Oil States International PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

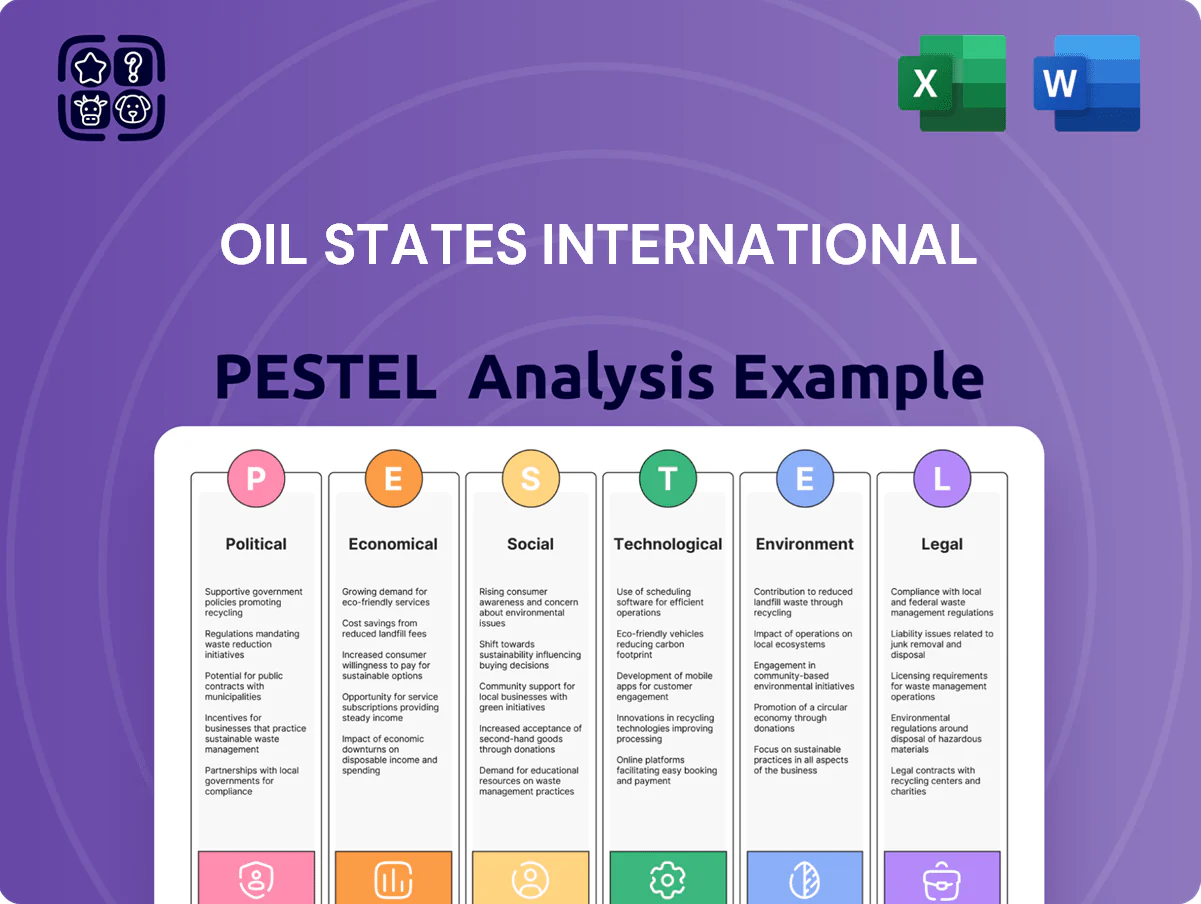

Unlock strategic clarity with our PESTLE Analysis of Oil States International—concise insights into political, economic, social, technological, legal, and environmental forces shaping its future; ideal for investors and strategists seeking actionable intelligence. Purchase the full report to access detailed risk assessments, opportunities, and ready-to-use charts for immediate decision-making.

Political factors

Geopolitical instability and energy security

Geopolitical conflicts and shifting alliances have pushed energy security to the forefront for Western nations; 2024 US domestic oil production averaged 12.2 million bpd, fueling policies to reduce reliance on adversarial exporters.

Oil States International stands to gain from incentives for domestic energy supply chains—US IRA/CHIPS-style energy provisions and increased capital expenditure in 2024 (US upstream capex rose ~8% YoY) favor service providers.

This political climate underpins multiyear investments in offshore and onshore infrastructure in stable jurisdictions, supporting backlog stability and higher-margin project opportunities for the company through 2025.

Trade policies and tariff structures

Changes in international trade agreements and tariffs on steel and specialized components have raised Oil States International's input costs, with global steel tariffs averaging 15-25% in 2025 and sector-specific duties adding up to $200–$800 per ton on tubular goods.

