The New York Times SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

The New York Times combines strong brand recognition, digital subscription growth, and journalistic credibility with challenges from ad revenue shifts and competition in digital news; our full SWOT unpacks these dynamics with financial context and strategic recommendations. Purchase the complete analysis to access a professionally written, editable report and Excel matrix—ideal for investors, analysts, and strategists seeking actionable insights.

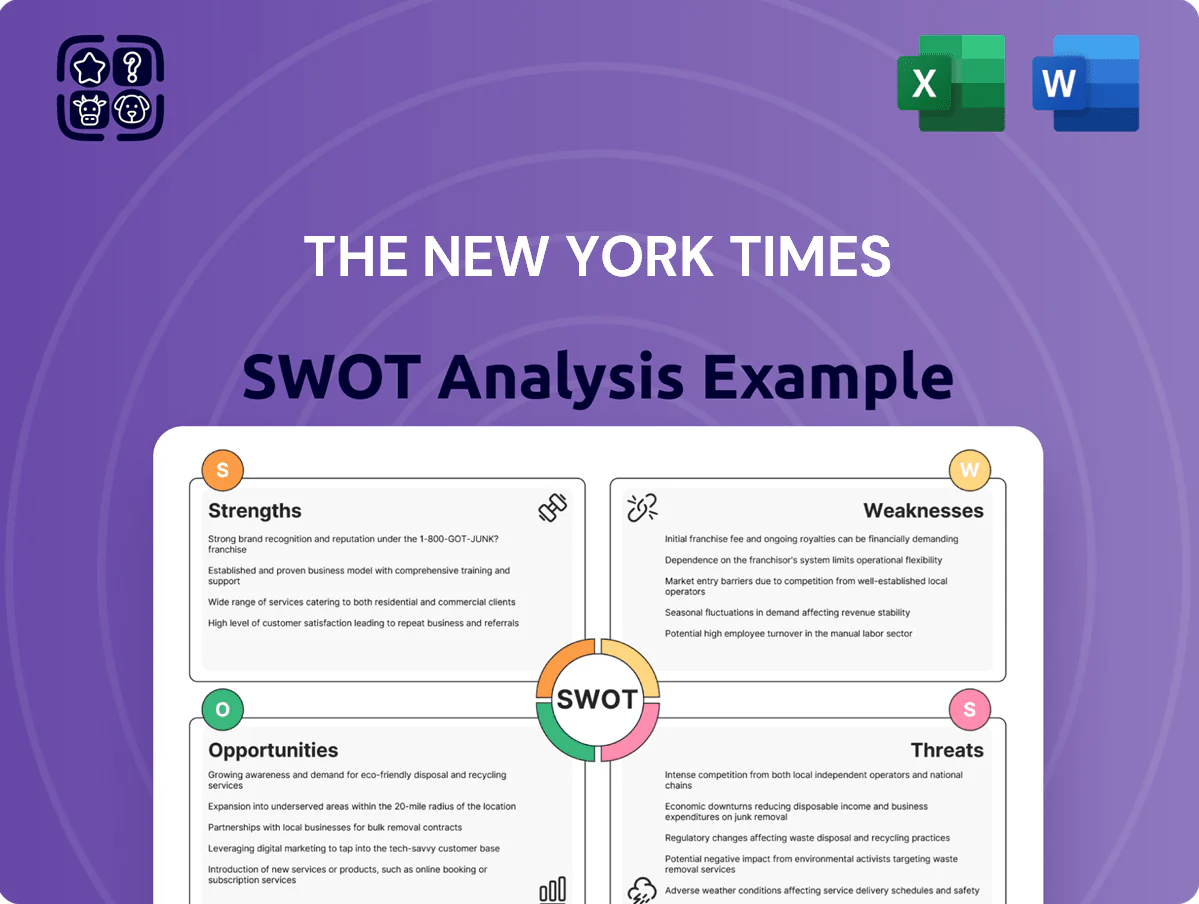

Strengths

Robust Digital Subscription Bundle

The New York Times shifted to a digital-first bundle—News, Games, Cooking, Wirecutter, The Athletic—lifting ARPU and lowering churn by embedding daily habits; by end-2025 paid digital subscriptions reached ~11.9 million and subscription revenue totaled $2.3 billion, giving a steadier recurring stream versus ad-driven outlets.

High Journalistic Brand Equity

The New York Times holds strong global brand equity—ranked 6th in the 2024 Brand Finance Media 50—anchoring trust against low-quality AI content and boosting subscription pricing power (paid subs 9.3M, Q4 2024).

