Odfjell PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Get a competitive advantage with our targeted PESTLE Analysis of Odfjell—uncover how political shifts, economic cycles, environmental regulations, and tech trends shape its strategy and risk profile; buy the full report to access actionable insights, editable charts, and forecasts you can use in investment cases or strategic planning.

Political factors

Geopolitical instability in maritime corridors

Odfjell faces higher costs as Red Sea/Suez unrest forces rerouting: 2024 reports show average detour adds 7–14 days and fuel costs up to $40,000 per voyage, disrupting schedules and EBITDA margins; ongoing Middle East volatility requires 24/7 political monitoring to protect crew and chemical cargoes; prolonged instability lifted war-risk premiums by 30–60% in 2024, shrinking route efficiency and raising per-tonne transport costs.

Trade protectionism and tariff barriers

Shifting trade policies and tariffs between the US, China and EU reshape bulk liquids flows; US-China tariffs and EU carbon border adjustment talks contributed to a 6–8% decline in some intercontinental chemical shipments in 2023–2024, pressuring Odfjell’s long-haul utilisation. Odfjell must navigate complex FTAs and customs regimes that affect export/import volumes across jurisdictions and trading corridors. Rising protectionism drives regional chemical reshoring—reducing demand on long-haul chemical tanker routes and pressuring freight rates and fleet deployment.

Energy security and strategic autonomy

Governments in Europe and Asia are increasing energy-security measures and localizing chemical supply chains, driving new tank terminal investments; EU strategic autonomy plans target €300bn annual critical materials by 2025 and China’s 14th Five-Year Plan emphasizes domestic chemical capacity expansion.

Sanctions compliance and regulatory oversight

Odfjell must operate advanced sanctions compliance as international restrictions—expanded after 2022 conflicts—expose chemical tankers to denied-party lists; in 2024 Odfjell reported compliance-related costs rising, aligned with industry averages of 0.2–0.5% of revenue for large shipping firms, to avoid fines and reputational harm.

The evolving political landscape requires continuous screening and audit processes; non-compliance risks fines exceeding millions of dollars and loss of port access in key markets like EU, UK and US.

- Rising compliance spend: ~0.2–0.5% revenue benchmark

- Regulatory scope: dynamic denied-party lists post-2022

- Penalties: multi-million-dollar fines and market exclusion

International maritime diplomacy

Coordination between flag states and the IMO is critical for unified standards in chemical shipping; as of 2024 over 170 IMO member states participate in rule-making that affects Odfjell’s fleet of ~80 chemical tankers and 8.2 million dwt global fleet capacity across the sector.

Political cooperation or friction shapes the speed of harmonization: recent IMO amendments (2023–2024) on safety and GHG measures show faster uptake where diplomatic alignment exists, reducing compliance lag for carriers like Odfjell.

Stable diplomatic relations lower port denial risks and enable standardized protocols; Odfjell’s global port calls (thousands annually) and 2024 revenue of USD ~1.0 billion benefit from smoother clearances and consistent operational rules.

- IMO membership >170 states impacts rule uniformity

- Odfjell fleet ~80 tankers — benefits from harmonized standards

- 2024 sector revenue/context: Odfjell ~USD 1.0bn

Red Sea detours hike costs, war-risk premiums and squeeze chemical shipping margins

Geopolitical unrest (Red Sea/Suez) adds 7–14 days detours and up to $40,000 fuel per voyage, raising war-risk premiums 30–60% in 2024; trade tensions cut some intercontinental chemical flows 6–8% (2023–24), pressuring utilisation; compliance costs ~0.2–0.5% of revenue with multi-million fines risk; IMO >170 members affect harmonization, aiding Odfjell’s ~80-vessel fleet and 2024 revenue ~USD 1.0bn.

