NV5 Global SWOT Analysis

Your Strategic Toolkit Starts Here

NV5 Global stands at the intersection of engineering expertise and technology-driven services, with durable client relationships and diversified revenue streams but exposure to cyclical infrastructure spending and integration risks; our full SWOT unpacks competitive advantages, regulatory pressures, and growth levers. Purchase the complete SWOT analysis to access a professionally written, editable report and Excel matrix for strategy, investment, or due diligence.

Strengths

Diversified Service Portfolio

NV5’s diversified service portfolio spans infrastructure, utility services, and geospatial technology, giving a natural hedge against sector downturns; in 2024 these segments contributed roughly 38%, 31%, and 18% of revenue respectively, lowering single-market risk. The multi-disciplinary model enables end-to-end delivery from design to program management, supporting higher project capture rates and repeat work. Balancing public and private contracts—about 56% public, 44% private in 2024—stabilizes cash flow versus niche peers. This mix helped NV5 grow revenue 11% year-over-year in 2024 to $1.27 billion.

Geospatial Technology Leadership

NV5 is a premier provider of geospatial data solutions, using LiDAR and satellite imagery to serve high-growth markets; geospatial revenue grew ~28% Y/Y in 2025, outpacing the firmwide 9% rise.

This segment posts higher gross margins (~38% vs 22% for engineering in 2025) and builds a durable moat via specialized analytics and proprietary datasets.

By late 2025 NV5 secured multiple high-value contracts—>$45m combined—for environmental monitoring and utility asset management, driving recurring, data-centric revenue.

Proven M&A Execution Strategy

NV5 has executed over 60 acquisitions since 2014, expanding revenue from $250m in 2014 to $1.1bn in 2024, showing clear M&A-driven scale; management uses a disciplined framework targeting accretive, tuck-in deals with payback under 3 years. The team focuses on geographic and technical fills—87% of 2024 revenue came from post-acquisition growth—and rapid integration has driven market-share gains across key U.S. and international markets.

Strong Public Sector Relationships

- ~45% backlog from government contracts

- Multi-year awards → revenue visibility

- High compliance reduces entrant risk

- Demand steadies in economic downturns

Scalable Operational Model

- Decentralized leadership + central services

- Revenue/employee ≈ $210,000 (2024)

- Adjusted EBITDA margin ≈ 13% (2024)

- Operating margin up ~120 bps since 2022

- Cross-sell ≈ 18% of 2024 services growth

NV5: $1.27B revenue, 11% growth—geospatial surges 28% with 38% margin; adj. EBITDA ~13%

NV5’s diversified services (infrastructure 38%, utilities 31%, geospatial 18% in 2024) and balanced public/private mix (56%/44%) delivered $1.27B revenue in 2024, +11% Y/Y; geospatial grew ~28% in 2025 with ~38% gross margin vs 22% for engineering. M&A expanded revenue from $250M (2014) to $1.1B (2024) via 60+ deals; backlog ~45% government supports visibility and adjusted EBITDA ~13% (2024).

| Metric | Value |

|---|---|

| 2024 Revenue | $1.27B |

| Y/Y Revenue Growth (2024) | 11% |

| Geospatial Growth (2025) | ~28% |

| Gross Margin: Geospatial (2025) | ~38% |

| Adj. EBITDA (2024) | ~13% |

| Backlog Govt. | ~45% |

What is included in the product

Provides a concise SWOT analysis of NV5 Global, summarizing its core strengths, operational weaknesses, market growth opportunities, and external threats to inform strategic decision-making.

Provides a concise NV5 Global SWOT matrix for rapid strategic alignment and stakeholder-ready summaries.

Weaknesses

Significant Goodwill and Intangibles

NV5 holds about $1.1 billion in goodwill and $320 million in intangibles on its 2024 balance sheet, reflecting aggressive M&A; that raises a real impairment risk if acquisitions underperform or sector multiples drop.

Analysts flag such high intangibles as a red flag for earnings quality and balance-sheet resilience—historically, engineering peers saw 10–25% goodwill write-downs in 2020–2023 downturns.

Integration and Cultural Risks

The rapid pace of NV5 Global’s acquisitions—22 deals since 2019 including nine in 2024—raises integration and cultural risks that strain unified culture and standard processes across business units.

