NYAB Porter's Five Forces Analysis

From Overview to Strategy Blueprint

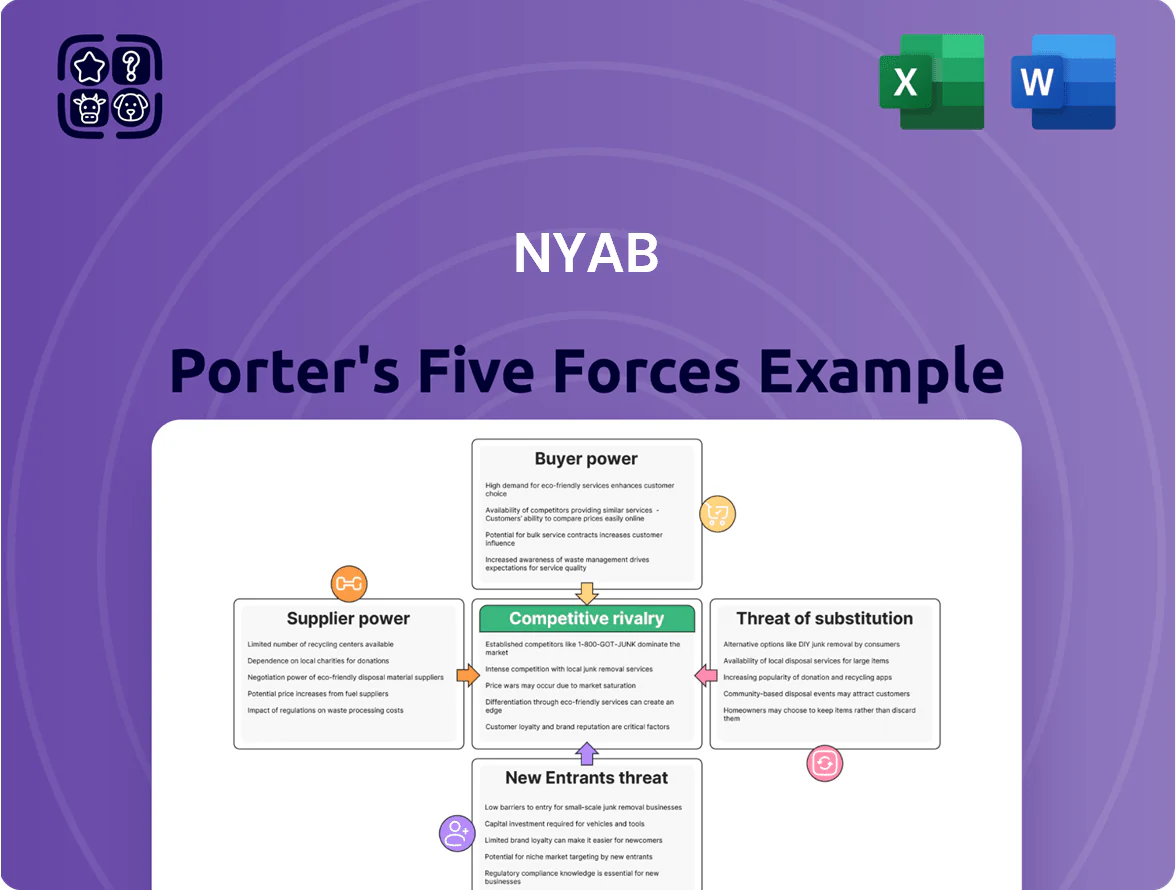

NYAB faces moderate buyer power, niche supplier leverage, and manageable new-entrant threats thanks to scale and product specialization, while rivalry intensifies around pricing and innovation—this snapshot highlights key pressures but omits granular metrics and scenario analysis.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore NYAB’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of Specialized Skilled Labor

The construction sector in Northern Europe faces a persistent shortage of engineers and technicians for renewable energy projects; Eurostat and national labor surveys show vacancy rates in green energy roles at 3.8%–5.4% in 2024, driving wage inflation of 6%–9% year-on-year. As NYAB scales through 2025, fierce competition and strong unions give workers leverage, pushing firms to spend more on training and retention—often 1%–2% of revenue—to protect project margins.

Volatility in Raw Material Pricing

Suppliers of steel, concrete and grid components hold strong leverage as global steel prices rose ~18% in 2024 and copper jumped 22% YTD to Jan 2025, so raw-material volatility can squeeze NYAB margins despite long-term procurement contracts; for example NYAB’s 2024 procurement hedges covered ~60% of forecasted inputs, leaving exposure on the rest. Limited certified green suppliers—estimated <30 global firms meeting high environmental standards—further boosts supplier bargaining power.

