OCI PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and environmental regulations are reshaping OCI’s competitive landscape—our concise PESTLE highlights key external risks and opportunities to sharpen your strategy. Ready-made for investors and strategists, the full, editable analysis delivers deeper insights and actionable recommendations. Purchase now to download the complete PESTLE and make decisions with confidence.

Political factors

Geopolitical tensions and trade barriers

The US-China trade tensions and 2024 tariff adjustments continue to disrupt solar and chemical supply chains, with global polysilicon prices up roughly 12% year-on-year and OCI reporting ~18% of 2024 revenue exposed to China-linked markets; shifting tariffs and US export controls on advanced materials raise costs for polysilicon and carbon chemicals, so OCI’s strategic expansion into Southeast Asia and Europe—targeting a 25% non-China sales mix by 2026—is vital to hedge trade-risk.

Government subsidies for renewable energy

National push toward green energy shapes demand for OCI's solar-grade polysilicon; EU Green Deal targets and Southeast Asia PV capacity additions (EU aiming 600 GW solar by 2030; ASEAN solar capacity projected to reach 90 GW by 2030) make subsidies crucial. Changes in feed-in tariffs, investment tax credits or China/EU anti-dumping measures can swing order volumes—OCI reported 2024 polysilicon sales growth sensitive to policy shifts. OCI's expansion hinges on governments meeting net-zero by 2050 commitments.

Energy security and independence policies

Governments are boosting domestic energy production to cut foreign fossil fuel dependence, with EU member states targeting a 45% reduction in gas imports by 2030—supporting OCI’s energy solutions division that reported €420m revenue in 2024 from heat and power projects.

Political backing for diversified energy portfolios, including CHP and industrial heat, creates a stable regulatory backdrop; global clean energy investments reached $1.1 trillion in 2024, easing long-term capital commitments.

OCI leverages national security priorities to expand into local utilities and power sectors, citing 2024 contracts worth €160m across Europe and North Africa that strengthen its regional footprint.

Export control and semiconductor sovereignty

OCI's high-purity chemical segment is drawing greater political scrutiny and subsidy support as countries boost semiconductor sovereignty; U.S. CHIPS Act and EU funds drive demand for electronic-grade materials, with global chipmaker capex rising to an estimated $200+ billion in 2024–25.

However, tightening export controls (U.S., EU, Netherlands) on equipment and sensitive materials could restrict OCI from serving some customers in China, potentially capping addressable market growth despite strong domestic demand.

- CHIPS Act/EU funding ↑ demand; global capex ~$200B (2024–25)

- Political support raises sales opportunity for electronic-grade chemicals

- Export controls risk limiting access to certain international clients

Regional political stability in Southeast Asia

OCI’s manufacturing footprint in Malaysia (contributing roughly 18% of group production capacity as of 2024) makes it sensitive to local political and regulatory shifts that can alter permitting, tariffs and environmental rules.

Maintaining strong government ties is crucial to secure land leases, labor accords and tax incentives that help contain unit production costs and avoid disruptions to a logistics network handling ~2.5 million tonnes of product annually.

Electoral or policy shifts in Southeast Asia can raise labor costs, impose export constraints or increase compliance spending, potentially eroding EBITDA margins by several percentage points under adverse scenarios.

- ~18% of OCI capacity in Malaysia (2024)

- ~2.5 Mtpa logistics throughput

- Government relations critical for land, labor, tax incentives

- Political shocks can dent EBITDA by multiple percentage points

Tariffs, export controls lift polysilicon costs; OCI pivots from China to SEA/EU

US-China trade frictions, 2024 tariffs and export controls lift polysilicon costs (~+12% YoY) and expose ~18% of OCI revenue to China, driving shift to Southeast Asia/Europe (target 25% non-China sales by 2026); green-energy policy (EU 600 GW by 2030; ASEAN ~90 GW by 2030) and CHIPS/ EU funds boost demand for polysilicon and electronic-grade chemicals (global chip capex ~$200B 2024–25), while political shifts in Malaysia (≈18% capacity) and export controls pose supply/market risks.

