Nxera Pharma PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain strategic clarity with our PESTLE Analysis of Nxera Pharma—uncover how political shifts, regulatory pressures, economic trends, and technological advances will shape its trajectory and competitive standing. This concise yet powerful brief highlights risks and opportunities investors and strategists need now. Purchase the full, ready-to-use report for detailed insights, data-backed scenarios, and actionable recommendations.

Political factors

Global Drug Pricing Legislation

The US Inflation Reduction Act enables Medicare drug price negotiation starting 2026, potentially lowering prices for top-selling therapies by up to 60%, while EU moves (Germany, UK) tighten price controls and reference pricing—these shifts could compress peak sales forecasts for Nxera Pharma’s GPCR-targeted neurologic candidates, where orphan designations (affecting ~5–10% of neurology drugs) and payer negotiation power will determine net pricing and long-term EBITDA margins.

Geopolitical R&D Collaboration

As a UK–Japan operator, Nxera Pharma depends on post-Brexit trade agreements and the UK–Japan Comprehensive Economic Partnership (effective 2021) to ease tariffs and regulatory alignment for cross-border R&D; UK–Japan goods trade reached £33.1bn in 2023, underscoring material flows relevant to supply chains.

Political stability and bilateral investment treaties support capital and talent mobility—Japan’s skilled migration rose 12% in 2024—critical for Nxera’s drug-discovery teams across both hubs.

Any diplomatic disruption could impede IP transfers and lab asset deployment: international patent filings between the UK and Japan totaled roughly 18,000 in 2022, highlighting scale at risk from policy shifts.

Government Healthcare Funding

Public sector investment in neurodegenerative research underpins clinical-stage biopharma; in 2024 US federal funding for Alzheimer's and related dementias reached about $3.1 billion, supporting preclinical and clinical partnerships relevant to Nxera Pharma.

Political agendas prioritizing Alzheimer's and Parkinson's can expand grant pools and academic collaborations, with NIH awards to neurodegeneration rising ~8% year-over-year into 2024.

Conversely, policy shifts toward infectious disease or other priorities risk diverting funds, as seen when pandemic response reallocated billions from chronic disease research during 2020–2022.

Regulatory Harmonization Initiatives

Political efforts via the ICH to harmonize standards—now covering 17 guideline areas—accelerate Nxera Pharma's time-to-market by aligning requirements across FDA, EMA and PMDA, potentially cutting multi-region approval prep by an estimated 12–18% based on industry benchmarking through 2024–2025.

Streamlined regulatory convergence reduces administrative overhead for multi-regional trials, lowering per-trial compliance costs which the industry reports fell ~10% between 2021–2024, aiding Nxera's global development efficiency.

Ongoing political support for expedited pathways for unmet needs—reflected in 25% of FDA oncology approvals using accelerated programs in 2024—remains a key driver of Nxera's projected development timelines into late 2025.

- ICH harmonization may cut approval prep 12–18%

- Compliance costs down ~10% (2021–2024)

- 25% of FDA oncology approvals used accelerated programs in 2024

Trade Policy and Supply Chains

Tariffs and trade restrictions on lab equipment and reagents have raised input costs; US tariffs and export controls contributed to a ~5–8% price increase for specialty reagents in 2024, squeezing Dxera-like R&D budgets.

Political moves toward friend-shoring—reshoring to trusted partners—shift sourcing away from China, raising supply-chain redundancy but adding 6–12% logistic and manufacturing premiums for pharmaceutical components in 2024–25.

Nxera must adapt supplier diversification, local sourcing, and inventory buffers to prevent delays to structural biology and chemistry platforms and avoid capex or opex spikes that could erode R&D timelines.

