NuVista Energy Porter's Five Forces Analysis

Don't Miss the Bigger Picture

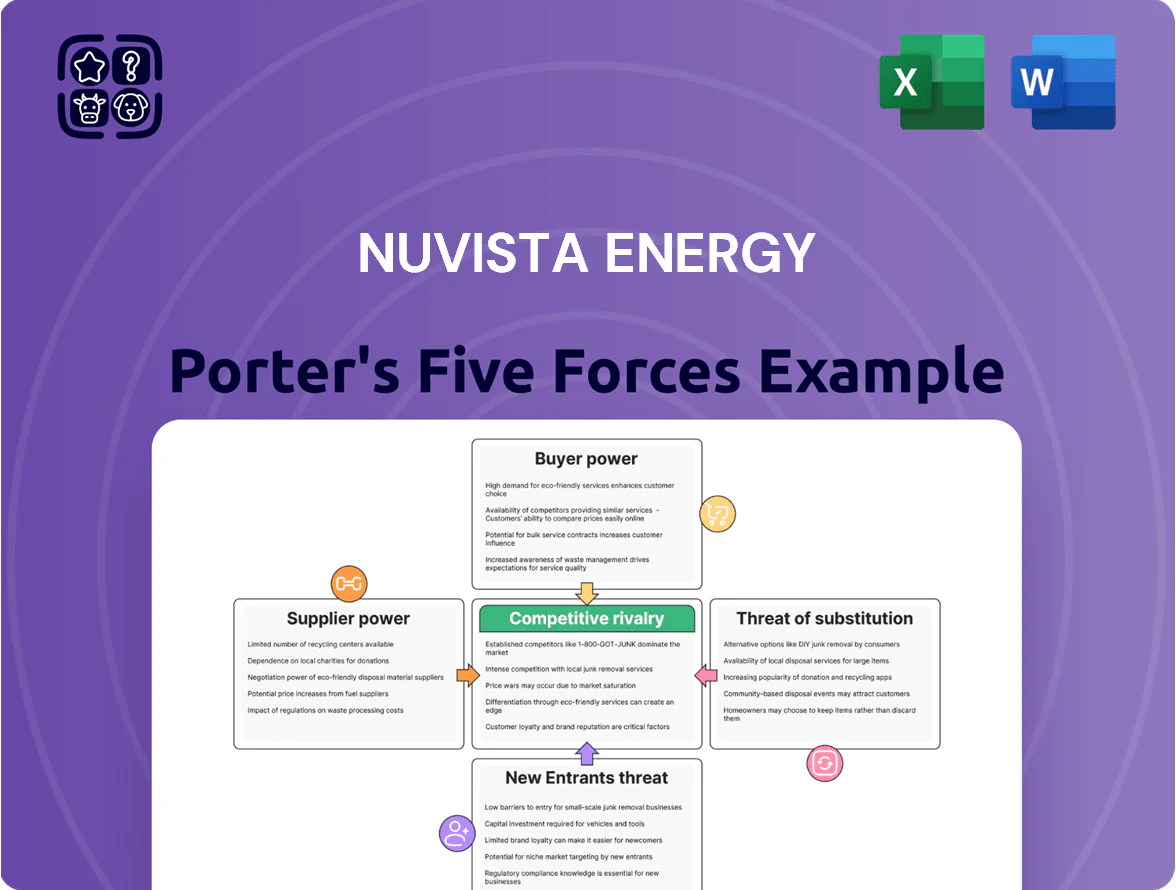

NuVista Energy operates in a capital-intensive, cyclical sector where buyer bargaining, supplier relationships, and regulatory pressures shape margins and growth prospects; this snapshot highlights key competitive tensions and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights that clarify NuVista’s risks and opportunities for investment or strategy.

Suppliers Bargaining Power

Concentration of Oilfield Service Providers

NuVista depends on a small set of specialist oilfield service firms for Montney frac and horizontal-drill rigs; by end-2025 Canadian service firm count fell roughly 30% since 2020, concentrating supply and boosting supplier pricing power.

