Northern Star Porter's Five Forces Analysis

From Overview to Strategy Blueprint

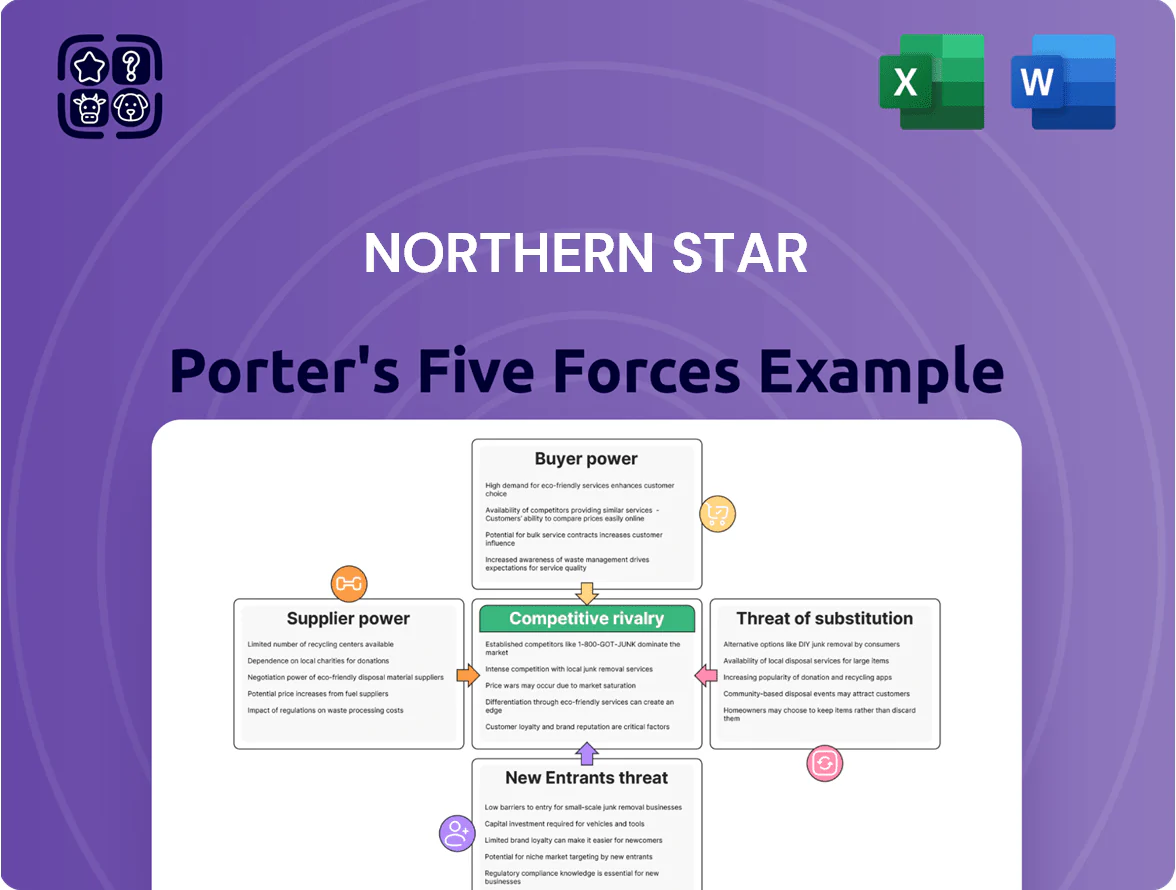

Northern Star faces moderate buyer power and substitution risk, tempered by strong operational scale and high capital intensity that limit new entrants; supplier leverage and regulatory shifts present nuanced vulnerabilities worth monitoring. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Northern Star’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Mining Equipment

The heavy-duty mining machinery market is concentrated: Caterpillar and Komatsu held roughly 45%–55% global share of large mining equipment sales in 2024, so Northern Star relies on a few OEMs for drills and haul trucks, giving suppliers moderate pricing and service leverage. Northern Star’s 2024 capex of ~US$450m and fleet scale secure bulk-purchase discounts of 5%–12%, which partly offsets supplier power.

Energy and Fuel Price Volatility

Mining ops like Kalgoorlie (Australia) and Pogo (Alaska) burn large diesel and grid power; energy can be ~15–25% of cash costs—diesel rose 30% in 2022–23 and global oil shocks keep price risk high.

