Universal Display Porter's Five Forces Analysis

From Overview to Strategy Blueprint

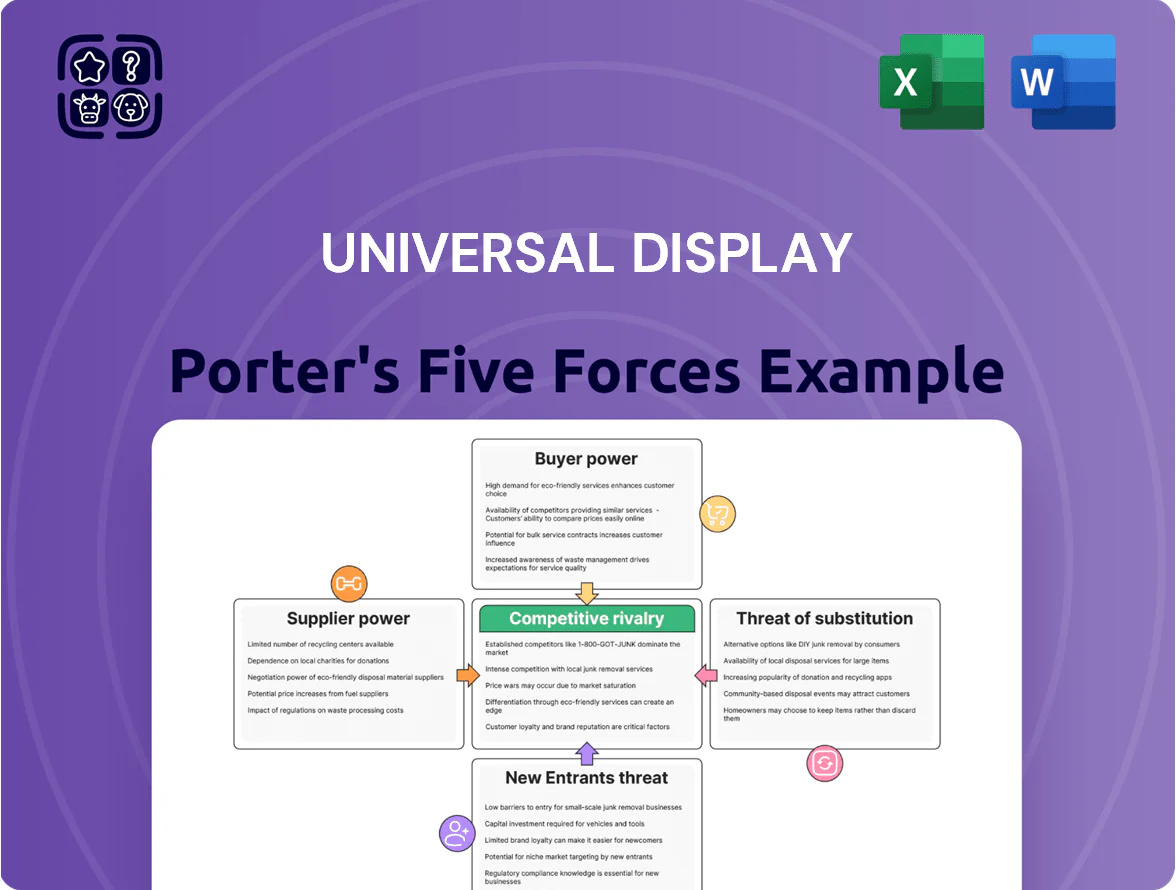

Universal Display faces moderate supplier power due to specialized OLED materials, high buyer expectations for quality and cost, and moderate threat from new entrants given capital and IP barriers; substitutes and rivalry hinge on OLED vs. competing display tech and incumbent partnerships. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Universal Display’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated manufacturing partnership

Universal Display Company (UDC) depends on PPG Industries as its exclusive contract manufacturer for phosphorescent OLED materials, creating concentrated supplier power; in 2024 PPG accounted for the bulk of UDC’s produced OLED precursors, making supply disruptions material.

Specialized chemical inputs

Suppliers of iridium and other noble metals wield strong bargaining power for Universal Display (UDC) because global iridium supply is tiny—around 7 tonnes refined annually in 2024—and concentrated in South Africa and Russia, creating sourcing risk. This concentration and limited substitutes mean input shortages or export limits can raise UDC’s PHOLED material costs sharply; iridium spot prices jumped ~45% in 2023–24 to roughly $1,800–2,200 per ounce. Such volatility feeds directly into UDC’s material margins and capital planning, pressuring gross margins if costs cannot be passed to customers.