This concentration let suppliers pass through ~6–8% annual inflation in equipment and labor in 2024–25 and secure longer-term contracts, raising NuVista’s medium-term operating cost risk.

Skilled Labor Shortages in Western Canada

The Alberta Deep Basin’s technical complexity demands experienced engineers and field techs, but Western Canadian Sedimentary Basin shortages mean vacancy rates hit ~6.5% in 2024 for oilfield skilled trades, tightening supply.

Competition from oil & gas and growing geothermal projects pushed average senior engineer wages up ~12% YoY to CAD 150–180k in 2024, raising NuVista’s labor cost risk.

With limited talent, specialized contractors can charge premiums; NuVista likely must raise compensation or invest in training to retain staff and avoid $/boe production delays.

Scarcity of Specialized Drilling Components

Global supply-chain strains in 2025 keep high-grade steel tubulars and frack-specific components scarce; world steel export capacity slipped 4% YoY in 2024 and lead times for premium tubulars average 26–32 weeks, boosting supplier leverage.

Few certified alternatives meet Montney safety and 15,000+ psi pressure specs, so NuVista faces real risk: a 4–8 week delay can defer wells and raise capital costs by roughly CAD 0.5–1.2M per well based on 2024 completion budgets.

Midstream Infrastructure Constraints

Suppliers of midstream services—processing plants and gathering systems—wield strong leverage over NuVista Energy because these assets need billions in capital and are tied to specific basins; for example, Alberta gas processing capacity saw 2024 utilization above 90%, limiting flexibility.

Geographic fixity and scarce spare capacity mean NuVista faces few reroute options if fees rise, and long-term take-or-pay contracts shift cash-flow risk to producers.

- High midstream leverage: >90% Alberta processing utilization (2024)

- Capital intensity: facilities cost hundreds of millions to billions

- Contract risk: take-or-pay terms transfer demand risk to NuVista

Technological Proprietary Software and Data

As NuVista adopts AI-driven reservoir modeling and automated drilling, dependence on third-party tech rises; global oilfield software spend hit about $6.2B in 2024, concentrating vendor leverage.

Vendors use subscription pricing and report 20–30% switching cost equivalents (integration, retraining, data migration), fueling strong bargaining power at renewals.

Proprietary analytics lock data formats and workflows, so switching risks downtime, estimated 4–8 weeks, and potential data loss unless heavy migration spend occurs.

- 2024 oilfield software market ~$6.2B

- Switching cost impact ~20–30% of annual software spend

- Estimated downtime if switching 4–8 weeks

- Subscription models raise renewal leverage

Supplier leverage squeezes wells: higher costs, long lead times, CAD8.2B software lock-in

Suppliers hold strong leverage: concentrated service firms (-30% since 2020), 2024–25 equipment/labor inflation ~6–8% and 12% senior-engineer wage rise to CAD150–180k; tubular lead times 26–32 weeks; Alberta gas processing >90% utilization (2024); 4–8 week delays add CAD0.5–1.2M/well; oilfield software market ~CAD8.2B (2024) with 20–30% switching-cost equivalent.

| Metric | Value |

|---|---|

| Service firm decline | -30% (2020–2025) |

| Equipment/labor inflation | 6–8% (2024–25) |

| Senior engineer pay | CAD150–180k (2024) |

| Tubular lead time | 26–32 weeks (2025) |

| Processing utilization | >90% (Alberta, 2024) |

| Delay cost/well | CAD0.5–1.2M |

| Software market | CAD8.2B (2024) |

| Switching cost | 20–30% |

What is included in the product

Tailored Porter's Five Forces analysis for NuVista Energy, uncovering key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market position.

Concise Porter's Five Forces snapshot for NuVista Energy—instantly highlights competitive pressures and strategic levers to accelerate decision-making.