Northern Star is adding renewables (targeting ~30% site renewables by 2026), but still buys long-term contracts and faces local utility rates; 2024 inflation pushed energy opex up ~8%, squeezing margins.

Scarcity of Skilled Technical Labor

The Australian mining sector reported a 14% shortfall in skilled mining roles in 2024, giving engineers, geologists and heavy-equipment operators strong leverage and raising labor hire rates ~18% year-over-year; this scarcity boosts suppliers’ bargaining power versus miners like Northern Star.

Northern Star faces wage-cost pressure—labour and contractor spend rose ~12% in 2024—and must fund retention, apprenticeships and upskilling; expect multi‑million AUD annual training budgets to keep production steady.

Consolidation of Mining Service Providers

- Top-5 providers ≈65% market share (2025)

- Single-vendor exposure <30% of annual spend (FY2024)

- In-house teams for key underground works

Environmental and Regulatory Compliance Services

As ESG mandates tighten by late 2025, demand for specialized environmental consultancy and carbon-offset services has jumped, with global ESG-related compliance spending projected up 18% in 2024–25 to about $52 billion (Verdant Insights, 2025).

Niche providers exert power: their certifications are required for Northern Star to keep its social license to operate, and only ~6 firms globally can audit large-scale gold operations, boosting supplier leverage and pricing power.

- ESG compliance spend +18% to $52B (2024–25)

- ~6 reputable global auditors for large gold ops

- Certifications mandatory for social license

- Higher fees and switching costs for Northern Star

Northern Star supplier squeeze: concentrated OEMs, rising energy, labour and ESG costs

Northern Star faces moderate–high supplier power: 2 OEMs held 45%–55% market share (2024), capex ~US$450m gave 5%–12% bulk discounts, but energy (15%–25% cash cost) and diesel volatility +30% (2022–23) raise exposure; labour shortages (14% shortfall) lifted hire rates ~18% (2024) and top-5 contractors now ≈65% market share (2025), while ESG auditors (~6 global) command premium fees.

| Metric | Value |

|---|---|

| OEM share (2024) | 45%–55% |

| Capex (2024) | US$450m |

| Bulk discounts | 5%–12% |

| Energy % cash cost | 15%–25% |

| Diesel change (2022–23) | +30% |

| Labour shortfall (Aus, 2024) | 14% |

| Hire rate rise (2024) | +18% |

| Top-5 contractors (2025) | ≈65% |

| ESG auditors (global) | ~6 firms |

What is included in the product

Uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitute threats, and rivalry intensity specific to Northern Star, with strategic insights on vulnerabilities and defensive opportunities.

A concise Porter's Five Forces one-sheet tailored to Northern Star—instantly highlights competitive pressures and strategic levers for faster, confident decision-making.

Customers Bargaining Power

Gold as a Global Commodity

Northern Star sells gold, a standardized commodity traded on exchanges such as the London Bullion Market Association (LBMA) and New York COMEX, where spot gold averaged about 2,030 USD/oz in 2025 YTD (Jan–Dec 2025 consensus). Because global supply-demand sets price, individual buyers cannot negotiate below the prevailing market rate, keeping customer bargaining power low. Gold’s perfect liquidity and universal pricing mean Northern Star faces price-takers, not price-makers.

Fragmented Global Buyer Base

The global buyer base for gold is highly fragmented—central banks, ETFs and institutional investors, jewelry makers, and tech firms together drove demand of about 4,200 tonnes in 2024 per World Gold Council—so no single customer can push Northern Star Resources to cut prices.

Lack of Product Differentiation

Because traded gold bullion must meet LBMA (London Bullion Market Association) purity standards, Northern Star Resources cannot differentiate bars for buyers, so it lacks pricing power and cannot charge a premium.

That said, buyers also cannot push for bespoke specs that raise production costs, keeping Northern Star's AIS (all-in sustaining) cost per ounce—US$1,180 in FY2024—stable.

The standardized output speeds sales and reduces negotiation levers, limiting buyer bargaining despite gold's spot price volatility (average 2024 spot ~US$2,100/oz).

High Liquidity and Immediate Settlement

The gold market had average daily trading volume of about $140 billion in 2024, letting Northern Star convert gold to cash almost instantly at spot prices; this liquidity frees the company from buyer-specific payment terms and credit cycles.

Selling into a deep, transparent market—LBMA cleared bars and exchange-traded venues—means no single purchaser can exert meaningful price or contractual pressure on Northern Star, effectively nullifying customer bargaining power.

