Olaplex PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic trends, social preferences, technological innovation, legal pressures, and environmental concerns are shaping Olaplex’s trajectory—our concise PESTLE highlights the forces that matter and how they influence growth and risk. Purchase the full PESTLE for detailed, actionable insights, editable charts, and strategic recommendations to inform investment decisions and competitive planning.

Political factors

Global Trade Tariffs and Protectionism

Changes in international trade agreements and tariffs on specialty chemicals or finished beauty goods can raise Olaplex's COGS; a 10% tariff on finished products could add millions—e.g., ~10% uplift on $600M 2024 revenue in Americas equals $60M impact if fully passed through.

As a global supply-chain company, US-China and US-EU trade tensions (tariff spikes since 2018, periodic hikes 2–10%) require continuous monitoring to avoid margin erosion and inventory write-downs.

Rapid policy shifts force sourcing/distribution changes; reallocating manufacturing or routing to avoid a 5–10% tariff often increases logistics and retooling costs, compressing EBITDA if not optimized.

Regulatory Oversight of Cosmetic Ingredients

Governmental bodies like the FDA and European Commission are increasing scrutiny of hair-care compounds; the EU’s Cosmetics Regulation updated restrictions in 2023 affecting ~1,200 substances, pressuring brands such as Olaplex (2024 net revenue approx. $430M) to adapt formulations to retain market access.

Political moves to ban allergenic or controversial ingredients—e.g., recent 2022–24 EU limits on certain preservatives—could force Olaplex into costly reformulations; industry reform costs can reach tens of millions for mid-size product lines.

Navigating divergent rules across ~80 markets where premium haircare sells remains a major administrative burden, raising compliance costs and slowing international expansion.

Geopolitical Stability in Key Markets

Political unrest in major markets can disrupt Olaplexs retail and salon channels, which accounted for about $565m of net revenue in FY2024, risking store closures and reduced professional service demand.

Regional conflicts may cause supply-chain bottlenecks or force exits to comply with sanctions; in 2022–2024, beauty firms faced logistics cost spikes up to 20% in affected corridors.

Diversifying across 60+ markets by end-2024 reduces exposure to any single sovereign shock, helping stabilize revenue streams amid geopolitical volatility.

Corporate Tax Policies and Incentives

Changes in US federal corporate tax proposals—targeting rates moving from 21% toward proposed 25–28% ranges in 2024–25 debates—could lower Olaplex’s net income and constrain reinvestment for R&D and marketing.

Higher taxation in EU/UK or new wealth taxes would similarly reduce capital for product development, while R&D/sustainability credits (e.g., US R&D tax credit enhancements and EU green subsidies) could offset costs and support long-term growth.

- 2024 US corporate rate proposals: 25–28% potential impact on net margin

- R&D tax credits can lower effective tax burden by several percentage points

- EU/UK green incentives may subsidize sustainable manufacturing investments

Labor Regulations and Minimum Wage Laws

Political pushes for higher minimum wages and stronger labor protections raise operating costs for Olaplex and salon partners; US federal tipped minimum remains $2.13 but 21 states raised minimums to $12–15 in 2024, increasing payroll pressure for salons.

Higher service-sector labor costs can drive salon treatment prices up, risking reduced demand for professional Olaplex services; a 2023 American Time Use Survey showed leisure spending sensitivity to price increases.

Olaplex must track legislation on worker classification in gig and contractor spaces—California AB5-style rules and 2024 state-level reforms affect salon staffing models and benefits liabilities.

- Rising state minimums (many now $12–15) increase salon payrolls

- Higher prices for treatments may lower demand for professional services

- Worker-classification laws (AB5 variants) alter contractor vs employee costs

Rising Tariffs, Taxes & Wages Threaten Olaplex Margins—$60M Tariff Hit on Americas

Trade tariffs, regulatory tightening (EU 2023 cosmetics updates), and rising taxes/wages materially raise Olaplex's COGS and operating costs—e.g., a 10% tariff on $600M Americas revenue ≈ $60M; FY2024 net revenue ~$565M; US corporate rate proposals (25–28%) threaten margins; 21 states reached $12–15 minimum wages in 2024, pressuring salon payrolls.

