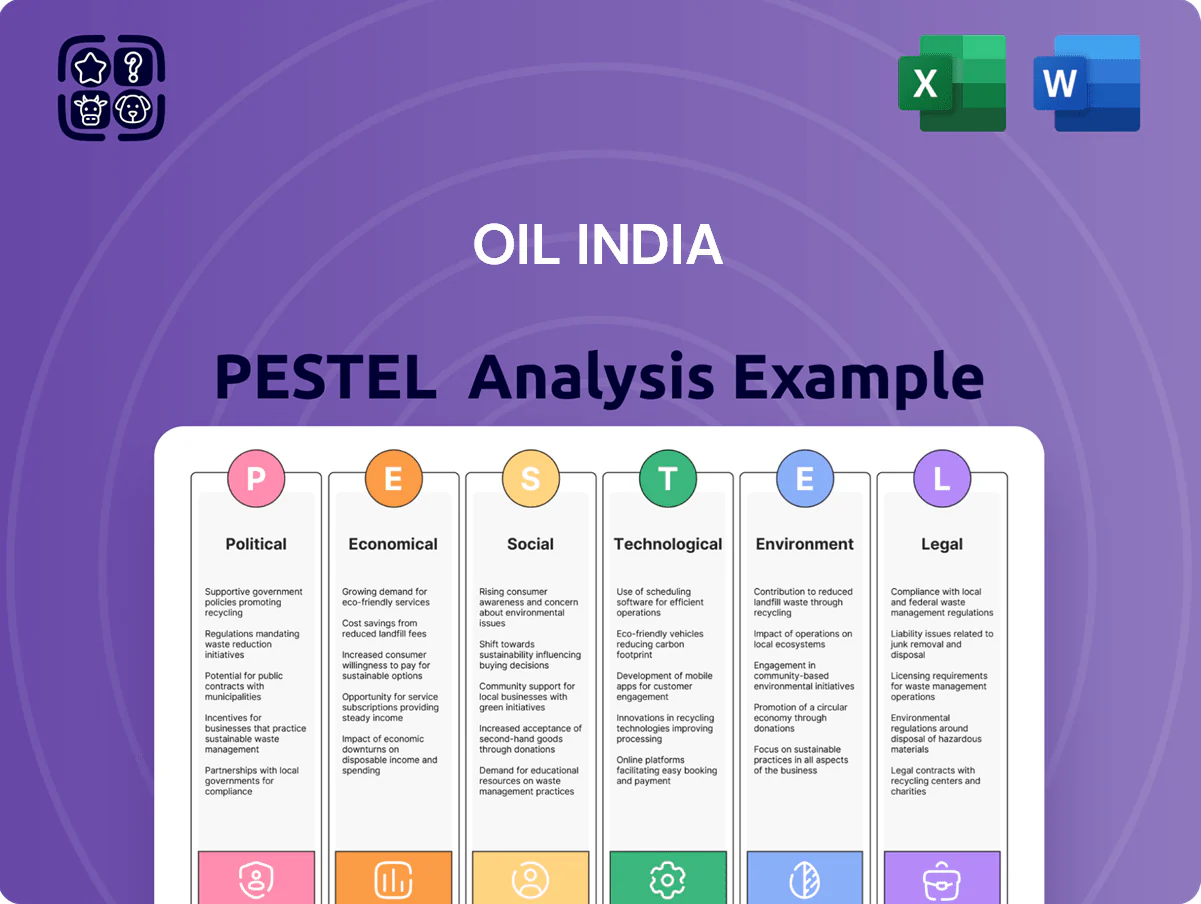

Oil India PESTLE Analysis

Skip the Research. Get the Strategy.

Stay ahead with our targeted PESTLE Analysis of Oil India—uncover how political shifts, economic cycles, and environmental regulations are reshaping operations and value creation; perfect for investors and strategists seeking actionable foresight. Purchase the full report to access detailed risk matrices, growth levers, and ready-to-use slides that accelerate decision-making and strategy development.