- Avg daily gold volume ~$140B (2024)

- Spot market pricing, immediate settlement

- No dependence on single buyers or credit terms

- LBMA/exchange liquidity reduces buyer leverage

Role of Central Bank Demand

Central banks remained net buyers in 2025, adding about 400 tonnes through Q3 (World Gold Council), which lifts baseline demand and limits downside price pressure for major producers like Northern Star.

These institutions value supply security and scale over small price cuts, so their purchases reduce customer bargaining leverage and support long-term contract volumes.

- ~400 tonnes net buy YTD 2025

- Institutional demand raises demand floor

- Favors large producers with secure supply

Northern Star: Low buyer leverage as gold liquidity, central bank demand lift prices

Northern Star faces low customer bargaining power: gold is a standardized, highly liquid commodity priced on LBMA/COMEX (avg spot ~US$2,030/oz 2025 YTD), with global demand ~4,200t (2024) and avg daily trading ~$140B (2024); AIS cost US$1,180/oz FY2024 limits buyer leverage; central banks added ~400t YTD 2025, supporting demand.

| Metric | Value |

|---|---|

| Spot price (2025 YTD) | US$2,030/oz |

| Avg daily volume (2024) | $140B |

| Global demand (2024) | 4,200 tonnes |

| Northern Star AIS (FY2024) | US$1,180/oz |

| Central bank net buys (2025 YTD) | ~400 tonnes |

Preview the Actual Deliverable

Northern Star Porter's Five Forces Analysis

This preview shows the exact Northern Star Porter's Five Forces analysis you'll receive instantly after purchase—no placeholders, no mockups.

The document displayed here is the professionally written, fully formatted file ready for download and use the moment you buy; what you see is what you get.

No samples or excerpts—this is the final deliverable, provided complete and ready for immediate application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Northern Star faces moderate buyer power and substitution risk, tempered by strong operational scale and high capital intensity that limit new entrants; supplier leverage and regulatory shifts present nuanced vulnerabilities worth monitoring. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Northern Star’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Mining Equipment

The heavy-duty mining machinery market is concentrated: Caterpillar and Komatsu held roughly 45%–55% global share of large mining equipment sales in 2024, so Northern Star relies on a few OEMs for drills and haul trucks, giving suppliers moderate pricing and service leverage. Northern Star’s 2024 capex of ~US$450m and fleet scale secure bulk-purchase discounts of 5%–12%, which partly offsets supplier power.

Energy and Fuel Price Volatility

Mining ops like Kalgoorlie (Australia) and Pogo (Alaska) burn large diesel and grid power; energy can be ~15–25% of cash costs—diesel rose 30% in 2022–23 and global oil shocks keep price risk high.

Northern Star is adding renewables (targeting ~30% site renewables by 2026), but still buys long-term contracts and faces local utility rates; 2024 inflation pushed energy opex up ~8%, squeezing margins.

Scarcity of Skilled Technical Labor

The Australian mining sector reported a 14% shortfall in skilled mining roles in 2024, giving engineers, geologists and heavy-equipment operators strong leverage and raising labor hire rates ~18% year-over-year; this scarcity boosts suppliers’ bargaining power versus miners like Northern Star.

Northern Star faces wage-cost pressure—labour and contractor spend rose ~12% in 2024—and must fund retention, apprenticeships and upskilling; expect multi‑million AUD annual training budgets to keep production steady.

Consolidation of Mining Service Providers

- Top-5 providers ≈65% market share (2025)

- Single-vendor exposure <30% of annual spend (FY2024)

- In-house teams for key underground works

Environmental and Regulatory Compliance Services

As ESG mandates tighten by late 2025, demand for specialized environmental consultancy and carbon-offset services has jumped, with global ESG-related compliance spending projected up 18% in 2024–25 to about $52 billion (Verdant Insights, 2025).

Niche providers exert power: their certifications are required for Northern Star to keep its social license to operate, and only ~6 firms globally can audit large-scale gold operations, boosting supplier leverage and pricing power.