Combining diverse technical teams and legacy IT can cause service disruptions and turnover; NV5 reported 7–9% attrition in select acquired divisions in 2023.

If NV5 fails to harmonize systems and people, projected $40–60m annual synergies from recent deals could be diluted, pressuring long-term margins and ROIC.

Dependence on Government Funding

NV5’s heavy reliance on public-sector contracts offers steady revenue but raises exposure to political shifts; federal infrastructure funding fell 4% year-over-year in 2024, tightening available work. Delays in federal appropriations and 2025 budget uncertainty have already pushed projects into later quarters, trimming backlog by an estimated 6% in FY2024. This dependence forces continuous legislative monitoring to forecast funding headwinds and adjust bidding and staffing plans.

High Relative Leverage

NV5 Global’s acquisition-fueled growth has driven a higher debt load—total long-term debt was about $300 million as of FY2024 (Dec 31, 2024)—raising interest expense and constraining cash for organic investment.

In a 2024–25 high-rate backdrop, elevated debt service trimmed net income and limited flexibility; keeping debt-to-equity near management targets remains a clear governance challenge.

- Long-term debt ≈ $300M (FY2024)

- Higher interest expense reduces free cash flow

- High rates limit capital for organic growth

- Balancing M&A with healthy debt ratios is critical

Geographic Concentration in Select Markets

- 78% of 2024 revenue from US

- $1.36B total revenue (FY2024)

- High exposure to regional weather/regulation

NV5’s M&A-fueled balance sheet: $1.1B goodwill, $300M debt, high integration risk

Heavy M&A left NV5 with ~$1.1B goodwill and $320M intangibles (FY2024), raising impairment risk; long-term debt ≈ $300M increases interest expense and limits capex; 78% of $1.36B revenue is US‑centric, concentrating regional and political exposure; rapid deal pace (22 deals since 2019) fuels integration, attrition, and synergy execution risks.

