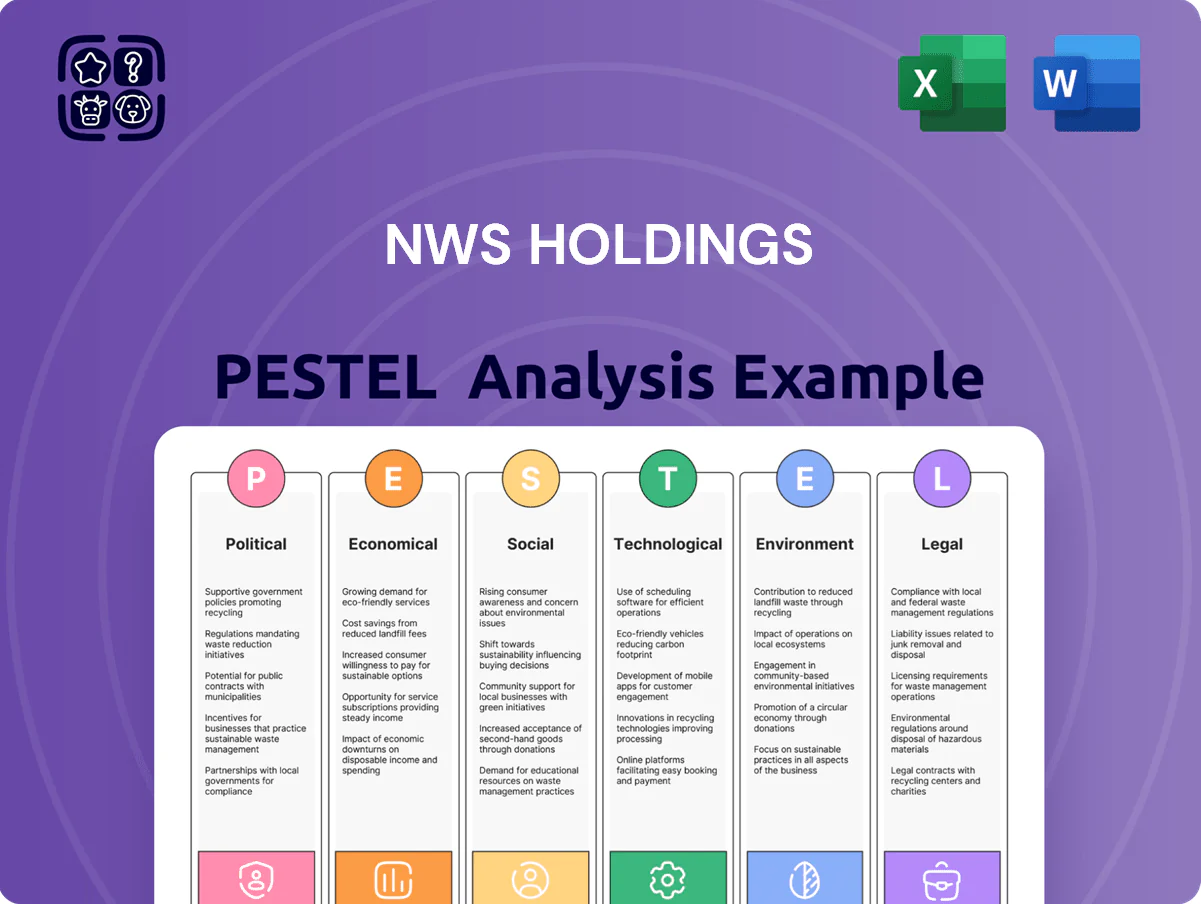

NWS Holdings PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain a strategic edge with our concise PESTLE Analysis of NWS Holdings—spot how regulatory shifts, macroeconomic trends, and technological disruption shape its growth trajectory and risk profile; purchase the full report to access actionable, exportable insights and ready-to-use slides for investment decisions or boardroom strategy.

Political factors

GBA Integration Policy

The ongoing Greater Bay Area integration drives NWS Holdings as it aligns HK$28.7bn (2024) infrastructure assets toward regional connectivity, supporting long-term toll-road value through increased cross-border traffic forecasts of 12% CAGR to 2027 per government estimates.

