Olam Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

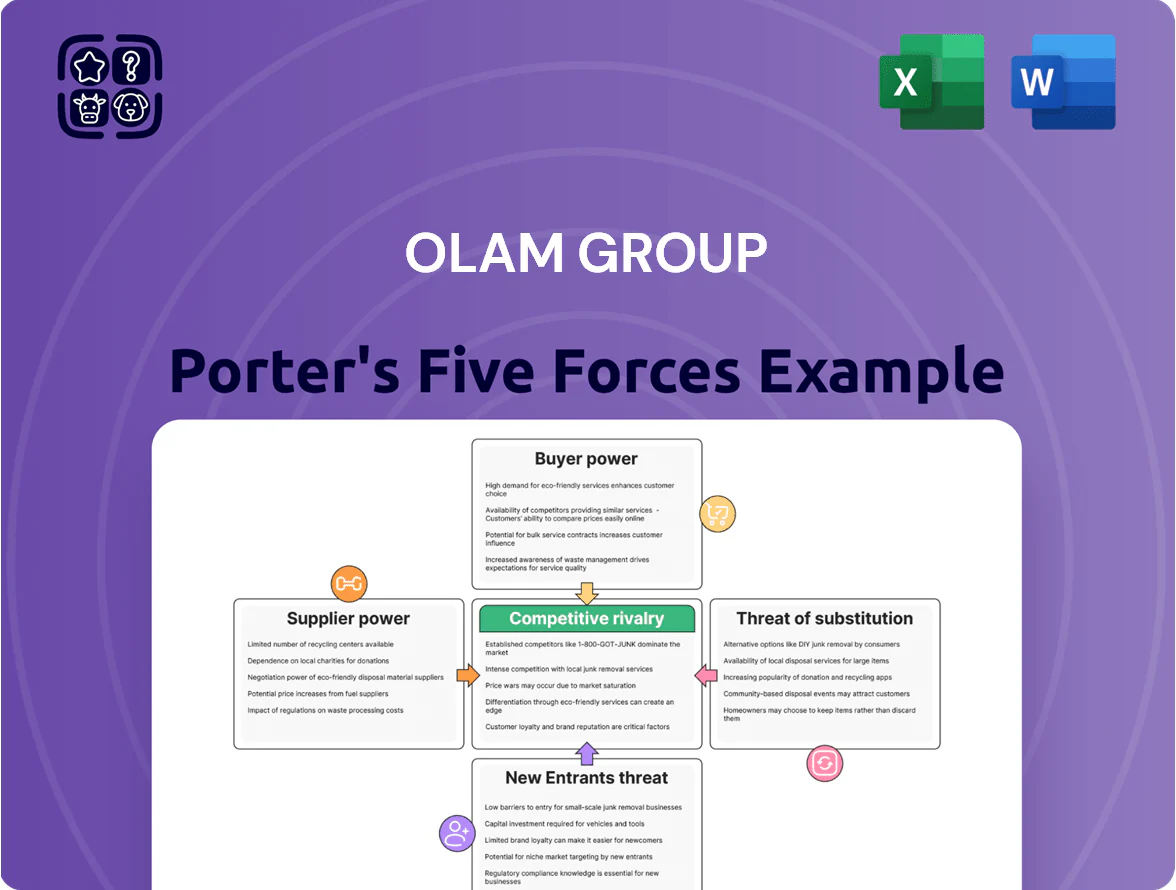

Olam Group operates in a complex agro-commodities landscape where supplier fragmentation, volatile commodity prices, and growing buyer consolidation shape strategic choices; regulatory shifts and sustainability demands add external pressure while substitution risks remain moderate.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Olam Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmentation of smallholder farmer networks

Olam sources a large share of raw materials from millions of smallholder farmers across Africa, Asia and Latin America, so individual suppliers have limited bargaining power and cannot sway prices or volumes. Olam exploits this fragmentation by offering seeds, agrochemicals and $500m+ in farmer financing (2024 figure) to lock in loyalty and steady supply. By 2025 Olam expanded direct sourcing programs, cutting out many traders and raising direct-buy volumes—reducing procurement costs and middlemen margins.

Impact of climate change on crop availability

By late 2025, a 35% rise in extreme weather events vs. 2000–2010 has caused localized scarcities in cocoa and coffee, temporarily boosting supplier leverage in unaffected regions.

Olam’s diversified footprint limits long-term supplier power, but producers in stable climates have extracted premiums up to 12% when global stocks tighten after droughts or floods.