| Metric | Value |

|---|---|

| Goodwill | $1.1B |

| Intangibles | $320M |

| Long-term debt | $300M |

| Revenue (FY2024) | $1.36B |

| US revenue share | 78% |

| Deals since 2019 | 22 |

What You See Is What You Get

NV5 Global SWOT Analysis

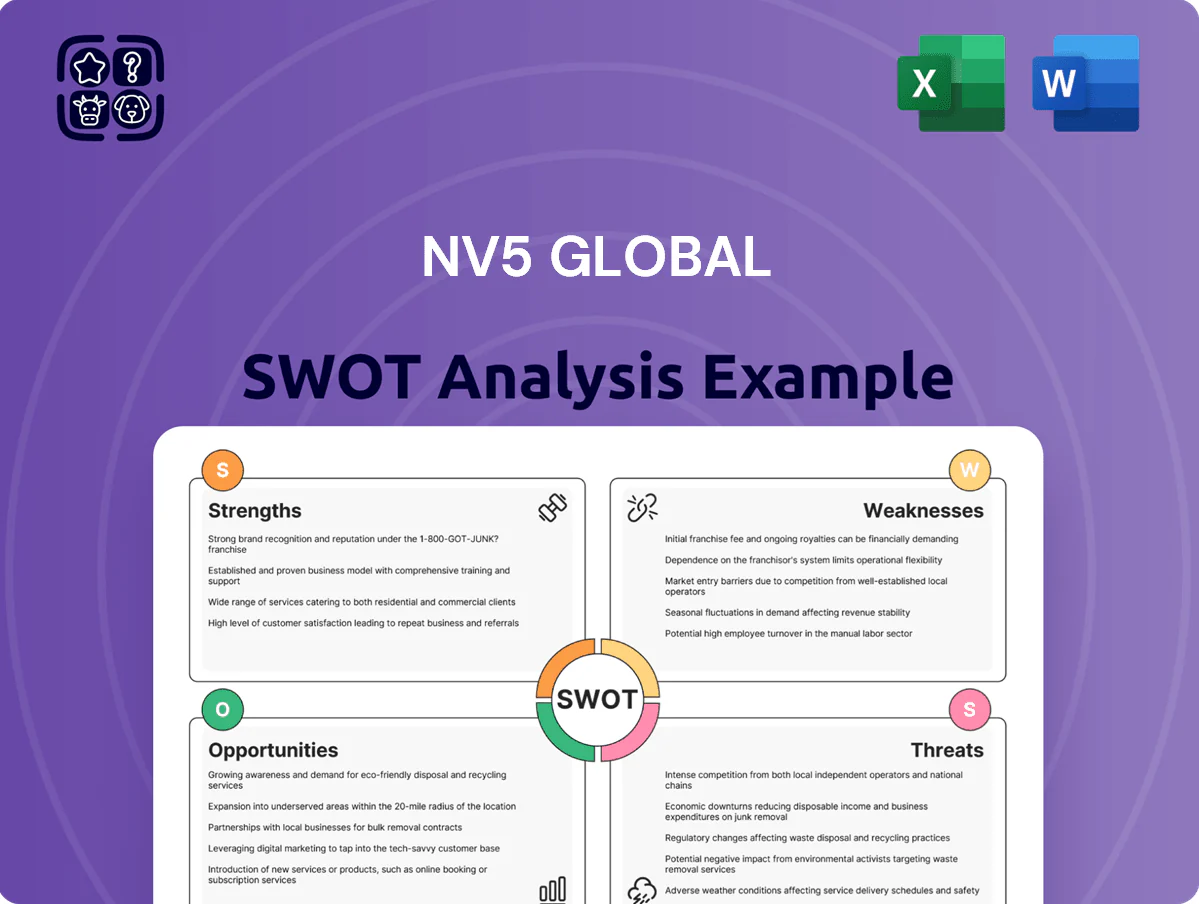

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full NV5 Global report, so what you see is what you'll download after payment. Purchase unlocks the complete, editable version with in-depth strengths, weaknesses, opportunities, and threats. Use it immediately for analysis or presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

NV5 Global stands at the intersection of engineering expertise and technology-driven services, with durable client relationships and diversified revenue streams but exposure to cyclical infrastructure spending and integration risks; our full SWOT unpacks competitive advantages, regulatory pressures, and growth levers. Purchase the complete SWOT analysis to access a professionally written, editable report and Excel matrix for strategy, investment, or due diligence.

Strengths

Diversified Service Portfolio

NV5’s diversified service portfolio spans infrastructure, utility services, and geospatial technology, giving a natural hedge against sector downturns; in 2024 these segments contributed roughly 38%, 31%, and 18% of revenue respectively, lowering single-market risk. The multi-disciplinary model enables end-to-end delivery from design to program management, supporting higher project capture rates and repeat work. Balancing public and private contracts—about 56% public, 44% private in 2024—stabilizes cash flow versus niche peers. This mix helped NV5 grow revenue 11% year-over-year in 2024 to $1.27 billion.

Geospatial Technology Leadership

NV5 is a premier provider of geospatial data solutions, using LiDAR and satellite imagery to serve high-growth markets; geospatial revenue grew ~28% Y/Y in 2025, outpacing the firmwide 9% rise.

This segment posts higher gross margins (~38% vs 22% for engineering in 2025) and builds a durable moat via specialized analytics and proprietary datasets.

By late 2025 NV5 secured multiple high-value contracts—>$45m combined—for environmental monitoring and utility asset management, driving recurring, data-centric revenue.

Proven M&A Execution Strategy

NV5 has executed over 60 acquisitions since 2014, expanding revenue from $250m in 2014 to $1.1bn in 2024, showing clear M&A-driven scale; management uses a disciplined framework targeting accretive, tuck-in deals with payback under 3 years. The team focuses on geographic and technical fills—87% of 2024 revenue came from post-acquisition growth—and rapid integration has driven market-share gains across key U.S. and international markets.