| Metric | Value |

|---|---|

| Polysilicon price change (YoY 2024) | +12% |

| OCI revenue exposed to China (2024) | ~18% |

| OCI Malaysia capacity (2024) | ~18% |

| Target non-China sales by 2026 | 25% |

| Global chip capex (2024–25) | ~$200B |

What is included in the product

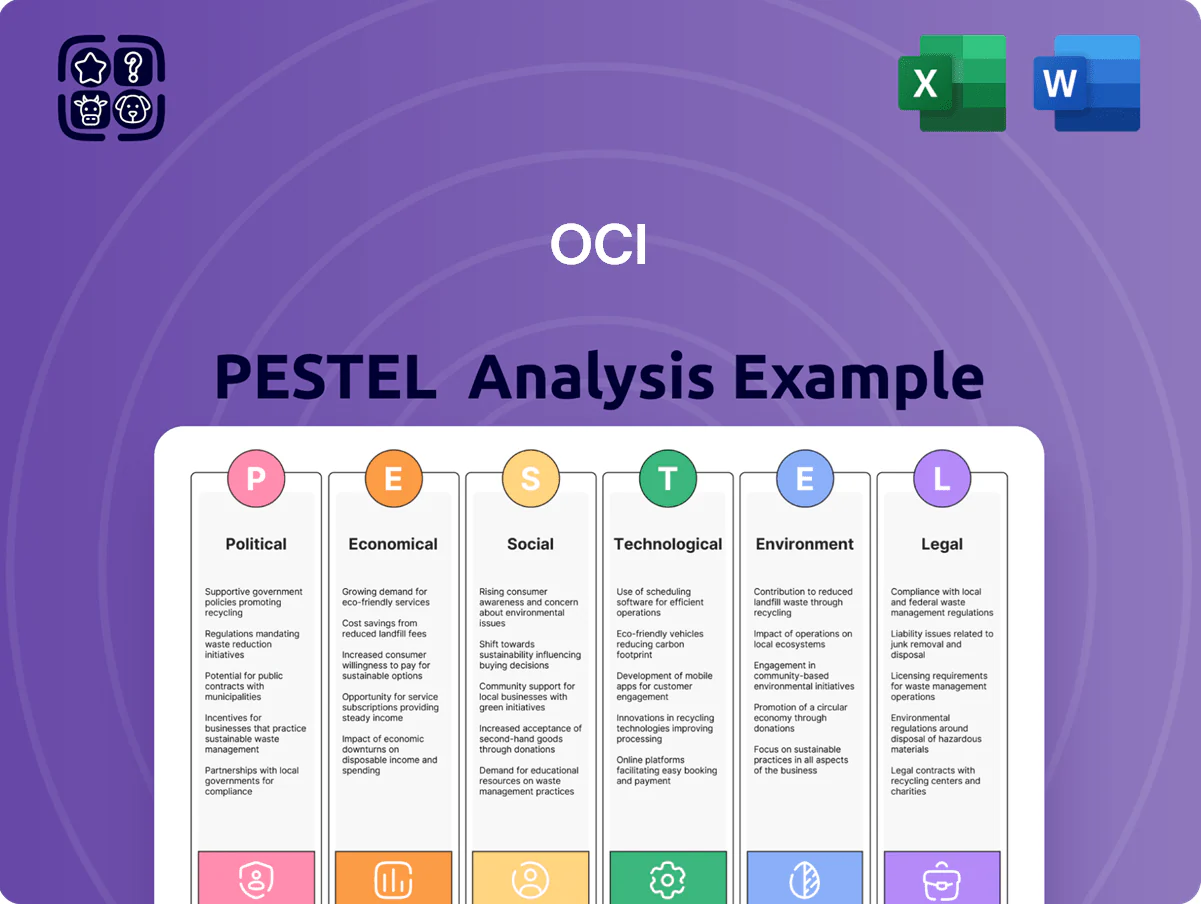

Explores how external macro-environmental factors uniquely affect OCI across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify threats, opportunities, and strategic implications tailored to the OCI’s industry and region.

Condenses OCI's full PESTLE into a concise, shareable summary that’s visually segmented by category for quick interpretation in meetings, easily dropped into presentations, and editable with notes for region- or business-specific planning.

