Oerlikon PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our targeted PESTLE Analysis of Oerlikon—uncover how political shifts, economic cycles, tech advances, and regulatory trends will shape its trajectory; download the full report now for actionable, board-ready insights to inform investments, strategy, and risk management.

Political factors

Geopolitical Trade Barriers and Tariffs

Trade tensions among the US, China and EU materially affect Oerlikon’s supply chain for high-tech machinery; tariffs raised between 2021–2025 increased component import costs by an estimated 6–9%, pressuring margins on surface solution equipment.

Rising protectionism through late 2025 has driven Oerlikon to expand localized production—adding two new Asian sites and one in North America—to avoid average cross-border tariff rates of ~8% on critical parts.

Fluctuating trade agreements and periodic export controls restrict access to key manufacturing markets, with Asia and North America accounting for roughly 68% of Oerlikon’s revenue exposure, increasing strategic volatility.

Defense and Aerospace Strategic Spending

Oerlikon’s aerospace segment is tied to national defense budgets and government aviation initiatives; global defense spending rose 4.1% to a record US$2.24 trillion in 2023, supporting demand for advanced coatings and AM parts for military aircraft.

Heightened geopolitical instability since 2022 has accelerated procurement cycles, boosting market for thermal and wear coatings and metal additive manufacturing used in fighter and transport platforms.

Political moves to reshore aerospace supply chains in the US and EU—with US defense industrial incentives exceeding US$100 billion in recent packages and EU strategic autonomy programs—create partnership and contract opportunities for Oerlikon with government-contracted suppliers.

Energy Sovereignty and Hydrogen Policy

Government mandates for energy independence are pushing hydrogen targets: EU aims 20 Mt electrolytic hydrogen by 2030 and Germany committed €9 billion in 2024 for hydrogen projects, accelerating demand for storage and transport solutions.

Oerlikon Metco benefits from subsidies and frameworks—EU Innovation Fund and Germany’s H2Global—helping finance coating and additive manufacturing for hydrogen infrastructure; market for hydrogen equipment projected to reach $240bn by 2030 (BloombergNEF 2025).

Policies promoting green transitions increase demand for specialized surface solutions in high-wear energy environments; Oerlikon’s coatings address embrittlement and corrosion, aligning with rising CAPEX in renewable and hydrogen projects (global clean energy investment $1.7trn in 2024, IEA).

Geopolitical Supply Chain Resilience

Geopolitical instability in cobalt- and nickel-producing countries raises supply risk for Oerlikon, prompting diversification plans after 2024 when 30% of specialty-metal volumes originated from high-risk regions.

Regulators and investors demand conflict-free sourcing; Oerlikon faces audits and potential tariffs tied to provenance compliance, increasing supply-chain compliance costs by an estimated 2–3% of COGS in 2024.

To secure production through 2025, Oerlikon is expanding strategic stockpiles equal to ~3 months of consumption and qualifying alternative suppliers in Europe and North America to reduce single-region exposure.

- 30% of volumes from high-risk regions (2024)

- Compliance adds ~2–3% to COGS

- Stockpiles = ~3 months consumption

- Supplier diversification into EU/NA underway

Incentives for Green Manufacturing

Governments worldwide offered over USD 450 billion in clean manufacturing incentives in 2024; tax credits and grants accelerate adoption of energy-efficient equipment.

Oerlikon’s Polymer Processing Solutions provides low-energy textile extrusion and finishing systems that can cut factory energy use by up to 25%, aligning with subsidy criteria.

Leveraging incentives can lower Oerlikon’s effective tax rate and boost revenue from its sustainable-tech portfolio, which accounted for about 18% of group sales in 2024.

