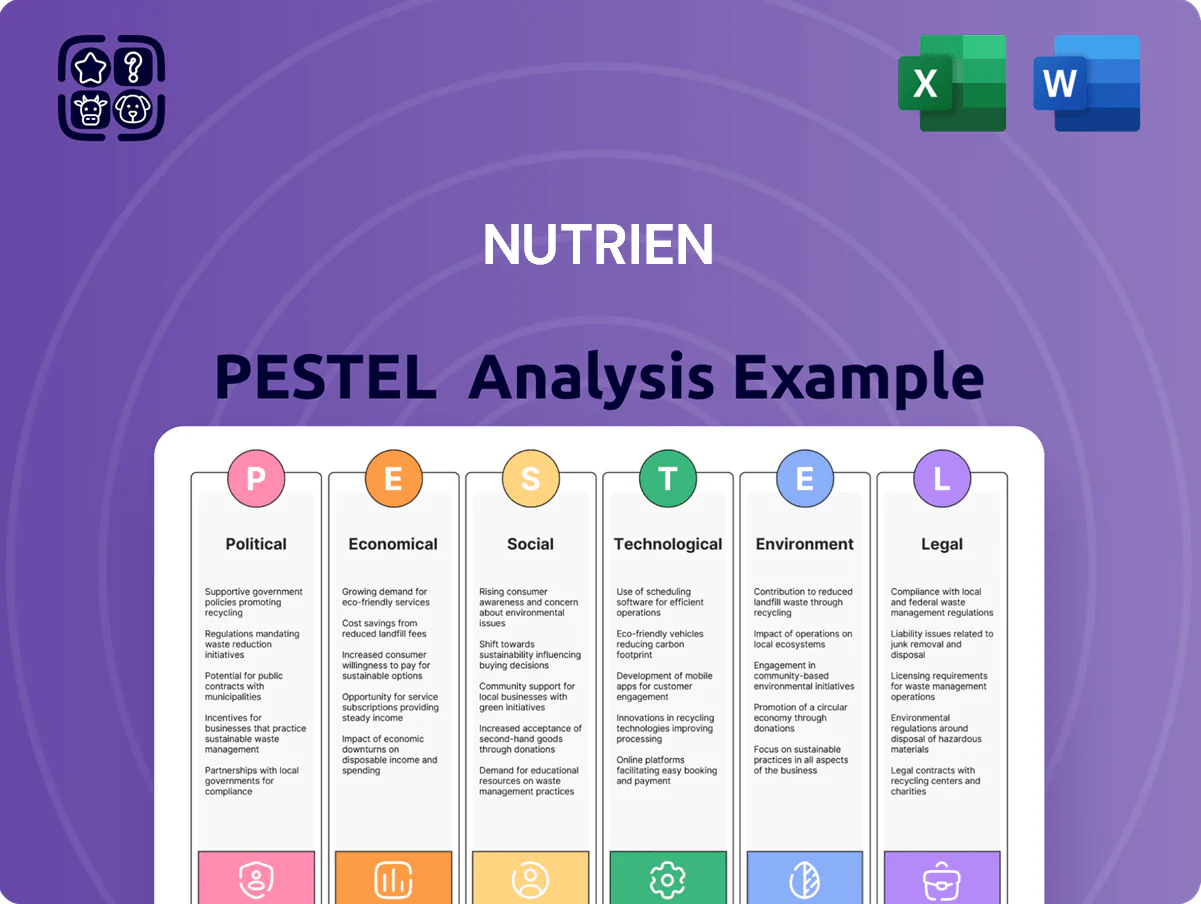

Nutrien PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our targeted PESTLE Analysis of Nutrien—spot regulatory risks, market drivers, and technological shifts shaping its fertilizer leadership and margins.

Perfect for investors and strategists, this concise, fully editable report delivers actionable insights you can use immediately—purchase the full version to access the complete deep-dive and supporting data.

Political factors

Geopolitical Potash Supply Dynamics

Geopolitical instability in Eastern Europe and sanctions on Belarus and Russia have tightened global potash supplies, pushing 2024–2025 seaborne potash premiums up over 25% and elevating market volatility. Nutrien, as a North American supplier accounting for roughly 18% of global potash capacity, gains pricing power and reliability advantages. Ongoing diplomatic shifts require continual monitoring to protect Nutrien’s market share and support global food security.