Advertisers pay premiums for a brand-safe environment; NYT reported digital ad revenue of $514M in 2024, reflecting demand for reputable inventory.

In a misinformation era, the masthead drives acquisition and retention: 73% of readers cite trust as a primary reason for subscribing (NYT 2024 reader survey).

Diversified and Resilient Revenue Mix

Strong Balance Sheet and Cash Position

The New York Times Company held $1.0 billion in cash and equivalents and had long-term debt of $206 million as of Dec 31, 2024, giving it low leverage and strong liquidity.

This cash strength lets NYT fund acquisitions (e.g., Wordle-related deals), invest in AI-driven products and journalism tech, and support $100 million buyback authorization announced in 2024.

First-Party Data Advantage

The New York Times holds ~10.9 million paid subscriptions worldwide as of Q4 2025 and millions more registered users, creating a vast proprietary first-party data set for precise ad targeting and personalized recommendations.

Relying on its internal data avoids the shrinking third-party cookie pool and supports higher CPMs in premium ad deals; first-party signals also drive product experiments and retention strategies amid stricter privacy rules.

As GDPR-like laws and cookieless shifts raise ad costs and uncertainty, NYT’s owned data becomes a strategic moat for monetization and product differentiation.

- ~10.9M paid subs (Q4 2025)

- Higher CPMs from premium, privacy-safe targeting

- Enables personalized recommendations and retention

- Reduces reliance on third-party cookies

NYT’s subscription-led growth: 10.9M subs, $2.3B revenue, $1B cash, low debt

NYT’s digital-first bundle and strong brand drove ~10.9M paid subs (Q4 2025), $2.3B subscription revenue (2025), $514M digital ad revenue (2024), ~60% revenue from subscriptions (2024), $1.0B cash vs $206M long-term debt (Dec 31, 2024), and $100M buyback (2024), creating recurring revenue, high CPMs, first-party data, and low leverage.

| Metric | Value |

|---|---|

| Paid subs | 10.9M (Q4 2025) |

| Subscription rev | $2.3B (2025) |

| Digital ad rev | $514M (2024) |

| Cash / Debt | $1.0B / $206M (Dec 31, 2024) |

What is included in the product

Provides a clear SWOT framework analyzing The New York Times’s strategic strengths, weaknesses, opportunities, and threats to assess its competitive position and future growth prospects.

Offers a clear SWOT snapshot of The New York Times to quickly align digital and editorial strategies for executives and teams.

Weaknesses

Ongoing Decline of Print Operations

The New York Times faces a structural decline in print: U.S. weekday circulation fell about 6% year-over-year to ~650,000 in 2024 while print ad revenue dropped ~9% vs 2023, yet print still carries heavy fixed costs—printing, paper, distribution—and represented roughly 18% of operating expenses in FY2024; shifting away risks alienating older, higher-paying subscribers, and the cost of sustaining print operations continues to drag corporate margins.

High Sensitivity to Labor Costs

Maintaining a world-class newsroom and competitive tech staff demands heavy human-capital spending, leaving The New York Times vulnerable to wage inflation after 2023 union wins that raised newsroom pay by roughly 10–15% and tech headcount growth of ~8% in 2024.

Frequent contract talks with multiple unions and NYC’s 2025 median rent of $4,200/mo push operating costs higher, contributing to personnel expenses that were 45% of total operating costs in 2024.

Prolonged strikes—like the 2022 newsworker action that paused some coverage—could halt content production, erode subscription growth (NYT added 2.3M subs in 2024) and harm brand trust.

Market Saturation in the United States

The New York Times has saturated the US college-educated market—about 6.7 million subscribers by Q4 2025—raising marginal customer acquisition costs as remaining readers are harder to convert.

Core demographic penetration is near peak in major metros, so domestic growth is slowing: US subscription growth fell to 3.2% YoY in 2025, down from 8.1% in 2021.

That forces a costly pivot to international expansion, where NYT spent $120m on content and marketing in 2024, a risky move to sustain top-line growth.

Dependence on Third-Party Platform Algorithms

A large share of audience discovery for The New York Times still depends on Google, Meta, and Apple; in 2024, referrals from external platforms accounted for roughly 28% of site traffic, so algorithm tweaks by these firms cause volatile referral swings.

These algorithm shifts can cut top-of-funnel reach quickly, raising CAC (customer acquisition cost) and weakening subscription funnel predictability; NYT reported a 6% QoQ referral traffic drop after a 2024 algorithm change.

The Times is partly beholden to tech giants whose product and revenue priorities may conflict with quality journalism, leaving strategic exposure despite NYT’s growing direct and subscription revenues (2024 subscription revenue about $2.1 billion).