Strong Public Sector Relationships

- ~45% backlog from government contracts

- Multi-year awards → revenue visibility

- High compliance reduces entrant risk

- Demand steadies in economic downturns

Scalable Operational Model

- Decentralized leadership + central services

- Revenue/employee ≈ $210,000 (2024)

- Adjusted EBITDA margin ≈ 13% (2024)

- Operating margin up ~120 bps since 2022

- Cross-sell ≈ 18% of 2024 services growth

NV5: $1.27B revenue, 11% growth—geospatial surges 28% with 38% margin; adj. EBITDA ~13%

NV5’s diversified services (infrastructure 38%, utilities 31%, geospatial 18% in 2024) and balanced public/private mix (56%/44%) delivered $1.27B revenue in 2024, +11% Y/Y; geospatial grew ~28% in 2025 with ~38% gross margin vs 22% for engineering. M&A expanded revenue from $250M (2014) to $1.1B (2024) via 60+ deals; backlog ~45% government supports visibility and adjusted EBITDA ~13% (2024).

| Metric | Value |

|---|---|

| 2024 Revenue | $1.27B |

| Y/Y Revenue Growth (2024) | 11% |

| Geospatial Growth (2025) | ~28% |

| Gross Margin: Geospatial (2025) | ~38% |

| Adj. EBITDA (2024) | ~13% |

| Backlog Govt. | ~45% |

What is included in the product

Provides a concise SWOT analysis of NV5 Global, summarizing its core strengths, operational weaknesses, market growth opportunities, and external threats to inform strategic decision-making.

Provides a concise NV5 Global SWOT matrix for rapid strategic alignment and stakeholder-ready summaries.

Weaknesses

Significant Goodwill and Intangibles

NV5 holds about $1.1 billion in goodwill and $320 million in intangibles on its 2024 balance sheet, reflecting aggressive M&A; that raises a real impairment risk if acquisitions underperform or sector multiples drop.

Analysts flag such high intangibles as a red flag for earnings quality and balance-sheet resilience—historically, engineering peers saw 10–25% goodwill write-downs in 2020–2023 downturns.

Integration and Cultural Risks

The rapid pace of NV5 Global’s acquisitions—22 deals since 2019 including nine in 2024—raises integration and cultural risks that strain unified culture and standard processes across business units.

Combining diverse technical teams and legacy IT can cause service disruptions and turnover; NV5 reported 7–9% attrition in select acquired divisions in 2023.

If NV5 fails to harmonize systems and people, projected $40–60m annual synergies from recent deals could be diluted, pressuring long-term margins and ROIC.

Dependence on Government Funding

NV5’s heavy reliance on public-sector contracts offers steady revenue but raises exposure to political shifts; federal infrastructure funding fell 4% year-over-year in 2024, tightening available work. Delays in federal appropriations and 2025 budget uncertainty have already pushed projects into later quarters, trimming backlog by an estimated 6% in FY2024. This dependence forces continuous legislative monitoring to forecast funding headwinds and adjust bidding and staffing plans.

High Relative Leverage

NV5 Global’s acquisition-fueled growth has driven a higher debt load—total long-term debt was about $300 million as of FY2024 (Dec 31, 2024)—raising interest expense and constraining cash for organic investment.

In a 2024–25 high-rate backdrop, elevated debt service trimmed net income and limited flexibility; keeping debt-to-equity near management targets remains a clear governance challenge.

- Long-term debt ≈ $300M (FY2024)

- Higher interest expense reduces free cash flow

- High rates limit capital for organic growth

- Balancing M&A with healthy debt ratios is critical

Geographic Concentration in Select Markets

- 78% of 2024 revenue from US

- $1.36B total revenue (FY2024)

- High exposure to regional weather/regulation

NV5’s M&A-fueled balance sheet: $1.1B goodwill, $300M debt, high integration risk

Heavy M&A left NV5 with ~$1.1B goodwill and $320M intangibles (FY2024), raising impairment risk; long-term debt ≈ $300M increases interest expense and limits capex; 78% of $1.36B revenue is US‑centric, concentrating regional and political exposure; rapid deal pace (22 deals since 2019) fuels integration, attrition, and synergy execution risks.

| Metric | Value |

|---|---|

| Goodwill | $1.1B |

| Intangibles | $320M |

| Long-term debt | $300M |

| Revenue (FY2024) | $1.36B |

| US revenue share | 78% |

| Deals since 2019 | 22 |

What You See Is What You Get

NV5 Global SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full NV5 Global report, so what you see is what you'll download after payment. Purchase unlocks the complete, editable version with in-depth strengths, weaknesses, opportunities, and threats. Use it immediately for analysis or presentation.