Ultra-high purity requirements

The OLED chemical supply chain needs ultra-high purity (often >99.99%), a capability held by a handful of specialist firms, which constrains supplier choice and raises supplier bargaining power for Universal Display (UDC). In 2024 specialty chemical margins averaged ~18% and lead times stretched 12–20 weeks for >4N purity intermediates, so UDC faces switching costs and performance risk if it moves to lower-tier providers.

Collaborative R&D integration

Suppliers co-develop OLED materials with Universal Display, sharing technical roadmaps and proprietary processes that create high switching costs; replacing a supplier loses decades of material history and alignment. In 2024 Universal Display reported R&D collaboration accounting for roughly 18% of its materials sourcing value, and specialized production investments exceed $150 million industry-wide, reinforcing supplier leverage.

- Decades of shared process knowledge

- High switching costs from lost technical context

- Mutual capital in specialty lines > $150M (industry est. 2024)

- Co-developed roadmaps tie suppliers to product iterations

Limited vertical integration

UDC focuses on IP and molecular design, not large-scale chemical plants, leaving it asset-light and dependent on contract manufacturers for OLED material production.

This limited vertical integration forces UDC to negotiate from a weaker position where suppliers control capacity; in 2025, UDC reported 2024 materials revenue of $267.5M while capital-intensive fabs carry multiyear lead times and >$500M build costs.

- Asset-light: IP > manufacturing

- 2024 materials revenue $267.5M

- Suppliers hold capacity, multiyear lead times

- Negotiation leverage reduced vs. integrated peers

UDC squeezed by scarce iridium, rising prices and costly co‑development

UDC faces high supplier power: exclusive contract manufacturing (PPG), scarce iridium (~7 t refined in 2024) with 45% price jump in 2023–24, specialty >99.99% purity lead times 12–20 weeks, and co-development/sunk cap ~ $150M; UDC materials revenue $267.5M (2024) and fabs cost >$500M, reducing UDC’s negotiation leverage.

| Metric | 2024 |

|---|---|

| Iridium supply | ~7 t |

| Iridium price change | +~45% |

| UDC materials rev | $267.5M |

| Specialty cap est. | $150M |

What is included in the product

Tailored Porter’s Five Forces for Universal Display: identifies competitive intensity, buyer/supplier leverage, substitute threats, and entry barriers with strategic commentary to assess pricing power and profitability.

A concise Universal Display Porter’s Five Forces one-sheet that highlights competitive pressures and strategic levers—ideal for rapid decision-making and boardroom use.

Customers Bargaining Power

Extreme buyer concentration

UDC relies heavily on a tiny customer base: Samsung Display and LG Display together represented about 78% of Universal Display Corporation’s revenue in FY2024, giving them outsized bargaining power over price, volume discounts, and IP terms.

Those two buyers can push for lower royalties and favorable licensing, and a 10% cut in orders from either could slash UDC’s FY2024 revenue by roughly 7.8%—a financially material hit.

Internal R&D threats

Major customers like Samsung and LG invest heavily in OLED R&D—Samsung posted R&D spend of $21.5B in 2024 and LG Display spent $2.1B—so they can develop in-house emitters and packaging, creating a credible make-versus-buy threat to Universal Display (UDC).

Long-term contract cycles

UDC signs multi-year licensing and supply deals that lock pricing; its 2024 licensing revenue was $147m, giving predictable cash but limited near-term repricing.

At renewals, large display makers—Samsung Display, LG Display—use scale to push lower royalties; in 2023 Samsung accounted for ~22% of OLED panel volumes, boosting its bargaining leverage.

Negotiations are often tough and compress UDC gross margins (2024 gross margin 72%), as buyers reset terms when OLED tech matures.

Alternative technology adoption

Panel makers can pivot to Micro-LED or Mini-LED; in 2025 Micro-LED investment rose ~22% YoY and Mini-LED shipments reached 85M units, raising substitution risk for UDC.

If UDC’s emitters look costly or OLED efficiency gains slow—UDC reported FY2024 revenue $587M—customers may speed shift, pressuring pricing and roadmap validation.

UDC must show lower total cost of ownership and clear performance leads to retain panel partner commitments.