- Tariff-driven reagent price rise: ~5–8% (2024)

- Friend-shoring premium: ~6–12% added costs (2024–25)

- Mitigation: supplier diversification, local sourcing, safety stock

Drug pricing cuts, trade shifts and R&D funding reshape pharma costs and approvals

Medicare negotiation (IRA) may cut top-drug prices up to 60% from 2026; UK–Japan trade (£33.1bn 2023) and post-Brexit rules affect supply/R&D; US neuro research funding ~$3.1bn (2024) and NIH +8% YOY support partnerships; tariffs/friend-shoring raised reagent/logistics costs ~5–12% (2024–25), while ICH harmonization and expedited pathways shave ~12–18% approval prep and speed timelines.

| Metric | Value |

|---|---|

| Medicare negotiation impact | Up to -60% |

| UK–Japan trade 2023 | £33.1bn |

| US neuro funding 2024 | $3.1bn |

| Reagent/logistics cost rise | ~5–12% |

| ICH prep reduction | 12–18% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Nxera Pharma, with each section backed by current data and trends to surface actionable risks and opportunities for executives, investors, and strategists.

A concise, shareable PESTLE snapshot of Nxera Pharma that highlights regulatory, market, and technological risks and opportunities for quick alignment in meetings or client reports.

Economic factors

Interest Rate Environment

As of late 2025, global policy rates remain elevated—US Fed funds ~5.25–5.50% and ECB refi ~4.25%—raising Nxera Pharma’s cost of capital and discount rates used in DCFs, which compresses valuations for clinical-stage biotech with long cash‑burn horizons.

Higher rates make equity financing more dilutive and debt more expensive; analysts should model longer financing needs given Nxera’s pre‑revenue status and 12–24 month cash runway assumptions.

Currency Exchange Volatility

Nxera Pharma operates across Japan, the UK and the US, making its top-line sensitive to JPY/GBP/USD swings; 2024 saw the USD/JPY range about 132–153 and GBP/USD 1.20–1.35, amplifying FX risk on milestone payments.

With milestone revenues often invoiced in foreign currency while R&D and manufacturing costs are local, exchange moves created material accounting gains/losses—biotech peers reported FX impacts of up to 8–12% of EBITDA in 2024.

Robust hedging—forwards, options and natural hedges—plus rolling cash-flow forecasts are essential to preserve Nxera’s cash runway and limit downside from adverse currency shifts.

Milestone Payment Dependency

The company’s economic stability hinges on securing clinical and regulatory milestones from Big Pharma partners, with Nxera reporting potential milestone payments up to $420 million across deals as of 2025, which directly fund R&D without equity dilution. These non-dilutive payments reduced Nxera’s 2024 external financing needs by an estimated 35%, lowering cash burn pressure. Analysts monitor milestone triggers as leading economic indicators of solvency and capacity to sustain long-term research operations.

Bio-Pharmaceutical R&D Inflation

Rising costs for specialized labor, trial recruitment and advanced lab tech squeeze Nxera’s margins; US biotech wage growth averaged 6.2% in 2024 in major hubs, driving payroll inflation. Phase II/III per-patient costs rose ~8%–12% in 2023–24, raising cash needs and pushing some programs toward partnering.

- 6.2% biotech wage growth (2024)

- Phase II/III per-patient cost +8%–12% (2023–24)

- Higher recruitment costs lengthen timelines

Venture Capital and Equity Appetite

Broader economic sentiment shapes follow-on financing for clinical-stage biotech: in 2024 global VC funding to life sciences rose to about $62.5B, easing capital access for high-upside GPCR discovery platforms like Nxera.

During bull cycles investors favor early-stage platforms; 2023–2025 public biotech IPO windows showed 40–60% higher valuations versus bear phases, enhancing partnership leverage for Nxera.

Nxera must time capital raises and collaboration announcements to market cycles to maximize valuation and reduce dilution risk.

- 2024 global life sciences VC: ~$62.5B

- IPO valuation uplift in bull windows: 40–60%

- Strategy: align fundraising and partnership news with bullish biotech sentiment

Higher rates, FX swings and rising biotech costs squeeze Nxera’s valuation and cash runway

Elevated 2025 policy rates (Fed 5.25–5.50%, ECB 4.25%) raise Nxera’s discount rates, pressuring valuations and making equity/debt costlier; 2024 USD/JPY 132–153 and GBP/USD 1.20–1.35 amplified FX risk versus milestone receipts (potential $420M). 2024 biotech wage growth ~6.2% and Phase II/III per‑patient cost +8–12% increased cash burn; 2024 life‑sciences VC ~$62.5B.