By late 2025 protectionist measures in Brazil, India and the US increased lead times by 20–30%, forcing higher inventory and logistics spend to protect margins.

Analysts note these shifts affect equipment pricing: offshore drilling unit contract bids rose ~8–12% year-over-year in 2025, directly pressuring order profitability.

Government incentives for energy transition

Political backing for renewables and carbon reduction creates both headwinds and openings for Oil States International; US federal spending under the Inflation Reduction Act reached roughly $369 billion through 2031 for clean energy, boosting demand for offshore-wind and CCS equipment.

Permitting and regulatory environment for drilling

Federal and state permitting policies for public-land and offshore drilling directly affect demand for well-site services; for example, US DOI issued roughly 1,800 permits for onshore drilling in 2024 versus 2,100 in 2023, tightening activity in key basins.

Political shifts alter rig counts and completions—Baker Hughes US rig count averaged 600 in 2024 vs 720 in 2022—impacting Downhole Technologies revenue linked to active rigs and completions.

Monitoring evolving regulations, including methane rules and lease auction cadence, is essential to forecast regional service demand and allocate capital and crews effectively.

- DOI onshore permits: ~1,800 (2024)

- Baker Hughes US rig count: ~600 avg (2024)

- Downhole demand tied to rig/completion trends and methane/lease policy changes

Military and defense spending priorities

As a supplier to the military, Oil States International is sensitive to U.S. defense budget shifts; the FY2025 defense topline of about $858 billion and a projected 3% annual growth into 2026 boosts procurement opportunities for its specialized manufacturing.

Rising geopolitical tensions and a 7% increase in global defense spending in 2024 benefit firms with diversified capabilities, while defense contracts help offset volatility from a 2024 oil & gas capex decline of ~12%.

- FY2025 US defense budget ~$858B supports procurement

- Global defense spending +7% in 2024 increases demand

- Defense contracts hedge ~12% decline in 2024 oil & gas capex

Energy & Defense Drive US Onshore/Offshore Investment Amid Costs, Tariffs, Clean-Energy Boom

Geopolitical tensions and US energy security policies (US oil ~12.2M bpd in 2024) boost onshore/offshore investment; 2024 US rig count ~600 and DOI permits ~1,800 tighten activity while IRA clean-energy funding (~$369B through 2031) creates new markets; global defense spend +7% (2024) and FY2025 US defense ~$858B diversify revenue but tariffs/lead-time increases (steel tariffs 15–25%) raise input costs.

| Metric | Value |

|---|---|

| US oil prod (2024) | 12.2M bpd |

| US rig count (2024 avg) | ~600 |

| DOI permits (2024) | ~1,800 |

| IRA clean energy | $369B (thru 2031) |

| FY2025 US defense | $858B |

| Global defense spend (2024) | +7% |

| Steel tariffs | 15–25% |

What is included in the product

Explores how macro-environmental factors uniquely affect Oil States International across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform executives, investors, and strategists.

A concise PESTLE snapshot of Oil States International that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to streamline external risk discussions and strategic planning.

Economic factors

Volatility in global hydrocarbon prices

Demand for Oil States' services tracks E&P capex; global oil averaged about 77 USD/bbl in 2024 and Brent rose ~12% Y/Y, supporting higher offshore spend—US rig count fell to ~480 in 2024 vs 678 in 2019, but rose to ~510 by Jan 2025 as prices recovered, lifting completion-tool utilization and dayrates for deepwater assets.

Interest rate environment and cost of capital

High interest rates sustained through 2025—US Fed funds peak ~5.25–5.50% in 2023–24 with markets pricing terminal rates near 5% into 2025—raised weighted average cost of capital for energy projects by several hundred basis points, increasing project financing costs and capex hurdles.

Clients therefore demand more efficient, lower-cost solutions from service providers like Oil States, pressuring margins and accelerating demand for modular, high-margin offerings.

Oil States’ own net debt (~$210m at end-2024, pro forma) and interest expense rise with tighter monetary policy, constraining R&D spending and capital allocation until rates ease or refinancing occurs.

Labor market constraints and wage inflation

The energy sector faces a competitive labor market with a 2024 U.S. oilfield services vacancy rate near 9%, driven by shortages of skilled technicians and engineers; Oil States International reports rising labor costs that contributed to a 6–8% increase in operating expenses in recent quarters. Investments in specialized training and certification programs, often costing thousands per employee, compress margins across completions, rentals and manufacturing segments. Retention pressures—turnover rates above 20% in some regions—force higher payroll and incentive spend to maintain service quality.

Emerging market demand for energy infrastructure

Economic growth in developing regions—Asia, Africa, Latin America—drives rising demand for reliable energy and infrastructure; IMF projects EM growth ~4.1% in 2025, sustaining offshore investment.

Oil States targets international markets where offshore exploration is expanding, leveraging its subsea and well-construction services to capture projects tied to regional energy development.