Ownership Stability under CTF

The 2018 acquisition by Chow Tai Fook (CTF) that raised its stake to c.55% has delivered ownership stability for NWS Holdings, aligning corporate strategy with CTF’s HK/Mainland focus; NWS reported HKD 28.7bn revenue in FY2024, enabling scale for public‑private projects.

Sino-US Trade Relations

Geopolitical tensions between the US and China have cut container throughput via Hong Kong 2023–24, with HK port throughput down ~8% in 2024 versus 2019 pre-COVID levels, pressuring NWS Holdings’ port and logistics revenue streams.

NWS must manage exposure to sanctions and shifting supply chains—global rerouting increased transshipment demand in Southeast Asia by ~6% in 2024, altering capex and contract priorities for its logistics assets.

Maintaining geographic diversification—assets across Mainland China, Hong Kong and SE Asia that contributed ~45% of group recurring revenue in FY2024—helps mitigate localized political disruption risk.

Infrastructure Stimulus in China

China pledged CNY 2.5 trillion in infrastructure spending for 2024–25 to boost growth, directly supporting NWS Holdings’ core toll-road operations through higher traffic and new projects.

Policy focus on high-quality development and transport modernization opens prospects to renew/extend concessions and win maintenance contracts, aligning with NWS’s expertise.

State-led programs sustain a steady pipeline: provincial transport budgets rose ~8% YoY in 2024, signaling continued tender flow for mainland infrastructure.

- Direct demand boost for toll-road revenue and traffic recovery

- Concession renewal and extension opportunities

- Increased provincial transport budgets (~8% YoY 2024)

Hong Kong Policy Address Initiatives

Hong Kong Policy Address priorities on housing, healthcare and transport secure predictable contract pipelines for NWS Holdings’ construction and facilities units; government capital works budget for 2025–26 is HK$171.6 billion, underpinning demand.

Alignment with the Northern Metropolis plan is critical—estimated HK$600 billion-plus regional investment—affording NWS opportunities for long-term service agreements and major build contracts.

NWS’s track record delivering complex urban projects and integrated facilities management positions it as a preferred partner for government-led schemes, enhancing bid success and recurring revenue streams.

- HK$171.6bn 2025–26 capital works budget

- Northern Metropolis ~HK$600bn investment

- Strong public-sector pipeline for construction and FM

NWS set to gain from CNY2.5tn China infra, HK capex and shifting port flows

Political support for Greater Bay Area and CNY2.5tn 2024–25 infrastructure spend boosts NWS’s toll-road and construction pipelines; HK capital works HK$171.6bn (2025–26) and Northern Metropolis ~HK$600bn reinforce FM and build demand, while CTF majority ownership (~55%) provides strategic stability; HK port throughput -8% (2024 vs 2019) and SE Asia transshipment +6% (2024) reshape logistics exposures.

| Item | Value |

|---|---|

| CTF stake | ~55% |

| China infra spend | CNY2.5tn (2024–25) |

| HK capital works | HK$171.6bn (2025–26) |

| Northern Metropolis | ~HK$600bn |

| HK port throughput | -8% (2024 vs 2019) |

| SE Asia transshipment | +6% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect NWS Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend-backed subpoints to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for NWS Holdings that streamlines external risk assessment and market positioning, easily dropped into presentations or shared across teams for quick strategic alignment.

Economic factors

Interest Rate Volatility

The high-interest-rate environment at end-2025—HKD HIBOR around 4.2% and US 10-year at ~4.6%—elevates financing costs for NWS Holdings’ capital-intensive projects, with gross debt ~HKD 37.5bn (2024) making margins sensitive to HKD/USD moves. Effective hedging reduced FX/IR exposure by an estimated 60% in 2024, while refinancing toward longer tenors and lower spreads is critical to preserve dividend per share of HKD 0.30 in 2025.

Renminbi Exchange Rate Fluctuations

As ~60% of NWS Holdings revenue in 2024 derived from Mainland China, a stronger Renminbi versus the HKD boosts translated income and mainland asset valuations, while RMB weakness compresses consolidated results; 2024 RMB/HKD average rose ~0.9% year-on-year, causing measurable earnings swing.