| Metric | Value |

|---|---|

| Fed rate (2025) | 5.25–5.50% |

| USD/JPY (2024) | 132–153 |

| Wage growth (2024) | 6.2% |

| VC funding (2024) | $62.5B |

What You See Is What You Get

Nxera Pharma PESTLE Analysis

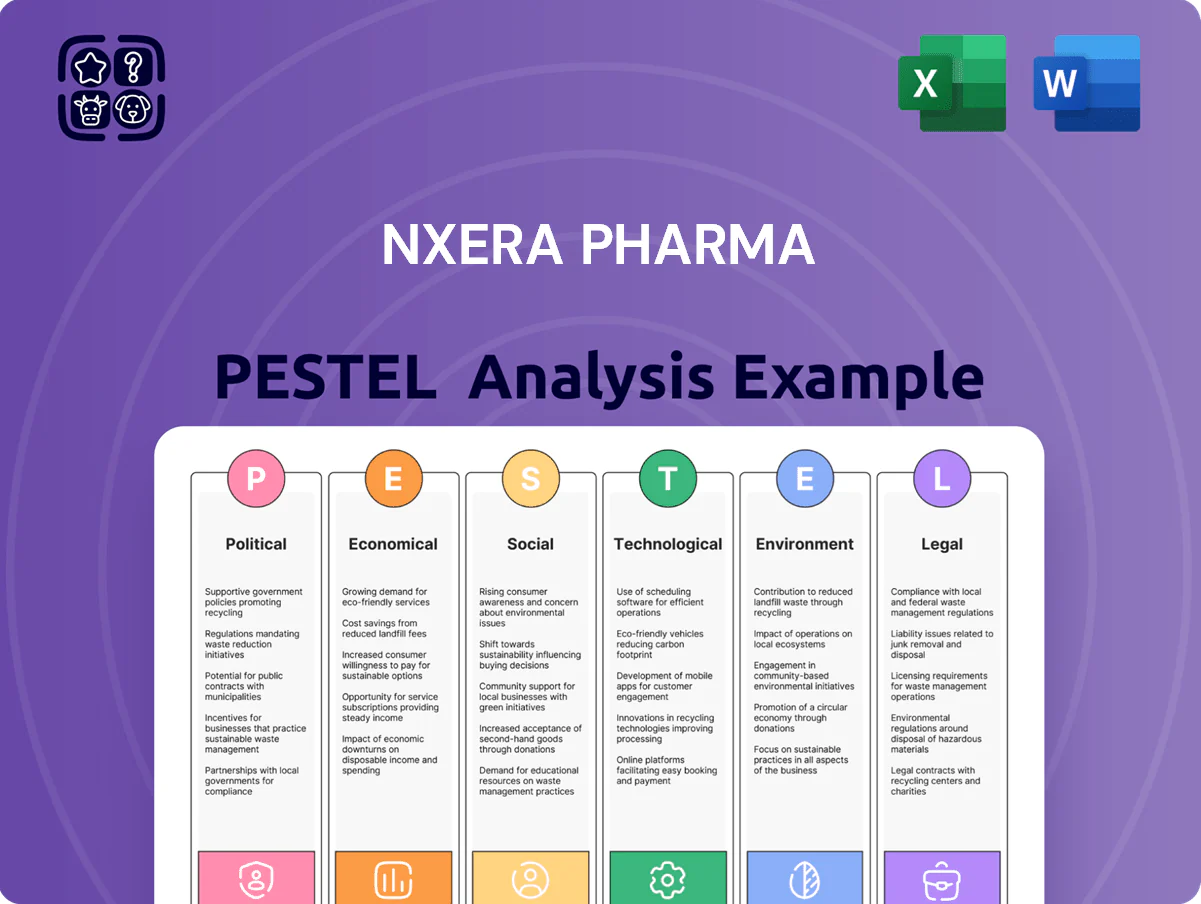

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use, presenting a concise PESTLE analysis of Nxera Pharma covering political, economic, social, technological, legal, and environmental factors.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain strategic clarity with our PESTLE Analysis of Nxera Pharma—uncover how political shifts, regulatory pressures, economic trends, and technological advances will shape its trajectory and competitive standing. This concise yet powerful brief highlights risks and opportunities investors and strategists need now. Purchase the full, ready-to-use report for detailed insights, data-backed scenarios, and actionable recommendations.