Olam counters via $420m invested in climate-smart ag since 2020 and by growing its plantation assets to improve vertical integration and reduce spot-market exposure.

Strategic backward integration and asset ownership

Olam’s ownership of almond orchards and dairy farms cuts supplier power by locking in cost and quality control; Olam Food Ingredients and Olam Agri aimed to cover ~35%–40% of raw-input needs internally by end-2025, reducing exposure to external price spikes.

Regulatory influence and government intervention

Regulatory bodies and marketing boards in origin countries act as centralized suppliers, setting minimum prices and export quotas—notably in cocoa and cotton—raising Olam’s supplier bargaining pressure.

By 2025 sovereign rules to keep more value locally (e.g., Ghana/Ivory Coast cocoa premium talks, Nigeria cotton export controls) increase compliance costs and constrain margins; Olam offsets this via local partnerships and in-country processing investments.

- State-level price controls: common in West African cocoa markets

- Export quotas raise procurement risk and working capital needs

- 2025: higher local processing mandates drive CAPEX and Olam risk exposure

Digitalization of procurement through Olam Direct

- 1.2M+ tonnes transacted via Olam Direct in 2025

- 8–12% estimated procurement price volatility reduction

- Direct farm-gate connections lower aggregator influence

- Real-time pricing increases transparency and control

Olam cuts supplier power with scale & integration but pays ~12% climate-driven premiums

Olam’s supplier power is low due to millions of fragmented smallholders, direct-sourcing scale (1.2M+ tonnes via Olam Direct in 2025) and vertical integration (35–40% internal sourcing target end-2025), but climate-driven local scarcities and state price controls can raise premiums (~12%) and compliance costs; Olam offsets via $420m climate investment since 2020 and $500m+ farmer finance (2024).

| Metric | Value |

|---|---|

| Olam Direct volume (2025) | 1.2M+ tonnes |

| Internal sourcing target (end-2025) | 35–40% |

| Farmer finance (2024) | $500m+ |

| Climate investment (since 2020) | $420m |

| Supplier premium in tight supply | ~12% |

What is included in the product

Tailored Porter's Five Forces assessment for Olam Group that uncovers competitive pressures, supplier and buyer influence on pricing, entry barriers protecting incumbents, threats from substitutes and disruptors, and strategic implications for profitability and market positioning.

Compact Porter’s Five Forces summary tailored for Olam Group—quickly visualize supplier/buyer power, competitive rivalry, threats of entry/substitution to guide risk mitigation and strategic sourcing.

Customers Bargaining Power

Concentration of global food and beverage manufacturers

Olam primarily serves large multinationals with strong buying power, enabling them to demand lower prices and consolidate orders for volume discounts; top 10 global food firms accounted for ~28% of industry procurement by 2024.

These buyers can shift to rivals like Cargill or ADM, increasing price pressure; M&A and private-label growth raised buyer concentration by 2025.

Olam defends margin by supplying specialized, hard-to-replace ingredients and services—value-added sales made up ~35% of Olam's FY2024 revenue—forcing buyers to weigh switching costs.

Heightened demand for sustainability and traceability

Customers in 2025 weigh ESG and traceability heavily: 72% of global retailers report ESG criteria as decisive (Kantar 2024), pushing suppliers to meet strict standards. Large brands force compliance, raising Olam’s operating costs but favoring suppliers with traceability. Olam’s AtSource platform tracked 1.2m farmers and 4.5m tonnes of produce in 2024, letting Olam sell services and shift toward strategic partnerships, easing some downward price pressure.

Price sensitivity in the commodity trading segment

In Olam Agri’s commodity segment, staples like grains and edible oils are undifferentiated, so price drives buying; customers prioritize cost over brand, leading to high bargaining power.

Low switching costs let buyers shift to cheaper suppliers quickly, forcing Olam to push for extreme operational efficiency to protect margins.

By end-2025, heightened market volatility raised price sensitivity: global agricultural price volatility index rose ~28% in 2024–25, making buyers more reactive to short-term supply shifts.

Customization and co-creation of food ingredients

Olam Food Ingredients (OFI) shifted to a solutions model, co-creating bespoke flavors and ingredient systems that embed OFI into clients’ R&D and recipes, raising switching costs and lowering buyer bargaining power.

When OFI is integral to a unique product, relationships become collaborative, cutting price-driven churn; OFI reported 2024 branded and solutions revenue growth of ~12%, insulating part of sales from raw-price sensitivity.