- USD 450B global clean manufacturing incentives (2024)

- Up to 25% energy savings from PPS equipment

- Sustainable-tech ≈18% of Oerlikon 2024 sales

Geo‑trade frictions, defense & hydrogen push costs up, fueling localization and green growth

Trade tensions, export controls and reshoring (US/EU incentives >$100bn) raised component costs ~6–9% (2021–25) and drove localization; defense spending up 4.1% to $2.24tn (2023) supports AM/coatings demand; hydrogen targets (EU 20 Mt by 2030) and €9bn Germany support drive market growth; 30% specialty metals from high‑risk regions (2024), compliance adds ~2–3% COGS; sustainable tech ≈18% of 2024 sales.

| Metric | Value |

|---|---|

| Tariff impact | 6–9% |

| Defense spend | $2.24tn (2023) |

| Hydrogen target | EU 20 Mt by 2030 |

| High‑risk sourcing | 30% (2024) |

| Compliance cost | 2–3% COGS |

| Sustainable sales | 18% (2024) |

What is included in the product

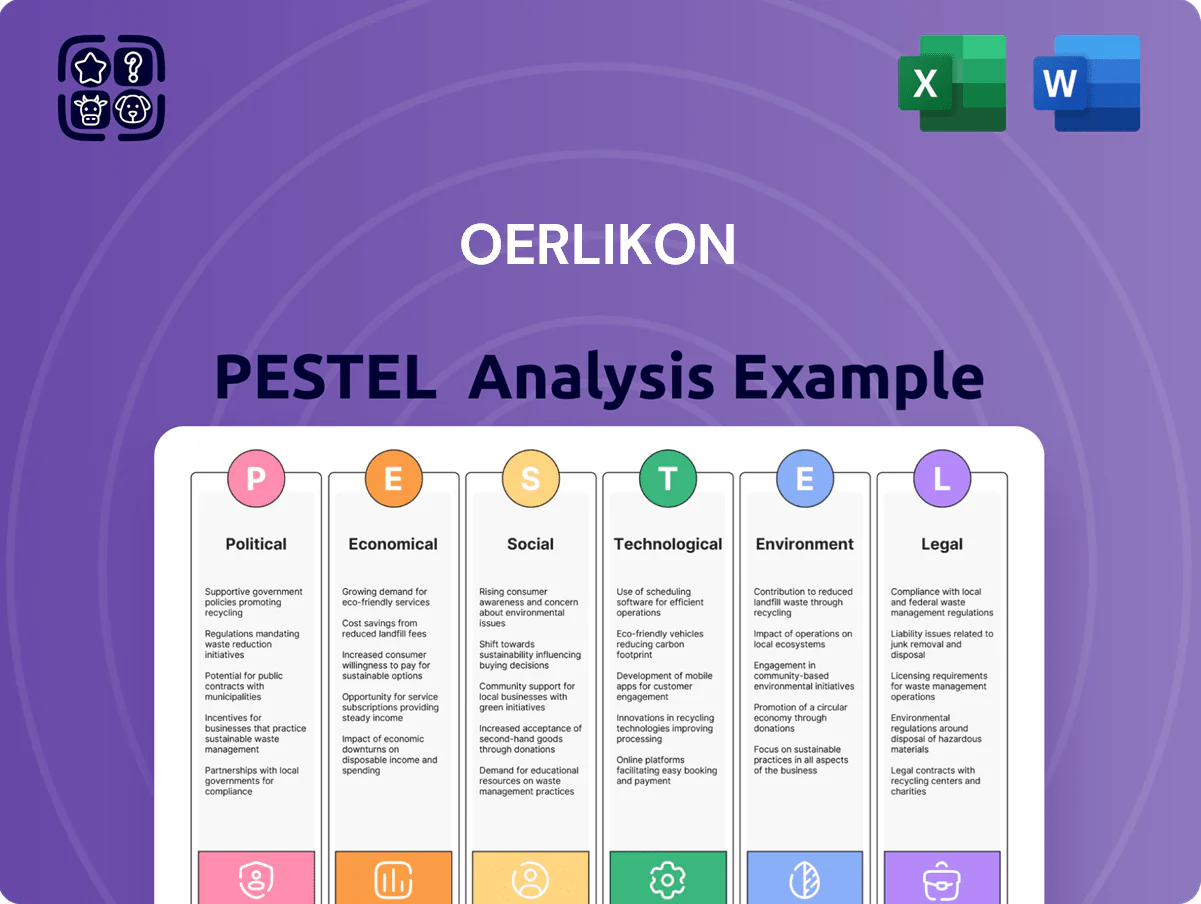

Explores how external macro-environmental factors uniquely affect Oerlikon across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and investors.

Provides a concise, visually segmented PESTLE summary of Oerlikon that’s easily dropped into presentations or shared across teams to support quick alignment and risk discussions during planning sessions.

Economic factors

Industrial Capital Expenditure Cycles

The demand for Oerlikon’s heavy machinery and surface solutions is tightly linked to the global industrial capex cycle; global manufacturing investment grew 3.1% in 2024 but volatility persists into 2025 as global interest rates averaged 4.5% in H2 2025, creating a mixed environment for auto and textile capex. Customers in these sectors have delayed orders—OEM machinery orders fell ~6% YoY in 2025Q1—forcing Oerlikon to manage revenue timing as buyers adjust purchases to borrowing costs and outlooks.

Volatility in Specialty Metal Prices

Oerlikon depends on tungsten, cobalt and titanium for materials and AM; tungsten spot prices rose ~28% in 2024 and cobalt averaged $35–40/lb in 2024–2025, creating margin pressure when costs cannot be passed on. Commodity volatility and speculative flows can spike input costs rapidly, but Oerlikon mitigates exposure via hedging programs and multi-year supply contracts covering ~60–80% of requirements, stabilizing its cost base.

Currency Exchange Rate Sensitivity

As a Swiss-based global entity, Oerlikon is highly sensitive to CHF moves versus EUR and USD; a 10% CHF appreciation since 2021 cut reported export competitiveness and reduced translated revenues—CHF strengthened ~8% vs EUR and ~12% vs USD by end-2024. Currency swings materially affect margins and the translation of ~65% of FY2024 international sales into CHF. Management emphasizes natural hedging, aligning production costs with local sales currencies to limit FX exposure and reported volatility.

Recovery of Global Textile Markets

The Polymer Processing Solutions division depends on apparel and technical textile demand; China and India account for about 40-50% of global man-made fiber capacity, so a consumer slowdown there cuts Oerlikon Barmag order intake and utilization.

An economic rebound—China GDP growth ~5.2% (2024) and India ~7% (2024)—fuels large capacity expansions; Oerlikon reported Q4 2024 backlog growth of ~12%, reflecting higher system orders.

- Dependency: Apparel/textile demand drives PPS sales

- Risk: China/India slowdowns reduce orders

- Upside: 2024 GDP recovery linked to ~12% backlog rise

- Concentration: 40–50% of man-made fiber capacity in Asia

Inflationary Pressures on R and D Costs

Persistent inflation in specialized labor markets and rising prices for technical components pushed Oerlikon’s R&D cost base up; Swiss manufacturing wage growth averaged 3.2% in 2024, raising engineer and scientist payroll expenses significantly.

Maintaining leadership in additive manufacturing and surface solutions requires continuous investment; Oerlikon invested CHF 170m in R&D in 2024, a figure strained by higher input costs.

The company must rebalance innovation budgets against operational efficiency to protect margins and market share.

- 2024 R&D spend CHF 170m

- Swiss manufacturing wage growth ~3.2% (2024)

- Higher component inflation adds upward pressure on unit R&D costs

Oerlikon margins squeezed by commodity spikes, CHF strength and rising Swiss costs

Global capex volatility (manufacturing investment +3.1% in 2024) and higher commodity costs (tungsten +28% in 2024; cobalt $35–40/lb 2024–25) pressure Oerlikon margins, while CHF strength (~+8% vs EUR, +12% vs USD by end-2024) reduces reported revenues; R&D CHF170m (2024) and Swiss wage growth ~3.2% raise costs, offset partially by hedges and multi‑year supply contracts.

| Metric | 2024/25 |

|---|---|

| Manufacturing capex | +3.1% (2024) |

| Tungsten | +28% (2024) |

| Cobalt | $35–40/lb (2024–25) |

| CHF vs EUR/USD | +8% / +12% vs end‑2024 |

| R&D | CHF170m (2024) |

What You See Is What You Get

Oerlikon PESTLE Analysis

The preview shown here is the exact Oerlikon PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our targeted PESTLE Analysis of Oerlikon—uncover how political shifts, economic cycles, tech advances, and regulatory trends will shape its trajectory; download the full report now for actionable, board-ready insights to inform investments, strategy, and risk management.

Political factors

Geopolitical Trade Barriers and Tariffs

Trade tensions among the US, China and EU materially affect Oerlikon’s supply chain for high-tech machinery; tariffs raised between 2021–2025 increased component import costs by an estimated 6–9%, pressuring margins on surface solution equipment.

Rising protectionism through late 2025 has driven Oerlikon to expand localized production—adding two new Asian sites and one in North America—to avoid average cross-border tariff rates of ~8% on critical parts.

Fluctuating trade agreements and periodic export controls restrict access to key manufacturing markets, with Asia and North America accounting for roughly 68% of Oerlikon’s revenue exposure, increasing strategic volatility.

Defense and Aerospace Strategic Spending

Oerlikon’s aerospace segment is tied to national defense budgets and government aviation initiatives; global defense spending rose 4.1% to a record US$2.24 trillion in 2023, supporting demand for advanced coatings and AM parts for military aircraft.

Heightened geopolitical instability since 2022 has accelerated procurement cycles, boosting market for thermal and wear coatings and metal additive manufacturing used in fighter and transport platforms.

Political moves to reshore aerospace supply chains in the US and EU—with US defense industrial incentives exceeding US$100 billion in recent packages and EU strategic autonomy programs—create partnership and contract opportunities for Oerlikon with government-contracted suppliers.

Energy Sovereignty and Hydrogen Policy

Government mandates for energy independence are pushing hydrogen targets: EU aims 20 Mt electrolytic hydrogen by 2030 and Germany committed €9 billion in 2024 for hydrogen projects, accelerating demand for storage and transport solutions.

Oerlikon Metco benefits from subsidies and frameworks—EU Innovation Fund and Germany’s H2Global—helping finance coating and additive manufacturing for hydrogen infrastructure; market for hydrogen equipment projected to reach $240bn by 2030 (BloombergNEF 2025).

Policies promoting green transitions increase demand for specialized surface solutions in high-wear energy environments; Oerlikon’s coatings address embrittlement and corrosion, aligning with rising CAPEX in renewable and hydrogen projects (global clean energy investment $1.7trn in 2024, IEA).

Geopolitical Supply Chain Resilience

Geopolitical instability in cobalt- and nickel-producing countries raises supply risk for Oerlikon, prompting diversification plans after 2024 when 30% of specialty-metal volumes originated from high-risk regions.

Regulators and investors demand conflict-free sourcing; Oerlikon faces audits and potential tariffs tied to provenance compliance, increasing supply-chain compliance costs by an estimated 2–3% of COGS in 2024.

To secure production through 2025, Oerlikon is expanding strategic stockpiles equal to ~3 months of consumption and qualifying alternative suppliers in Europe and North America to reduce single-region exposure.

- 30% of volumes from high-risk regions (2024)

- Compliance adds ~2–3% to COGS

- Stockpiles = ~3 months consumption

- Supplier diversification into EU/NA underway

Incentives for Green Manufacturing

Governments worldwide offered over USD 450 billion in clean manufacturing incentives in 2024; tax credits and grants accelerate adoption of energy-efficient equipment.

Oerlikon’s Polymer Processing Solutions provides low-energy textile extrusion and finishing systems that can cut factory energy use by up to 25%, aligning with subsidy criteria.

Leveraging incentives can lower Oerlikon’s effective tax rate and boost revenue from its sustainable-tech portfolio, which accounted for about 18% of group sales in 2024.

- USD 450B global clean manufacturing incentives (2024)

- Up to 25% energy savings from PPS equipment

- Sustainable-tech ≈18% of Oerlikon 2024 sales

Geo‑trade frictions, defense & hydrogen push costs up, fueling localization and green growth

Trade tensions, export controls and reshoring (US/EU incentives >$100bn) raised component costs ~6–9% (2021–25) and drove localization; defense spending up 4.1% to $2.24tn (2023) supports AM/coatings demand; hydrogen targets (EU 20 Mt by 2030) and €9bn Germany support drive market growth; 30% specialty metals from high‑risk regions (2024), compliance adds ~2–3% COGS; sustainable tech ≈18% of 2024 sales.

| Metric | Value |

|---|---|

| Tariff impact | 6–9% |

| Defense spend | $2.24tn (2023) |

| Hydrogen target | EU 20 Mt by 2030 |

| High‑risk sourcing | 30% (2024) |

| Compliance cost | 2–3% COGS |

| Sustainable sales | 18% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Oerlikon across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and investors.

Provides a concise, visually segmented PESTLE summary of Oerlikon that’s easily dropped into presentations or shared across teams to support quick alignment and risk discussions during planning sessions.

Economic factors

Industrial Capital Expenditure Cycles

The demand for Oerlikon’s heavy machinery and surface solutions is tightly linked to the global industrial capex cycle; global manufacturing investment grew 3.1% in 2024 but volatility persists into 2025 as global interest rates averaged 4.5% in H2 2025, creating a mixed environment for auto and textile capex. Customers in these sectors have delayed orders—OEM machinery orders fell ~6% YoY in 2025Q1—forcing Oerlikon to manage revenue timing as buyers adjust purchases to borrowing costs and outlooks.

Volatility in Specialty Metal Prices

Oerlikon depends on tungsten, cobalt and titanium for materials and AM; tungsten spot prices rose ~28% in 2024 and cobalt averaged $35–40/lb in 2024–2025, creating margin pressure when costs cannot be passed on. Commodity volatility and speculative flows can spike input costs rapidly, but Oerlikon mitigates exposure via hedging programs and multi-year supply contracts covering ~60–80% of requirements, stabilizing its cost base.

Currency Exchange Rate Sensitivity

As a Swiss-based global entity, Oerlikon is highly sensitive to CHF moves versus EUR and USD; a 10% CHF appreciation since 2021 cut reported export competitiveness and reduced translated revenues—CHF strengthened ~8% vs EUR and ~12% vs USD by end-2024. Currency swings materially affect margins and the translation of ~65% of FY2024 international sales into CHF. Management emphasizes natural hedging, aligning production costs with local sales currencies to limit FX exposure and reported volatility.

Recovery of Global Textile Markets

The Polymer Processing Solutions division depends on apparel and technical textile demand; China and India account for about 40-50% of global man-made fiber capacity, so a consumer slowdown there cuts Oerlikon Barmag order intake and utilization.

An economic rebound—China GDP growth ~5.2% (2024) and India ~7% (2024)—fuels large capacity expansions; Oerlikon reported Q4 2024 backlog growth of ~12%, reflecting higher system orders.

- Dependency: Apparel/textile demand drives PPS sales

- Risk: China/India slowdowns reduce orders

- Upside: 2024 GDP recovery linked to ~12% backlog rise

- Concentration: 40–50% of man-made fiber capacity in Asia

Inflationary Pressures on R and D Costs

Persistent inflation in specialized labor markets and rising prices for technical components pushed Oerlikon’s R&D cost base up; Swiss manufacturing wage growth averaged 3.2% in 2024, raising engineer and scientist payroll expenses significantly.

Maintaining leadership in additive manufacturing and surface solutions requires continuous investment; Oerlikon invested CHF 170m in R&D in 2024, a figure strained by higher input costs.

The company must rebalance innovation budgets against operational efficiency to protect margins and market share.

- 2024 R&D spend CHF 170m

- Swiss manufacturing wage growth ~3.2% (2024)

- Higher component inflation adds upward pressure on unit R&D costs

Oerlikon margins squeezed by commodity spikes, CHF strength and rising Swiss costs

Global capex volatility (manufacturing investment +3.1% in 2024) and higher commodity costs (tungsten +28% in 2024; cobalt $35–40/lb 2024–25) pressure Oerlikon margins, while CHF strength (~+8% vs EUR, +12% vs USD by end-2024) reduces reported revenues; R&D CHF170m (2024) and Swiss wage growth ~3.2% raise costs, offset partially by hedges and multi‑year supply contracts.

| Metric | 2024/25 |

|---|---|

| Manufacturing capex | +3.1% (2024) |

| Tungsten | +28% (2024) |

| Cobalt | $35–40/lb (2024–25) |

| CHF vs EUR/USD | +8% / +12% vs end‑2024 |

| R&D | CHF170m (2024) |

What You See Is What You Get

Oerlikon PESTLE Analysis

The preview shown here is the exact Oerlikon PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis and decision-making.