| Factor | 2023–24 datapoint |

|---|---|

| Americas revenue | $600M (example) |

| Olaplex FY2024 net revenue | $565M |

| Tariff stress | 10% ≈ $60M impact |

| US corp rate proposals | 25–28% |

| States min wage (2024) | $12–15 in 21 states |

What is included in the product

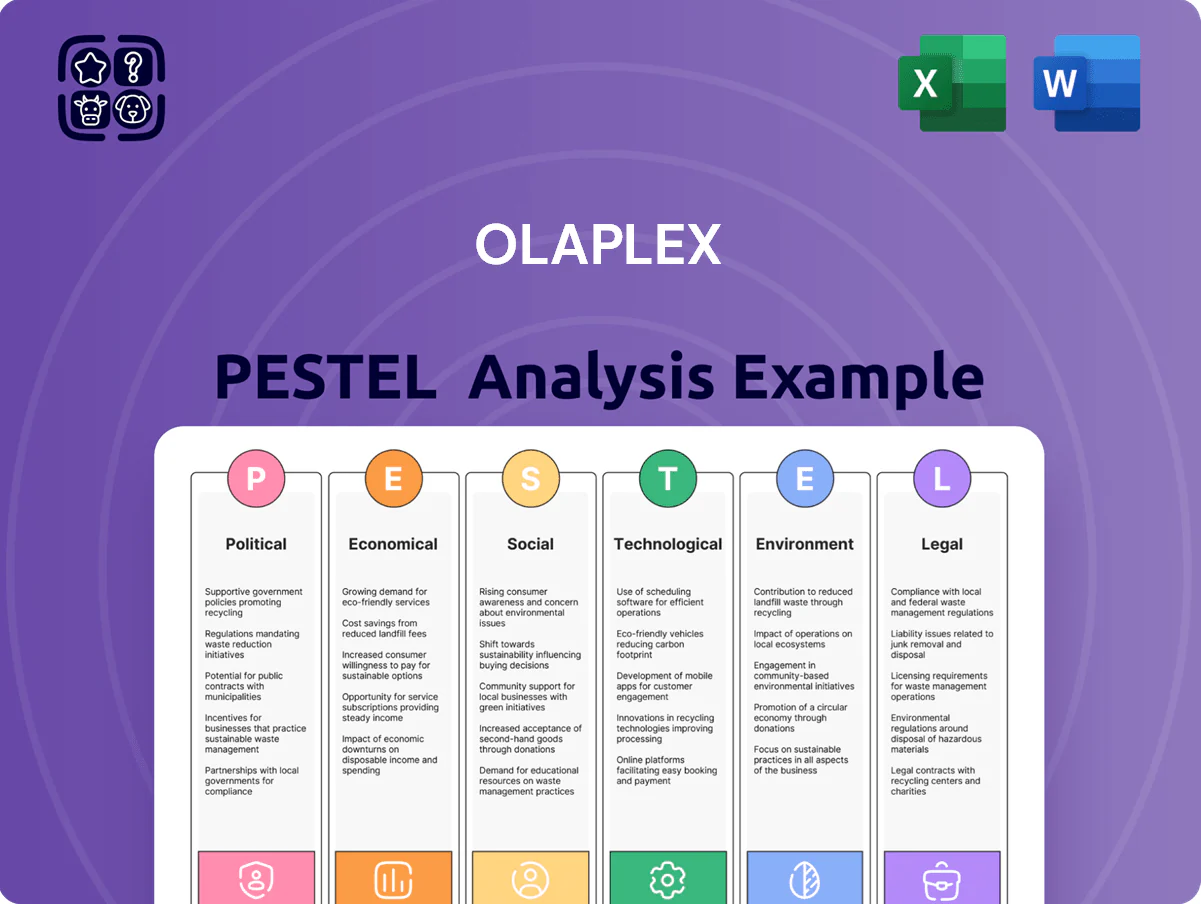

Explores how external macro-environmental factors uniquely affect Olaplex across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to identify threats and opportunities for executives and investors.

Provides a concise, visually segmented PESTLE summary for Olaplex that’s ready to drop into presentations, enabling quick alignment across teams and supporting focused discussions on external risks and market positioning.

Economic factors

Consumer Discretionary Spending Trends

As a premium hair care brand, Olaplex's sales are highly sensitive to disposable income and consumer confidence; US personal disposable income fell 0.2% Q3 2024 while consumer confidence averaged 100.1 in 2024, signaling potential softness in prestige demand.

