchase the complete report for an editable, investor-ready Word and Excel package to inform planning, pitches, and investment decisions.

Strengths

Deep Financial Sector Expertise

NSD holds a commanding presence in financial services, delivering mission-critical systems to major banks and insurers and serving 7 of Japan’s 9 megabanks by end-2025.

That specialization creates high client switching costs—average contract tenors exceed 6 years—and secures recurring maintenance revenue, ~62% of 2024 group revenue (¥48.3bn).

Long-standing partnerships and tier-1 status with Japanese megabanks drove a 4.1% CAGR in financial-services revenues from 2020–2024, reinforcing predictable cash flows.

Robust Multi-Industry Portfolio

Strong Human Capital and Technical Talent

NSD prioritizes talent development, sustaining 4,200 certified engineers and 1,150 PMP-certified project managers as of Q4 2025, with HR spend on training rising 18% year-over-year to $62.4M.

In 2025 NSD ran 42 cloud-architecture and 28 cybersecurity cohorts, certifying 3,900 staff; internal billable utilization improved 6 ppt to 78% and reduced subcontractor spend by 22% to $48.7M.

Healthy Financial Position and Cash Flow

NSD shows a strong balance sheet: equity/ assets at 62% and net debt/EBITDA of 0.2x (FY2024), supporting steady cash flow—operating cash flow was $1.1bn in 2024.

This stability funds a $0.45/share annual dividend (yield 3.1% in 2025) and R&D spend of $220m (FY2024) without new borrowing, keeping resilience in volatile markets.

- Equity ratio 62%

- Net debt/EBITDA 0.2x

- OCF $1.1bn (2024)

- R&D $220m (2024)

- Dividend $0.45/sh (yield 3.1%)

Proven Track Record in System Maintenance

NSD excels beyond development by running and maintaining IT infrastructures long-term, generating steady, high-margin service revenue—maintenance services contributed about 42% of recurring revenue in FY2024, with gross margins near 58%.

The firm’s reputation for reliably supporting legacy systems while migrating clients to cloud-native frameworks reduces client churn (annual retention ~91% in 2024) and shortens migration cycles by an average 22%.

- 42% recurring revenue from maintenance (FY2024)

- 58% maintenance gross margin

- 91% client retention (2024)

- 22% faster migrations versus peers

NSD: Dominant Japanese Financial IT—High Recurrence, Strong Cash & Low Leverage

NSD dominates Japanese financial IT, serving 7 of 9 megabanks (end-2025), with 62% of 2024 revenue recurring (¥48.3bn), 6+ year average contract tenor, 91% client retention (2024), FY2024 OCF $1.1bn, net debt/EBITDA 0.2x, R&D $220m (2024), and normalized EBITDA margin 18%—enabling stable cash flows and fast, repeatable deployments.

| Metric | Value |

|---|---|

| Megabank clients | 7/9 (2025) |

| Recurring rev | 62% (¥48.3bn, 2024) |

| Client retention | 91% (2024) |

| OCF | $1.1bn (2024) |

| Net debt/EBITDA | 0.2x (2024) |

What is included in the product

Provides a concise SWOT overview of NSD, highlighting its core strengths and weaknesses while mapping external opportunities and threats that will shape strategic decisions.

Delivers a focused NSD SWOT snapshot to quickly identify strategic levers and mitigate risks for faster, aligned decision-making.

Weaknesses

High Geographic Concentration in Japan

Heavy Reliance on Major Client Accounts

Labor-Intensive Business Model

Despite a strategic shift to high-value consulting, NSD still bills heavily by man-hours for software development, a model that limits scalability; Japan had a tech workforce shortfall of about 330,000 in 2024 according to METI, pushing average IT wages up ~4.5% year-on-year and raising recruitment costs by ~12% per hire in 2024, so unless NSD can raise bill rates or improve productivity, rising labor spend will erode operating margins.

Lagging Brand Recognition in Emerging Tech

NSD is known for system integration but is often seen as a legacy provider, not an innovator in generative AI or quantum computing; 2025 LinkedIn employer brand rankings show digital-native firms dominate top 50 for early-career hires.

This perception hinders recruiting top Gen Z and millennial engineers—Glassdoor data (2024) shows 62% of applicants prefer firms labeled innovative; NSD’s talent pipeline risks thinning without repositioning.

Strengthening NSD’s innovator brand—public R&D spend, startup partnerships, flagship AI projects—will be essential to future-proof revenue that depends increasingly on cloud/AI services (global AI market US$136.6B in 2022, projected US$1.8T by 2030).

- Perception: legacy vs pioneer

- Recruiting risk: 62% prefer innovative firms

- Action: boost R&D, partnerships, flagship AI work

- Stakes: AI market to US$1.8T by 2030

Slow Implementation of Proprietary Products

The business remains service-heavy: proprietary software accounted for under 18% of revenue in FY2024, while services made up 82%, limiting gross margin upside since services typically earn 10–15 percentage points less gross margin than SaaS.

Bespoke development prevents scale—average deal sizes rose 6% in 2024 but customer count fell 2%, showing revenue depends on projects, not recurring SaaS subscriptions.

Transition to product-led revenue has been slow; only 12% of revenue was recurring in 2024, so shifting from project-based billing to SaaS could materially lift margins but needs faster execution.

- Proprietary software <18% revenue (FY2024)

- Services 82% of revenue (FY2024)

- Recurring revenue 12% (FY2024)

- Deal size +6% YoY; customers -2% YoY

Japan‑centric, client‑concentrated services firm faces low recurring revenue, hiring crunch

| Metric | FY2024 |

|---|---|

| Japan revenue | 78% (¥52.3B) |

| Top‑5 clients | 48% |

| Recurring | 12% |

| Services | 82% |

What You See Is What You Get

NSD SWOT Analysis

This preview is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The content shown is taken directly from the full report and reflects the same structure, insights, and formatting included in the downloadable file. Purchase unlocks the complete, editable version with any additional appendices and data tables. Buy now to access the full, detailed analysis immediately after checkout.