Dependency on Renewable Technology OEMs

NYAB depends on global OEMs for turbines, panels, and batteries; the top 10 OEMs control ~65% of wind and 70% of utility battery supply as of 2024, giving suppliers strong pricing power.

Proprietary tech and long lead times mean few substitutes; in 2023 OEM price rises (up to 12%) and 6–9 month delivery delays raised capex for many projects.

Any OEM-led disruption or tariff risk would directly increase NYAB’s unit costs and delay project cash flows, squeezing margins and ROI.

Regional Subcontractor Availability

In remote Northern Sweden and Finland, NYAB faces a thin pool of subcontractors for specialized earthworks and electrical work, raising localized supplier leverage; a 2024 Trafikverket/ELY region survey found vacancy rates for skilled construction crews above 18% in these areas. NYAB must keep preferred-vendor agreements and near-term capacity reservations to avoid 5–12% cost overruns and schedule slips.

- Limited local suppliers → higher bargaining power

- 18%+ regional crew shortages (2024)

- Preferred-vendor contracts cut 5–12% overrun risk

- Capacity reservations reduce schedule delays

Energy and Logistics Cost Inflation

Energy and transport cost inflation raises supplier power for NYAB because heavy machinery and logistics for infrastructure projects are highly energy‑intensive; diesel prices in Sweden rose ~18% in 2023 and carbon taxes added ~€30/ton CO2 in 2024, increasing operating costs for suppliers.

Nordic fuel and logistics providers have passed on green‑fuel and tax costs, squeezing margins; NYAB must boost route, fuel and equipment efficiency to shield EBIT from energy shocks.

- Diesel +18% (Sweden, 2023)

- EU carbon price ~€80/ton (2024 avg)

- Logistics surcharges up 5–12%

- Action: optimize routing, telematics, fuel contracts

Supplier power bites: metals, OEM concentration & crew shortages drive costs up

Suppliers (materials, OEMs, skilled crews, fuel/logistics) exert high bargaining power: steel +18% (2024), copper +22% (Jan 2025), top 10 OEMs = ~65–70% share, regional crew vacancies >18% (2024), diesel +18% (Sweden, 2023), EU carbon ~€80/ton (2024). NYAB hedges ~60% procurement; preferred-vendor and capacity reservations cut 5–12% overrun risk.

| Metric | Value |

|---|---|

| Steel | +18% (2024) |

| Copper | +22% (Jan 2025) |

| OEM share | 65–70% (2024) |

| Crew vacancies | >18% (2024) |

| Procurement hedge | ~60% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for NYAB that uncovers competition drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats—providing strategic insights to inform pricing, positioning, and risk mitigation.

Compact Porter's Five Forces snapshot for NYAB—quickly pinpoint competitive threats and relief strategies to streamline strategic planning.

Customers Bargaining Power

Concentration of Public Sector Clients

Northern European infrastructure spending is heavily public: in 2024 EU member states allocated about €330bn to local infrastructure, and municipalities drive large tenders that push price competition and favor proven contractors, squeezing margins; NYAB’s 2023 revenue mix showed roughly 55% from public-sector contracts, so shifts in policy or a 5–10% cut in municipal budgets could cut NYAB sales materially.

Influence of Major Energy Developers

High Standards for ESG Compliance

Nordic buyers now demand ESG transparency: 78% of Nordic institutional investors said ESG reporting is a deal-breaker in 2024, giving customers leverage to exclude contractors missing carbon targets (IEA: EU buildings CO2 cut target 60% by 2030). NYAB must upgrade green credentials—track Scope 1–3 emissions, supply-chain audits, and align with EU CSRD—to stay preferred by pension funds and corporates steering ~€1.2tn in sustainable procurement.

Competitive Bidding Dynamics

The standardized nature of many infrastructure tenders (70% of NYAB-relevant public bids in 2024) lets buyers compare on price and delivery, boosting buyer bargaining power as firms are pitted against each other in final negotiations.

NYAB counters by highlighting specialized technical expertise for complex industrial projects—areas where price matters less and lifecycle risk reduction and uptime value can justify 10–25% price premiums.

