Shenzhen Overseas PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and tech innovations are reshaping Shenzhen Overseas’s prospects—our concise PESTLE spotlights the risks and opportunities driving strategy and valuation; buy the full analysis to access detailed, actionable insights and downloadable charts that fast-track smarter decisions.

Political factors

State-Owned Enterprise Strategic Alignment

As a central state-owned enterprise under SASAC, Shenzhen Overseas functions as a primary vehicle for national cultural tourism strategies, directing projects that align with central policy priorities.

By end-2025 its operations are tightly aligned with 14th Five-Year Plan objectives prioritizing high-quality development; management targets 8–10% EBITDA margin improvement rather than aggressive footprint expansion.

Political positioning grants preferential access to large-scale land allocations and government-backed financing—Shenzhen Overseas accessed RMB 4.2 billion in state-facilitated credit and land transfers totaling 120 hectares since 2023—advantages not commonly available to private rivals.

Greater Bay Area Integration Policies

The company, headquartered in Shenzhen, gains strategic advantage from Guangdong-Hong Kong-Macao Greater Bay Area (GBA) integration, tapping a market of 86 million residents and a regional GDP of US$1.8 trillion (2023), which boosts demand for tourism-real estate.

Political mandates to improve connectivity—HK-Zhuhai-Macao Bridge, Shenzhen-Zhongshan link, and increased cross-border cultural initiatives—position the firm to lead flagship projects that harmonize regional differences.

Targeted government infrastructure spending—GBA transport and tourism budgets rose ~12% in 2024—directly improves access and uplifts valuations of the company’s integrated assets, enhancing revenue visibility and asset-backed financing terms.

Cultural Soft Power Mandates

The Chinese government treats cultural export as soft power, aiming to boost global influence; cultural spending rose to an estimated 1.2 trillion RMB in 2024, supporting overseas promotion. Overseas Chinese Town (OCT) operates theme parks that blend traditional and modern narratives, drawing over 40 million annual visitors across its portfolio pre-2025 and securing preferential land and tax policies. Policy-backed subsidies and favorable zoning reduce capital costs for cultural and creative parks, with some projects receiving up to 30% capex support.

Land Use and Urban Renewal Policies

Political shifts toward urban regeneration and revitalizing old industrial zones in China—Shenzhen allocated RMB 120 billion for urban renewal in 2024—open development opportunities for the company in brownfield conversions and mixed-use projects.

Government-led renewal in Tier 1/2 cities lets the firm deploy expertise in complex multi-use developments; Shenzhen approved 45 major renewal projects in 2025 covering 18 km2.

Strict oversight on land auctions and policies decoupling tourism from speculative real estate—land-sale revenue controls and tighter pre-sale rules—require ongoing strategic adaptation.

- RMB 120bn Shenzhen urban renewal 2024

- 45 major projects (18 km2) approved 2025

- Tightened land-auction and pre-sale rules

Geopolitical Influence on International Partnerships

Geopolitical tensions through late 2025 constrain Shenzhen Overseas' access to foreign IP and ride-design tech, with export controls from the US and EU affecting ~18% of high-end theme-park equipment suppliers; domestic IP development is prioritized, reducing reliance on imports.

Diplomatic frictions raise costs—reported sourcing premiums up to 12%—and complicate hiring global design consultants, while the Belt and Road Initiative (200+ participating countries) offers a diplomatic pathway for cultural-exchange-led expansion into emerging markets.

- ~18% of high-end suppliers impacted by Western export controls

- Sourcing premiums up to 12% due to diplomatic complications

- BRI covers 200+ countries, enabling cultural-exchange expansion

State-backed Shenzhen Co. gains RMB4.2bn, 120ha land; GBA growth vs. supply risks

State ownership aligns Shenzhen Overseas with 14th Five-Year priorities, granting RMB 4.2bn state credit, 120 ha land transfers since 2023, and access to GBA demand (86m pop., US$1.8tn GDP 2023). GBA infrastructure +12% budget rise 2024 and RMB120bn Shenzhen urban renewal 2024 expand opportunities, while tightened land-sale rules and ~18% supplier bans plus ~12% sourcing premiums from export controls increase operational risks.