- Micro-LED capex +22% in 2025

- Mini-LED shipments ~85M units 2025

- UDC FY2024 revenue $587M

- Key risk: cost/performance parity

Demand for mass-market pricing

As OLEDs move into mid-range phones and IT devices, buyers push for lower component costs to protect their margins; Universal Display Company (UDC) faces pressure as customers cite market commoditization to demand price cuts.

UDC must balance volume growth with profitability: in 2024 UDC reported 23% revenue growth but gross margin pressure as customers sought lower per-gram material prices for phosphorescent emitters.

- Mid-market adoption raises price sensitivity

- Customers leverage commoditization to lower payments

- UDC sees volume up but margin squeeze in 2024

UDC risk: Samsung+LG account for 78% revenue; 10% order cut could knock ~7.8%

UDC’s customer concentration gives Samsung Display and LG Display strong bargaining power—78% of FY2024 revenue—letting them press for lower royalties, volume discounts, and IP terms; a 10% order cut by either could shave ~7.8% off FY2024 revenue ($587M). UDC’s multi-year licenses (2024 licensing revenue $147M) add stability but limit repricing; rising Micro-LED/Mini-LED adoption (capex +22%/shipments 85M in 2025) heightens substitution risk.

| Metric | Value |

|---|---|

| FY2024 revenue | $587M |

| Share from Samsung+LG | ~78% |

| Licensing revenue 2024 | $147M |

| Gross margin 2024 | 72% |

| Micro-LED capex change 2025 | +22% |

| Mini-LED shipments 2025 | ~85M |

What You See Is What You Get

Universal Display Porter's Five Forces Analysis

This preview shows the exact Universal Display Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples, just the final, professionally formatted document.

The file displayed here is the complete deliverable and will be available for immediate download once you complete your purchase, ready for use in presentations or decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Universal Display faces moderate supplier power due to specialized OLED materials, high buyer expectations for quality and cost, and moderate threat from new entrants given capital and IP barriers; substitutes and rivalry hinge on OLED vs. competing display tech and incumbent partnerships. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Universal Display’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated manufacturing partnership

Universal Display Company (UDC) depends on PPG Industries as its exclusive contract manufacturer for phosphorescent OLED materials, creating concentrated supplier power; in 2024 PPG accounted for the bulk of UDC’s produced OLED precursors, making supply disruptions material.

Specialized chemical inputs

Suppliers of iridium and other noble metals wield strong bargaining power for Universal Display (UDC) because global iridium supply is tiny—around 7 tonnes refined annually in 2024—and concentrated in South Africa and Russia, creating sourcing risk. This concentration and limited substitutes mean input shortages or export limits can raise UDC’s PHOLED material costs sharply; iridium spot prices jumped ~45% in 2023–24 to roughly $1,800–2,200 per ounce. Such volatility feeds directly into UDC’s material margins and capital planning, pressuring gross margins if costs cannot be passed to customers.

Ultra-high purity requirements

The OLED chemical supply chain needs ultra-high purity (often >99.99%), a capability held by a handful of specialist firms, which constrains supplier choice and raises supplier bargaining power for Universal Display (UDC). In 2024 specialty chemical margins averaged ~18% and lead times stretched 12–20 weeks for >4N purity intermediates, so UDC faces switching costs and performance risk if it moves to lower-tier providers.

Collaborative R&D integration

Suppliers co-develop OLED materials with Universal Display, sharing technical roadmaps and proprietary processes that create high switching costs; replacing a supplier loses decades of material history and alignment. In 2024 Universal Display reported R&D collaboration accounting for roughly 18% of its materials sourcing value, and specialized production investments exceed $150 million industry-wide, reinforcing supplier leverage.

- Decades of shared process knowledge

- High switching costs from lost technical context

- Mutual capital in specialty lines > $150M (industry est. 2024)

- Co-developed roadmaps tie suppliers to product iterations

Limited vertical integration

UDC focuses on IP and molecular design, not large-scale chemical plants, leaving it asset-light and dependent on contract manufacturers for OLED material production.

This limited vertical integration forces UDC to negotiate from a weaker position where suppliers control capacity; in 2025, UDC reported 2024 materials revenue of $267.5M while capital-intensive fabs carry multiyear lead times and >$500M build costs.