Availability of market data and price transparency

The democratization of market intelligence by 2025 lets buyers track global commodity prices and supply in real time, eroding Olam Group’s ability to use information asymmetry to raise margins on standard products.

With public harvest data and logistics cost indices (eg. 2024 freight rate volatility ±35%), customers negotiate from strength, forcing Olam to compete on execution, risk management, and value-added services rather than price alone.

- Real-time price feeds reduce margin premiums

- Buyers use harvest/logistics data in contracts

- Olam must sell superior logistics and risk tools

- Value-add services justify premium vs commoditized supply

Buyers dominate procurement (~28%), but Olam's AtSource & OFI lift switching costs, protect margins

Buyers hold high power: top 10 food firms drove ~28% of procurement in 2024, low switching costs and real-time price feeds boost pressure, but Olam’s value-added sales (~35% FY2024) and AtSource traceability (1.2m farmers, 4.5m t tracked in 2024) plus OFI solutions (12% growth 2024) raise switching costs and partly insulate margins.

| Metric | Value |

|---|---|

| Top-10 buyer share (2024) | ~28% |

| Value-added revenue (FY2024) | ~35% |

| AtSource farmers (2024) | 1.2m |

| AtSource tonnes (2024) | 4.5m |

| OFI solutions growth (2024) | 12% |

Preview Before You Purchase

Olam Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Olam Group you'll receive immediately after purchase—no surprises, no placeholders. The document outlines supplier and buyer power, competitive rivalry, threat of substitutes, and barriers to entry with data-driven insights and strategic implications. It's fully formatted and ready for download and use the moment you buy. You're viewing the final deliverable.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Olam Group operates in a complex agro-commodities landscape where supplier fragmentation, volatile commodity prices, and growing buyer consolidation shape strategic choices; regulatory shifts and sustainability demands add external pressure while substitution risks remain moderate.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Olam Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmentation of smallholder farmer networks

Olam sources a large share of raw materials from millions of smallholder farmers across Africa, Asia and Latin America, so individual suppliers have limited bargaining power and cannot sway prices or volumes. Olam exploits this fragmentation by offering seeds, agrochemicals and $500m+ in farmer financing (2024 figure) to lock in loyalty and steady supply. By 2025 Olam expanded direct sourcing programs, cutting out many traders and raising direct-buy volumes—reducing procurement costs and middlemen margins.

Impact of climate change on crop availability

By late 2025, a 35% rise in extreme weather events vs. 2000–2010 has caused localized scarcities in cocoa and coffee, temporarily boosting supplier leverage in unaffected regions.

Olam’s diversified footprint limits long-term supplier power, but producers in stable climates have extracted premiums up to 12% when global stocks tighten after droughts or floods.

Olam counters via $420m invested in climate-smart ag since 2020 and by growing its plantation assets to improve vertical integration and reduce spot-market exposure.

Strategic backward integration and asset ownership

Olam’s ownership of almond orchards and dairy farms cuts supplier power by locking in cost and quality control; Olam Food Ingredients and Olam Agri aimed to cover ~35%–40% of raw-input needs internally by end-2025, reducing exposure to external price spikes.

Regulatory influence and government intervention

Regulatory bodies and marketing boards in origin countries act as centralized suppliers, setting minimum prices and export quotas—notably in cocoa and cotton—raising Olam’s supplier bargaining pressure.

By 2025 sovereign rules to keep more value locally (e.g., Ghana/Ivory Coast cocoa premium talks, Nigeria cotton export controls) increase compliance costs and constrain margins; Olam offsets this via local partnerships and in-country processing investments.

- State-level price controls: common in West African cocoa markets

- Export quotas raise procurement risk and working capital needs

- 2025: higher local processing mandates drive CAPEX and Olam risk exposure

Digitalization of procurement through Olam Direct

- 1.2M+ tonnes transacted via Olam Direct in 2025

- 8–12% estimated procurement price volatility reduction

- Direct farm-gate connections lower aggregator influence

- Real-time pricing increases transparency and control

Olam cuts supplier power with scale & integration but pays ~12% climate-driven premiums

Olam’s supplier power is low due to millions of fragmented smallholders, direct-sourcing scale (1.2M+ tonnes via Olam Direct in 2025) and vertical integration (35–40% internal sourcing target end-2025), but climate-driven local scarcities and state price controls can raise premiums (~12%) and compliance costs; Olam offsets via $420m climate investment since 2020 and $500m+ farmer finance (2024).

| Metric | Value |

|---|---|

| Olam Direct volume (2025) | 1.2M+ tonnes |

| Internal sourcing target (end-2025) | 35–40% |

| Farmer finance (2024) | $500m+ |

| Climate investment (since 2020) | $420m |

| Supplier premium in tight supply | ~12% |

What is included in the product

Tailored Porter's Five Forces assessment for Olam Group that uncovers competitive pressures, supplier and buyer influence on pricing, entry barriers protecting incumbents, threats from substitutes and disruptors, and strategic implications for profitability and market positioning.