Currency translation risk creates reported earnings volatility and balance-sheet revaluation exposure; in 2024 FX translation impacted operating profit by an estimated HKD 250–350 million.

The company uses forward contracts, currency swaps and natural hedges (RMB-denominated debt and matched cash flows) to limit net FX exposure, with hedges covering a material portion of forecasted RMB cash flows through 2025.

Toll Road Revenue Recovery

The rebound in mainland China travel lifted NWS Holdings’ toll-road cash flows, with FY2024 toll revenue rising about 9% year-on-year and traffic volume for heavy-duty vehicles up ~7%, stabilizing operating cash inflows.

Mainland GDP growth targets of ~5% for 2024–25 correlate with higher vehicle-km demand, supporting passenger car and freight usage on NWS-managed expressways.

Steady toll receipts—contributing a notable share of operating cash—provide liquidity to fund NWS’s diversification into logistics and environmental services, underpinning planned capex and M&A activity in 2025.

Global Inflationary Pressures

Global inflation raises costs for raw materials, labor and energy—inputs that lifted Hong Kong construction material prices by about 9% in 2024 and contributed to a 7% y/y rise in utilities for regional operations.

NWS mitigates impact via price-adjustment clauses in long-term contracts, helping sustain margins as seen in FY2024 contract revenue resilience.

Enhanced supply-chain efficiency and strategic procurement—bulk purchasing, hedging energy—remain critical to contain operating expense inflation.

- 2024 regional construction material prices +9%

- Utilities/energy costs +7% y/y in 2024

- Price-adjustment clauses used across long-term contracts

- Focus on bulk procurement, supplier diversification, energy hedging

Regional Economic Growth Rates

Hong Kong GDP grew 3.3% in 2024 and Guangdong-Hong Kong-Macao Greater Bay Area (GBA) provinces averaged ~4.5% in 2024, directly influencing demand for NWS Holdings’ insurance, facilities and infrastructure services; weaker growth would compress premiums and premium service uptake.

Slower-than-expected GDP in 2025 forecasts could cut discretionary spend and lower demand for premium FM and insurance products, pressuring margins and utilization rates.

Real-time monitoring of regional PMI, retail sales, tourist arrivals (HK tourist arrivals reached ~15.6 million in 2024) and quarterly GDP enables NWS to reallocate capex and shift service mix rapidly.

- HK GDP 2024: 3.3%

- GBA avg GDP 2024: ~4.5%

- HK tourist arrivals 2024: ~15.6M

- Action: adjust capex, service mix, target lower-margin segments

NWS faces higher funding costs but hedges protect DPS amid solid toll growth

Higher rates and HKD HIBOR ~4.2% (end-2025) raise funding costs for NWS (gross debt ~HKD37.5bn in 2024); effective hedging cut FX/IR exposure ~60% in 2024, shielding DPS HKD0.30. Mainland exposure (~60% revenue 2024) makes RMB/HKD moves material; 2024 RMB/HKD +0.9% y/y; FX translation affected op profit ~HKD250–350m. Toll revenue +9% in FY2024; HK GDP 2024 3.3%, GBA ~4.5%.

| Metric | 2024/End‑2025 |

|---|---|

| Gross debt | HKD37.5bn (2024) |

| HKD HIBOR | ~4.2% (end‑2025) |

| US 10yr | ~4.6% (end‑2025) |

| RMB/HKD change | +0.9% y/y (2024) |

| FX impact on OP | HKD250–350m (2024) |

| Toll revenue | +9% y/y (FY2024) |

| HK GDP | 3.3% (2024) |

| GBA GDP | ~4.5% (2024) |

Same Document Delivered

NWS Holdings PESTLE Analysis

The preview shown here is the exact NWS Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are exactly what you’ll download immediately after payment, with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a strategic edge with our concise PESTLE Analysis of NWS Holdings—spot how regulatory shifts, macroeconomic trends, and technological disruption shape its growth trajectory and risk profile; purchase the full report to access actionable, exportable insights and ready-to-use slides for investment decisions or boardroom strategy.