Political factors

Government Ownership and Strategic Control

As a Navratna PSU under the Ministry of Petroleum and Natural Gas, Oil India Limited benefits from state backing for capital-heavy projects—reflected in government equity of ~51% and access to subsidized funding—while being exposed to policy shifts; the 2024 national oil strategy prioritized energy security, guiding OIL’s capex of Rs 2,300 crore in FY2024 and influencing mandated dividend payouts (Rs 475 crore declared in FY2023) and overseas diplomatic-linked investments.

Geopolitical Stability in Northeast India

A significant portion of Oil India’s assets are in Assam and the Northeast, where 2024 production contributed roughly 60% of the company’s 8.4 MMtoe output, leaving operations highly sensitive to local political stability and security incidents; disruptions in 2023–24 linked to protests caused production halts of up to 5–7% in some fields. Political movements or civil unrest can delay exploration and threaten pipeline integrity, increasing capex and insurance costs. Maintaining strong relations with Assam and neighbouring state governments is essential to secure permits, rights-of-way and H1 2025 infrastructure projects worth ~INR 3–4 billion.

Energy Security and Import Substitution

The Indian government aims to cut crude import dependence from ~85% in 2023 to below 70% by 2030, pressuring Oil India to raise domestic output—its FY2024 crude oil production was ~1.4 million tonnes. Policies like the Hydrocarbon Exploration and Licensing Policy (HELP) and recent bid rounds enabled Oil India to acquire additional blocks, while Atmanirbhar Bharat incentives push investment in enhanced oil recovery and frontier basins to boost reserves and revenue.

International Diplomatic Relations

Oil India’s overseas portfolio—including stakes in Russia, Africa, and the Middle East—is sensitive to India’s bilateral ties and sanctions; in 2024, ~15–20% of upstream value was tied to these regions, raising exposure to sanctions-related cashflow disruptions.

Geopolitical tensions can impede dividend repatriation and JV operations; e.g., 2023–24 trade frictions delayed payments in some Russian and African projects, impacting cashflow and project timelines.

Political risk insurance and active diplomatic support are essential; Oil India reported covering ~60% of its foreign investments with PRI by 2024 and seeks government facilitation for dispute resolution and repatriation.

- Foreign exposure ~15–20% of upstream value (2024)

- ~60% of foreign investments covered by political risk insurance (2024)

- Sanctions/tensions have caused dividend delays in 2023–24

Subsidy Burden and Pricing Policies

Political control over domestic gas pricing remains pivotal for Oil India; despite market-linked pricing for petroleum, gas prices grew only modestly after 2023 reforms, keeping upstream margins under pressure.

Government rejection of parts of the Kirit Parikh Committee recommendations has limited uplift for legacy-field economics, reducing potential revenue increases for older assets.

Recent ad hoc windfall tax adjustments and royalty hikes—used in 2024–2025 to curb fiscal deficits and tame inflation—have periodically trimmed operator EBITDA by up to mid-single-digit percentage points.

- Market-linked petrol; gas pricing politically constrained

- Kirit Parikh interventions blunt legacy-field profitability

- 2024–25 windfall/royalty moves cut operator EBITDA ~3–7%

State-backed energy push: capex, NE risks and cuts to crude imports by 2030

State backing (51% govt) supports capex (Rs 2,300 crore FY2024) and PRI; Assam/NorthEast ~60% of 8.4 MMtoe (2024) raises local security risk; foreign exposure ~15–20% of upstream value with ~60% PRI coverage; govt targets cutting crude import from ~85% (2023) to <70% by 2030, pressuring domestic output (OIL crude ~1.4 mt FY2024).

| Metric | 2023/24 |

|---|---|

| Govt equity | ~51% |

| Capex FY2024 | Rs 2,300 cr |

| Production share NE | ~60% |

| Total output | 8.4 MMtoe |

| Crude production | ~1.4 mt |

| Foreign exposure | 15–20% |

| PRI coverage | ~60% |

What is included in the product

Explores how macro-environmental factors uniquely affect Oil India across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis.

A concise PESTLE snapshot of Oil India that distills regulatory, economic, social, technological, environmental, and political risks into a shareable slide-ready format for quick team alignment and strategic planning.