- Standardized tenders: 70% (2024 public bids)

- Buyer leverage: price + completion time focus

- NYAB differentiation: complex-industrial expertise

- Estimated premium: 10–25% on specialized contracts

Demand for Integrated Lifecycle Services

Modern buyers increasingly seek long-term partners covering design through maintenance, letting them bundle services and demand lower prices for construction work; in 2024, 58% of large UK infrastructure clients preferred integrated contracts, pressuring standalone construction margins by ~120–180 bps.

NYAB’s pivot to full lifecycle solutions targets this bargaining power, aiming for longer contracts and recurring revenue—NYAB projects lifecycle services to lift recurring revenue from 22% in 2023 to 35% by 2026.

- 58% large clients prefer integrated contracts (2024)

- Construction margin squeeze ~120–180 bps

- NYAB recurring rev 22% (2023) → est. 35% (2026)

Public tenders squeeze margins as NYAB pivots to recurring, ESG-driven revenues

Northern Europe public tenders drive price pressure—€330bn infra spend (2024); 70% of public bids standardized; 55% of NYAB revenue from public contracts. Large private developers (top 10 = ~35% US additions, 2024) demand integrated EPC+O&M, trimming EPC margins ~2–4 ppt. ESG rules matter: 78% Nordic investors require ESG reporting (2024). NYAB aims to lift recurring rev 22% (2023) → 35% (2026).

| Metric | 2023–2026 |

|---|---|

| Public infra spend (EU) | €330bn (2024) |

| Standardized public bids | 70% (2024) |

| NYAB public revenue | 55% (2023) |

| Top developers share | 35% US additions (2024) |

| ESG deal-breakers | 78% Nordic investors (2024) |

| EPC margin squeeze | −2–4 ppt (2023–24) |

| Recurring rev | 22% (2023) → 35% (est. 2026) |

Same Document Delivered

NYAB Porter's Five Forces Analysis

This preview shows the exact NYAB Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders, and fully formatted for use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

NYAB faces moderate buyer power, niche supplier leverage, and manageable new-entrant threats thanks to scale and product specialization, while rivalry intensifies around pricing and innovation—this snapshot highlights key pressures but omits granular metrics and scenario analysis.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore NYAB’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of Specialized Skilled Labor

The construction sector in Northern Europe faces a persistent shortage of engineers and technicians for renewable energy projects; Eurostat and national labor surveys show vacancy rates in green energy roles at 3.8%–5.4% in 2024, driving wage inflation of 6%–9% year-on-year. As NYAB scales through 2025, fierce competition and strong unions give workers leverage, pushing firms to spend more on training and retention—often 1%–2% of revenue—to protect project margins.

Volatility in Raw Material Pricing

Suppliers of steel, concrete and grid components hold strong leverage as global steel prices rose ~18% in 2024 and copper jumped 22% YTD to Jan 2025, so raw-material volatility can squeeze NYAB margins despite long-term procurement contracts; for example NYAB’s 2024 procurement hedges covered ~60% of forecasted inputs, leaving exposure on the rest. Limited certified green suppliers—estimated <30 global firms meeting high environmental standards—further boosts supplier bargaining power.

Dependency on Renewable Technology OEMs

NYAB depends on global OEMs for turbines, panels, and batteries; the top 10 OEMs control ~65% of wind and 70% of utility battery supply as of 2024, giving suppliers strong pricing power.

Proprietary tech and long lead times mean few substitutes; in 2023 OEM price rises (up to 12%) and 6–9 month delivery delays raised capex for many projects.

Any OEM-led disruption or tariff risk would directly increase NYAB’s unit costs and delay project cash flows, squeezing margins and ROI.

Regional Subcontractor Availability

In remote Northern Sweden and Finland, NYAB faces a thin pool of subcontractors for specialized earthworks and electrical work, raising localized supplier leverage; a 2024 Trafikverket/ELY region survey found vacancy rates for skilled construction crews above 18% in these areas. NYAB must keep preferred-vendor agreements and near-term capacity reservations to avoid 5–12% cost overruns and schedule slips.

- Limited local suppliers → higher bargaining power

- 18%+ regional crew shortages (2024)

- Preferred-vendor contracts cut 5–12% overrun risk

- Capacity reservations reduce schedule delays

Energy and Logistics Cost Inflation

Energy and transport cost inflation raises supplier power for NYAB because heavy machinery and logistics for infrastructure projects are highly energy‑intensive; diesel prices in Sweden rose ~18% in 2023 and carbon taxes added ~€30/ton CO2 in 2024, increasing operating costs for suppliers.

Nordic fuel and logistics providers have passed on green‑fuel and tax costs, squeezing margins; NYAB must boost route, fuel and equipment efficiency to shield EBIT from energy shocks.

