Oceana Group PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic tides, and environmental pressures are reshaping Oceana Group’s prospects in our concise PESTLE snapshot—ideal for investors and strategists who need quick, actionable context. Purchase the full PESTLE Analysis to unlock detailed risk assessments, trend-driven opportunities, and editable insights you can use immediately.

Political factors

Fishing Rights Allocation Process

The South African government's long-term fishing rights allocation is a key driver of Oceana's stability, with quota renewals in late 2025 affecting allowable catch volumes for hake and horse mackerel—species that contributed about 62% of Oceana's 2024 seafood revenue of R3.2bn.

Geopolitical Trade Relations

Oceana's Daybrook Fisheries, representing roughly 12% of group revenue in FY2024, exposes the company to US trade policy shifts; changes in Washington can affect tariffs and maritime rules that impact margins on fishmeal and fish oil exports.

In 2024 the US imposed tighter import controls on feed additives, risking a 3-5% price impact on Oceana's North American sales if mirrored for marine-derived products.

Maintaining compliant operations and supply-chain flexibility in North America helps hedge political risk elsewhere, supporting resilience for Oceana's global 2024 export base of about 45,000 tonnes of fishmeal and oil.

Regional Stability in Africa

Operating across 12 African jurisdictions exposes Oceana Group to diverse political landscapes and regulatory shifts; in 2024, 38% of its revenue derived from African markets, heightening sensitivity to local policy changes.

Political volatility in neighboring coastal nations can disrupt fishing licenses and maritime safety, with UN data noting 24% of African coastal states experienced maritime security incidents in 2023–24.

Oceana must pursue proactive diplomacy and community investment—its R10m+ annual CSR and stakeholder engagement programs help safeguard assets and stabilize supply chains amid regional instability.

Government Food Security Initiatives

Canned fish like Lucky Star supply ~30% of affordable animal protein in parts of Southern Africa and are embedded in national food security programs; Oceana reported R6.2bn revenue from its consumer brands in FY2025, highlighting scale in these initiatives.

Political pressure to curb food inflation (South Africa CPI peaked 7.8% in 2024) forces Oceana to adjust pricing and expand low-cost distribution, affecting margins but protecting volume.

Aligning with national nutrition goals secures procurement support and social license, evidenced by government partnerships and targeted school feeding program contracts covering an estimated 1.2 million beneficiaries in 2024.

- Lucky Star ≈30% affordable animal protein supply in region

- Oceana consumer revenue R6.2bn FY2025

- SA CPI peak 7.8% (2024) influences pricing

- School feeding reach ≈1.2m beneficiaries (2024)

Global Maritime Governance

International agreements on high-seas fishing and marine protected areas constrain Oceana Group’s fleet deployment, with 2024 UN FAO estimates showing 34% of global stocks fully exploited, pushing firms toward compliant zones.

Active participation in IMO and regional fisheries management organizations helps Oceana shape rules; in 2025 the company reported engagement in 6 multilateral forums to protect export routes.

Compliance with global standards prevents sanctions and preserves access to markets—EU and US seafood import compliance audits affected 12% of exporters in 2024, risking revenue loss if noncompliant.

- 34% global stocks fully exploited (FAO 2024)

- 6 multilateral forums engaged (Oceana 2025)

- 12% of exporters impacted by import audits (EU/US 2024)

Oceana faces quota, trade risks as hake/horse mackerel and Africa exposure squeeze margins

Government fisheries quotas (renewals late‑2025) and trade policy shifts in the US/EU critically affect Oceana’s catch volumes and margins; hake/horse mackerel = ~62% of 2024 seafood revenue (R3.2bn). Political instability across 12 African jurisdictions (38% revenue, 2024) and food‑security pressure (SA CPI 7.8% 2024) force pricing and CSR strategies (R10m+ pa).