| Metric | Value |

|---|---|

| State credit | RMB 4.2bn |

| Land transfers | 120 ha |

| GBA population | 86m |

| GBA GDP (2023) | US$1.8tn |

| Infrastructure budget growth (2024) | +12% |

| Shenzhen urban renewal (2024) | RMB 120bn |

| Suppliers affected | ~18% |

| Sourcing premium | ~12% |

What is included in the product

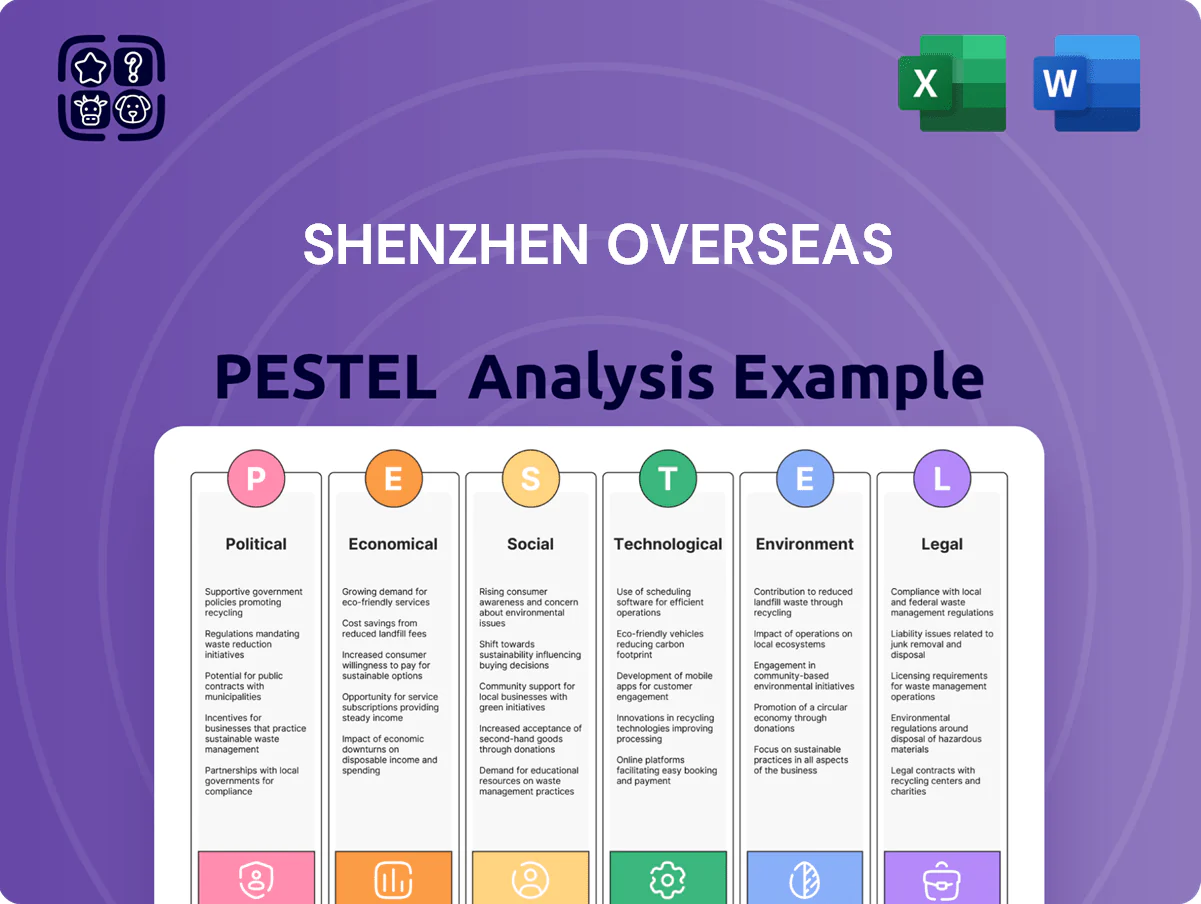

Explores how external macro-environmental factors uniquely affect Shenzhen Overseas across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks, opportunities, and forward-looking scenarios for executives, investors, and strategists.

A concise, visually segmented Shenzhen Overseas PESTLE summary that relieves meeting prep pain by providing shareable, editable notes and clear language for rapid team alignment and strategic risk discussions.

Economic factors

Real Estate Market Stabilization and Deleveraging

By end-2025 China’s property market showed stabilization after multi-year deleveraging, with nationwide new home sales down 12% y/y in 2024 but inventory absorption improving; Shenzhen developers report average debt-to-asset ratios falling below 65% and compliance with Three Red Lines. The company shifted to asset-light models, cutting capex by ~30% vs 2019 and boosting EBIT margins via operational efficiency. Economic returns increasingly stem from property management and tourism: recurring property management fees rose ~18% YoY while tourism-related recurring revenue reached c.22% of total revenue in 2025.