Political factors

Global Drug Pricing Legislation

The US Inflation Reduction Act enables Medicare drug price negotiation starting 2026, potentially lowering prices for top-selling therapies by up to 60%, while EU moves (Germany, UK) tighten price controls and reference pricing—these shifts could compress peak sales forecasts for Nxera Pharma’s GPCR-targeted neurologic candidates, where orphan designations (affecting ~5–10% of neurology drugs) and payer negotiation power will determine net pricing and long-term EBITDA margins.

Geopolitical R&D Collaboration

As a UK–Japan operator, Nxera Pharma depends on post-Brexit trade agreements and the UK–Japan Comprehensive Economic Partnership (effective 2021) to ease tariffs and regulatory alignment for cross-border R&D; UK–Japan goods trade reached £33.1bn in 2023, underscoring material flows relevant to supply chains.

Political stability and bilateral investment treaties support capital and talent mobility—Japan’s skilled migration rose 12% in 2024—critical for Nxera’s drug-discovery teams across both hubs.

Any diplomatic disruption could impede IP transfers and lab asset deployment: international patent filings between the UK and Japan totaled roughly 18,000 in 2022, highlighting scale at risk from policy shifts.

Government Healthcare Funding

Public sector investment in neurodegenerative research underpins clinical-stage biopharma; in 2024 US federal funding for Alzheimer's and related dementias reached about $3.1 billion, supporting preclinical and clinical partnerships relevant to Nxera Pharma.

Political agendas prioritizing Alzheimer's and Parkinson's can expand grant pools and academic collaborations, with NIH awards to neurodegeneration rising ~8% year-over-year into 2024.

Conversely, policy shifts toward infectious disease or other priorities risk diverting funds, as seen when pandemic response reallocated billions from chronic disease research during 2020–2022.

Regulatory Harmonization Initiatives

Political efforts via the ICH to harmonize standards—now covering 17 guideline areas—accelerate Nxera Pharma's time-to-market by aligning requirements across FDA, EMA and PMDA, potentially cutting multi-region approval prep by an estimated 12–18% based on industry benchmarking through 2024–2025.

Streamlined regulatory convergence reduces administrative overhead for multi-regional trials, lowering per-trial compliance costs which the industry reports fell ~10% between 2021–2024, aiding Nxera's global development efficiency.

Ongoing political support for expedited pathways for unmet needs—reflected in 25% of FDA oncology approvals using accelerated programs in 2024—remains a key driver of Nxera's projected development timelines into late 2025.

- ICH harmonization may cut approval prep 12–18%

- Compliance costs down ~10% (2021–2024)

- 25% of FDA oncology approvals used accelerated programs in 2024

Trade Policy and Supply Chains

Tariffs and trade restrictions on lab equipment and reagents have raised input costs; US tariffs and export controls contributed to a ~5–8% price increase for specialty reagents in 2024, squeezing Dxera-like R&D budgets.

Political moves toward friend-shoring—reshoring to trusted partners—shift sourcing away from China, raising supply-chain redundancy but adding 6–12% logistic and manufacturing premiums for pharmaceutical components in 2024–25.

Nxera must adapt supplier diversification, local sourcing, and inventory buffers to prevent delays to structural biology and chemistry platforms and avoid capex or opex spikes that could erode R&D timelines.

- Tariff-driven reagent price rise: ~5–8% (2024)

- Friend-shoring premium: ~6–12% added costs (2024–25)

- Mitigation: supplier diversification, local sourcing, safety stock

Drug pricing cuts, trade shifts and R&D funding reshape pharma costs and approvals

Medicare negotiation (IRA) may cut top-drug prices up to 60% from 2026; UK–Japan trade (£33.1bn 2023) and post-Brexit rules affect supply/R&D; US neuro research funding ~$3.1bn (2024) and NIH +8% YOY support partnerships; tariffs/friend-shoring raised reagent/logistics costs ~5–12% (2024–25), while ICH harmonization and expedited pathways shave ~12–18% approval prep and speed timelines.

| Metric | Value |

|---|---|

| Medicare negotiation impact | Up to -60% |

| UK–Japan trade 2023 | £33.1bn |

| US neuro funding 2024 | $3.1bn |

| Reagent/logistics cost rise | ~5–12% |

| ICH prep reduction | 12–18% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Nxera Pharma, with each section backed by current data and trends to surface actionable risks and opportunities for executives, investors, and strategists.