| Metric | Value |

|---|---|

| Hake/horse mackerel share | 62% (2024) |

| Seafood revenue | R3.2bn (2024) |

| Consumer revenue | R6.2bn (FY2025) |

| African revenue share | 38% (2024) |

| SA CPI peak | 7.8% (2024) |

What is included in the product

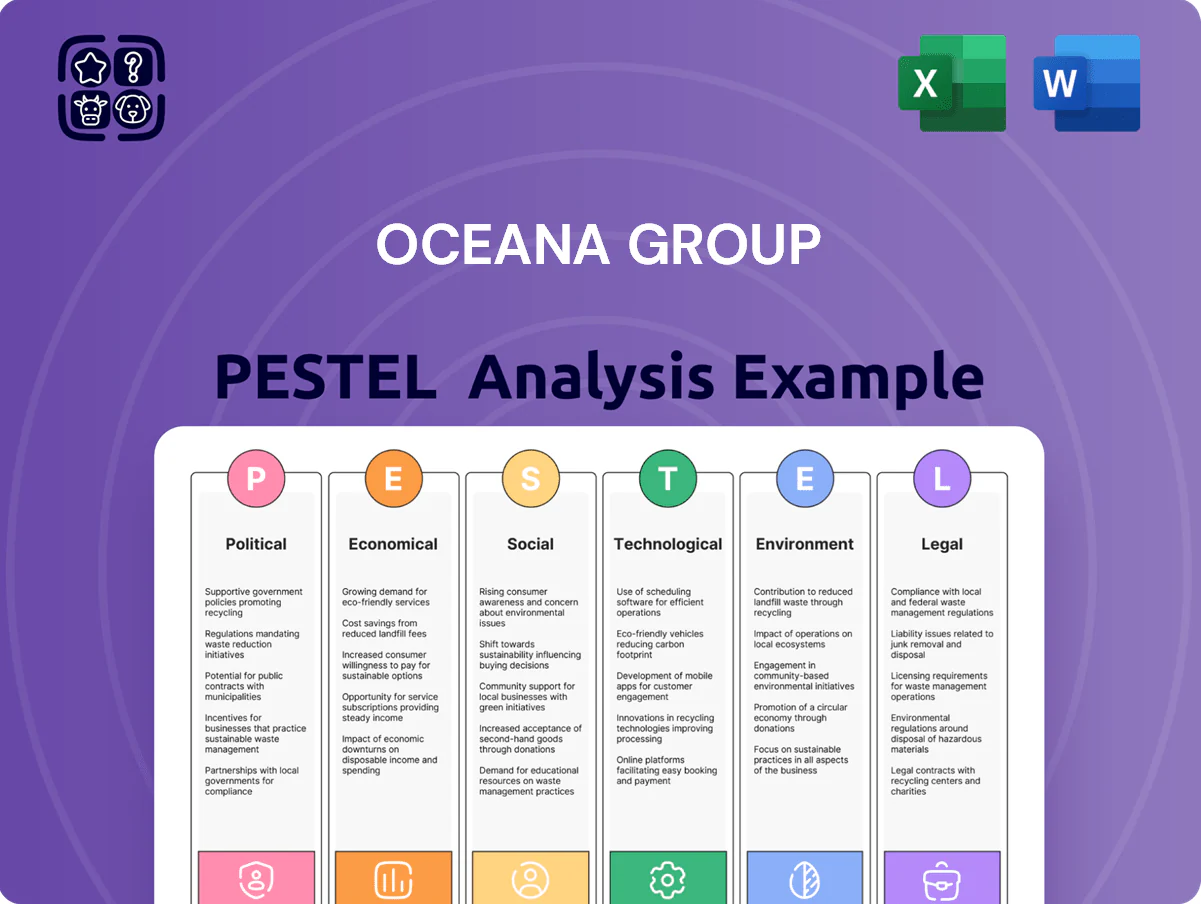

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Oceana Group, combining region- and industry-specific data with forward-looking insights to identify risks and opportunities for executives and investors.

A concise Oceana Group PESTLE summary that’s easy to drop into presentations, quickly highlighting regulatory, environmental, and market risks to streamline strategic discussions.