Economic factors

Global Crude Oil Price Volatility

Oil India’s revenue and margins move with Brent crude; Brent averaged about 85 USD/bbl in 2024 and 78 USD/bbl YTD 2025, directly affecting export realizations and INR-denominated cash flow.

OPEC+ cuts and demand shifts drove >20% intra-year Brent swings in 2024, complicating cash-flow forecasting and capex scheduling for field development.

High Brent boosts EBITDA per barrel but prompted India to consider windfall levies in 2024 discussions, while sustained prices below ~55–60 USD/bbl would endanger marginal field economics.

Exchange Rate Fluctuations

A volatile Indian Rupee against the US Dollar materially affects Oil India since crude is priced in USD; a 10% rupee depreciation in 2023 raised rupee-equivalent export revenues while increasing import costs for rigs and compressors, which made up about 18% of capex in FY2024. The company reported forex losses of INR 120 crore in H1 FY2025 linked to currency swings. Consequently, hedging and FX risk management remain central to treasury, using forwards and natural hedges to protect margins.

Inflationary Pressure on Operating Costs

Rising global inflation raised input costs for Oil India, with steel up ~20% and key chemicals up 12–15% in 2024, while specialized oilfield service rates climbed ~10–18%, squeezing margins when average realized crude prices only rose ~8% year-on-year; operating cost inflation contributed to a 2024 opex per BOE increase of ~9%. The company must pursue rigorous cost-optimization, supplier renegotiation, and higher operational efficiency to protect margins in a persistently high-cost environment.

Capital Market Access and Interest Rates

Oil India needs large capital for expansion—FY2024 capex guidance ~INR 10–12 bn and planned investments in refinery/upgrades and new blocks raising needs into FY2025–26.

RBI policy rate at 6.50% (Feb 2025) raises domestic borrowing costs, impacting interest expense and DCF valuations.

Institutional inflows hinge on ESG metrics; 2024 divestment trends in fossil fuels lowered sector PE multiples by ~15% versus energy peers.

- FY2024 capex ~INR 10–12 bn

- RBI repo 6.50% (Feb 2025)

- Sector PE gap ~15% due to ESG sentiment

Natural Gas Demand and Pricing

The economic viability of Oil India’s gas projects hinges on demand from fertilizer, power, and city gas distribution; India’s gas consumption rose to about 201 bcm in 2024, supporting long-term off‑take but pricing remains volatile—domestic NG price averaged roughly $6–8/MMBtu in 2024 with periodic administrative caps—while India’s 2023–24 GDP growth near 7% underpins industrial gas demand, a key revenue driver for the company.

- Gas consumption ~201 bcm (2024)

- Domestic price avg $6–8/MMBtu (2024)

- India GDP ~7% (2023–24) boosting industrial demand

- Fertilizer, power, CGD = major off‑take sectors

Oil-led revenue boosts vs rising costs and ESG discount: margins under pressure

Brent avg $85 (2024), $78 YTD (2025) drives revenue; FY2024 capex ~INR 10–12 bn; RBI repo 6.50% (Feb 2025) raises borrowing costs; India gas demand ~201 bcm (2024) with domestic price $6–8/MMBtu; forex volatility and input inflation (steel +20% in 2024) squeeze margins; sector PE discount ~15% from ESG pressure.

| Metric | Value |

|---|---|

| Brent | $85 (2024), $78 YTD 2025 |

| Capex FY2024 | INR 10–12 bn |

| RBI repo | 6.50% Feb 2025 |

| Gas demand | 201 bcm (2024) |

| Gas price | $6–8/MMBtu (2024) |

| Sector PE gap | ~15% |

Preview the Actual Deliverable

Oil India PESTLE Analysis

The preview shown here is the exact Oil India PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.

The layout, content, and insights visible in this preview are identical to the downloadable file you’ll get immediately after payment—no placeholders, no surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Stay ahead with our targeted PESTLE Analysis of Oil India—uncover how political shifts, economic cycles, and environmental regulations are reshaping operations and value creation; perfect for investors and strategists seeking actionable foresight. Purchase the full report to access detailed risk matrices, growth levers, and ready-to-use slides that accelerate decision-making and strategy development.