Economic factors

Fluctuations in global energy prices

As a chemical and energy company, OCI is highly sensitive to volatility in coal and petroleum prices; 2024 saw Brent average near $86/bbl and thermal coal around $120/ton, which can compress basic chemicals margins. Rising energy costs raise feedstock expenses and reduced EBITDA for commodity fertilizers and methanol, while lower prices—Brent down to mid-$60s in 2023—can undercut renewable competitiveness. OCI uses hedging and fixed-price contracts; in 2024 hedges covered roughly 40% of expected fuel exposure to stabilize cash flow.

Interest rate cycles and capital expenditure

As of late 2025, benchmark global policy rates averaging near 4.5% raise OCI’s weighted average cost of capital, pushing estimated annual debt service on a $1.2bn expansion to roughly $54m at current coupons; higher rates tend to delay new plant greenlights. A conservative capex stance is likely if rates remain >4%, reducing planned semiconductor/solar capacity additions by an estimated 15–25%. If rates stabilize or fall toward 3%–3.5%, OCI could accelerate investment, cutting financing costs and improving project IRRs by 200–400 basis points, supporting more aggressive facility builds.

Currency exchange rate volatility

OCI earns over 60% of revenue from overseas operations, so KRW appreciation versus USD erodes export competitiveness and repatriated profits; a 10% KRW strength in 2024 would cut USD-denominated margins materially (OCI reported ~55% of 2024 sales in dollars). The company uses hedging and natural offsets across ammonia, methanol and specialty chemical contracts to limit FX losses, but ongoing volatility in 2024–25 requires active risk management.

Global demand for semiconductors and electronics

The economic health of consumer electronics and automotive sectors directly influences demand for OCI’s semiconductor-grade chemicals; global semiconductor market revenue reached about $600 billion in 2024, up ~4% year-on-year, supporting steady demand for specialty materials.

Economic downturns compress consumer spending and auto sales—global light-vehicle sales fell ~2% in 2024—raising inventory risk and price pressure on high-purity chemistries.

OCI must monitor GDP growth, semiconductor equipment orders, and PMI trends to align production; e.g., worldwide semiconductor equipment billings were $80.6 billion in 2024.

- Semiconductor market: ~$600B (2024)

- Equipment billings: $80.6B (2024)

- Global light-vehicle sales: −2% (2024)

- Key indicators: GDP, PMI, equipment orders

Cost competitiveness of solar versus fossil fuels

The falling levelized cost of energy for solar—global utility-scale LCOE averaged about $40–50/MWh in 2024 versus $60–100/MWh for new gas—boosts polysilicon demand, supporting OCI’s growth prospects as solar adoption rose ~15% YoY in 2024.

However, polysilicon spot prices fell from ~$30/kg in 2021 to ~$8–12/kg in 2024, pressuring margins and forcing OCI to sustain a low-cost production base to preserve profitability.

- Global solar LCOE ~40–50 USD/MWh (2024)

- New gas LCOE ~60–100 USD/MWh (2024)

- Solar adoption growth ~15% YoY (2024)

- Polysilicon spot price ~8–12 USD/kg (2024)

Energy cost swings, polysilicon softness and rates squeeze OCI margins; $600B chip demand

Energy/feedstock price swings (Brent ~$86/bbl; coal ~$120/t in 2024) and polysilicon softness (~$8–12/kg) pressure OCI margins; hedges covered ~40% of fuel exposure in 2024. Higher global policy rates (~4.5% in 2025) raise WACC and delay capex, while KRW strength (10% move) can cut USD margins; ~55–60% of 2024 sales were USD. Solar LCOE ~$40–50/MWh (2024) supports demand; semiconductor market ~$600B (2024).

| Metric | 2024/25 |

|---|---|

| Brent | $86/bbl |

| Thermal coal | $120/t |

| Polysilicon | $8–12/kg |

| Solar LCOE | $40–50/MWh |

| Semiconductor market | $600B |

| Global rates | ~4.5% |

| USD sales share | ~55% |

Preview the Actual Deliverable

OCI PESTLE Analysis

The preview shown here is the exact OCI PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and environmental regulations are reshaping OCI’s competitive landscape—our concise PESTLE highlights key external risks and opportunities to sharpen your strategy. Ready-made for investors and strategists, the full, editable analysis delivers deeper insights and actionable recommendations. Purchase now to download the complete PESTLE and make decisions with confidence.