Political factors

GBA Integration Policy

The ongoing Greater Bay Area integration drives NWS Holdings as it aligns HK$28.7bn (2024) infrastructure assets toward regional connectivity, supporting long-term toll-road value through increased cross-border traffic forecasts of 12% CAGR to 2027 per government estimates.

Ownership Stability under CTF

The 2018 acquisition by Chow Tai Fook (CTF) that raised its stake to c.55% has delivered ownership stability for NWS Holdings, aligning corporate strategy with CTF’s HK/Mainland focus; NWS reported HKD 28.7bn revenue in FY2024, enabling scale for public‑private projects.

Sino-US Trade Relations

Geopolitical tensions between the US and China have cut container throughput via Hong Kong 2023–24, with HK port throughput down ~8% in 2024 versus 2019 pre-COVID levels, pressuring NWS Holdings’ port and logistics revenue streams.

NWS must manage exposure to sanctions and shifting supply chains—global rerouting increased transshipment demand in Southeast Asia by ~6% in 2024, altering capex and contract priorities for its logistics assets.

Maintaining geographic diversification—assets across Mainland China, Hong Kong and SE Asia that contributed ~45% of group recurring revenue in FY2024—helps mitigate localized political disruption risk.

Infrastructure Stimulus in China

China pledged CNY 2.5 trillion in infrastructure spending for 2024–25 to boost growth, directly supporting NWS Holdings’ core toll-road operations through higher traffic and new projects.

Policy focus on high-quality development and transport modernization opens prospects to renew/extend concessions and win maintenance contracts, aligning with NWS’s expertise.

State-led programs sustain a steady pipeline: provincial transport budgets rose ~8% YoY in 2024, signaling continued tender flow for mainland infrastructure.

- Direct demand boost for toll-road revenue and traffic recovery

- Concession renewal and extension opportunities

- Increased provincial transport budgets (~8% YoY 2024)

Hong Kong Policy Address Initiatives

Hong Kong Policy Address priorities on housing, healthcare and transport secure predictable contract pipelines for NWS Holdings’ construction and facilities units; government capital works budget for 2025–26 is HK$171.6 billion, underpinning demand.

Alignment with the Northern Metropolis plan is critical—estimated HK$600 billion-plus regional investment—affording NWS opportunities for long-term service agreements and major build contracts.

NWS’s track record delivering complex urban projects and integrated facilities management positions it as a preferred partner for government-led schemes, enhancing bid success and recurring revenue streams.

- HK$171.6bn 2025–26 capital works budget

- Northern Metropolis ~HK$600bn investment

- Strong public-sector pipeline for construction and FM

NWS set to gain from CNY2.5tn China infra, HK capex and shifting port flows

Political support for Greater Bay Area and CNY2.5tn 2024–25 infrastructure spend boosts NWS’s toll-road and construction pipelines; HK capital works HK$171.6bn (2025–26) and Northern Metropolis ~HK$600bn reinforce FM and build demand, while CTF majority ownership (~55%) provides strategic stability; HK port throughput -8% (2024 vs 2019) and SE Asia transshipment +6% (2024) reshape logistics exposures.

| Item | Value |

|---|---|

| CTF stake | ~55% |

| China infra spend | CNY2.5tn (2024–25) |

| HK capital works | HK$171.6bn (2025–26) |

| Northern Metropolis | ~HK$600bn |

| HK port throughput | -8% (2024 vs 2019) |

| SE Asia transshipment | +6% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect NWS Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend-backed subpoints to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for NWS Holdings that streamlines external risk assessment and market positioning, easily dropped into presentations or shared across teams for quick strategic alignment.

Economic factors

Interest Rate Volatility

The high-interest-rate environment at end-2025—HKD HIBOR around 4.2% and US 10-year at ~4.6%—elevates financing costs for NWS Holdings’ capital-intensive projects, with gross debt ~HKD 37.5bn (2024) making margins sensitive to HKD/USD moves. Effective hedging reduced FX/IR exposure by an estimated 60% in 2024, while refinancing toward longer tenors and lower spreads is critical to preserve dividend per share of HKD 0.30 in 2025.