Political factors

Government Ownership and Strategic Control

As a Navratna PSU under the Ministry of Petroleum and Natural Gas, Oil India Limited benefits from state backing for capital-heavy projects—reflected in government equity of ~51% and access to subsidized funding—while being exposed to policy shifts; the 2024 national oil strategy prioritized energy security, guiding OIL’s capex of Rs 2,300 crore in FY2024 and influencing mandated dividend payouts (Rs 475 crore declared in FY2023) and overseas diplomatic-linked investments.

Geopolitical Stability in Northeast India

A significant portion of Oil India’s assets are in Assam and the Northeast, where 2024 production contributed roughly 60% of the company’s 8.4 MMtoe output, leaving operations highly sensitive to local political stability and security incidents; disruptions in 2023–24 linked to protests caused production halts of up to 5–7% in some fields. Political movements or civil unrest can delay exploration and threaten pipeline integrity, increasing capex and insurance costs. Maintaining strong relations with Assam and neighbouring state governments is essential to secure permits, rights-of-way and H1 2025 infrastructure projects worth ~INR 3–4 billion.

Energy Security and Import Substitution

The Indian government aims to cut crude import dependence from ~85% in 2023 to below 70% by 2030, pressuring Oil India to raise domestic output—its FY2024 crude oil production was ~1.4 million tonnes. Policies like the Hydrocarbon Exploration and Licensing Policy (HELP) and recent bid rounds enabled Oil India to acquire additional blocks, while Atmanirbhar Bharat incentives push investment in enhanced oil recovery and frontier basins to boost reserves and revenue.

International Diplomatic Relations

Oil India’s overseas portfolio—including stakes in Russia, Africa, and the Middle East—is sensitive to India’s bilateral ties and sanctions; in 2024, ~15–20% of upstream value was tied to these regions, raising exposure to sanctions-related cashflow disruptions.

Geopolitical tensions can impede dividend repatriation and JV operations; e.g., 2023–24 trade frictions delayed payments in some Russian and African projects, impacting cashflow and project timelines.

Political risk insurance and active diplomatic support are essential; Oil India reported covering ~60% of its foreign investments with PRI by 2024 and seeks government facilitation for dispute resolution and repatriation.

- Foreign exposure ~15–20% of upstream value (2024)

- ~60% of foreign investments covered by political risk insurance (2024)

- Sanctions/tensions have caused dividend delays in 2023–24

Subsidy Burden and Pricing Policies

Political control over domestic gas pricing remains pivotal for Oil India; despite market-linked pricing for petroleum, gas prices grew only modestly after 2023 reforms, keeping upstream margins under pressure.

Government rejection of parts of the Kirit Parikh Committee recommendations has limited uplift for legacy-field economics, reducing potential revenue increases for older assets.

Recent ad hoc windfall tax adjustments and royalty hikes—used in 2024–2025 to curb fiscal deficits and tame inflation—have periodically trimmed operator EBITDA by up to mid-single-digit percentage points.

- Market-linked petrol; gas pricing politically constrained

- Kirit Parikh interventions blunt legacy-field profitability

- 2024–25 windfall/royalty moves cut operator EBITDA ~3–7%

State-backed energy push: capex, NE risks and cuts to crude imports by 2030

State backing (51% govt) supports capex (Rs 2,300 crore FY2024) and PRI; Assam/NorthEast ~60% of 8.4 MMtoe (2024) raises local security risk; foreign exposure ~15–20% of upstream value with ~60% PRI coverage; govt targets cutting crude import from ~85% (2023) to <70% by 2030, pressuring domestic output (OIL crude ~1.4 mt FY2024).

| Metric | 2023/24 |

|---|---|

| Govt equity | ~51% |

| Capex FY2024 | Rs 2,300 cr |

| Production share NE | ~60% |

| Total output | 8.4 MMtoe |

| Crude production | ~1.4 mt |

| Foreign exposure | 15–20% |

| PRI coverage | ~60% |

What is included in the product

Explores how macro-environmental factors uniquely affect Oil India across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis.