Global Food Security Policies

Governments are boosting food sovereignty: 72 countries expanded domestic agri-support in 2022–2024, driving higher fertilizer demand; global fertilizer consumption rose 3.5% in 2023 to ~193 Mt, favoring Nutrien’s integrated retail and production model that reported CA$22.6B revenue in FY2024.

However, political shifts prompt risks—since 2021 over a dozen major exporters imposed export curbs or stockpile policies, disrupting trade flows and pressuring Nutrien’s international distribution and pricing strategies.

Agricultural Subsidy Frameworks

The financial health of Nutrien’s core customers is tied to subsidy programs in the US, Canada and Brazil, where farm supports totalled roughly US$70–90 billion annually (2024 OECD/USDA estimates), directly affecting fertilizer and seed demand. Changes in US farm bills or Canada’s AgriStability can swing farmer purchasing power for high‑value inputs by 10–20% seasonally. Political debates in 2025 over climate‑linked subsidies have shifted budgets toward sustainable inputs, lifting Nutrien’s specialty product sales by mid‑single digits.

Trade Tariffs and Export Restrictions

Trade tensions and retaliatory tariffs—e.g., 2023–2024 tariffs that altered North American soybean flows by ~6–8%—can shift global crop choices and fertilizer demand, affecting Nutrien’s potash and nitrogen volumes.

Complex trade agreements and protectionist moves raise import costs for raw materials; Nutrien’s 2024 supply-chain expenses rose ~4% YoY, underscoring exposure.

Political barriers force flexible logistics and localized retail: Nutrien’s 2024 retail footprint in 12 countries helps hedge regional risk.

- Tariff-driven crop shifts change fertilizer mix and volumes

- 2024 supply-chain costs +4% YoY, increasing margin pressure

- Localized retail in 12 countries supports regional mitigation

Regulatory Stability in North America

Nutrien operates mainly in Canada and the US, where political stability supports long-term capital investments; Canada accounted for about 35% of 2024 revenue and the US ~40% (2024 annual report), providing predictable permitting and infrastructure frameworks.

Both governments broadly support resource extraction and large-scale agri-manufacturing, but tightening environmental mandates (e.g., Canada’s 2030 emissions targets, US state-level fertilizer regulations) require active government relations.

Maintaining strong regional policymaker ties is critical to secure permits, pipeline and rail access, and public funding for infrastructure supporting Nutrien’s FY2024 CAPEX of roughly US$1.8 billion.

- Stable jurisdictions: Canada/US = ~75% revenue (2024)

- FY2024 CAPEX ~US$1.8B

- Rising environmental mandates = regulatory risk

- Policy engagement essential for permits/infrastructure

Nutrien rides >25% seaborne potash premium as export curbs heighten market risks

Geopolitical supply shocks raised seaborne potash premiums >25% (2024–25); Nutrien holds ~18% global potash capacity and CA$22.6B FY2024 revenue, gaining pricing leverage. Global fertilizer use ~193 Mt (2023), up 3.5%; 72 countries increased agri-support (2022–24). Export curbs by 12+ exporters since 2021 and 2024 supply‑chain costs +4% YoY heighten trade and margin risks.

| Metric | Value |

|---|---|

| Nutrien FY2024 revenue | CA$22.6B |

| Global potash capacity share | ~18% |

| Global fertilizer consumption (2023) | ~193 Mt (+3.5%) |

| Seaborne potash premium change (2024–25) | +>25% |

| Supply‑chain costs YoY (2024) | +4% |

What is included in the product

Explores how macro-environmental forces uniquely affect Nutrien across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and regional market context to identify risks and opportunities for executives, investors, and strategists.

Provides a clean, summarized Nutrien PESTLE that’s visually segmented by category for quick interpretation, easily dropped into presentations or shared across teams to support risk discussions and strategic planning.

Economic factors

Fertilizer Commodity Price Volatility

Fertilizer profitability for Nutrien closely tracks global potash, nitrogen and phosphate prices, which saw 2024-25 volatility—potash averaged about US$360/tonne in 2024 versus peaks near US$450/tonne in 2023—driven by cyclical demand and supply shifts.

By end-2025 investors remain focused on price stability as new production (notably expanded potash capacity in Canada and Belarus post-sanctions adjustments) and slowing grain prices temper margins.

Nutrien mitigates commodity swings via a diversified mix—2024 retail sales accounted for roughly 60% of EBITDA—plus a 2,000-strong retail network that smooths margins relative to wholesale manufacturing exposure.