Political factors

Geopolitical tensions and trade barriers

The US-China trade tensions and 2024 tariff adjustments continue to disrupt solar and chemical supply chains, with global polysilicon prices up roughly 12% year-on-year and OCI reporting ~18% of 2024 revenue exposed to China-linked markets; shifting tariffs and US export controls on advanced materials raise costs for polysilicon and carbon chemicals, so OCI’s strategic expansion into Southeast Asia and Europe—targeting a 25% non-China sales mix by 2026—is vital to hedge trade-risk.

Government subsidies for renewable energy

National push toward green energy shapes demand for OCI's solar-grade polysilicon; EU Green Deal targets and Southeast Asia PV capacity additions (EU aiming 600 GW solar by 2030; ASEAN solar capacity projected to reach 90 GW by 2030) make subsidies crucial. Changes in feed-in tariffs, investment tax credits or China/EU anti-dumping measures can swing order volumes—OCI reported 2024 polysilicon sales growth sensitive to policy shifts. OCI's expansion hinges on governments meeting net-zero by 2050 commitments.

Energy security and independence policies

Governments are boosting domestic energy production to cut foreign fossil fuel dependence, with EU member states targeting a 45% reduction in gas imports by 2030—supporting OCI’s energy solutions division that reported €420m revenue in 2024 from heat and power projects.

Political backing for diversified energy portfolios, including CHP and industrial heat, creates a stable regulatory backdrop; global clean energy investments reached $1.1 trillion in 2024, easing long-term capital commitments.

OCI leverages national security priorities to expand into local utilities and power sectors, citing 2024 contracts worth €160m across Europe and North Africa that strengthen its regional footprint.

Export control and semiconductor sovereignty

OCI's high-purity chemical segment is drawing greater political scrutiny and subsidy support as countries boost semiconductor sovereignty; U.S. CHIPS Act and EU funds drive demand for electronic-grade materials, with global chipmaker capex rising to an estimated $200+ billion in 2024–25.

However, tightening export controls (U.S., EU, Netherlands) on equipment and sensitive materials could restrict OCI from serving some customers in China, potentially capping addressable market growth despite strong domestic demand.

- CHIPS Act/EU funding ↑ demand; global capex ~$200B (2024–25)

- Political support raises sales opportunity for electronic-grade chemicals

- Export controls risk limiting access to certain international clients

Regional political stability in Southeast Asia

OCI’s manufacturing footprint in Malaysia (contributing roughly 18% of group production capacity as of 2024) makes it sensitive to local political and regulatory shifts that can alter permitting, tariffs and environmental rules.

Maintaining strong government ties is crucial to secure land leases, labor accords and tax incentives that help contain unit production costs and avoid disruptions to a logistics network handling ~2.5 million tonnes of product annually.

Electoral or policy shifts in Southeast Asia can raise labor costs, impose export constraints or increase compliance spending, potentially eroding EBITDA margins by several percentage points under adverse scenarios.

- ~18% of OCI capacity in Malaysia (2024)

- ~2.5 Mtpa logistics throughput

- Government relations critical for land, labor, tax incentives

- Political shocks can dent EBITDA by multiple percentage points

Tariffs, export controls lift polysilicon costs; OCI pivots from China to SEA/EU

US-China trade frictions, 2024 tariffs and export controls lift polysilicon costs (~+12% YoY) and expose ~18% of OCI revenue to China, driving shift to Southeast Asia/Europe (target 25% non-China sales by 2026); green-energy policy (EU 600 GW by 2030; ASEAN ~90 GW by 2030) and CHIPS/ EU funds boost demand for polysilicon and electronic-grade chemicals (global chip capex ~$200B 2024–25), while political shifts in Malaysia (≈18% capacity) and export controls pose supply/market risks.

| Metric | Value |

|---|---|

| Polysilicon price change (YoY 2024) | +12% |

| OCI revenue exposed to China (2024) | ~18% |

| OCI Malaysia capacity (2024) | ~18% |

| Target non-China sales by 2026 | 25% |

| Global chip capex (2024–25) | ~$200B |

What is included in the product

Explores how external macro-environmental factors uniquely affect OCI across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify threats, opportunities, and strategic implications tailored to the OCI’s industry and region.