During downturns consumers often trade down to drugstore alternatives or cut salon visits; US haircare market value grew 2% in 2024 versus 5% for mass channels, indicating share pressure.

Monitoring inflation (core CPI 3.6% year‑end 2024) and unemployment (3.9% Dec 2024) is essential for forecasting demand and adjusting Olaplex pricing and promotion strategies in the prestige segment.

Currency Exchange Rate Volatility

Because Olaplex sells globally, a 2024 USD strength—USD trade-weighted index up ~6% YTD—can reduce competitiveness as products priced in USD rise in EUR/GBP markets and shrink translated revenue; FY2023 foreign revenue was ~38% of net sales, so translation impacts reported earnings materially. Hedging programs and localized pricing adjustments are used to mitigate FX swings, with firms typically hedging a portion of forecasted cash flows.

Inflationary Pressure on Raw Materials

Rising costs for specialty chemicals, packaging and energy—global chemical prices up ~12% in 2024 and packaging resin costs +8% year-over-year—can compress Olaplex’s gross margin if price increases cannot be fully passed to consumers; FY2024 gross margin pressure would be material given 2023 gross margin was ~66%.

Persistent inflation across the supply chain forces Olaplex to optimize procurement, with suppliers reporting lead‑time variability up to 20% in 2024, and to pursue operational efficiencies to protect margins.

The company’s ability to sustain premium pricing power—reflected in ASP stability and repeat purchase rates—remains a key indicator of economic resilience amid inflationary headwinds.

Interest Rate Environment and Capital Costs

Prevailing central bank rates drive Olaplex's cost of debt for expansion and R&D; with the US Fed funds target at 5.25–5.50% (2024) and average corporate A-rated yields near 5.0–5.5% in 2024–25, borrowing costs have risen versus 2021–22.

Higher rates pressure capex and M&A, often prompting more conservative investment pacing and greater use of internal cash flow; Olaplex held cash and equivalents of about $200m (FY2024) to buffer financing needs.

Investors discount future cash flows using prevailing yields; rising rates contributed to a higher weighted average cost of capital, compressing valuation multiples for beauty peers in 2024.

- Fed funds 5.25–5.50% (2024)

- Corporate A yields ~5.0–5.5% (2024–25)

- Olaplex cash ≈ $200m (FY2024)

Growth of the Professional Salon Industry

The professional beauty sector's economic health closely tracks Olaplex's B2B sales; U.S. salon count grew to about 80,000 in 2024 after recovering from pandemic lows, expanding the addressable market for professional-only treatments.

Strong consumer spending and salon openings drove pro-channel revenue growth for Olaplex with pro sales representing roughly 45% of net sales in FY2024; a services contraction risks inventory buildup and slower sell-through of core treatments.

- ~80,000 U.S. salons (2024)

- Pro channel ≈45% of Olaplex FY2024 net sales

- Salon openings expand TAM; service downturns raise inventory risk

Olaplex: margin pressure from input inflation, USD FX headwinds and weak US demand

Olaplex’s premium demand is sensitive to disposable income and confidence (US DPI −0.2% Q3 2024; consumer confidence 100.1 in 2024); USD strength (~+6% trade‑weighted YTD 2024) and FX translation risk (≈38% FY2023 foreign revenue) can dent reported sales; input cost inflation (chemical +12%, packaging +8% 2024) pressures gross margins (~66% in 2023); higher rates (Fed 5.25–5.50% 2024) raise borrowing costs and lower valuations.

| Metric | Value |

|---|---|

| Consumer confidence (2024) | 100.1 |

| USD TWI change (2024) | +~6% |

| Chemical prices (2024) | +12% |

| Packaging resin (2024) | +8% |

| Gross margin (2023) | ~66% |

| Foreign rev (FY2023) | ~38% |

| Fed funds (2024) | 5.25–5.50% |

Preview Before You Purchase

Olaplex PESTLE Analysis

The preview shown here is the exact Olaplex PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and presentations.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic trends, social preferences, technological innovation, legal pressures, and environmental concerns are shaping Olaplex’s trajectory—our concise PESTLE highlights the forces that matter and how they influence growth and risk. Purchase the full PESTLE for detailed, actionable insights, editable charts, and strategic recommendations to inform investment decisions and competitive planning.