Natural Gas Input Costs

Nutrien's nitrogen margins are highly tied to natural gas, which accounted for roughly 60-70% of feedstock costs for ammonia in 2024; North American shale gas at ~$3–4/MMBtu that year supported lower per-ton production costs versus global averages near $8–10/MMBtu during 2022–24 spikes.

Global price volatility can erode export competitiveness when spot gas rises; Nutrien reported locking ~30–40% of its energy needs under long-term contracts by 2024 to stabilize costs.

Investments in high-efficiency Haber-Bosch units and ongoing electrification pilots aim to cut energy intensity, underpinning 2025 EBITDA sensitivity to average gas prices per MMBtu and fixed-rate hedges.

Global Interest Rate Environment

As a capital-intensive firm, Nutrien faces higher borrowing costs when global policy rates rise; the US Federal Reserve's policy rate peaking near 5.25–5.50% in 2023–2024 raised average corporate borrowing spreads, increasing project financing costs for 2024 capex of about US$1.1–1.3bn.

Higher rates also tighten farm financing: Canadian and US farm loan rates moved roughly 200–300bps higher vs. 2021, which can reduce farmer spending on premium seeds and crop protection, pressuring Nutrien's retail volumes.

The market expectation of a more stabilized global rate environment by late 2025—implied by futures showing rate cuts beginning H2 2025—shapes Nutrien's capital allocation and M&A timing decisions.

Emerging Market Currency Exposure

Nutrien’s large footprint in Brazil exposes it to FX volatility: a 10% USD appreciation vs BRL cut reported Brazilian revenue and can lower local farmers’ purchasing power; in 2024 Brazil accounted for about 12% of Nutrien’s retail volumes.

When USD strengthens, import costs rise—urea and potash local prices jumped ~15% in 2023–24—potentially reducing fertilizer demand.

Robust hedging, local currency pricing and procurement, and pass-through mechanisms are critical to protect margins and stabilize earnings.

- Brazil ~12% of retail volumes (2024)

- USD up 10% vs BRL reduces reported revenue materially

- Fertilizer local price swings ~15% in 2023–24

- Hedging and localized pricing mitigate FX risk

Farm Income and Credit Availability

Farm income and credit availability drive Nutrien's addressable market; 2024 global grain stocks-to-use fell to about 110% supporting higher prices and farm EBITDA margins—U.S. net farm income estimated at $141 billion in 2024, up from $120 billion in 2023, bolstering fertilizer demand.

High grain and oilseed demand through 2025 encourages investment in yield-enhancing inputs, but rising input costs and tighter ag credit—U.S. Farm Service Agency lending up ~6% in 2024—mean farmer balance-sheet management will shape Nutrien's sales.

- 2024 U.S. net farm income ~ $141B

- Global stocks-to-use ~110% in 2024

- FSA lending +6% in 2024

- Farmer balance-sheet focus through end-2025 affects input spend

Fertilizer margins driven by potash, gas & FX; farm income supports demand

Fertilizer margins hinge on commodity and gas prices: potash ~US$360/t (2024), N costs tied to gas ~$3–4/MMBtu (NA, 2024) vs global ~$8–10; retail ≈60% EBITDA (2024). Higher rates (Fed ~5.25–5.50% peak 2023–24) raised capex cost (2024 capex US$1.1–1.3bn). FX exposure: Brazil ~12% retail (2024); USD↑10% cuts reported revenue. Farm income supportive: US net farm income ≈$141B (2024).

| Metric | 2024 |

|---|---|

| Potash price | ~US$360/t |

| Gas (NA) | $3–4/MMBtu |

| Retail % EBITDA | ~60% |

| Brazil share | ~12% |

| US net farm income | $141B |

What You See Is What You Get

Nutrien PESTLE Analysis

The preview shown here is the exact Nutrien PESTLE document you’ll receive after purchase—fully formatted and ready to use.

No placeholders or teasers: the layout, content, and structure visible are exactly what you’ll download immediately after buying.

This is the real, finished file—professionally structured and ready for immediate application in your analysis or presentations.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our targeted PESTLE Analysis of Nutrien—spot regulatory risks, market drivers, and technological shifts shaping its fertilizer leadership and margins.

Perfect for investors and strategists, this concise, fully editable report delivers actionable insights you can use immediately—purchase the full version to access the complete deep-dive and supporting data.