Domestic Consumption and Tourism Recovery

In 2025 domestic consumption in China recovered strongly, with retail sales up 7.5% year-on-year and leisure travel spending growing over 20% as middle-class household travel frequency rose; Shenzhen Overseas’ domestic resorts and theme parks benefited from a 15–25% rise in visitor numbers. With international arrivals still 10–15% below pre-pandemic levels, domestic tourism now supplies a steadier cash flow, reducing exposure to the property market’s cyclicality. This shift supports EBITDA resilience, contributing an estimated 30–40% of operating cash inflows in 2025.

Interest Rate Environment and Financing Costs

China's monetary policy in 2024–25 remained supportive of strategic SOEs, with benchmark loan prime rate at 3.65% (Aug 2024) and targeted lending easing, allowing Shenzhen Overseas to secure financing below industry averages (~3.5% vs. sector ~4.2%).

With CPI around 0.8% in 2024 and selective stimulus, the company refinanced maturing debt—cutting interest expense by ~120 bps—and redirected low-cost credit into long-term tourism infrastructure.

These funding advantages sustain capital-intensive theme park projects, reducing WACC and preserving cashflow flexibility for multi-year developments.

Cost Inflation in Construction and Operations

Economic pressures from fluctuating raw material prices and rising labor costs compressed development margins; steel and cement rose ~12–18% YoY in 2024–2025, while skilled labor wage inflation in Shenzhen reached ~8% in 2024.

By late 2025, specialized construction costs for high-tech attractions increased ~20% vs 2022, forcing more sophisticated procurement and supply-chain financing to protect margins.

The company must offset rising OPEX through ticketing strategies without losing price-sensitive domestic consumers; Shenzhen visitor sensitivity studies (2024) show demand drops >10% when prices rise >8%.

- Raw material inflation 2024–25: steel/cement +12–18% YoY

- Skilled labor wage inflation (Shenzhen) 2024: ~8%

- Specialized construction cost increase by late 2025: ~20% vs 2022

- Demand elasticity: >10% drop if ticket prices increase >8% (2024 study)

Disposable Income Growth and Premiumization

Rising urban disposable income in China—up 5.0% in real terms in 2024 to ¥37,200 per capita—is fueling premiumization in tourism, boosting demand for Shenzhen Overseas’s luxury hotels and high-end resorts.

Travelers now favor unique, high-quality experiences over generic tours; luxury segment ADRs grew ~8% in 2024 versus economy, supporting higher RevPAR and margins.

The trend justifies investment in value-added services and exclusive memberships to raise customer lifetime value and repeat bookings.

- 2024 urban disposable income +5.0% to ¥37,200

- Luxury ADR growth ~8% (2024)

- Focus: exclusive memberships, premium experiences

Lower financing and tourism lift recurring revenue; input costs squeeze margins

Stabilized property market and supportive monetary policy cut financing costs (company avg ~3.5% vs sector 4.2%), boosting recurring tourism/property-management revenue (property management +18% YoY; tourism ~22% of revenue) while rising input and labor costs (steel/cement +12–18% YoY; skilled wages +8%) compress margins; premiumization (urban disposable income +5% to ¥37,200; luxury ADR +8%) supports higher RevPAR.

| Metric | 2024/2025 |

|---|---|

| Company financing rate | ~3.5% |

| Sector avg rate | ~4.2% |

| Property mgmt revenue growth | +18% YoY |

| Tourism share of revenue | ~22% |

| Steel/cement inflation | +12–18% YoY |

| Skilled wage inflation (Shenzhen) | ~8% |

| Urban disposable income | +5% to ¥37,200 |

| Luxury ADR growth | +8% |

What You See Is What You Get

Shenzhen Overseas PESTLE Analysis

The preview shown here is the exact Shenzhen Overseas PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and analysis visible in this preview are identical to the downloadable file you’ll get immediately after checkout—no placeholders, no surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and tech innovations are reshaping Shenzhen Overseas’s prospects—our concise PESTLE spotlights the risks and opportunities driving strategy and valuation; buy the full analysis to access detailed, actionable insights and downloadable charts that fast-track smarter decisions.

Political factors

State-Owned Enterprise Strategic Alignment

As a central state-owned enterprise under SASAC, Shenzhen Overseas functions as a primary vehicle for national cultural tourism strategies, directing projects that align with central policy priorities.