- ESG compliance spend +18% to $52B (2024–25)

- ~6 reputable global auditors for large gold ops

- Certifications mandatory for social license

- Higher fees and switching costs for Northern Star

Northern Star supplier squeeze: concentrated OEMs, rising energy, labour and ESG costs

Northern Star faces moderate–high supplier power: 2 OEMs held 45%–55% market share (2024), capex ~US$450m gave 5%–12% bulk discounts, but energy (15%–25% cash cost) and diesel volatility +30% (2022–23) raise exposure; labour shortages (14% shortfall) lifted hire rates ~18% (2024) and top-5 contractors now ≈65% market share (2025), while ESG auditors (~6 global) command premium fees.

| Metric | Value |

|---|---|

| OEM share (2024) | 45%–55% |

| Capex (2024) | US$450m |

| Bulk discounts | 5%–12% |

| Energy % cash cost | 15%–25% |

| Diesel change (2022–23) | +30% |

| Labour shortfall (Aus, 2024) | 14% |

| Hire rate rise (2024) | +18% |

| Top-5 contractors (2025) | ≈65% |

| ESG auditors (global) | ~6 firms |

What is included in the product

Uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitute threats, and rivalry intensity specific to Northern Star, with strategic insights on vulnerabilities and defensive opportunities.

A concise Porter's Five Forces one-sheet tailored to Northern Star—instantly highlights competitive pressures and strategic levers for faster, confident decision-making.

Customers Bargaining Power

Gold as a Global Commodity

Northern Star sells gold, a standardized commodity traded on exchanges such as the London Bullion Market Association (LBMA) and New York COMEX, where spot gold averaged about 2,030 USD/oz in 2025 YTD (Jan–Dec 2025 consensus). Because global supply-demand sets price, individual buyers cannot negotiate below the prevailing market rate, keeping customer bargaining power low. Gold’s perfect liquidity and universal pricing mean Northern Star faces price-takers, not price-makers.

Fragmented Global Buyer Base

The global buyer base for gold is highly fragmented—central banks, ETFs and institutional investors, jewelry makers, and tech firms together drove demand of about 4,200 tonnes in 2024 per World Gold Council—so no single customer can push Northern Star Resources to cut prices.

Lack of Product Differentiation

Because traded gold bullion must meet LBMA (London Bullion Market Association) purity standards, Northern Star Resources cannot differentiate bars for buyers, so it lacks pricing power and cannot charge a premium.

That said, buyers also cannot push for bespoke specs that raise production costs, keeping Northern Star's AIS (all-in sustaining) cost per ounce—US$1,180 in FY2024—stable.

The standardized output speeds sales and reduces negotiation levers, limiting buyer bargaining despite gold's spot price volatility (average 2024 spot ~US$2,100/oz).

High Liquidity and Immediate Settlement

The gold market had average daily trading volume of about $140 billion in 2024, letting Northern Star convert gold to cash almost instantly at spot prices; this liquidity frees the company from buyer-specific payment terms and credit cycles.

Selling into a deep, transparent market—LBMA cleared bars and exchange-traded venues—means no single purchaser can exert meaningful price or contractual pressure on Northern Star, effectively nullifying customer bargaining power.

- Avg daily gold volume ~$140B (2024)

- Spot market pricing, immediate settlement

- No dependence on single buyers or credit terms

- LBMA/exchange liquidity reduces buyer leverage

Role of Central Bank Demand

Central banks remained net buyers in 2025, adding about 400 tonnes through Q3 (World Gold Council), which lifts baseline demand and limits downside price pressure for major producers like Northern Star.

These institutions value supply security and scale over small price cuts, so their purchases reduce customer bargaining leverage and support long-term contract volumes.

- ~400 tonnes net buy YTD 2025

- Institutional demand raises demand floor

- Favors large producers with secure supply

Northern Star: Low buyer leverage as gold liquidity, central bank demand lift prices

Northern Star faces low customer bargaining power: gold is a standardized, highly liquid commodity priced on LBMA/COMEX (avg spot ~US$2,030/oz 2025 YTD), with global demand ~4,200t (2024) and avg daily trading ~$140B (2024); AIS cost US$1,180/oz FY2024 limits buyer leverage; central banks added ~400t YTD 2025, supporting demand.

| Metric | Value |

|---|---|

| Spot price (2025 YTD) | US$2,030/oz |

| Avg daily volume (2024) | $140B |

| Global demand (2024) | 4,200 tonnes |

| Northern Star AIS (FY2024) | US$1,180/oz |

| Central bank net buys (2025 YTD) | ~400 tonnes |

Preview the Actual Deliverable

Northern Star Porter's Five Forces Analysis

This preview shows the exact Northern Star Porter's Five Forces analysis you'll receive instantly after purchase—no placeholders, no mockups.

The document displayed here is the professionally written, fully formatted file ready for download and use the moment you buy; what you see is what you get.

No samples or excerpts—this is the final deliverable, provided complete and ready for immediate application.