Revenue diversification from EMs can offset North American cyclicality; international backlog exposure grew toward ~25% of order book in 2024 for comparable service providers.

- IMF EM growth ~4.1% (2025 forecast)

- Offshore expansion increasing international project mix

- ~25% order book exposure to international markets (2024 benchmark)

Supply chain resilience and material costs

Inflationary pressures raised high-grade steel and specialized polymer costs by ~18% YoY in 2024, lifting Oil States International manufacturing input costs and compressing gross margins.

Strategic sourcing, longer-term supplier contracts and indexed pricing have been adopted to hedge commodity volatility after 2023–24 steel price swings of ±15%.

Global supply-chain stability—notably timely delivery of offshore components from Gulf and Asia—remains critical as 2024 lead times averaged 22 weeks, risking project delays.

- 2024 steel/polymer +18% YoY

- Steel volatility ±15% (2023–24)

- Average lead time 22 weeks (2024)

Oil steady at $77/bbl, rigs ~510, Oil States debt $210M as Fed funds ~5%

Oil prices averaged ~$77/bbl in 2024; Brent +12% Y/Y; US rig count ~510 by Jan‑2025; Oil States net debt ~$210m (end‑2024); Fed funds ~5% into 2025; EM growth ~4.1% (IMF 2025); 2024 steel/polymer +18% YoY; avg lead time 22 weeks; labor vacancy ~9%, turnover >20%.

| Metric | 2024/2025 |

|---|---|

| Oil price | $77/bbl |

| Rig count | ~510 (Jan‑2025) |

| Net debt | $210m |

| Fed funds | ~5% |

| EM growth | 4.1% |

Preview Before You Purchase

Oil States International PESTLE Analysis

The preview shown here is the exact Oil States International PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use without substitutions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE Analysis of Oil States International—concise insights into political, economic, social, technological, legal, and environmental forces shaping its future; ideal for investors and strategists seeking actionable intelligence. Purchase the full report to access detailed risk assessments, opportunities, and ready-to-use charts for immediate decision-making.

Political factors

Geopolitical instability and energy security

Geopolitical conflicts and shifting alliances have pushed energy security to the forefront for Western nations; 2024 US domestic oil production averaged 12.2 million bpd, fueling policies to reduce reliance on adversarial exporters.

Oil States International stands to gain from incentives for domestic energy supply chains—US IRA/CHIPS-style energy provisions and increased capital expenditure in 2024 (US upstream capex rose ~8% YoY) favor service providers.

This political climate underpins multiyear investments in offshore and onshore infrastructure in stable jurisdictions, supporting backlog stability and higher-margin project opportunities for the company through 2025.

Trade policies and tariff structures

Changes in international trade agreements and tariffs on steel and specialized components have raised Oil States International's input costs, with global steel tariffs averaging 15-25% in 2025 and sector-specific duties adding up to $200–$800 per ton on tubular goods.

By late 2025 protectionist measures in Brazil, India and the US increased lead times by 20–30%, forcing higher inventory and logistics spend to protect margins.

Analysts note these shifts affect equipment pricing: offshore drilling unit contract bids rose ~8–12% year-over-year in 2025, directly pressuring order profitability.

Government incentives for energy transition

Political backing for renewables and carbon reduction creates both headwinds and openings for Oil States International; US federal spending under the Inflation Reduction Act reached roughly $369 billion through 2031 for clean energy, boosting demand for offshore-wind and CCS equipment.

Permitting and regulatory environment for drilling

Federal and state permitting policies for public-land and offshore drilling directly affect demand for well-site services; for example, US DOI issued roughly 1,800 permits for onshore drilling in 2024 versus 2,100 in 2023, tightening activity in key basins.

Political shifts alter rig counts and completions—Baker Hughes US rig count averaged 600 in 2024 vs 720 in 2022—impacting Downhole Technologies revenue linked to active rigs and completions.

Monitoring evolving regulations, including methane rules and lease auction cadence, is essential to forecast regional service demand and allocate capital and crews effectively.

- DOI onshore permits: ~1,800 (2024)

- Baker Hughes US rig count: ~600 avg (2024)

- Downhole demand tied to rig/completion trends and methane/lease policy changes

Military and defense spending priorities

As a supplier to the military, Oil States International is sensitive to U.S. defense budget shifts; the FY2025 defense topline of about $858 billion and a projected 3% annual growth into 2026 boosts procurement opportunities for its specialized manufacturing.

Rising geopolitical tensions and a 7% increase in global defense spending in 2024 benefit firms with diversified capabilities, while defense contracts help offset volatility from a 2024 oil & gas capex decline of ~12%.