Customers Bargaining Power

Commodity Price Taker Dynamics

NuVista sells standardized commodities—natural gas, condensate, NGLs—priced off transparent hubs like AECO and NYMEX, leaving it a pure price taker; in 2024 Canada gas averaged C$2.75/GJ at AECO and Henry Hub averaged US$2.95/MMBtu, directly driving revenue.

Customers can switch to other Montney producers with minimal cost, so NuVista has almost no pricing leverage and must compete on cost and reliability.

As a result, NuVista’s topline swings with hub volatility—gas price variance of ±30% in 2023–24 mapped closely to company cash flow and EBITDA sensitivity.

Concentration of Large Scale Industrial Buyers

A significant share of NuVista Energy’s gas (about 40–50% of 2024 production sold) goes to a handful of industrial buyers, utilities, and aggregators, giving them scale to demand price concessions and flexible delivery terms.

These buyers can re-route volumes during Western Canada supply gluts—Alberta wellhead gas averaged C$2.10/GJ in 2024—reducing NuVista’s leverage in long-term contract talks.

Access to Downstream Takeaway Capacity

Customers with firm export-pipeline capacity—often midstream operators or large buyers—can extract concessions from producers; in 2025 roughly 30–40% of Western Canadian gas-export capacity is contracted, so NuVista without transport often must sell at the wellhead or AECO hub to intermediaries at discounts of C$0.50–C$2.00/Mcf.

Refining and Processing Requirements

Buyers of NuVista’s condensate and NGLs—mostly refineries and petrochemical plants—require tight specs for API gravity and sulfur; in 2024 North American condensate refinery takedown rates tightened, raising quality premiums by about US$2–4/bbl.

Because buyers can dock payments for off-spec batches, they push discounts and contract clauses that shift quality risk to producers, compressing NuVista’s realized liquids price versus WTI by an estimated 3–6% in 2024.

- Feedstock specs matter: API, sulfur, BTEX limits

- Price impact: quality premiums US$2–4/bbl (2024)

- Realized discount: ~3–6% vs WTI (2024)

- Contract clauses: docking, penalties, tight delivery windows

Availability of Alternative Supply Sources

Buyers in 2025 face abundant alternatives from the Permian, Marcellus, Montney and other shale plays, with US gas production at ~100 Bcf/d and Canadian gas exports rising 8% YoY, so NuVista cannot reliably command a premium.

High substitutability means purchasers can switch suppliers quickly; if NuVista raises price by >5–10% buyers likely shift to lower-cost producers, keeping bargaining power with buyers.

- North America supply ~100 Bcf/d (2025)

- Canadian gas exports +8% YoY (2024→25)

- Price premium vulnerability >5–10%

Buyers Dictate Pricing: NuVista a Price-Taker; >5–10% Hikes Spur Substitution

Buyers wield strong power: NuVista is a price taker on AECO/NYMEX (2024 AECO C$2.75/GJ, HH US$2.95/MMBtu), 40–50% of volumes to few large buyers, easy supplier switching, and pipeline access shifts leverage; quality discounts trimmed liquids by ~3–6% (2024) and docking penalties raised premiums US$2–4/bbl. Price hikes >5–10% likely trigger buyer substitution.

| Metric | 2024–25 |

|---|---|

| AECO | C$2.75/GJ (2024) |

| Henry Hub | US$2.95/MMBtu (2024) |

| Volumes to big buyers | 40–50% |

| Liquids discount vs WTI | 3–6% |

| Quality premium | US$2–4/bbl |

What You See Is What You Get

NuVista Energy Porter's Five Forces Analysis

This preview shows the exact NuVista Energy Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the part of the full, professionally formatted file you’ll be able to download and use the moment you buy. You’re looking at the actual deliverable; once payment is complete, you’ll get instant access to this exact file. No mockups or samples—what you see is what you get.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

NuVista Energy operates in a capital-intensive, cyclical sector where buyer bargaining, supplier relationships, and regulatory pressures shape margins and growth prospects; this snapshot highlights key competitive tensions and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights that clarify NuVista’s risks and opportunities for investment or strategy.

