Olympic Group PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic foresight with our PESTLE Analysis of Olympic Group—concise, current, and tailored to reveal how political shifts, economic trends, social change, technological advances, legal frameworks, and environmental pressures shape the company’s prospects; purchase the full report to access in-depth insights, actionable recommendations, and ready-to-use slides for smarter investment and strategy decisions.

Political factors

Government localization initiatives

The Egyptian government has intensified localization to cut imports and save foreign currency, targeting a 15–20% reduction in appliance import bills by 2025; Olympic Group benefits from incentives for models achieving local content thresholds, receiving tariff exemptions and tax rebates tied to component localization rates. These measures support Olympic Group’s plan to expand its domestic supply chain and invest in new manufacturing capacity through 2025, aligning with reported capex guidance of EGP 500–700 million.

Trade agreements and export potential

Egypt's membership in COMESA (21 members) and GAFTA (18+ Arab states) gives Olympic Group preferential market access, enabling tariff reductions that helped exports grow; Egyptian appliance exports rose 12% to $210m in 2024, supporting Olympic's regional shipments.

Regional geopolitical stability

The political landscape in the Middle East and North Africa remains critical for Olympic Group’s supply chain and export logistics, with 2024 Red Sea freight rates up about 35% year-on-year impacting regional shipping costs. Ongoing tensions can reroute shipments, raising transport expenses for finished goods by an estimated 10–15% and delaying deliveries to neighboring markets. Management must monitor diplomatic relations and contingency ports to mitigate cross-border trade disruption risks and potential revenue losses tied to logistics volatility.

Import regulations on components

Strict import controls on non-essential goods and industrial components force Olympic Group to adjust production scheduling; Egypt's 2024 import tariffs and licensing led to average customs delays of 12–18 days for electrical components, raising working capital needs by an estimated 3–5%.

While meant to protect local industry, shortages of domestically sourced parts have created bottlenecks impacting output by up to 6% in peak months; Olympic Group maintains active coordination with trade authorities and suppliers to secure priority clearance for critical inputs.

- Customs delays 12–18 days (2024)

- Working capital impact 3–5%

- Production shortfall up to 6% in peak months

- Ongoing dialogue with trade authorities for priority clearance

Political support for industrial zones

The Egyptian government’s push for industrial zones and the New Administrative Capital gives Olympic Group access to modern infrastructure and faster administrative clearances; the government announced 2024 investments of $10.4bn in new industrial zones and NAC utilities, improving manufacturing capacity.

Large-scale transport and logistics projects—$8.2bn in 2023–24 road and rail spending—lower distribution times and cut operating costs, supporting scale efficiencies and supply-chain resilience for Olympic Group.

Egypt targets 15–20% appliance import cut by 2025; exports up 12%, logistics raise costs

Government localization targets aim to cut appliance import bills 15–20% by 2025, backing Olympic Group with tariff exemptions and EGP 500–700m capex support; 2024 customs delays averaged 12–18 days, lifting working capital needs 3–5% and causing up to 6% peak-month output shortfalls; exports benefited from COMESA/GAFTA access as Egyptian appliance exports rose 12% to $210m in 2024; Red Sea freight rates +35% y/y raised regional shipping costs ~10–15%.