Political factors

Geopolitical Potash Supply Dynamics

Geopolitical instability in Eastern Europe and sanctions on Belarus and Russia have tightened global potash supplies, pushing 2024–2025 seaborne potash premiums up over 25% and elevating market volatility. Nutrien, as a North American supplier accounting for roughly 18% of global potash capacity, gains pricing power and reliability advantages. Ongoing diplomatic shifts require continual monitoring to protect Nutrien’s market share and support global food security.

Global Food Security Policies

Governments are boosting food sovereignty: 72 countries expanded domestic agri-support in 2022–2024, driving higher fertilizer demand; global fertilizer consumption rose 3.5% in 2023 to ~193 Mt, favoring Nutrien’s integrated retail and production model that reported CA$22.6B revenue in FY2024.

However, political shifts prompt risks—since 2021 over a dozen major exporters imposed export curbs or stockpile policies, disrupting trade flows and pressuring Nutrien’s international distribution and pricing strategies.

Agricultural Subsidy Frameworks

The financial health of Nutrien’s core customers is tied to subsidy programs in the US, Canada and Brazil, where farm supports totalled roughly US$70–90 billion annually (2024 OECD/USDA estimates), directly affecting fertilizer and seed demand. Changes in US farm bills or Canada’s AgriStability can swing farmer purchasing power for high‑value inputs by 10–20% seasonally. Political debates in 2025 over climate‑linked subsidies have shifted budgets toward sustainable inputs, lifting Nutrien’s specialty product sales by mid‑single digits.

Trade Tariffs and Export Restrictions

Trade tensions and retaliatory tariffs—e.g., 2023–2024 tariffs that altered North American soybean flows by ~6–8%—can shift global crop choices and fertilizer demand, affecting Nutrien’s potash and nitrogen volumes.

Complex trade agreements and protectionist moves raise import costs for raw materials; Nutrien’s 2024 supply-chain expenses rose ~4% YoY, underscoring exposure.

Political barriers force flexible logistics and localized retail: Nutrien’s 2024 retail footprint in 12 countries helps hedge regional risk.

- Tariff-driven crop shifts change fertilizer mix and volumes

- 2024 supply-chain costs +4% YoY, increasing margin pressure

- Localized retail in 12 countries supports regional mitigation

Regulatory Stability in North America

Nutrien operates mainly in Canada and the US, where political stability supports long-term capital investments; Canada accounted for about 35% of 2024 revenue and the US ~40% (2024 annual report), providing predictable permitting and infrastructure frameworks.

Both governments broadly support resource extraction and large-scale agri-manufacturing, but tightening environmental mandates (e.g., Canada’s 2030 emissions targets, US state-level fertilizer regulations) require active government relations.

Maintaining strong regional policymaker ties is critical to secure permits, pipeline and rail access, and public funding for infrastructure supporting Nutrien’s FY2024 CAPEX of roughly US$1.8 billion.

- Stable jurisdictions: Canada/US = ~75% revenue (2024)

- FY2024 CAPEX ~US$1.8B

- Rising environmental mandates = regulatory risk

- Policy engagement essential for permits/infrastructure

Nutrien rides >25% seaborne potash premium as export curbs heighten market risks

Geopolitical supply shocks raised seaborne potash premiums >25% (2024–25); Nutrien holds ~18% global potash capacity and CA$22.6B FY2024 revenue, gaining pricing leverage. Global fertilizer use ~193 Mt (2023), up 3.5%; 72 countries increased agri-support (2022–24). Export curbs by 12+ exporters since 2021 and 2024 supply‑chain costs +4% YoY heighten trade and margin risks.

| Metric | Value |

|---|---|

| Nutrien FY2024 revenue | CA$22.6B |

| Global potash capacity share | ~18% |

| Global fertilizer consumption (2023) | ~193 Mt (+3.5%) |

| Seaborne potash premium change (2024–25) | +>25% |

| Supply‑chain costs YoY (2024) | +4% |

What is included in the product

Explores how macro-environmental forces uniquely affect Nutrien across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and regional market context to identify risks and opportunities for executives, investors, and strategists.

Provides a clean, summarized Nutrien PESTLE that’s visually segmented by category for quick interpretation, easily dropped into presentations or shared across teams to support risk discussions and strategic planning.

Economic factors

Fertilizer Commodity Price Volatility

Fertilizer profitability for Nutrien closely tracks global potash, nitrogen and phosphate prices, which saw 2024-25 volatility—potash averaged about US$360/tonne in 2024 versus peaks near US$450/tonne in 2023—driven by cyclical demand and supply shifts.