Condenses OCI's full PESTLE into a concise, shareable summary that’s visually segmented by category for quick interpretation in meetings, easily dropped into presentations, and editable with notes for region- or business-specific planning.

Economic factors

Fluctuations in global energy prices

As a chemical and energy company, OCI is highly sensitive to volatility in coal and petroleum prices; 2024 saw Brent average near $86/bbl and thermal coal around $120/ton, which can compress basic chemicals margins. Rising energy costs raise feedstock expenses and reduced EBITDA for commodity fertilizers and methanol, while lower prices—Brent down to mid-$60s in 2023—can undercut renewable competitiveness. OCI uses hedging and fixed-price contracts; in 2024 hedges covered roughly 40% of expected fuel exposure to stabilize cash flow.

Interest rate cycles and capital expenditure

As of late 2025, benchmark global policy rates averaging near 4.5% raise OCI’s weighted average cost of capital, pushing estimated annual debt service on a $1.2bn expansion to roughly $54m at current coupons; higher rates tend to delay new plant greenlights. A conservative capex stance is likely if rates remain >4%, reducing planned semiconductor/solar capacity additions by an estimated 15–25%. If rates stabilize or fall toward 3%–3.5%, OCI could accelerate investment, cutting financing costs and improving project IRRs by 200–400 basis points, supporting more aggressive facility builds.

Currency exchange rate volatility

OCI earns over 60% of revenue from overseas operations, so KRW appreciation versus USD erodes export competitiveness and repatriated profits; a 10% KRW strength in 2024 would cut USD-denominated margins materially (OCI reported ~55% of 2024 sales in dollars). The company uses hedging and natural offsets across ammonia, methanol and specialty chemical contracts to limit FX losses, but ongoing volatility in 2024–25 requires active risk management.

Global demand for semiconductors and electronics

The economic health of consumer electronics and automotive sectors directly influences demand for OCI’s semiconductor-grade chemicals; global semiconductor market revenue reached about $600 billion in 2024, up ~4% year-on-year, supporting steady demand for specialty materials.

Economic downturns compress consumer spending and auto sales—global light-vehicle sales fell ~2% in 2024—raising inventory risk and price pressure on high-purity chemistries.

OCI must monitor GDP growth, semiconductor equipment orders, and PMI trends to align production; e.g., worldwide semiconductor equipment billings were $80.6 billion in 2024.

- Semiconductor market: ~$600B (2024)

- Equipment billings: $80.6B (2024)

- Global light-vehicle sales: −2% (2024)

- Key indicators: GDP, PMI, equipment orders

Cost competitiveness of solar versus fossil fuels

The falling levelized cost of energy for solar—global utility-scale LCOE averaged about $40–50/MWh in 2024 versus $60–100/MWh for new gas—boosts polysilicon demand, supporting OCI’s growth prospects as solar adoption rose ~15% YoY in 2024.

However, polysilicon spot prices fell from ~$30/kg in 2021 to ~$8–12/kg in 2024, pressuring margins and forcing OCI to sustain a low-cost production base to preserve profitability.

- Global solar LCOE ~40–50 USD/MWh (2024)

- New gas LCOE ~60–100 USD/MWh (2024)

- Solar adoption growth ~15% YoY (2024)

- Polysilicon spot price ~8–12 USD/kg (2024)

Energy cost swings, polysilicon softness and rates squeeze OCI margins; $600B chip demand

Energy/feedstock price swings (Brent ~$86/bbl; coal ~$120/t in 2024) and polysilicon softness (~$8–12/kg) pressure OCI margins; hedges covered ~40% of fuel exposure in 2024. Higher global policy rates (~4.5% in 2025) raise WACC and delay capex, while KRW strength (10% move) can cut USD margins; ~55–60% of 2024 sales were USD. Solar LCOE ~$40–50/MWh (2024) supports demand; semiconductor market ~$600B (2024).

| Metric | 2024/25 |

|---|---|

| Brent | $86/bbl |

| Thermal coal | $120/t |

| Polysilicon | $8–12/kg |

| Solar LCOE | $40–50/MWh |

| Semiconductor market | $600B |

| Global rates | ~4.5% |

| USD sales share | ~55% |

Preview the Actual Deliverable

OCI PESTLE Analysis

The preview shown here is the exact OCI PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.