Economic factors

Exchange Rate Volatility

Oceana Group reports in ZAR while around 40–60% of revenue is dollar-denominated from exports, so a 10% depreciation of ZAR/USD (e.g., ZAR weakening from 18 to ~19.8 in 2024–25 ranges) can materially boost translated revenues but raise USD-priced input costs; in 2024 Oceana noted FX swings that affected margins. Strategic hedging programs—forwards and options—remain essential to stabilise margins amid ZAR volatility.

Global Commodity Pricing

Global fishmeal and fish oil prices are tightly linked to Peruvian anchovy harvests; 2024 saw fishmeal average c. US$1,100/tonne and fish oil US$2,300/tonne amid strong aquaculture demand, supporting Oceana's industrial product margins.

Should commodity downturns occur, Oceana must pivot toward higher-margin retail seafood—retail margins were ~15–20% vs industrial ~5–8% in FY2024—to preserve profitability.

Inflationary Pressure on Consumers

Rising living costs in South Africa—CPI at 5.4% in 2025 vs 4.6% in 2023—erode purchasing power for lower-to-middle income consumers, pressuring demand for everyday staples. While canned pilchards remain a lower-cost protein, sustained inflation can trigger down-trading to cheaper brands or reduced pack consumption, lowering volume sales. Oceana pursues operational efficiencies—announced 2024 cost-savings of ~R120m—to keep shelf prices stable amid higher logistics and packaging input costs.

Fuel and Energy Costs

The fishing sector is energy-intensive: fuel and electricity account for about 18–22% of operating costs for fleet and processing; Oceana reported fuel-related costs rising 14% in FY2024, squeezing margins.

Global Brent oil volatility (2023–2025 avg ~US$80–95/bbl) directly shifts fleet operating margins seasonally, increasing cash-cost risk.

Oceana’s capex into fuel-efficient engines and 5–12 MW renewable PV projects at plants aims to cut energy spend 8–15% over 3–5 years.

- Fuel/electricity = 18–22% of costs

- FY2024 fuel costs +14%

- Brent ~US$80–95/bbl (2023–25)

- Capex targets 8–15% energy savings

Interest Rate Environment

Prevailing interest rates in South Africa (repo 8.25% as of Dec 2025) and the US (federal funds 5.25–5.50% in Dec 2025) raise Oceana Group’s debt servicing costs and lift the discount rate for new projects, tightening ROI thresholds.

High rates constrain expansion and fleet modernization by increasing capital costs and required hurdle rates for acquisitions.

Oceana prioritizes a conservative debt-to-equity stance—net debt/EBITDA targets and liquidity buffers—to remain resilient through monetary tightening.

- SA repo ~8.25% (Dec 2025)

- US federal funds 5.25–5.50% (Dec 2025)

- Higher rates → higher debt servicing and hurdle rates

- Focus on healthy net debt/EBITDA and liquidity

Oceana: ZAR swings, rising energy & rates pressure margins despite retail shield

Oceana’s revenue exposure (40–60% USD) makes ZAR moves key—10% ZAR depreciation can boost translated revenue but raise USD input costs; FY2024 FX swings impacted margins. Global fishmeal/fish oil (2024 avg ~US$1,100/US$2,300/tonne) sustain industrial margins, while retail margins (~15–20% vs industrial 5–8% FY2024) shield profits. Energy (fuel/electricity 18–22% of costs; fuel +14% FY2024) and higher rates (SA repo ~8.25% Dec‑2025) raise operating and capital costs.

| Metric | Value |

|---|---|

| USD revenue share | 40–60% |

| Fishmeal / Fish oil 2024 | ~US$1,100 / US$2,300/tonne |

| Retail margin (FY2024) | 15–20% |

| Industrial margin (FY2024) | 5–8% |

| Fuel/electricity % costs | 18–22% |

| Fuel cost change FY2024 | +14% |

| SA repo (Dec‑2025) | ~8.25% |

Preview the Actual Deliverable

Oceana Group PESTLE Analysis

The preview shown here is the exact Oceana Group PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic tides, and environmental pressures are reshaping Oceana Group’s prospects in our concise PESTLE snapshot—ideal for investors and strategists who need quick, actionable context. Purchase the full PESTLE Analysis to unlock detailed risk assessments, trend-driven opportunities, and editable insights you can use immediately.