Compact Porter’s Five Forces summary tailored for Olam Group—quickly visualize supplier/buyer power, competitive rivalry, threats of entry/substitution to guide risk mitigation and strategic sourcing.

Customers Bargaining Power

Concentration of global food and beverage manufacturers

Olam primarily serves large multinationals with strong buying power, enabling them to demand lower prices and consolidate orders for volume discounts; top 10 global food firms accounted for ~28% of industry procurement by 2024.

These buyers can shift to rivals like Cargill or ADM, increasing price pressure; M&A and private-label growth raised buyer concentration by 2025.

Olam defends margin by supplying specialized, hard-to-replace ingredients and services—value-added sales made up ~35% of Olam's FY2024 revenue—forcing buyers to weigh switching costs.

Heightened demand for sustainability and traceability

Customers in 2025 weigh ESG and traceability heavily: 72% of global retailers report ESG criteria as decisive (Kantar 2024), pushing suppliers to meet strict standards. Large brands force compliance, raising Olam’s operating costs but favoring suppliers with traceability. Olam’s AtSource platform tracked 1.2m farmers and 4.5m tonnes of produce in 2024, letting Olam sell services and shift toward strategic partnerships, easing some downward price pressure.

Price sensitivity in the commodity trading segment

In Olam Agri’s commodity segment, staples like grains and edible oils are undifferentiated, so price drives buying; customers prioritize cost over brand, leading to high bargaining power.

Low switching costs let buyers shift to cheaper suppliers quickly, forcing Olam to push for extreme operational efficiency to protect margins.

By end-2025, heightened market volatility raised price sensitivity: global agricultural price volatility index rose ~28% in 2024–25, making buyers more reactive to short-term supply shifts.

Customization and co-creation of food ingredients

Olam Food Ingredients (OFI) shifted to a solutions model, co-creating bespoke flavors and ingredient systems that embed OFI into clients’ R&D and recipes, raising switching costs and lowering buyer bargaining power.

When OFI is integral to a unique product, relationships become collaborative, cutting price-driven churn; OFI reported 2024 branded and solutions revenue growth of ~12%, insulating part of sales from raw-price sensitivity.

Availability of market data and price transparency

The democratization of market intelligence by 2025 lets buyers track global commodity prices and supply in real time, eroding Olam Group’s ability to use information asymmetry to raise margins on standard products.

With public harvest data and logistics cost indices (eg. 2024 freight rate volatility ±35%), customers negotiate from strength, forcing Olam to compete on execution, risk management, and value-added services rather than price alone.

- Real-time price feeds reduce margin premiums

- Buyers use harvest/logistics data in contracts

- Olam must sell superior logistics and risk tools

- Value-add services justify premium vs commoditized supply

Buyers dominate procurement (~28%), but Olam's AtSource & OFI lift switching costs, protect margins

Buyers hold high power: top 10 food firms drove ~28% of procurement in 2024, low switching costs and real-time price feeds boost pressure, but Olam’s value-added sales (~35% FY2024) and AtSource traceability (1.2m farmers, 4.5m t tracked in 2024) plus OFI solutions (12% growth 2024) raise switching costs and partly insulate margins.

| Metric | Value |

|---|---|

| Top-10 buyer share (2024) | ~28% |

| Value-added revenue (FY2024) | ~35% |

| AtSource farmers (2024) | 1.2m |

| AtSource tonnes (2024) | 4.5m |

| OFI solutions growth (2024) | 12% |

Preview Before You Purchase

Olam Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Olam Group you'll receive immediately after purchase—no surprises, no placeholders. The document outlines supplier and buyer power, competitive rivalry, threat of substitutes, and barriers to entry with data-driven insights and strategic implications. It's fully formatted and ready for download and use the moment you buy. You're viewing the final deliverable.