A concise, shareable PESTLE snapshot of Nxera Pharma that highlights regulatory, market, and technological risks and opportunities for quick alignment in meetings or client reports.

Economic factors

Interest Rate Environment

As of late 2025, global policy rates remain elevated—US Fed funds ~5.25–5.50% and ECB refi ~4.25%—raising Nxera Pharma’s cost of capital and discount rates used in DCFs, which compresses valuations for clinical-stage biotech with long cash‑burn horizons.

Higher rates make equity financing more dilutive and debt more expensive; analysts should model longer financing needs given Nxera’s pre‑revenue status and 12–24 month cash runway assumptions.

Currency Exchange Volatility

Nxera Pharma operates across Japan, the UK and the US, making its top-line sensitive to JPY/GBP/USD swings; 2024 saw the USD/JPY range about 132–153 and GBP/USD 1.20–1.35, amplifying FX risk on milestone payments.

With milestone revenues often invoiced in foreign currency while R&D and manufacturing costs are local, exchange moves created material accounting gains/losses—biotech peers reported FX impacts of up to 8–12% of EBITDA in 2024.

Robust hedging—forwards, options and natural hedges—plus rolling cash-flow forecasts are essential to preserve Nxera’s cash runway and limit downside from adverse currency shifts.

Milestone Payment Dependency

The company’s economic stability hinges on securing clinical and regulatory milestones from Big Pharma partners, with Nxera reporting potential milestone payments up to $420 million across deals as of 2025, which directly fund R&D without equity dilution. These non-dilutive payments reduced Nxera’s 2024 external financing needs by an estimated 35%, lowering cash burn pressure. Analysts monitor milestone triggers as leading economic indicators of solvency and capacity to sustain long-term research operations.

Bio-Pharmaceutical R&D Inflation

Rising costs for specialized labor, trial recruitment and advanced lab tech squeeze Nxera’s margins; US biotech wage growth averaged 6.2% in 2024 in major hubs, driving payroll inflation. Phase II/III per-patient costs rose ~8%–12% in 2023–24, raising cash needs and pushing some programs toward partnering.

- 6.2% biotech wage growth (2024)

- Phase II/III per-patient cost +8%–12% (2023–24)

- Higher recruitment costs lengthen timelines

Venture Capital and Equity Appetite

Broader economic sentiment shapes follow-on financing for clinical-stage biotech: in 2024 global VC funding to life sciences rose to about $62.5B, easing capital access for high-upside GPCR discovery platforms like Nxera.

During bull cycles investors favor early-stage platforms; 2023–2025 public biotech IPO windows showed 40–60% higher valuations versus bear phases, enhancing partnership leverage for Nxera.

Nxera must time capital raises and collaboration announcements to market cycles to maximize valuation and reduce dilution risk.

- 2024 global life sciences VC: ~$62.5B

- IPO valuation uplift in bull windows: 40–60%

- Strategy: align fundraising and partnership news with bullish biotech sentiment

Higher rates, FX swings and rising biotech costs squeeze Nxera’s valuation and cash runway

Elevated 2025 policy rates (Fed 5.25–5.50%, ECB 4.25%) raise Nxera’s discount rates, pressuring valuations and making equity/debt costlier; 2024 USD/JPY 132–153 and GBP/USD 1.20–1.35 amplified FX risk versus milestone receipts (potential $420M). 2024 biotech wage growth ~6.2% and Phase II/III per‑patient cost +8–12% increased cash burn; 2024 life‑sciences VC ~$62.5B.

| Metric | Value |

|---|---|

| Fed rate (2025) | 5.25–5.50% |

| USD/JPY (2024) | 132–153 |

| Wage growth (2024) | 6.2% |

| VC funding (2024) | $62.5B |

What You See Is What You Get

Nxera Pharma PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use, presenting a concise PESTLE analysis of Nxera Pharma covering political, economic, social, technological, legal, and environmental factors.