Political factors

Fishing Rights Allocation Process

The South African government's long-term fishing rights allocation is a key driver of Oceana's stability, with quota renewals in late 2025 affecting allowable catch volumes for hake and horse mackerel—species that contributed about 62% of Oceana's 2024 seafood revenue of R3.2bn.

Geopolitical Trade Relations

Oceana's Daybrook Fisheries, representing roughly 12% of group revenue in FY2024, exposes the company to US trade policy shifts; changes in Washington can affect tariffs and maritime rules that impact margins on fishmeal and fish oil exports.

In 2024 the US imposed tighter import controls on feed additives, risking a 3-5% price impact on Oceana's North American sales if mirrored for marine-derived products.

Maintaining compliant operations and supply-chain flexibility in North America helps hedge political risk elsewhere, supporting resilience for Oceana's global 2024 export base of about 45,000 tonnes of fishmeal and oil.

Regional Stability in Africa

Operating across 12 African jurisdictions exposes Oceana Group to diverse political landscapes and regulatory shifts; in 2024, 38% of its revenue derived from African markets, heightening sensitivity to local policy changes.

Political volatility in neighboring coastal nations can disrupt fishing licenses and maritime safety, with UN data noting 24% of African coastal states experienced maritime security incidents in 2023–24.

Oceana must pursue proactive diplomacy and community investment—its R10m+ annual CSR and stakeholder engagement programs help safeguard assets and stabilize supply chains amid regional instability.

Government Food Security Initiatives

Canned fish like Lucky Star supply ~30% of affordable animal protein in parts of Southern Africa and are embedded in national food security programs; Oceana reported R6.2bn revenue from its consumer brands in FY2025, highlighting scale in these initiatives.

Political pressure to curb food inflation (South Africa CPI peaked 7.8% in 2024) forces Oceana to adjust pricing and expand low-cost distribution, affecting margins but protecting volume.

Aligning with national nutrition goals secures procurement support and social license, evidenced by government partnerships and targeted school feeding program contracts covering an estimated 1.2 million beneficiaries in 2024.

- Lucky Star ≈30% affordable animal protein supply in region

- Oceana consumer revenue R6.2bn FY2025

- SA CPI peak 7.8% (2024) influences pricing

- School feeding reach ≈1.2m beneficiaries (2024)

Global Maritime Governance

International agreements on high-seas fishing and marine protected areas constrain Oceana Group’s fleet deployment, with 2024 UN FAO estimates showing 34% of global stocks fully exploited, pushing firms toward compliant zones.

Active participation in IMO and regional fisheries management organizations helps Oceana shape rules; in 2025 the company reported engagement in 6 multilateral forums to protect export routes.

Compliance with global standards prevents sanctions and preserves access to markets—EU and US seafood import compliance audits affected 12% of exporters in 2024, risking revenue loss if noncompliant.

- 34% global stocks fully exploited (FAO 2024)

- 6 multilateral forums engaged (Oceana 2025)

- 12% of exporters impacted by import audits (EU/US 2024)

Oceana faces quota, trade risks as hake/horse mackerel and Africa exposure squeeze margins

Government fisheries quotas (renewals late‑2025) and trade policy shifts in the US/EU critically affect Oceana’s catch volumes and margins; hake/horse mackerel = ~62% of 2024 seafood revenue (R3.2bn). Political instability across 12 African jurisdictions (38% revenue, 2024) and food‑security pressure (SA CPI 7.8% 2024) force pricing and CSR strategies (R10m+ pa).

| Metric | Value |

|---|---|

| Hake/horse mackerel share | 62% (2024) |

| Seafood revenue | R3.2bn (2024) |

| Consumer revenue | R6.2bn (FY2025) |

| African revenue share | 38% (2024) |

| SA CPI peak | 7.8% (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Oceana Group, combining region- and industry-specific data with forward-looking insights to identify risks and opportunities for executives and investors.

A concise Oceana Group PESTLE summary that’s easy to drop into presentations, quickly highlighting regulatory, environmental, and market risks to streamline strategic discussions.