By end-2025 investors remain focused on price stability as new production (notably expanded potash capacity in Canada and Belarus post-sanctions adjustments) and slowing grain prices temper margins.

Nutrien mitigates commodity swings via a diversified mix—2024 retail sales accounted for roughly 60% of EBITDA—plus a 2,000-strong retail network that smooths margins relative to wholesale manufacturing exposure.

Natural Gas Input Costs

Nutrien's nitrogen margins are highly tied to natural gas, which accounted for roughly 60-70% of feedstock costs for ammonia in 2024; North American shale gas at ~$3–4/MMBtu that year supported lower per-ton production costs versus global averages near $8–10/MMBtu during 2022–24 spikes.

Global price volatility can erode export competitiveness when spot gas rises; Nutrien reported locking ~30–40% of its energy needs under long-term contracts by 2024 to stabilize costs.

Investments in high-efficiency Haber-Bosch units and ongoing electrification pilots aim to cut energy intensity, underpinning 2025 EBITDA sensitivity to average gas prices per MMBtu and fixed-rate hedges.

Global Interest Rate Environment

As a capital-intensive firm, Nutrien faces higher borrowing costs when global policy rates rise; the US Federal Reserve's policy rate peaking near 5.25–5.50% in 2023–2024 raised average corporate borrowing spreads, increasing project financing costs for 2024 capex of about US$1.1–1.3bn.

Higher rates also tighten farm financing: Canadian and US farm loan rates moved roughly 200–300bps higher vs. 2021, which can reduce farmer spending on premium seeds and crop protection, pressuring Nutrien's retail volumes.

The market expectation of a more stabilized global rate environment by late 2025—implied by futures showing rate cuts beginning H2 2025—shapes Nutrien's capital allocation and M&A timing decisions.

Emerging Market Currency Exposure

Nutrien’s large footprint in Brazil exposes it to FX volatility: a 10% USD appreciation vs BRL cut reported Brazilian revenue and can lower local farmers’ purchasing power; in 2024 Brazil accounted for about 12% of Nutrien’s retail volumes.

When USD strengthens, import costs rise—urea and potash local prices jumped ~15% in 2023–24—potentially reducing fertilizer demand.

Robust hedging, local currency pricing and procurement, and pass-through mechanisms are critical to protect margins and stabilize earnings.

- Brazil ~12% of retail volumes (2024)

- USD up 10% vs BRL reduces reported revenue materially

- Fertilizer local price swings ~15% in 2023–24

- Hedging and localized pricing mitigate FX risk

Farm Income and Credit Availability

Farm income and credit availability drive Nutrien's addressable market; 2024 global grain stocks-to-use fell to about 110% supporting higher prices and farm EBITDA margins—U.S. net farm income estimated at $141 billion in 2024, up from $120 billion in 2023, bolstering fertilizer demand.

High grain and oilseed demand through 2025 encourages investment in yield-enhancing inputs, but rising input costs and tighter ag credit—U.S. Farm Service Agency lending up ~6% in 2024—mean farmer balance-sheet management will shape Nutrien's sales.

- 2024 U.S. net farm income ~ $141B

- Global stocks-to-use ~110% in 2024

- FSA lending +6% in 2024

- Farmer balance-sheet focus through end-2025 affects input spend

Fertilizer margins driven by potash, gas & FX; farm income supports demand

Fertilizer margins hinge on commodity and gas prices: potash ~US$360/t (2024), N costs tied to gas ~$3–4/MMBtu (NA, 2024) vs global ~$8–10; retail ≈60% EBITDA (2024). Higher rates (Fed ~5.25–5.50% peak 2023–24) raised capex cost (2024 capex US$1.1–1.3bn). FX exposure: Brazil ~12% retail (2024); USD↑10% cuts reported revenue. Farm income supportive: US net farm income ≈$141B (2024).

| Metric | 2024 |

|---|---|

| Potash price | ~US$360/t |

| Gas (NA) | $3–4/MMBtu |

| Retail % EBITDA | ~60% |

| Brazil share | ~12% |

| US net farm income | $141B |

What You See Is What You Get

Nutrien PESTLE Analysis

The preview shown here is the exact Nutrien PESTLE document you’ll receive after purchase—fully formatted and ready to use.

No placeholders or teasers: the layout, content, and structure visible are exactly what you’ll download immediately after buying.

This is the real, finished file—professionally structured and ready for immediate application in your analysis or presentations.