Suppliers Bargaining Power

Concentration of Oilfield Service Providers

NuVista depends on a small set of specialist oilfield service firms for Montney frac and horizontal-drill rigs; by end-2025 Canadian service firm count fell roughly 30% since 2020, concentrating supply and boosting supplier pricing power.

This concentration let suppliers pass through ~6–8% annual inflation in equipment and labor in 2024–25 and secure longer-term contracts, raising NuVista’s medium-term operating cost risk.

Skilled Labor Shortages in Western Canada

The Alberta Deep Basin’s technical complexity demands experienced engineers and field techs, but Western Canadian Sedimentary Basin shortages mean vacancy rates hit ~6.5% in 2024 for oilfield skilled trades, tightening supply.

Competition from oil & gas and growing geothermal projects pushed average senior engineer wages up ~12% YoY to CAD 150–180k in 2024, raising NuVista’s labor cost risk.

With limited talent, specialized contractors can charge premiums; NuVista likely must raise compensation or invest in training to retain staff and avoid $/boe production delays.

Scarcity of Specialized Drilling Components

Global supply-chain strains in 2025 keep high-grade steel tubulars and frack-specific components scarce; world steel export capacity slipped 4% YoY in 2024 and lead times for premium tubulars average 26–32 weeks, boosting supplier leverage.

Few certified alternatives meet Montney safety and 15,000+ psi pressure specs, so NuVista faces real risk: a 4–8 week delay can defer wells and raise capital costs by roughly CAD 0.5–1.2M per well based on 2024 completion budgets.

Midstream Infrastructure Constraints

Suppliers of midstream services—processing plants and gathering systems—wield strong leverage over NuVista Energy because these assets need billions in capital and are tied to specific basins; for example, Alberta gas processing capacity saw 2024 utilization above 90%, limiting flexibility.

Geographic fixity and scarce spare capacity mean NuVista faces few reroute options if fees rise, and long-term take-or-pay contracts shift cash-flow risk to producers.

- High midstream leverage: >90% Alberta processing utilization (2024)

- Capital intensity: facilities cost hundreds of millions to billions

- Contract risk: take-or-pay terms transfer demand risk to NuVista

Technological Proprietary Software and Data

As NuVista adopts AI-driven reservoir modeling and automated drilling, dependence on third-party tech rises; global oilfield software spend hit about $6.2B in 2024, concentrating vendor leverage.

Vendors use subscription pricing and report 20–30% switching cost equivalents (integration, retraining, data migration), fueling strong bargaining power at renewals.

Proprietary analytics lock data formats and workflows, so switching risks downtime, estimated 4–8 weeks, and potential data loss unless heavy migration spend occurs.

- 2024 oilfield software market ~$6.2B

- Switching cost impact ~20–30% of annual software spend

- Estimated downtime if switching 4–8 weeks

- Subscription models raise renewal leverage

Supplier leverage squeezes wells: higher costs, long lead times, CAD8.2B software lock-in

Suppliers hold strong leverage: concentrated service firms (-30% since 2020), 2024–25 equipment/labor inflation ~6–8% and 12% senior-engineer wage rise to CAD150–180k; tubular lead times 26–32 weeks; Alberta gas processing >90% utilization (2024); 4–8 week delays add CAD0.5–1.2M/well; oilfield software market ~CAD8.2B (2024) with 20–30% switching-cost equivalent.

| Metric | Value |

|---|---|

| Service firm decline | -30% (2020–2025) |

| Equipment/labor inflation | 6–8% (2024–25) |

| Senior engineer pay | CAD150–180k (2024) |

| Tubular lead time | 26–32 weeks (2025) |

| Processing utilization | >90% (Alberta, 2024) |

| Delay cost/well | CAD0.5–1.2M |

| Software market | CAD8.2B (2024) |

| Switching cost | 20–30% |

What is included in the product

Tailored Porter's Five Forces analysis for NuVista Energy, uncovering key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market position.