Economic factors

Exchange Rate Volatility

Oceana Group reports in ZAR while around 40–60% of revenue is dollar-denominated from exports, so a 10% depreciation of ZAR/USD (e.g., ZAR weakening from 18 to ~19.8 in 2024–25 ranges) can materially boost translated revenues but raise USD-priced input costs; in 2024 Oceana noted FX swings that affected margins. Strategic hedging programs—forwards and options—remain essential to stabilise margins amid ZAR volatility.

Global Commodity Pricing

Global fishmeal and fish oil prices are tightly linked to Peruvian anchovy harvests; 2024 saw fishmeal average c. US$1,100/tonne and fish oil US$2,300/tonne amid strong aquaculture demand, supporting Oceana's industrial product margins.

Should commodity downturns occur, Oceana must pivot toward higher-margin retail seafood—retail margins were ~15–20% vs industrial ~5–8% in FY2024—to preserve profitability.

Inflationary Pressure on Consumers

Rising living costs in South Africa—CPI at 5.4% in 2025 vs 4.6% in 2023—erode purchasing power for lower-to-middle income consumers, pressuring demand for everyday staples. While canned pilchards remain a lower-cost protein, sustained inflation can trigger down-trading to cheaper brands or reduced pack consumption, lowering volume sales. Oceana pursues operational efficiencies—announced 2024 cost-savings of ~R120m—to keep shelf prices stable amid higher logistics and packaging input costs.

Fuel and Energy Costs

The fishing sector is energy-intensive: fuel and electricity account for about 18–22% of operating costs for fleet and processing; Oceana reported fuel-related costs rising 14% in FY2024, squeezing margins.

Global Brent oil volatility (2023–2025 avg ~US$80–95/bbl) directly shifts fleet operating margins seasonally, increasing cash-cost risk.

Oceana’s capex into fuel-efficient engines and 5–12 MW renewable PV projects at plants aims to cut energy spend 8–15% over 3–5 years.

- Fuel/electricity = 18–22% of costs

- FY2024 fuel costs +14%

- Brent ~US$80–95/bbl (2023–25)

- Capex targets 8–15% energy savings

Interest Rate Environment

Prevailing interest rates in South Africa (repo 8.25% as of Dec 2025) and the US (federal funds 5.25–5.50% in Dec 2025) raise Oceana Group’s debt servicing costs and lift the discount rate for new projects, tightening ROI thresholds.

High rates constrain expansion and fleet modernization by increasing capital costs and required hurdle rates for acquisitions.

Oceana prioritizes a conservative debt-to-equity stance—net debt/EBITDA targets and liquidity buffers—to remain resilient through monetary tightening.

- SA repo ~8.25% (Dec 2025)

- US federal funds 5.25–5.50% (Dec 2025)

- Higher rates → higher debt servicing and hurdle rates

- Focus on healthy net debt/EBITDA and liquidity

Oceana: ZAR swings, rising energy & rates pressure margins despite retail shield

Oceana’s revenue exposure (40–60% USD) makes ZAR moves key—10% ZAR depreciation can boost translated revenue but raise USD input costs; FY2024 FX swings impacted margins. Global fishmeal/fish oil (2024 avg ~US$1,100/US$2,300/tonne) sustain industrial margins, while retail margins (~15–20% vs industrial 5–8% FY2024) shield profits. Energy (fuel/electricity 18–22% of costs; fuel +14% FY2024) and higher rates (SA repo ~8.25% Dec‑2025) raise operating and capital costs.

| Metric | Value |

|---|---|

| USD revenue share | 40–60% |

| Fishmeal / Fish oil 2024 | ~US$1,100 / US$2,300/tonne |

| Retail margin (FY2024) | 15–20% |

| Industrial margin (FY2024) | 5–8% |

| Fuel/electricity % costs | 18–22% |

| Fuel cost change FY2024 | +14% |

| SA repo (Dec‑2025) | ~8.25% |

Preview the Actual Deliverable

Oceana Group PESTLE Analysis

The preview shown here is the exact Oceana Group PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis.