OGE Energy Boston Consulting Group Matrix

Download Your Competitive Advantage

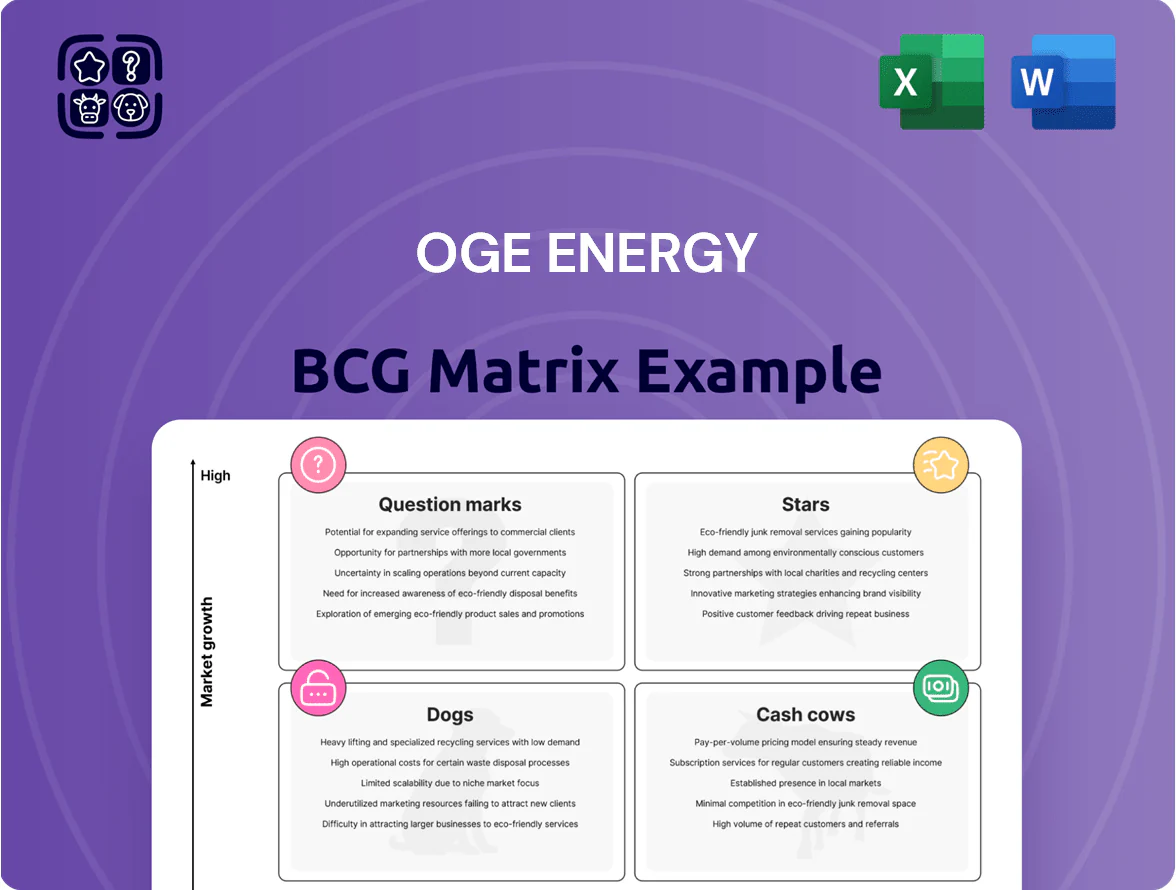

OGE Energy’s preliminary BCG Matrix snapshot highlights utility-scale generation as a potential Cash Cow with steady market share and regulated returns, while emerging renewables appear as Question Marks needing capital to grow market presence; transmission and distribution show Cash Cow characteristics, and legacy fossil assets risk sliding toward Dogs without strategic repositioning. This preview teases strategic moves and allocation priorities—purchase the full BCG Matrix for quadrant-by-quadrant analysis, data-backed recommendations, and ready-to-use Word and Excel deliverables to guide smarter investment and operational decisions.

Stars

Data Center Load Expansion

Finalizing a 1 GW contract with a hyperscale data center operator positions OGE Energy as a Star in the BCG matrix, adding roughly 1,000 MW of new load and driving revenue upside—at ~$80/MWh retail value that implies ~ $70–90m annual incremental EBITDA before regulated cost recovery.

Weather-normalized load rose 7% in 2025 from digital infrastructure growth, and management is crafting a large-load tariff to capture peak revenues while funding grid upgrades—estimated $120–200m capital spend over 2026–2028 to maintain reliability.

Frontier Battery Storage Project

As a Star in OGE Energy’s BCG Matrix, the 300-megawatt Frontier Energy Storage project—filed for regulatory pre-approval in 2025—targets high growth by addressing rising peak demand and intermittency from renewables.

The project marks OGE’s strategic pivot to modern battery storage, improving grid stability and fast-ramping capacity needed to integrate more wind and solar resources.

Frontier contributes to the 1.9 GW resource gap in OGE’s 2026 Integrated Resource Plan and, at an estimated $200–$250/kW installed, implies capex of roughly $60–$75 million for the 300 MW nameplate.

Advanced Transmission Infrastructure

OGE is expanding transmission with the 61-mile Piedmont rebuild and the Fort Smith–Muskogee project, classifying these as Stars in its BCG matrix due to high market share and growth; the company expects to spend roughly $1.8–2.2 billion on transmission 2024–2030, boosting regional capacity by an estimated 1,200–1,500 MW.

Natural Gas Capacity Replacements

The Horseshoe Lake Units 13 and 14 and new Tinker combustion turbines are a high-growth priority replacing aging gas units; together they add 550 MW of lower-emission capacity targeted to meet projected 2026 peak demand and support reliability.

OGE secured regulatory rider recovery to place these assets into the rate base, bolstering capital recovery and contributing to forecasted customer load growth and earnings stability.

- 550 MW combined capacity

- Targets 2026 demand peak

- Lower emissions vs older units

- Regulatory rider ensures rate-base recovery

Smart Grid Modernization

OGE Energy allocates roughly $400 million (2024–2026 capex plan) to smart grid and advanced metering in Oklahoma, a high-growth segment boosting resilience to extreme weather and enabling future IoT energy services.

These investments support OGE’s dominant market share by reducing outage hours (target: 20% drop by 2026) and enabling new demand‑response revenue streams estimated at $15–25 million annually by 2027.

- $400M capex (2024–2026)

- 20% outage-hour reduction target by 2026

- $15–25M potential annual demand-response revenue by 2027

OGE growth surge: 1GW data load, 300MW storage, $2B transmission, $400M smart-grid

OGE’s Stars—1 GW data-center load, 300 MW Frontier storage, ~550 MW new units, and $400M smart-grid—drive high growth and market share, implying ~$70–90M EBITDA from the data contract, $60–75M capex for Frontier, $1.8–2.2B transmission spend (2024–30), and $400M AMI/smart-grid (2024–26).

| Asset | Size | Capex | 2026 impact |

|---|---|---|---|

| Data-center load | 1,000 MW | — | $70–90M EBITDA |

| Frontier storage | 300 MW | $60–75M | Peak relief |

| New thermal units | 550 MW | — | Reliability |

| Transmission | 1,200–1,500 MW | $1.8–2.2B | Capacity boost |

| Smart grid / AMI | — | $400M | 20% fewer outage hrs |

What is included in the product

BCG Matrix breakdown of OGE Energy’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs for investment decisions.

One-page BCG matrix showing OGE Energy units by quadrant for quick strategic clarity.

Cash Cows

Regulated Residential Electric Service

The core regulated residential electric service is OGE Energy’s main cash cow, serving over 913,000 customers across Oklahoma and western Arkansas and delivering stable, predictable revenue in a mature market.

With dominant regional market share, the utility funds dividends and capex; in 2025 it contributed $2.47 per share to consolidated earnings, underscoring its role as the company’s financial bedrock.

Existing Natural Gas Generation Fleet

OGE’s existing natural gas fleet, with combined capacity around 1,200 MW and typical heat rates near 7,800 Btu/kWh, sits in a mature, low-growth market yet delivers high efficiency and steady baseload generation.

These plants produce strong cash flow—contributing to OGE Energy Corp’s 2025 guidance and enabling a 60–70% dividend payout ratio—requiring minimal promotional capex beyond routine maintenance.

Industrial and Commercial Baseload

OGE Energy’s Industrial and Commercial Baseload holds a dominant market share with roughly 55% of its regional commercial-industrial load in 2024, supplying consistent power to factories and data centers that need 24/7 reliability.

This mature segment generated about $850 million in 2024 regulated revenues, showing <1% volatility vs GDP and helping keep OGE’s investment-grade ratings (S&P BBB+, Moody’s Baa1 as of Dec 2024).

Stable cash flow from baseload operations supports interest coverage near 4.5x and enables steady long-term debt servicing—OGE had $3.4 billion total long-term debt at year-end 2024.

Dividend Distribution Program

OGE Energy has raised its dividend 18 consecutive years through 2025, reflecting a classic Cash Cow payout policy supported by steady regulated utility earnings—2024 consolidated net income was $327 million and utility rate base grew to $6.2 billion, underpinning reliable cash flow for distributions.

The dividend program yielded a 2025 forward yield near 4.2% (share price mid-2025), attracting income investors who value stability in a low-growth utility sector led by OGE’s regulated operations.

- 18 straight years of increases (through 2025)

- 2024 net income $327M; 2025 rate base ~$6.2B

- 2025 forward yield ~4.2%

- Regulated earnings drive predictable cash returns

Transmission and Distribution Grid

OGE Energy’s 30,000-square-mile transmission and distribution grid is a steady cash cow, delivering high market share and predictable cash flow; in 2025 regulated return on equity targets hover around 9.5–10.5%, supporting stable earnings.

Maintenance capital is recovered via established rate mechanisms—Oklahoma and Texas filings allowed ~60–70% recovery of infrastructure spend—so cash generation funds growth projects and covers dividends.

- 30,000 sq mi service area

- ROE targets ~9.5–10.5% (2025)

- 60–70% maintenance capex recovery

- Provides liquidity for Question Marks

OGE: Stable regulated cash flows, 18-year dividend streak and ~4.2% yield

OGE’s regulated electric and T&D operations are core cash cows, providing stable cash flow (2024 net income $327M; 2025 rate base ~$6.2B), funding an 18-year rising dividend (2025 forward yield ~4.2%) and supporting investment-grade ratings (S&P BBB+, Moody’s Baa1, Dec 2024).

| Metric | Value |

|---|---|

| 2024 Net Income | $327M |

| 2025 Rate Base | $6.2B |

| Dividend Run | 18 yrs |

| Forward Yield 2025 | ~4.2% |

What You See Is What You Get

OGE Energy BCG Matrix

The file you're previewing is the exact OGE Energy BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—fully formatted for strategic use. This preview mirrors the final downloadable document, built with market-backed analysis and ready for editing, printing, or inclusion in presentations. Upon purchase you'll get the complete, professional file immediately, prepared by strategy experts for seamless integration into your planning and stakeholder discussions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

OGE Energy’s preliminary BCG Matrix snapshot highlights utility-scale generation as a potential Cash Cow with steady market share and regulated returns, while emerging renewables appear as Question Marks needing capital to grow market presence; transmission and distribution show Cash Cow characteristics, and legacy fossil assets risk sliding toward Dogs without strategic repositioning. This preview teases strategic moves and allocation priorities—purchase the full BCG Matrix for quadrant-by-quadrant analysis, data-backed recommendations, and ready-to-use Word and Excel deliverables to guide smarter investment and operational decisions.

Stars

Data Center Load Expansion

Finalizing a 1 GW contract with a hyperscale data center operator positions OGE Energy as a Star in the BCG matrix, adding roughly 1,000 MW of new load and driving revenue upside—at ~$80/MWh retail value that implies ~ $70–90m annual incremental EBITDA before regulated cost recovery.

Weather-normalized load rose 7% in 2025 from digital infrastructure growth, and management is crafting a large-load tariff to capture peak revenues while funding grid upgrades—estimated $120–200m capital spend over 2026–2028 to maintain reliability.

Frontier Battery Storage Project

As a Star in OGE Energy’s BCG Matrix, the 300-megawatt Frontier Energy Storage project—filed for regulatory pre-approval in 2025—targets high growth by addressing rising peak demand and intermittency from renewables.

The project marks OGE’s strategic pivot to modern battery storage, improving grid stability and fast-ramping capacity needed to integrate more wind and solar resources.

Frontier contributes to the 1.9 GW resource gap in OGE’s 2026 Integrated Resource Plan and, at an estimated $200–$250/kW installed, implies capex of roughly $60–$75 million for the 300 MW nameplate.

Advanced Transmission Infrastructure

OGE is expanding transmission with the 61-mile Piedmont rebuild and the Fort Smith–Muskogee project, classifying these as Stars in its BCG matrix due to high market share and growth; the company expects to spend roughly $1.8–2.2 billion on transmission 2024–2030, boosting regional capacity by an estimated 1,200–1,500 MW.

Natural Gas Capacity Replacements

The Horseshoe Lake Units 13 and 14 and new Tinker combustion turbines are a high-growth priority replacing aging gas units; together they add 550 MW of lower-emission capacity targeted to meet projected 2026 peak demand and support reliability.

OGE secured regulatory rider recovery to place these assets into the rate base, bolstering capital recovery and contributing to forecasted customer load growth and earnings stability.

- 550 MW combined capacity

- Targets 2026 demand peak

- Lower emissions vs older units

- Regulatory rider ensures rate-base recovery

Smart Grid Modernization

OGE Energy allocates roughly $400 million (2024–2026 capex plan) to smart grid and advanced metering in Oklahoma, a high-growth segment boosting resilience to extreme weather and enabling future IoT energy services.

These investments support OGE’s dominant market share by reducing outage hours (target: 20% drop by 2026) and enabling new demand‑response revenue streams estimated at $15–25 million annually by 2027.

- $400M capex (2024–2026)

- 20% outage-hour reduction target by 2026

- $15–25M potential annual demand-response revenue by 2027

OGE growth surge: 1GW data load, 300MW storage, $2B transmission, $400M smart-grid

OGE’s Stars—1 GW data-center load, 300 MW Frontier storage, ~550 MW new units, and $400M smart-grid—drive high growth and market share, implying ~$70–90M EBITDA from the data contract, $60–75M capex for Frontier, $1.8–2.2B transmission spend (2024–30), and $400M AMI/smart-grid (2024–26).

| Asset | Size | Capex | 2026 impact |

|---|---|---|---|

| Data-center load | 1,000 MW | — | $70–90M EBITDA |

| Frontier storage | 300 MW | $60–75M | Peak relief |

| New thermal units | 550 MW | — | Reliability |

| Transmission | 1,200–1,500 MW | $1.8–2.2B | Capacity boost |

| Smart grid / AMI | — | $400M | 20% fewer outage hrs |

What is included in the product

BCG Matrix breakdown of OGE Energy’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs for investment decisions.

One-page BCG matrix showing OGE Energy units by quadrant for quick strategic clarity.

Cash Cows

Regulated Residential Electric Service

The core regulated residential electric service is OGE Energy’s main cash cow, serving over 913,000 customers across Oklahoma and western Arkansas and delivering stable, predictable revenue in a mature market.

With dominant regional market share, the utility funds dividends and capex; in 2025 it contributed $2.47 per share to consolidated earnings, underscoring its role as the company’s financial bedrock.

Existing Natural Gas Generation Fleet

OGE’s existing natural gas fleet, with combined capacity around 1,200 MW and typical heat rates near 7,800 Btu/kWh, sits in a mature, low-growth market yet delivers high efficiency and steady baseload generation.

These plants produce strong cash flow—contributing to OGE Energy Corp’s 2025 guidance and enabling a 60–70% dividend payout ratio—requiring minimal promotional capex beyond routine maintenance.

Industrial and Commercial Baseload

OGE Energy’s Industrial and Commercial Baseload holds a dominant market share with roughly 55% of its regional commercial-industrial load in 2024, supplying consistent power to factories and data centers that need 24/7 reliability.

This mature segment generated about $850 million in 2024 regulated revenues, showing <1% volatility vs GDP and helping keep OGE’s investment-grade ratings (S&P BBB+, Moody’s Baa1 as of Dec 2024).

Stable cash flow from baseload operations supports interest coverage near 4.5x and enables steady long-term debt servicing—OGE had $3.4 billion total long-term debt at year-end 2024.

Dividend Distribution Program

OGE Energy has raised its dividend 18 consecutive years through 2025, reflecting a classic Cash Cow payout policy supported by steady regulated utility earnings—2024 consolidated net income was $327 million and utility rate base grew to $6.2 billion, underpinning reliable cash flow for distributions.

The dividend program yielded a 2025 forward yield near 4.2% (share price mid-2025), attracting income investors who value stability in a low-growth utility sector led by OGE’s regulated operations.

- 18 straight years of increases (through 2025)

- 2024 net income $327M; 2025 rate base ~$6.2B

- 2025 forward yield ~4.2%

- Regulated earnings drive predictable cash returns

Transmission and Distribution Grid

OGE Energy’s 30,000-square-mile transmission and distribution grid is a steady cash cow, delivering high market share and predictable cash flow; in 2025 regulated return on equity targets hover around 9.5–10.5%, supporting stable earnings.

Maintenance capital is recovered via established rate mechanisms—Oklahoma and Texas filings allowed ~60–70% recovery of infrastructure spend—so cash generation funds growth projects and covers dividends.

- 30,000 sq mi service area

- ROE targets ~9.5–10.5% (2025)

- 60–70% maintenance capex recovery

- Provides liquidity for Question Marks

OGE: Stable regulated cash flows, 18-year dividend streak and ~4.2% yield

OGE’s regulated electric and T&D operations are core cash cows, providing stable cash flow (2024 net income $327M; 2025 rate base ~$6.2B), funding an 18-year rising dividend (2025 forward yield ~4.2%) and supporting investment-grade ratings (S&P BBB+, Moody’s Baa1, Dec 2024).

| Metric | Value |

|---|---|

| 2024 Net Income | $327M |

| 2025 Rate Base | $6.2B |

| Dividend Run | 18 yrs |

| Forward Yield 2025 | ~4.2% |

What You See Is What You Get

OGE Energy BCG Matrix

The file you're previewing is the exact OGE Energy BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—fully formatted for strategic use. This preview mirrors the final downloadable document, built with market-backed analysis and ready for editing, printing, or inclusion in presentations. Upon purchase you'll get the complete, professional file immediately, prepared by strategy experts for seamless integration into your planning and stakeholder discussions.