| Metric | 2023–24 |

|---|---|

| Detour delay | 7–14 days |

| Extra fuel/leg | up to $40,000 |

| War-risk premium | +30–60% |

| Trade flow decline | 6–8% |

| Compliance cost | 0.2–0.5% rev |

| Odfjell fleet | ~80 |

| 2024 revenue | ~USD 1.0bn |

What is included in the product

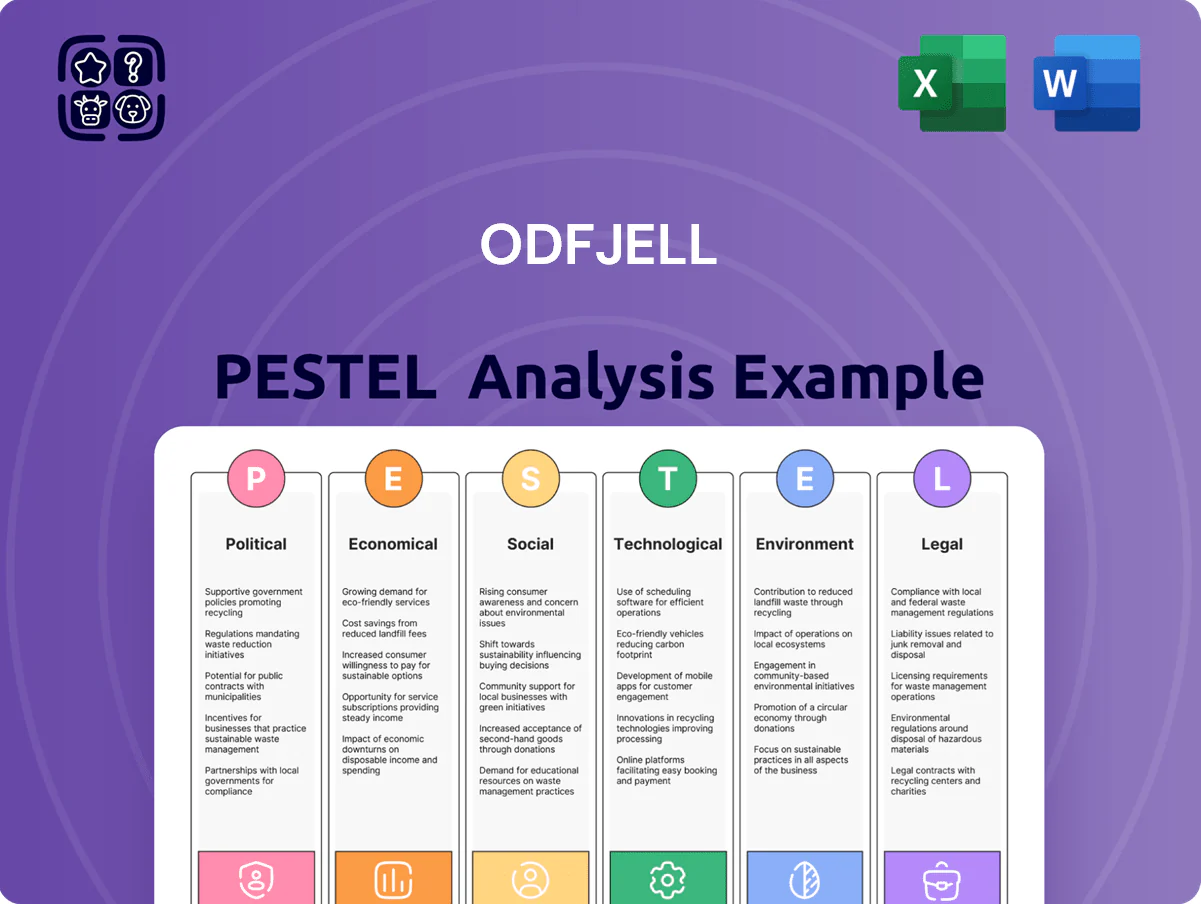

Explores how external macro-environmental factors uniquely affect Odfjell across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for Odfjell that eases meeting prep and decision-making by highlighting external risks and opportunities, ready to drop into presentations or share across teams.

Economic factors

Global chemical production cycles

The demand for Odfjell’s bulk chemical and tank terminal services tracks global chemical production, which rose 2.1% in 2024 after a 0.8% contraction in 2023, making tanker utilization sensitive to cyclical shifts in acids, edible oils and specialty liquids.