- FY2025 US defense budget ~$858B supports procurement

- Global defense spending +7% in 2024 increases demand

- Defense contracts hedge ~12% decline in 2024 oil & gas capex

Energy & Defense Drive US Onshore/Offshore Investment Amid Costs, Tariffs, Clean-Energy Boom

Geopolitical tensions and US energy security policies (US oil ~12.2M bpd in 2024) boost onshore/offshore investment; 2024 US rig count ~600 and DOI permits ~1,800 tighten activity while IRA clean-energy funding (~$369B through 2031) creates new markets; global defense spend +7% (2024) and FY2025 US defense ~$858B diversify revenue but tariffs/lead-time increases (steel tariffs 15–25%) raise input costs.

| Metric | Value |

|---|---|

| US oil prod (2024) | 12.2M bpd |

| US rig count (2024 avg) | ~600 |

| DOI permits (2024) | ~1,800 |

| IRA clean energy | $369B (thru 2031) |

| FY2025 US defense | $858B |

| Global defense spend (2024) | +7% |

| Steel tariffs | 15–25% |

What is included in the product

Explores how macro-environmental factors uniquely affect Oil States International across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform executives, investors, and strategists.

A concise PESTLE snapshot of Oil States International that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to streamline external risk discussions and strategic planning.

Economic factors

Volatility in global hydrocarbon prices

Demand for Oil States' services tracks E&P capex; global oil averaged about 77 USD/bbl in 2024 and Brent rose ~12% Y/Y, supporting higher offshore spend—US rig count fell to ~480 in 2024 vs 678 in 2019, but rose to ~510 by Jan 2025 as prices recovered, lifting completion-tool utilization and dayrates for deepwater assets.

Interest rate environment and cost of capital

High interest rates sustained through 2025—US Fed funds peak ~5.25–5.50% in 2023–24 with markets pricing terminal rates near 5% into 2025—raised weighted average cost of capital for energy projects by several hundred basis points, increasing project financing costs and capex hurdles.

Clients therefore demand more efficient, lower-cost solutions from service providers like Oil States, pressuring margins and accelerating demand for modular, high-margin offerings.

Oil States’ own net debt (~$210m at end-2024, pro forma) and interest expense rise with tighter monetary policy, constraining R&D spending and capital allocation until rates ease or refinancing occurs.

Labor market constraints and wage inflation

The energy sector faces a competitive labor market with a 2024 U.S. oilfield services vacancy rate near 9%, driven by shortages of skilled technicians and engineers; Oil States International reports rising labor costs that contributed to a 6–8% increase in operating expenses in recent quarters. Investments in specialized training and certification programs, often costing thousands per employee, compress margins across completions, rentals and manufacturing segments. Retention pressures—turnover rates above 20% in some regions—force higher payroll and incentive spend to maintain service quality.

Emerging market demand for energy infrastructure

Economic growth in developing regions—Asia, Africa, Latin America—drives rising demand for reliable energy and infrastructure; IMF projects EM growth ~4.1% in 2025, sustaining offshore investment.

Oil States targets international markets where offshore exploration is expanding, leveraging its subsea and well-construction services to capture projects tied to regional energy development.

Revenue diversification from EMs can offset North American cyclicality; international backlog exposure grew toward ~25% of order book in 2024 for comparable service providers.

- IMF EM growth ~4.1% (2025 forecast)

- Offshore expansion increasing international project mix

- ~25% order book exposure to international markets (2024 benchmark)

Supply chain resilience and material costs

Inflationary pressures raised high-grade steel and specialized polymer costs by ~18% YoY in 2024, lifting Oil States International manufacturing input costs and compressing gross margins.

Strategic sourcing, longer-term supplier contracts and indexed pricing have been adopted to hedge commodity volatility after 2023–24 steel price swings of ±15%.

Global supply-chain stability—notably timely delivery of offshore components from Gulf and Asia—remains critical as 2024 lead times averaged 22 weeks, risking project delays.

- 2024 steel/polymer +18% YoY

- Steel volatility ±15% (2023–24)

- Average lead time 22 weeks (2024)

Oil steady at $77/bbl, rigs ~510, Oil States debt $210M as Fed funds ~5%

Oil prices averaged ~$77/bbl in 2024; Brent +12% Y/Y; US rig count ~510 by Jan‑2025; Oil States net debt ~$210m (end‑2024); Fed funds ~5% into 2025; EM growth ~4.1% (IMF 2025); 2024 steel/polymer +18% YoY; avg lead time 22 weeks; labor vacancy ~9%, turnover >20%.

| Metric | 2024/2025 |

|---|---|

| Oil price | $77/bbl |

| Rig count | ~510 (Jan‑2025) |

| Net debt | $210m |

| Fed funds | ~5% |

| EM growth | 4.1% |

Preview Before You Purchase

Oil States International PESTLE Analysis

The preview shown here is the exact Oil States International PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use without substitutions.