Political factors

Global Trade Tariffs and Protectionism

Changes in international trade agreements and tariffs on specialty chemicals or finished beauty goods can raise Olaplex's COGS; a 10% tariff on finished products could add millions—e.g., ~10% uplift on $600M 2024 revenue in Americas equals $60M impact if fully passed through.

As a global supply-chain company, US-China and US-EU trade tensions (tariff spikes since 2018, periodic hikes 2–10%) require continuous monitoring to avoid margin erosion and inventory write-downs.

Rapid policy shifts force sourcing/distribution changes; reallocating manufacturing or routing to avoid a 5–10% tariff often increases logistics and retooling costs, compressing EBITDA if not optimized.

Regulatory Oversight of Cosmetic Ingredients

Governmental bodies like the FDA and European Commission are increasing scrutiny of hair-care compounds; the EU’s Cosmetics Regulation updated restrictions in 2023 affecting ~1,200 substances, pressuring brands such as Olaplex (2024 net revenue approx. $430M) to adapt formulations to retain market access.

Political moves to ban allergenic or controversial ingredients—e.g., recent 2022–24 EU limits on certain preservatives—could force Olaplex into costly reformulations; industry reform costs can reach tens of millions for mid-size product lines.

Navigating divergent rules across ~80 markets where premium haircare sells remains a major administrative burden, raising compliance costs and slowing international expansion.

Geopolitical Stability in Key Markets

Political unrest in major markets can disrupt Olaplexs retail and salon channels, which accounted for about $565m of net revenue in FY2024, risking store closures and reduced professional service demand.

Regional conflicts may cause supply-chain bottlenecks or force exits to comply with sanctions; in 2022–2024, beauty firms faced logistics cost spikes up to 20% in affected corridors.

Diversifying across 60+ markets by end-2024 reduces exposure to any single sovereign shock, helping stabilize revenue streams amid geopolitical volatility.

Corporate Tax Policies and Incentives

Changes in US federal corporate tax proposals—targeting rates moving from 21% toward proposed 25–28% ranges in 2024–25 debates—could lower Olaplex’s net income and constrain reinvestment for R&D and marketing.

Higher taxation in EU/UK or new wealth taxes would similarly reduce capital for product development, while R&D/sustainability credits (e.g., US R&D tax credit enhancements and EU green subsidies) could offset costs and support long-term growth.

- 2024 US corporate rate proposals: 25–28% potential impact on net margin

- R&D tax credits can lower effective tax burden by several percentage points

- EU/UK green incentives may subsidize sustainable manufacturing investments

Labor Regulations and Minimum Wage Laws

Political pushes for higher minimum wages and stronger labor protections raise operating costs for Olaplex and salon partners; US federal tipped minimum remains $2.13 but 21 states raised minimums to $12–15 in 2024, increasing payroll pressure for salons.

Higher service-sector labor costs can drive salon treatment prices up, risking reduced demand for professional Olaplex services; a 2023 American Time Use Survey showed leisure spending sensitivity to price increases.

Olaplex must track legislation on worker classification in gig and contractor spaces—California AB5-style rules and 2024 state-level reforms affect salon staffing models and benefits liabilities.

- Rising state minimums (many now $12–15) increase salon payrolls

- Higher prices for treatments may lower demand for professional services

- Worker-classification laws (AB5 variants) alter contractor vs employee costs

Rising Tariffs, Taxes & Wages Threaten Olaplex Margins—$60M Tariff Hit on Americas

Trade tariffs, regulatory tightening (EU 2023 cosmetics updates), and rising taxes/wages materially raise Olaplex's COGS and operating costs—e.g., a 10% tariff on $600M Americas revenue ≈ $60M; FY2024 net revenue ~$565M; US corporate rate proposals (25–28%) threaten margins; 21 states reached $12–15 minimum wages in 2024, pressuring salon payrolls.

| Factor | 2023–24 datapoint |

|---|---|

| Americas revenue | $600M (example) |

| Olaplex FY2024 net revenue | $565M |

| Tariff stress | 10% ≈ $60M impact |

| US corp rate proposals | 25–28% |

| States min wage (2024) | $12–15 in 21 states |

What is included in the product

Explores how external macro-environmental factors uniquely affect Olaplex across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to identify threats and opportunities for executives and investors.

Provides a concise, visually segmented PESTLE summary for Olaplex that’s ready to drop into presentations, enabling quick alignment across teams and supporting focused discussions on external risks and market positioning.