Economic slowdowns in EU, China or US—regions accounting for over 60% of chemical output—can cut production and pushed chemical tanker fleet utilization down to 78% in 2023 from 84% in 2021, reducing freight revenues.

Conversely, 2024 expansion increased seaborne chemical volumes by about 3–4%, supporting higher freight rates and boosting Odfjell’s operating margin, which improved toward pre-downturn levels as demand for sophisticated logistics rose.

Volatility in bunker fuel pricing

Fuel costs are among Odfjell's largest operating expenses, with bunker representing roughly 20-30% of voyage costs; global bunker 380CST prices swung from about 420 USD/ton in Jan 2024 to peaks near 650 USD/ton in late 2024, directly compressing margins. Odfjell uses fuel adjustment clauses, but sudden spikes still create short-term cash strain—EBITDA sensitivity can be several percentage points per 100 USD/ton move. Transitioning to low-carbon fuels (LNG, biofuel blends, methanol) raises capex and fuel cost expectations by 20-50%, complicating long-term financial planning and vessel efficiency investments.

Interest rate impacts on capital expenditure

Odfjell’s capital-intensive fleet renewal makes it highly sensitive to interest rates; a 100 bp rise can add materially to finance costs on newbuilds typically priced at $50–70m per MR/chemical tanker. Higher rates in 2024–25 raised average borrowing costs across shipping, increasing retrofit financing expenses for decarbonization technologies by an estimated 10–15%. Maintaining leverage near targeted covenants and securing long-term low-rate loans or export credit is therefore critical to control rising asset replacement costs.

Currency exchange rate fluctuations

As a global operator, Odfjell earns revenue and incurs costs primarily in USD and NOK; in 2024 about 78% of group revenue was USD-denominated while significant Norwegian operations expose results to NOK volatility.

Exchange swings create translational gains/losses—Odfjell reported a NOK 50–150m annual FX sensitivity range in recent years—affecting reported EBITDA and equity.

Robust hedging (forwards, options, natural hedges) is used to mitigate currency risk across the terminal network and shipping contracts.

- ~78% revenue in USD (2024)

- Reported FX sensitivity NOK 50–150m annually

- Hedging: forwards, options, natural hedges

Supply and demand balance in the tanker market

The balance between global chemical tanker supply and cargo volumes drives Odfjell’s earnings; as of end-2025 the global chemical tanker orderbook stood at about 6–8% of fleet capacity after several years of muted newbuild orders, sustaining freight rates and EBITDA margins for established owners.

Tracking the orderbook and scrapping rates is critical—if orderbook rises above ~15% of fleet it historically signals upcoming overcapacity and rate pressure.

- Orderbook ~6–8% of fleet (end-2025)

- Threshold for overcapacity risk ~15% orderbook

- Muted new orders -> elevated spot rates and EBITDA

Rising demand and rates vs cost pressures: fuel, capex, FX and overcapacity risks

Demand ties to global chemical output (up 2.1% in 2024); fleet utilization swung 78% (2023) to higher in 2024, lifting rates. Bunker volatility (420→650 USD/ton in 2024) and capex for low‑carbon fuels raise costs 20–50%. Interest hikes add financing costs for $50–70m newbuilds; orderbook ~6–8% end‑2025 (overcapacity risk >15%). FX: ~78% revenue USD; NOK FX sensitivity NOK 50–150m.

| Metric | Value |

|---|---|

| Global chem output (2024) | +2.1% |

| Fleet utilization (2023) | 78% |

| Bunker 380CST range (2024) | 420–650 USD/ton |

| Orderbook (end‑2025) | 6–8% |

| Revenue USD share (2024) | ~78% |

Full Version Awaits

Odfjell PESTLE Analysis

The preview shown here is the exact Odfjell PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Get a competitive advantage with our targeted PESTLE Analysis of Odfjell—uncover how political shifts, economic cycles, environmental regulations, and tech trends shape its strategy and risk profile; buy the full report to access actionable insights, editable charts, and forecasts you can use in investment cases or strategic planning.