- ~28% traffic from external referrals (2024)

- 6% QoQ referral drop after a 2024 algorithm change

- Subscription revenue ≈ $2.1B (2024)

Complexity of Multi-Product Integration

Managing a diverse portfolio—from NYT Cooking (6.5m subscribers across the platform in 2024) to The Athletic and Games—adds technical and organizational complexity that raises engineering costs (NYT reported $1.1B in tech/content costs in FY2024).

Maintaining seamless UX across apps demands continuous investment; missed integrations risk fragmenting users and diluting The New York Times brand.

- 6.5m Cooking users (2024)

- $1.1B tech/content costs (FY2024)

- Risk: UX fragmentation → subscriber churn

Margin squeeze: high fixed costs, saturated US market, platform dependence

Heavy fixed costs from declining print (weekday circulation ~650,000 in 2024; print ad revenue -9% YoY) and high personnel spend (personnel 45% of operating costs in 2024; post‑2023 wage rises ~10–15%) compress margins; US market saturation (6.7M US subs by Q4 2025; US sub growth 3.2% in 2025) raises CAC; dependence on platform referrals (~28% traffic 2024) creates volatility; tech/content costs $1.1B (FY2024) strain scaling.

| Metric | Value |

|---|---|

| Weekday circulation (2024) | ~650,000 |

| Print ad rev change (2024 vs 2023) | -9% |

| Personnel % of ops (2024) | 45% |

| US subscribers (Q4 2025) | 6.7M |

| US sub growth (2025) | 3.2% YoY |

| External referrals (2024) | ~28% traffic |

| Tech/content costs (FY2024) | $1.1B |

Same Document Delivered

The New York Times SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final, editable file. You’re viewing a live preview of the real analysis document; buy now to unlock the complete, detailed version. The full, structured report becomes available immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

The New York Times combines strong brand recognition, digital subscription growth, and journalistic credibility with challenges from ad revenue shifts and competition in digital news; our full SWOT unpacks these dynamics with financial context and strategic recommendations. Purchase the complete analysis to access a professionally written, editable report and Excel matrix—ideal for investors, analysts, and strategists seeking actionable insights.

Strengths

Robust Digital Subscription Bundle

The New York Times shifted to a digital-first bundle—News, Games, Cooking, Wirecutter, The Athletic—lifting ARPU and lowering churn by embedding daily habits; by end-2025 paid digital subscriptions reached ~11.9 million and subscription revenue totaled $2.3 billion, giving a steadier recurring stream versus ad-driven outlets.

High Journalistic Brand Equity

The New York Times holds strong global brand equity—ranked 6th in the 2024 Brand Finance Media 50—anchoring trust against low-quality AI content and boosting subscription pricing power (paid subs 9.3M, Q4 2024).

Advertisers pay premiums for a brand-safe environment; NYT reported digital ad revenue of $514M in 2024, reflecting demand for reputable inventory.

In a misinformation era, the masthead drives acquisition and retention: 73% of readers cite trust as a primary reason for subscribing (NYT 2024 reader survey).

Diversified and Resilient Revenue Mix

Strong Balance Sheet and Cash Position

The New York Times Company held $1.0 billion in cash and equivalents and had long-term debt of $206 million as of Dec 31, 2024, giving it low leverage and strong liquidity.

This cash strength lets NYT fund acquisitions (e.g., Wordle-related deals), invest in AI-driven products and journalism tech, and support $100 million buyback authorization announced in 2024.

First-Party Data Advantage

The New York Times holds ~10.9 million paid subscriptions worldwide as of Q4 2025 and millions more registered users, creating a vast proprietary first-party data set for precise ad targeting and personalized recommendations.

Relying on its internal data avoids the shrinking third-party cookie pool and supports higher CPMs in premium ad deals; first-party signals also drive product experiments and retention strategies amid stricter privacy rules.

As GDPR-like laws and cookieless shifts raise ad costs and uncertainty, NYT’s owned data becomes a strategic moat for monetization and product differentiation.

- ~10.9M paid subs (Q4 2025)

- Higher CPMs from premium, privacy-safe targeting

- Enables personalized recommendations and retention

- Reduces reliance on third-party cookies

NYT’s subscription-led growth: 10.9M subs, $2.3B revenue, $1B cash, low debt

NYT’s digital-first bundle and strong brand drove ~10.9M paid subs (Q4 2025), $2.3B subscription revenue (2025), $514M digital ad revenue (2024), ~60% revenue from subscriptions (2024), $1.0B cash vs $206M long-term debt (Dec 31, 2024), and $100M buyback (2024), creating recurring revenue, high CPMs, first-party data, and low leverage.

| Metric | Value |

|---|---|

| Paid subs | 10.9M (Q4 2025) |

| Subscription rev | $2.3B (2025) |

| Digital ad rev | $514M (2024) |

| Cash / Debt | $1.0B / $206M (Dec 31, 2024) |

What is included in the product

Provides a clear SWOT framework analyzing The New York Times’s strategic strengths, weaknesses, opportunities, and threats to assess its competitive position and future growth prospects.