A concise PESTLE snapshot of Oil India that distills regulatory, economic, social, technological, environmental, and political risks into a shareable slide-ready format for quick team alignment and strategic planning.

Economic factors

Global Crude Oil Price Volatility

Oil India’s revenue and margins move with Brent crude; Brent averaged about 85 USD/bbl in 2024 and 78 USD/bbl YTD 2025, directly affecting export realizations and INR-denominated cash flow.

OPEC+ cuts and demand shifts drove >20% intra-year Brent swings in 2024, complicating cash-flow forecasting and capex scheduling for field development.

High Brent boosts EBITDA per barrel but prompted India to consider windfall levies in 2024 discussions, while sustained prices below ~55–60 USD/bbl would endanger marginal field economics.

Exchange Rate Fluctuations

A volatile Indian Rupee against the US Dollar materially affects Oil India since crude is priced in USD; a 10% rupee depreciation in 2023 raised rupee-equivalent export revenues while increasing import costs for rigs and compressors, which made up about 18% of capex in FY2024. The company reported forex losses of INR 120 crore in H1 FY2025 linked to currency swings. Consequently, hedging and FX risk management remain central to treasury, using forwards and natural hedges to protect margins.

Inflationary Pressure on Operating Costs

Rising global inflation raised input costs for Oil India, with steel up ~20% and key chemicals up 12–15% in 2024, while specialized oilfield service rates climbed ~10–18%, squeezing margins when average realized crude prices only rose ~8% year-on-year; operating cost inflation contributed to a 2024 opex per BOE increase of ~9%. The company must pursue rigorous cost-optimization, supplier renegotiation, and higher operational efficiency to protect margins in a persistently high-cost environment.

Capital Market Access and Interest Rates

Oil India needs large capital for expansion—FY2024 capex guidance ~INR 10–12 bn and planned investments in refinery/upgrades and new blocks raising needs into FY2025–26.

RBI policy rate at 6.50% (Feb 2025) raises domestic borrowing costs, impacting interest expense and DCF valuations.

Institutional inflows hinge on ESG metrics; 2024 divestment trends in fossil fuels lowered sector PE multiples by ~15% versus energy peers.

- FY2024 capex ~INR 10–12 bn

- RBI repo 6.50% (Feb 2025)

- Sector PE gap ~15% due to ESG sentiment

Natural Gas Demand and Pricing

The economic viability of Oil India’s gas projects hinges on demand from fertilizer, power, and city gas distribution; India’s gas consumption rose to about 201 bcm in 2024, supporting long-term off‑take but pricing remains volatile—domestic NG price averaged roughly $6–8/MMBtu in 2024 with periodic administrative caps—while India’s 2023–24 GDP growth near 7% underpins industrial gas demand, a key revenue driver for the company.

- Gas consumption ~201 bcm (2024)

- Domestic price avg $6–8/MMBtu (2024)

- India GDP ~7% (2023–24) boosting industrial demand

- Fertilizer, power, CGD = major off‑take sectors

Oil-led revenue boosts vs rising costs and ESG discount: margins under pressure

Brent avg $85 (2024), $78 YTD (2025) drives revenue; FY2024 capex ~INR 10–12 bn; RBI repo 6.50% (Feb 2025) raises borrowing costs; India gas demand ~201 bcm (2024) with domestic price $6–8/MMBtu; forex volatility and input inflation (steel +20% in 2024) squeeze margins; sector PE discount ~15% from ESG pressure.

| Metric | Value |

|---|---|

| Brent | $85 (2024), $78 YTD 2025 |

| Capex FY2024 | INR 10–12 bn |

| RBI repo | 6.50% Feb 2025 |

| Gas demand | 201 bcm (2024) |

| Gas price | $6–8/MMBtu (2024) |

| Sector PE gap | ~15% |

Preview the Actual Deliverable

Oil India PESTLE Analysis

The preview shown here is the exact Oil India PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.

The layout, content, and insights visible in this preview are identical to the downloadable file you’ll get immediately after payment—no placeholders, no surprises.