Political factors

Geopolitical instability in maritime corridors

Odfjell faces higher costs as Red Sea/Suez unrest forces rerouting: 2024 reports show average detour adds 7–14 days and fuel costs up to $40,000 per voyage, disrupting schedules and EBITDA margins; ongoing Middle East volatility requires 24/7 political monitoring to protect crew and chemical cargoes; prolonged instability lifted war-risk premiums by 30–60% in 2024, shrinking route efficiency and raising per-tonne transport costs.

Trade protectionism and tariff barriers

Shifting trade policies and tariffs between the US, China and EU reshape bulk liquids flows; US-China tariffs and EU carbon border adjustment talks contributed to a 6–8% decline in some intercontinental chemical shipments in 2023–2024, pressuring Odfjell’s long-haul utilisation. Odfjell must navigate complex FTAs and customs regimes that affect export/import volumes across jurisdictions and trading corridors. Rising protectionism drives regional chemical reshoring—reducing demand on long-haul chemical tanker routes and pressuring freight rates and fleet deployment.

Energy security and strategic autonomy

Governments in Europe and Asia are increasing energy-security measures and localizing chemical supply chains, driving new tank terminal investments; EU strategic autonomy plans target €300bn annual critical materials by 2025 and China’s 14th Five-Year Plan emphasizes domestic chemical capacity expansion.

Sanctions compliance and regulatory oversight

Odfjell must operate advanced sanctions compliance as international restrictions—expanded after 2022 conflicts—expose chemical tankers to denied-party lists; in 2024 Odfjell reported compliance-related costs rising, aligned with industry averages of 0.2–0.5% of revenue for large shipping firms, to avoid fines and reputational harm.

The evolving political landscape requires continuous screening and audit processes; non-compliance risks fines exceeding millions of dollars and loss of port access in key markets like EU, UK and US.

- Rising compliance spend: ~0.2–0.5% revenue benchmark

- Regulatory scope: dynamic denied-party lists post-2022

- Penalties: multi-million-dollar fines and market exclusion

International maritime diplomacy

Coordination between flag states and the IMO is critical for unified standards in chemical shipping; as of 2024 over 170 IMO member states participate in rule-making that affects Odfjell’s fleet of ~80 chemical tankers and 8.2 million dwt global fleet capacity across the sector.

Political cooperation or friction shapes the speed of harmonization: recent IMO amendments (2023–2024) on safety and GHG measures show faster uptake where diplomatic alignment exists, reducing compliance lag for carriers like Odfjell.

Stable diplomatic relations lower port denial risks and enable standardized protocols; Odfjell’s global port calls (thousands annually) and 2024 revenue of USD ~1.0 billion benefit from smoother clearances and consistent operational rules.

- IMO membership >170 states impacts rule uniformity

- Odfjell fleet ~80 tankers — benefits from harmonized standards

- 2024 sector revenue/context: Odfjell ~USD 1.0bn

Red Sea detours hike costs, war-risk premiums and squeeze chemical shipping margins

Geopolitical unrest (Red Sea/Suez) adds 7–14 days detours and up to $40,000 fuel per voyage, raising war-risk premiums 30–60% in 2024; trade tensions cut some intercontinental chemical flows 6–8% (2023–24), pressuring utilisation; compliance costs ~0.2–0.5% of revenue with multi-million fines risk; IMO >170 members affect harmonization, aiding Odfjell’s ~80-vessel fleet and 2024 revenue ~USD 1.0bn.

| Metric | 2023–24 |

|---|---|

| Detour delay | 7–14 days |

| Extra fuel/leg | up to $40,000 |

| War-risk premium | +30–60% |

| Trade flow decline | 6–8% |

| Compliance cost | 0.2–0.5% rev |

| Odfjell fleet | ~80 |

| 2024 revenue | ~USD 1.0bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Odfjell across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for Odfjell that eases meeting prep and decision-making by highlighting external risks and opportunities, ready to drop into presentations or share across teams.