Offers a clear SWOT snapshot of The New York Times to quickly align digital and editorial strategies for executives and teams.

Weaknesses

Ongoing Decline of Print Operations

The New York Times faces a structural decline in print: U.S. weekday circulation fell about 6% year-over-year to ~650,000 in 2024 while print ad revenue dropped ~9% vs 2023, yet print still carries heavy fixed costs—printing, paper, distribution—and represented roughly 18% of operating expenses in FY2024; shifting away risks alienating older, higher-paying subscribers, and the cost of sustaining print operations continues to drag corporate margins.

High Sensitivity to Labor Costs

Maintaining a world-class newsroom and competitive tech staff demands heavy human-capital spending, leaving The New York Times vulnerable to wage inflation after 2023 union wins that raised newsroom pay by roughly 10–15% and tech headcount growth of ~8% in 2024.

Frequent contract talks with multiple unions and NYC’s 2025 median rent of $4,200/mo push operating costs higher, contributing to personnel expenses that were 45% of total operating costs in 2024.

Prolonged strikes—like the 2022 newsworker action that paused some coverage—could halt content production, erode subscription growth (NYT added 2.3M subs in 2024) and harm brand trust.

Market Saturation in the United States

The New York Times has saturated the US college-educated market—about 6.7 million subscribers by Q4 2025—raising marginal customer acquisition costs as remaining readers are harder to convert.

Core demographic penetration is near peak in major metros, so domestic growth is slowing: US subscription growth fell to 3.2% YoY in 2025, down from 8.1% in 2021.

That forces a costly pivot to international expansion, where NYT spent $120m on content and marketing in 2024, a risky move to sustain top-line growth.

Dependence on Third-Party Platform Algorithms

A large share of audience discovery for The New York Times still depends on Google, Meta, and Apple; in 2024, referrals from external platforms accounted for roughly 28% of site traffic, so algorithm tweaks by these firms cause volatile referral swings.

These algorithm shifts can cut top-of-funnel reach quickly, raising CAC (customer acquisition cost) and weakening subscription funnel predictability; NYT reported a 6% QoQ referral traffic drop after a 2024 algorithm change.

The Times is partly beholden to tech giants whose product and revenue priorities may conflict with quality journalism, leaving strategic exposure despite NYT’s growing direct and subscription revenues (2024 subscription revenue about $2.1 billion).

- ~28% traffic from external referrals (2024)

- 6% QoQ referral drop after a 2024 algorithm change

- Subscription revenue ≈ $2.1B (2024)

Complexity of Multi-Product Integration

Managing a diverse portfolio—from NYT Cooking (6.5m subscribers across the platform in 2024) to The Athletic and Games—adds technical and organizational complexity that raises engineering costs (NYT reported $1.1B in tech/content costs in FY2024).

Maintaining seamless UX across apps demands continuous investment; missed integrations risk fragmenting users and diluting The New York Times brand.

- 6.5m Cooking users (2024)

- $1.1B tech/content costs (FY2024)

- Risk: UX fragmentation → subscriber churn

Margin squeeze: high fixed costs, saturated US market, platform dependence

Heavy fixed costs from declining print (weekday circulation ~650,000 in 2024; print ad revenue -9% YoY) and high personnel spend (personnel 45% of operating costs in 2024; post‑2023 wage rises ~10–15%) compress margins; US market saturation (6.7M US subs by Q4 2025; US sub growth 3.2% in 2025) raises CAC; dependence on platform referrals (~28% traffic 2024) creates volatility; tech/content costs $1.1B (FY2024) strain scaling.

| Metric | Value |

|---|---|

| Weekday circulation (2024) | ~650,000 |

| Print ad rev change (2024 vs 2023) | -9% |

| Personnel % of ops (2024) | 45% |

| US subscribers (Q4 2025) | 6.7M |

| US sub growth (2025) | 3.2% YoY |

| External referrals (2024) | ~28% traffic |

| Tech/content costs (FY2024) | $1.1B |

Same Document Delivered

The New York Times SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final, editable file. You’re viewing a live preview of the real analysis document; buy now to unlock the complete, detailed version. The full, structured report becomes available immediately after checkout.