| Metric | Value (2024/2025) |

|---|---|

| Localization target | 15–20% import reduction by 2025 |

| Capex guidance | EGP 500–700m |

| Customs delays | 12–18 days |

| Working capital impact | 3–5% |

| Peak output shortfall | Up to 6% |

| Appliance exports | $210m (+12% y/y) |

| Red Sea freight rates | +35% y/y (costs +10–15%) |

What is included in the product

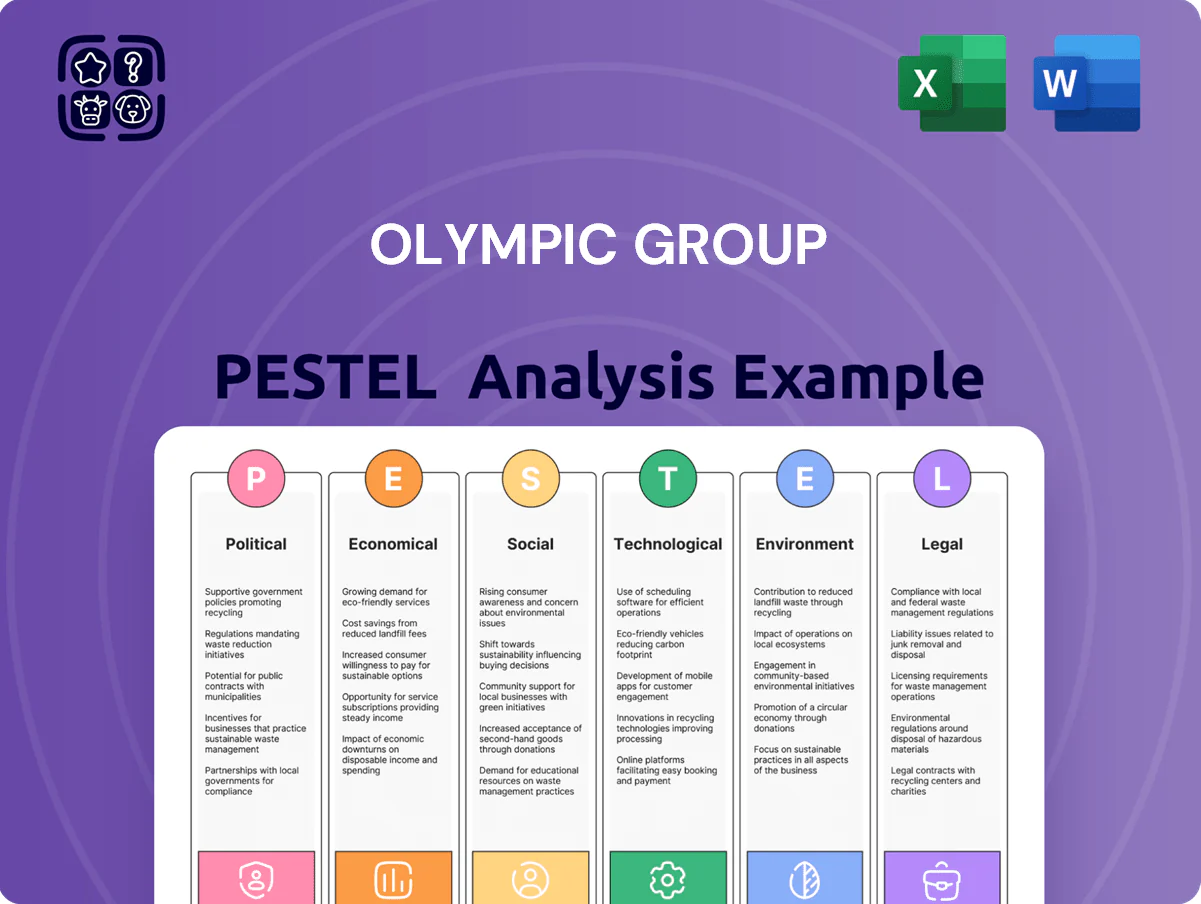

Explores how external macro-environmental factors uniquely affect the Olympic Group across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and current trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses Olympic Group's PESTLE into a clear, slide-ready summary that highlights key external risks and opportunities for fast alignment in meetings or strategy sessions.

Economic factors

Currency exchange rate fluctuations

The Egyptian Pound's 2024–2025 volatility—moving from ~30 EGP/USD in early 2024 to averages near 40 EGP/USD by late 2025—raised import costs for Olympic Group, increasing input bills for electronics by an estimated 25–35%, pressuring margins while local affordability remained key. The firm expanded hedging (FX forwards covering ~40% of annual import needs) and pushed local sourcing to ~28% of components to mitigate pass-through price shocks.

Inflationary pressure on household budgets

High inflation in Egypt (annual CPI ~39% in 2023, easing to ~25% by 2025) has squeezed household disposable income, reducing demand for durable goods; Olympic Group responded with financing plans (0%–18% instalments) and budget product lines, helping sustain sales volumes. In 2024 Olympic’s value-focused SKUs contributed an estimated 40% of unit sales, making price competitiveness a critical driver of market share in this price-sensitive environment.

Interest rates and consumer credit

Prevailing Central Bank of Egypt rates, at 23.25% (Dec 2024 policy rate), raise Olympic Group’s borrowing costs and tighten consumer lending; elevated rates reduce installment demand for appliances, a key sales driver—Egyptian consumer credit growth slowed to 7% YoY in 2024. Olympic Group mitigates this by partnering with banks and BNPL providers to offer subsidized financing, preserving affordability and supporting sales volumes.