Renminbi Exchange Rate Fluctuations

As ~60% of NWS Holdings revenue in 2024 derived from Mainland China, a stronger Renminbi versus the HKD boosts translated income and mainland asset valuations, while RMB weakness compresses consolidated results; 2024 RMB/HKD average rose ~0.9% year-on-year, causing measurable earnings swing.

Currency translation risk creates reported earnings volatility and balance-sheet revaluation exposure; in 2024 FX translation impacted operating profit by an estimated HKD 250–350 million.

The company uses forward contracts, currency swaps and natural hedges (RMB-denominated debt and matched cash flows) to limit net FX exposure, with hedges covering a material portion of forecasted RMB cash flows through 2025.

Toll Road Revenue Recovery

The rebound in mainland China travel lifted NWS Holdings’ toll-road cash flows, with FY2024 toll revenue rising about 9% year-on-year and traffic volume for heavy-duty vehicles up ~7%, stabilizing operating cash inflows.

Mainland GDP growth targets of ~5% for 2024–25 correlate with higher vehicle-km demand, supporting passenger car and freight usage on NWS-managed expressways.

Steady toll receipts—contributing a notable share of operating cash—provide liquidity to fund NWS’s diversification into logistics and environmental services, underpinning planned capex and M&A activity in 2025.

Global Inflationary Pressures

Global inflation raises costs for raw materials, labor and energy—inputs that lifted Hong Kong construction material prices by about 9% in 2024 and contributed to a 7% y/y rise in utilities for regional operations.

NWS mitigates impact via price-adjustment clauses in long-term contracts, helping sustain margins as seen in FY2024 contract revenue resilience.

Enhanced supply-chain efficiency and strategic procurement—bulk purchasing, hedging energy—remain critical to contain operating expense inflation.

- 2024 regional construction material prices +9%

- Utilities/energy costs +7% y/y in 2024

- Price-adjustment clauses used across long-term contracts

- Focus on bulk procurement, supplier diversification, energy hedging

Regional Economic Growth Rates

Hong Kong GDP grew 3.3% in 2024 and Guangdong-Hong Kong-Macao Greater Bay Area (GBA) provinces averaged ~4.5% in 2024, directly influencing demand for NWS Holdings’ insurance, facilities and infrastructure services; weaker growth would compress premiums and premium service uptake.

Slower-than-expected GDP in 2025 forecasts could cut discretionary spend and lower demand for premium FM and insurance products, pressuring margins and utilization rates.

Real-time monitoring of regional PMI, retail sales, tourist arrivals (HK tourist arrivals reached ~15.6 million in 2024) and quarterly GDP enables NWS to reallocate capex and shift service mix rapidly.

- HK GDP 2024: 3.3%

- GBA avg GDP 2024: ~4.5%

- HK tourist arrivals 2024: ~15.6M

- Action: adjust capex, service mix, target lower-margin segments

NWS faces higher funding costs but hedges protect DPS amid solid toll growth

Higher rates and HKD HIBOR ~4.2% (end-2025) raise funding costs for NWS (gross debt ~HKD37.5bn in 2024); effective hedging cut FX/IR exposure ~60% in 2024, shielding DPS HKD0.30. Mainland exposure (~60% revenue 2024) makes RMB/HKD moves material; 2024 RMB/HKD +0.9% y/y; FX translation affected op profit ~HKD250–350m. Toll revenue +9% in FY2024; HK GDP 2024 3.3%, GBA ~4.5%.

| Metric | 2024/End‑2025 |

|---|---|

| Gross debt | HKD37.5bn (2024) |

| HKD HIBOR | ~4.2% (end‑2025) |

| US 10yr | ~4.6% (end‑2025) |

| RMB/HKD change | +0.9% y/y (2024) |

| FX impact on OP | HKD250–350m (2024) |

| Toll revenue | +9% y/y (FY2024) |

| HK GDP | 3.3% (2024) |

| GBA GDP | ~4.5% (2024) |

Same Document Delivered

NWS Holdings PESTLE Analysis

The preview shown here is the exact NWS Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are exactly what you’ll download immediately after payment, with no placeholders or surprises.