Concise Porter's Five Forces snapshot for NuVista Energy—instantly highlights competitive pressures and strategic levers to accelerate decision-making.

Customers Bargaining Power

Commodity Price Taker Dynamics

NuVista sells standardized commodities—natural gas, condensate, NGLs—priced off transparent hubs like AECO and NYMEX, leaving it a pure price taker; in 2024 Canada gas averaged C$2.75/GJ at AECO and Henry Hub averaged US$2.95/MMBtu, directly driving revenue.

Customers can switch to other Montney producers with minimal cost, so NuVista has almost no pricing leverage and must compete on cost and reliability.

As a result, NuVista’s topline swings with hub volatility—gas price variance of ±30% in 2023–24 mapped closely to company cash flow and EBITDA sensitivity.

Concentration of Large Scale Industrial Buyers

A significant share of NuVista Energy’s gas (about 40–50% of 2024 production sold) goes to a handful of industrial buyers, utilities, and aggregators, giving them scale to demand price concessions and flexible delivery terms.

These buyers can re-route volumes during Western Canada supply gluts—Alberta wellhead gas averaged C$2.10/GJ in 2024—reducing NuVista’s leverage in long-term contract talks.

Access to Downstream Takeaway Capacity

Customers with firm export-pipeline capacity—often midstream operators or large buyers—can extract concessions from producers; in 2025 roughly 30–40% of Western Canadian gas-export capacity is contracted, so NuVista without transport often must sell at the wellhead or AECO hub to intermediaries at discounts of C$0.50–C$2.00/Mcf.

Refining and Processing Requirements

Buyers of NuVista’s condensate and NGLs—mostly refineries and petrochemical plants—require tight specs for API gravity and sulfur; in 2024 North American condensate refinery takedown rates tightened, raising quality premiums by about US$2–4/bbl.

Because buyers can dock payments for off-spec batches, they push discounts and contract clauses that shift quality risk to producers, compressing NuVista’s realized liquids price versus WTI by an estimated 3–6% in 2024.

- Feedstock specs matter: API, sulfur, BTEX limits

- Price impact: quality premiums US$2–4/bbl (2024)

- Realized discount: ~3–6% vs WTI (2024)

- Contract clauses: docking, penalties, tight delivery windows

Availability of Alternative Supply Sources

Buyers in 2025 face abundant alternatives from the Permian, Marcellus, Montney and other shale plays, with US gas production at ~100 Bcf/d and Canadian gas exports rising 8% YoY, so NuVista cannot reliably command a premium.

High substitutability means purchasers can switch suppliers quickly; if NuVista raises price by >5–10% buyers likely shift to lower-cost producers, keeping bargaining power with buyers.

- North America supply ~100 Bcf/d (2025)

- Canadian gas exports +8% YoY (2024→25)

- Price premium vulnerability >5–10%

Buyers Dictate Pricing: NuVista a Price-Taker; >5–10% Hikes Spur Substitution

Buyers wield strong power: NuVista is a price taker on AECO/NYMEX (2024 AECO C$2.75/GJ, HH US$2.95/MMBtu), 40–50% of volumes to few large buyers, easy supplier switching, and pipeline access shifts leverage; quality discounts trimmed liquids by ~3–6% (2024) and docking penalties raised premiums US$2–4/bbl. Price hikes >5–10% likely trigger buyer substitution.

| Metric | 2024–25 |

|---|---|

| AECO | C$2.75/GJ (2024) |

| Henry Hub | US$2.95/MMBtu (2024) |

| Volumes to big buyers | 40–50% |

| Liquids discount vs WTI | 3–6% |

| Quality premium | US$2–4/bbl |

What You See Is What You Get

NuVista Energy Porter's Five Forces Analysis

This preview shows the exact NuVista Energy Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the part of the full, professionally formatted file you’ll be able to download and use the moment you buy. You’re looking at the actual deliverable; once payment is complete, you’ll get instant access to this exact file. No mockups or samples—what you see is what you get.