Economic factors

Global chemical production cycles

The demand for Odfjell’s bulk chemical and tank terminal services tracks global chemical production, which rose 2.1% in 2024 after a 0.8% contraction in 2023, making tanker utilization sensitive to cyclical shifts in acids, edible oils and specialty liquids.

Economic slowdowns in EU, China or US—regions accounting for over 60% of chemical output—can cut production and pushed chemical tanker fleet utilization down to 78% in 2023 from 84% in 2021, reducing freight revenues.

Conversely, 2024 expansion increased seaborne chemical volumes by about 3–4%, supporting higher freight rates and boosting Odfjell’s operating margin, which improved toward pre-downturn levels as demand for sophisticated logistics rose.

Volatility in bunker fuel pricing

Fuel costs are among Odfjell's largest operating expenses, with bunker representing roughly 20-30% of voyage costs; global bunker 380CST prices swung from about 420 USD/ton in Jan 2024 to peaks near 650 USD/ton in late 2024, directly compressing margins. Odfjell uses fuel adjustment clauses, but sudden spikes still create short-term cash strain—EBITDA sensitivity can be several percentage points per 100 USD/ton move. Transitioning to low-carbon fuels (LNG, biofuel blends, methanol) raises capex and fuel cost expectations by 20-50%, complicating long-term financial planning and vessel efficiency investments.

Interest rate impacts on capital expenditure

Odfjell’s capital-intensive fleet renewal makes it highly sensitive to interest rates; a 100 bp rise can add materially to finance costs on newbuilds typically priced at $50–70m per MR/chemical tanker. Higher rates in 2024–25 raised average borrowing costs across shipping, increasing retrofit financing expenses for decarbonization technologies by an estimated 10–15%. Maintaining leverage near targeted covenants and securing long-term low-rate loans or export credit is therefore critical to control rising asset replacement costs.

Currency exchange rate fluctuations

As a global operator, Odfjell earns revenue and incurs costs primarily in USD and NOK; in 2024 about 78% of group revenue was USD-denominated while significant Norwegian operations expose results to NOK volatility.

Exchange swings create translational gains/losses—Odfjell reported a NOK 50–150m annual FX sensitivity range in recent years—affecting reported EBITDA and equity.

Robust hedging (forwards, options, natural hedges) is used to mitigate currency risk across the terminal network and shipping contracts.

- ~78% revenue in USD (2024)

- Reported FX sensitivity NOK 50–150m annually

- Hedging: forwards, options, natural hedges

Supply and demand balance in the tanker market

The balance between global chemical tanker supply and cargo volumes drives Odfjell’s earnings; as of end-2025 the global chemical tanker orderbook stood at about 6–8% of fleet capacity after several years of muted newbuild orders, sustaining freight rates and EBITDA margins for established owners.

Tracking the orderbook and scrapping rates is critical—if orderbook rises above ~15% of fleet it historically signals upcoming overcapacity and rate pressure.

- Orderbook ~6–8% of fleet (end-2025)

- Threshold for overcapacity risk ~15% orderbook

- Muted new orders -> elevated spot rates and EBITDA

Rising demand and rates vs cost pressures: fuel, capex, FX and overcapacity risks

Demand ties to global chemical output (up 2.1% in 2024); fleet utilization swung 78% (2023) to higher in 2024, lifting rates. Bunker volatility (420→650 USD/ton in 2024) and capex for low‑carbon fuels raise costs 20–50%. Interest hikes add financing costs for $50–70m newbuilds; orderbook ~6–8% end‑2025 (overcapacity risk >15%). FX: ~78% revenue USD; NOK FX sensitivity NOK 50–150m.

| Metric | Value |

|---|---|

| Global chem output (2024) | +2.1% |

| Fleet utilization (2023) | 78% |

| Bunker 380CST range (2024) | 420–650 USD/ton |

| Orderbook (end‑2025) | 6–8% |

| Revenue USD share (2024) | ~78% |

Full Version Awaits

Odfjell PESTLE Analysis

The preview shown here is the exact Odfjell PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment review.