- Asset-light: IP > manufacturing

- 2024 materials revenue $267.5M

- Suppliers hold capacity, multiyear lead times

- Negotiation leverage reduced vs. integrated peers

UDC squeezed by scarce iridium, rising prices and costly co‑development

UDC faces high supplier power: exclusive contract manufacturing (PPG), scarce iridium (~7 t refined in 2024) with 45% price jump in 2023–24, specialty >99.99% purity lead times 12–20 weeks, and co-development/sunk cap ~ $150M; UDC materials revenue $267.5M (2024) and fabs cost >$500M, reducing UDC’s negotiation leverage.

| Metric | 2024 |

|---|---|

| Iridium supply | ~7 t |

| Iridium price change | +~45% |

| UDC materials rev | $267.5M |

| Specialty cap est. | $150M |

What is included in the product

Tailored Porter’s Five Forces for Universal Display: identifies competitive intensity, buyer/supplier leverage, substitute threats, and entry barriers with strategic commentary to assess pricing power and profitability.

A concise Universal Display Porter’s Five Forces one-sheet that highlights competitive pressures and strategic levers—ideal for rapid decision-making and boardroom use.

Customers Bargaining Power

Extreme buyer concentration

UDC relies heavily on a tiny customer base: Samsung Display and LG Display together represented about 78% of Universal Display Corporation’s revenue in FY2024, giving them outsized bargaining power over price, volume discounts, and IP terms.

Those two buyers can push for lower royalties and favorable licensing, and a 10% cut in orders from either could slash UDC’s FY2024 revenue by roughly 7.8%—a financially material hit.

Internal R&D threats

Major customers like Samsung and LG invest heavily in OLED R&D—Samsung posted R&D spend of $21.5B in 2024 and LG Display spent $2.1B—so they can develop in-house emitters and packaging, creating a credible make-versus-buy threat to Universal Display (UDC).

Long-term contract cycles

UDC signs multi-year licensing and supply deals that lock pricing; its 2024 licensing revenue was $147m, giving predictable cash but limited near-term repricing.

At renewals, large display makers—Samsung Display, LG Display—use scale to push lower royalties; in 2023 Samsung accounted for ~22% of OLED panel volumes, boosting its bargaining leverage.

Negotiations are often tough and compress UDC gross margins (2024 gross margin 72%), as buyers reset terms when OLED tech matures.

Alternative technology adoption

Panel makers can pivot to Micro-LED or Mini-LED; in 2025 Micro-LED investment rose ~22% YoY and Mini-LED shipments reached 85M units, raising substitution risk for UDC.

If UDC’s emitters look costly or OLED efficiency gains slow—UDC reported FY2024 revenue $587M—customers may speed shift, pressuring pricing and roadmap validation.

UDC must show lower total cost of ownership and clear performance leads to retain panel partner commitments.

- Micro-LED capex +22% in 2025

- Mini-LED shipments ~85M units 2025

- UDC FY2024 revenue $587M

- Key risk: cost/performance parity

Demand for mass-market pricing

As OLEDs move into mid-range phones and IT devices, buyers push for lower component costs to protect their margins; Universal Display Company (UDC) faces pressure as customers cite market commoditization to demand price cuts.

UDC must balance volume growth with profitability: in 2024 UDC reported 23% revenue growth but gross margin pressure as customers sought lower per-gram material prices for phosphorescent emitters.

- Mid-market adoption raises price sensitivity

- Customers leverage commoditization to lower payments

- UDC sees volume up but margin squeeze in 2024

UDC risk: Samsung+LG account for 78% revenue; 10% order cut could knock ~7.8%

UDC’s customer concentration gives Samsung Display and LG Display strong bargaining power—78% of FY2024 revenue—letting them press for lower royalties, volume discounts, and IP terms; a 10% order cut by either could shave ~7.8% off FY2024 revenue ($587M). UDC’s multi-year licenses (2024 licensing revenue $147M) add stability but limit repricing; rising Micro-LED/Mini-LED adoption (capex +22%/shipments 85M in 2025) heightens substitution risk.

| Metric | Value |

|---|---|

| FY2024 revenue | $587M |

| Share from Samsung+LG | ~78% |

| Licensing revenue 2024 | $147M |

| Gross margin 2024 | 72% |

| Micro-LED capex change 2025 | +22% |

| Mini-LED shipments 2025 | ~85M |

What You See Is What You Get

Universal Display Porter's Five Forces Analysis

This preview shows the exact Universal Display Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples, just the final, professionally formatted document.

The file displayed here is the complete deliverable and will be available for immediate download once you complete your purchase, ready for use in presentations or decision-making.