- Diesel +18% (Sweden, 2023)

- EU carbon price ~€80/ton (2024 avg)

- Logistics surcharges up 5–12%

- Action: optimize routing, telematics, fuel contracts

Supplier power bites: metals, OEM concentration & crew shortages drive costs up

Suppliers (materials, OEMs, skilled crews, fuel/logistics) exert high bargaining power: steel +18% (2024), copper +22% (Jan 2025), top 10 OEMs = ~65–70% share, regional crew vacancies >18% (2024), diesel +18% (Sweden, 2023), EU carbon ~€80/ton (2024). NYAB hedges ~60% procurement; preferred-vendor and capacity reservations cut 5–12% overrun risk.

| Metric | Value |

|---|---|

| Steel | +18% (2024) |

| Copper | +22% (Jan 2025) |

| OEM share | 65–70% (2024) |

| Crew vacancies | >18% (2024) |

| Procurement hedge | ~60% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for NYAB that uncovers competition drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats—providing strategic insights to inform pricing, positioning, and risk mitigation.

Compact Porter's Five Forces snapshot for NYAB—quickly pinpoint competitive threats and relief strategies to streamline strategic planning.

Customers Bargaining Power

Concentration of Public Sector Clients

Northern European infrastructure spending is heavily public: in 2024 EU member states allocated about €330bn to local infrastructure, and municipalities drive large tenders that push price competition and favor proven contractors, squeezing margins; NYAB’s 2023 revenue mix showed roughly 55% from public-sector contracts, so shifts in policy or a 5–10% cut in municipal budgets could cut NYAB sales materially.

Influence of Major Energy Developers

High Standards for ESG Compliance

Nordic buyers now demand ESG transparency: 78% of Nordic institutional investors said ESG reporting is a deal-breaker in 2024, giving customers leverage to exclude contractors missing carbon targets (IEA: EU buildings CO2 cut target 60% by 2030). NYAB must upgrade green credentials—track Scope 1–3 emissions, supply-chain audits, and align with EU CSRD—to stay preferred by pension funds and corporates steering ~€1.2tn in sustainable procurement.

Competitive Bidding Dynamics

The standardized nature of many infrastructure tenders (70% of NYAB-relevant public bids in 2024) lets buyers compare on price and delivery, boosting buyer bargaining power as firms are pitted against each other in final negotiations.

NYAB counters by highlighting specialized technical expertise for complex industrial projects—areas where price matters less and lifecycle risk reduction and uptime value can justify 10–25% price premiums.

- Standardized tenders: 70% (2024 public bids)

- Buyer leverage: price + completion time focus

- NYAB differentiation: complex-industrial expertise

- Estimated premium: 10–25% on specialized contracts

Demand for Integrated Lifecycle Services

Modern buyers increasingly seek long-term partners covering design through maintenance, letting them bundle services and demand lower prices for construction work; in 2024, 58% of large UK infrastructure clients preferred integrated contracts, pressuring standalone construction margins by ~120–180 bps.

NYAB’s pivot to full lifecycle solutions targets this bargaining power, aiming for longer contracts and recurring revenue—NYAB projects lifecycle services to lift recurring revenue from 22% in 2023 to 35% by 2026.

- 58% large clients prefer integrated contracts (2024)

- Construction margin squeeze ~120–180 bps

- NYAB recurring rev 22% (2023) → est. 35% (2026)

Public tenders squeeze margins as NYAB pivots to recurring, ESG-driven revenues

Northern Europe public tenders drive price pressure—€330bn infra spend (2024); 70% of public bids standardized; 55% of NYAB revenue from public contracts. Large private developers (top 10 = ~35% US additions, 2024) demand integrated EPC+O&M, trimming EPC margins ~2–4 ppt. ESG rules matter: 78% Nordic investors require ESG reporting (2024). NYAB aims to lift recurring rev 22% (2023) → 35% (2026).

| Metric | 2023–2026 |

|---|---|

| Public infra spend (EU) | €330bn (2024) |

| Standardized public bids | 70% (2024) |

| NYAB public revenue | 55% (2023) |

| Top developers share | 35% US additions (2024) |

| ESG deal-breakers | 78% Nordic investors (2024) |

| EPC margin squeeze | −2–4 ppt (2023–24) |

| Recurring rev | 22% (2023) → 35% (est. 2026) |

Same Document Delivered

NYAB Porter's Five Forces Analysis

This preview shows the exact NYAB Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders, and fully formatted for use.