By end-2025 its operations are tightly aligned with 14th Five-Year Plan objectives prioritizing high-quality development; management targets 8–10% EBITDA margin improvement rather than aggressive footprint expansion.

Political positioning grants preferential access to large-scale land allocations and government-backed financing—Shenzhen Overseas accessed RMB 4.2 billion in state-facilitated credit and land transfers totaling 120 hectares since 2023—advantages not commonly available to private rivals.

Greater Bay Area Integration Policies

The company, headquartered in Shenzhen, gains strategic advantage from Guangdong-Hong Kong-Macao Greater Bay Area (GBA) integration, tapping a market of 86 million residents and a regional GDP of US$1.8 trillion (2023), which boosts demand for tourism-real estate.

Political mandates to improve connectivity—HK-Zhuhai-Macao Bridge, Shenzhen-Zhongshan link, and increased cross-border cultural initiatives—position the firm to lead flagship projects that harmonize regional differences.

Targeted government infrastructure spending—GBA transport and tourism budgets rose ~12% in 2024—directly improves access and uplifts valuations of the company’s integrated assets, enhancing revenue visibility and asset-backed financing terms.

Cultural Soft Power Mandates

The Chinese government treats cultural export as soft power, aiming to boost global influence; cultural spending rose to an estimated 1.2 trillion RMB in 2024, supporting overseas promotion. Overseas Chinese Town (OCT) operates theme parks that blend traditional and modern narratives, drawing over 40 million annual visitors across its portfolio pre-2025 and securing preferential land and tax policies. Policy-backed subsidies and favorable zoning reduce capital costs for cultural and creative parks, with some projects receiving up to 30% capex support.

Land Use and Urban Renewal Policies

Political shifts toward urban regeneration and revitalizing old industrial zones in China—Shenzhen allocated RMB 120 billion for urban renewal in 2024—open development opportunities for the company in brownfield conversions and mixed-use projects.

Government-led renewal in Tier 1/2 cities lets the firm deploy expertise in complex multi-use developments; Shenzhen approved 45 major renewal projects in 2025 covering 18 km2.

Strict oversight on land auctions and policies decoupling tourism from speculative real estate—land-sale revenue controls and tighter pre-sale rules—require ongoing strategic adaptation.

- RMB 120bn Shenzhen urban renewal 2024

- 45 major projects (18 km2) approved 2025

- Tightened land-auction and pre-sale rules

Geopolitical Influence on International Partnerships

Geopolitical tensions through late 2025 constrain Shenzhen Overseas' access to foreign IP and ride-design tech, with export controls from the US and EU affecting ~18% of high-end theme-park equipment suppliers; domestic IP development is prioritized, reducing reliance on imports.

Diplomatic frictions raise costs—reported sourcing premiums up to 12%—and complicate hiring global design consultants, while the Belt and Road Initiative (200+ participating countries) offers a diplomatic pathway for cultural-exchange-led expansion into emerging markets.

- ~18% of high-end suppliers impacted by Western export controls

- Sourcing premiums up to 12% due to diplomatic complications

- BRI covers 200+ countries, enabling cultural-exchange expansion

State-backed Shenzhen Co. gains RMB4.2bn, 120ha land; GBA growth vs. supply risks

State ownership aligns Shenzhen Overseas with 14th Five-Year priorities, granting RMB 4.2bn state credit, 120 ha land transfers since 2023, and access to GBA demand (86m pop., US$1.8tn GDP 2023). GBA infrastructure +12% budget rise 2024 and RMB120bn Shenzhen urban renewal 2024 expand opportunities, while tightened land-sale rules and ~18% supplier bans plus ~12% sourcing premiums from export controls increase operational risks.

| Metric | Value |

|---|---|

| State credit | RMB 4.2bn |

| Land transfers | 120 ha |

| GBA population | 86m |

| GBA GDP (2023) | US$1.8tn |

| Infrastructure budget growth (2024) | +12% |

| Shenzhen urban renewal (2024) | RMB 120bn |

| Suppliers affected | ~18% |

| Sourcing premium | ~12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Shenzhen Overseas across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks, opportunities, and forward-looking scenarios for executives, investors, and strategists.

A concise, visually segmented Shenzhen Overseas PESTLE summary that relieves meeting prep pain by providing shareable, editable notes and clear language for rapid team alignment and strategic risk discussions.