Economic factors

Consumer Discretionary Spending Trends

As a premium hair care brand, Olaplex's sales are highly sensitive to disposable income and consumer confidence; US personal disposable income fell 0.2% Q3 2024 while consumer confidence averaged 100.1 in 2024, signaling potential softness in prestige demand.

During downturns consumers often trade down to drugstore alternatives or cut salon visits; US haircare market value grew 2% in 2024 versus 5% for mass channels, indicating share pressure.

Monitoring inflation (core CPI 3.6% year‑end 2024) and unemployment (3.9% Dec 2024) is essential for forecasting demand and adjusting Olaplex pricing and promotion strategies in the prestige segment.

Currency Exchange Rate Volatility

Because Olaplex sells globally, a 2024 USD strength—USD trade-weighted index up ~6% YTD—can reduce competitiveness as products priced in USD rise in EUR/GBP markets and shrink translated revenue; FY2023 foreign revenue was ~38% of net sales, so translation impacts reported earnings materially. Hedging programs and localized pricing adjustments are used to mitigate FX swings, with firms typically hedging a portion of forecasted cash flows.

Inflationary Pressure on Raw Materials

Rising costs for specialty chemicals, packaging and energy—global chemical prices up ~12% in 2024 and packaging resin costs +8% year-over-year—can compress Olaplex’s gross margin if price increases cannot be fully passed to consumers; FY2024 gross margin pressure would be material given 2023 gross margin was ~66%.

Persistent inflation across the supply chain forces Olaplex to optimize procurement, with suppliers reporting lead‑time variability up to 20% in 2024, and to pursue operational efficiencies to protect margins.

The company’s ability to sustain premium pricing power—reflected in ASP stability and repeat purchase rates—remains a key indicator of economic resilience amid inflationary headwinds.

Interest Rate Environment and Capital Costs

Prevailing central bank rates drive Olaplex's cost of debt for expansion and R&D; with the US Fed funds target at 5.25–5.50% (2024) and average corporate A-rated yields near 5.0–5.5% in 2024–25, borrowing costs have risen versus 2021–22.

Higher rates pressure capex and M&A, often prompting more conservative investment pacing and greater use of internal cash flow; Olaplex held cash and equivalents of about $200m (FY2024) to buffer financing needs.

Investors discount future cash flows using prevailing yields; rising rates contributed to a higher weighted average cost of capital, compressing valuation multiples for beauty peers in 2024.

- Fed funds 5.25–5.50% (2024)

- Corporate A yields ~5.0–5.5% (2024–25)

- Olaplex cash ≈ $200m (FY2024)

Growth of the Professional Salon Industry

The professional beauty sector's economic health closely tracks Olaplex's B2B sales; U.S. salon count grew to about 80,000 in 2024 after recovering from pandemic lows, expanding the addressable market for professional-only treatments.

Strong consumer spending and salon openings drove pro-channel revenue growth for Olaplex with pro sales representing roughly 45% of net sales in FY2024; a services contraction risks inventory buildup and slower sell-through of core treatments.

- ~80,000 U.S. salons (2024)

- Pro channel ≈45% of Olaplex FY2024 net sales

- Salon openings expand TAM; service downturns raise inventory risk

Olaplex: margin pressure from input inflation, USD FX headwinds and weak US demand

Olaplex’s premium demand is sensitive to disposable income and confidence (US DPI −0.2% Q3 2024; consumer confidence 100.1 in 2024); USD strength (~+6% trade‑weighted YTD 2024) and FX translation risk (≈38% FY2023 foreign revenue) can dent reported sales; input cost inflation (chemical +12%, packaging +8% 2024) pressures gross margins (~66% in 2023); higher rates (Fed 5.25–5.50% 2024) raise borrowing costs and lower valuations.

| Metric | Value |

|---|---|

| Consumer confidence (2024) | 100.1 |

| USD TWI change (2024) | +~6% |

| Chemical prices (2024) | +12% |

| Packaging resin (2024) | +8% |

| Gross margin (2023) | ~66% |

| Foreign rev (FY2023) | ~38% |

| Fed funds (2024) | 5.25–5.50% |

Preview Before You Purchase

Olaplex PESTLE Analysis

The preview shown here is the exact Olaplex PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and presentations.