Economic factors

Real Estate Market Stabilization and Deleveraging

By end-2025 China’s property market showed stabilization after multi-year deleveraging, with nationwide new home sales down 12% y/y in 2024 but inventory absorption improving; Shenzhen developers report average debt-to-asset ratios falling below 65% and compliance with Three Red Lines. The company shifted to asset-light models, cutting capex by ~30% vs 2019 and boosting EBIT margins via operational efficiency. Economic returns increasingly stem from property management and tourism: recurring property management fees rose ~18% YoY while tourism-related recurring revenue reached c.22% of total revenue in 2025.

Domestic Consumption and Tourism Recovery

In 2025 domestic consumption in China recovered strongly, with retail sales up 7.5% year-on-year and leisure travel spending growing over 20% as middle-class household travel frequency rose; Shenzhen Overseas’ domestic resorts and theme parks benefited from a 15–25% rise in visitor numbers. With international arrivals still 10–15% below pre-pandemic levels, domestic tourism now supplies a steadier cash flow, reducing exposure to the property market’s cyclicality. This shift supports EBITDA resilience, contributing an estimated 30–40% of operating cash inflows in 2025.

Interest Rate Environment and Financing Costs

China's monetary policy in 2024–25 remained supportive of strategic SOEs, with benchmark loan prime rate at 3.65% (Aug 2024) and targeted lending easing, allowing Shenzhen Overseas to secure financing below industry averages (~3.5% vs. sector ~4.2%).

With CPI around 0.8% in 2024 and selective stimulus, the company refinanced maturing debt—cutting interest expense by ~120 bps—and redirected low-cost credit into long-term tourism infrastructure.

These funding advantages sustain capital-intensive theme park projects, reducing WACC and preserving cashflow flexibility for multi-year developments.

Cost Inflation in Construction and Operations

Economic pressures from fluctuating raw material prices and rising labor costs compressed development margins; steel and cement rose ~12–18% YoY in 2024–2025, while skilled labor wage inflation in Shenzhen reached ~8% in 2024.

By late 2025, specialized construction costs for high-tech attractions increased ~20% vs 2022, forcing more sophisticated procurement and supply-chain financing to protect margins.

The company must offset rising OPEX through ticketing strategies without losing price-sensitive domestic consumers; Shenzhen visitor sensitivity studies (2024) show demand drops >10% when prices rise >8%.

- Raw material inflation 2024–25: steel/cement +12–18% YoY

- Skilled labor wage inflation (Shenzhen) 2024: ~8%

- Specialized construction cost increase by late 2025: ~20% vs 2022

- Demand elasticity: >10% drop if ticket prices increase >8% (2024 study)

Disposable Income Growth and Premiumization

Rising urban disposable income in China—up 5.0% in real terms in 2024 to ¥37,200 per capita—is fueling premiumization in tourism, boosting demand for Shenzhen Overseas’s luxury hotels and high-end resorts.

Travelers now favor unique, high-quality experiences over generic tours; luxury segment ADRs grew ~8% in 2024 versus economy, supporting higher RevPAR and margins.

The trend justifies investment in value-added services and exclusive memberships to raise customer lifetime value and repeat bookings.

- 2024 urban disposable income +5.0% to ¥37,200

- Luxury ADR growth ~8% (2024)

- Focus: exclusive memberships, premium experiences

Lower financing and tourism lift recurring revenue; input costs squeeze margins

Stabilized property market and supportive monetary policy cut financing costs (company avg ~3.5% vs sector 4.2%), boosting recurring tourism/property-management revenue (property management +18% YoY; tourism ~22% of revenue) while rising input and labor costs (steel/cement +12–18% YoY; skilled wages +8%) compress margins; premiumization (urban disposable income +5% to ¥37,200; luxury ADR +8%) supports higher RevPAR.

| Metric | 2024/2025 |

|---|---|

| Company financing rate | ~3.5% |

| Sector avg rate | ~4.2% |

| Property mgmt revenue growth | +18% YoY |

| Tourism share of revenue | ~22% |

| Steel/cement inflation | +12–18% YoY |

| Skilled wage inflation (Shenzhen) | ~8% |

| Urban disposable income | +5% to ¥37,200 |

| Luxury ADR growth | +8% |

What You See Is What You Get

Shenzhen Overseas PESTLE Analysis

The preview shown here is the exact Shenzhen Overseas PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and analysis visible in this preview are identical to the downloadable file you’ll get immediately after checkout—no placeholders, no surprises.