Raw material price volatility

Global steel, plastic and copper price swings raised Olympic Group’s input costs by about 8% in 2023–24, with steel up ~22% YoY and copper averaging $9,200/tonne in 2024; as a large appliance maker, Olympic is exposed to these international cycle-driven commodity moves.

The company uses strategic procurement, forward contracts and inventory buffers—inventory days rose to 95 in FY2024—to mitigate sudden global price spikes and protect margins.

- 2023–24 input cost rise ~8%

Foreign direct investment climate

Egypt's 2024 FDI inflows rose to about $9.7bn, improving ease-of-doing-business metrics and drawing manufacturers; this climate benefits Olympic Group as a domestic market leader for attracting joint ventures and strategic partners.

Olympic Group's scale and 2023–24 revenue resilience position it to secure capital for tech upgrades and plant expansions amid government incentives and a positive GDP growth forecast near 4% for 2025.

- FDI 2024 ≈ $9.7bn; GDP growth ~4% (2025 forecast)

- Leader status = higher JV/PE interest for capex

- Access to funds supports tech upgrades and facility expansion

EGP ≈40, CPI easing to 25%, high rates squeeze demand as imports, hedges & FDI shape 2025

FX depreciation to ~40 EGP/USD by late 2025 raised import costs ~25–35%, hedging covers ~40% of imports; CPI eased from ~39% (2023) to ~25% (2025) hurting durable demand; CBE policy rate 23.25% (Dec 2024) tightened credit while BNPL/0%–18% instalments supported sales; commodity-driven input rise ~8% (2023–24); FDI 2024 ≈ $9.7bn, GDP ~4% (2025 forecast).

| Metric | Value |

|---|---|

| EGP/USD (late 2025) | ~40 |

| CPI (2025) | ~25% |

| CBE rate (Dec 2024) | 23.25% |

| Hedging coverage | ~40% |

| Input cost rise (2023–24) | ~8% |

| FDI 2024 | $9.7bn |

| GDP growth (2025 forecast) | ~4% |

What You See Is What You Get

Olympic Group PESTLE Analysis

The preview shown here is the exact Olympic Group PESTLE document you’ll receive after purchase—fully formatted and ready to use.

No placeholders or teasers: the layout, content, and structure visible here are exactly what you’ll download immediately after buying.

This is the real, finished file—professionally structured and delivered as shown, ready for analysis and presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic foresight with our PESTLE Analysis of Olympic Group—concise, current, and tailored to reveal how political shifts, economic trends, social change, technological advances, legal frameworks, and environmental pressures shape the company’s prospects; purchase the full report to access in-depth insights, actionable recommendations, and ready-to-use slides for smarter investment and strategy decisions.

Political factors

Government localization initiatives

The Egyptian government has intensified localization to cut imports and save foreign currency, targeting a 15–20% reduction in appliance import bills by 2025; Olympic Group benefits from incentives for models achieving local content thresholds, receiving tariff exemptions and tax rebates tied to component localization rates. These measures support Olympic Group’s plan to expand its domestic supply chain and invest in new manufacturing capacity through 2025, aligning with reported capex guidance of EGP 500–700 million.

Trade agreements and export potential

Egypt's membership in COMESA (21 members) and GAFTA (18+ Arab states) gives Olympic Group preferential market access, enabling tariff reductions that helped exports grow; Egyptian appliance exports rose 12% to $210m in 2024, supporting Olympic's regional shipments.

Regional geopolitical stability

The political landscape in the Middle East and North Africa remains critical for Olympic Group’s supply chain and export logistics, with 2024 Red Sea freight rates up about 35% year-on-year impacting regional shipping costs. Ongoing tensions can reroute shipments, raising transport expenses for finished goods by an estimated 10–15% and delaying deliveries to neighboring markets. Management must monitor diplomatic relations and contingency ports to mitigate cross-border trade disruption risks and potential revenue losses tied to logistics volatility.

Import regulations on components

Strict import controls on non-essential goods and industrial components force Olympic Group to adjust production scheduling; Egypt's 2024 import tariffs and licensing led to average customs delays of 12–18 days for electrical components, raising working capital needs by an estimated 3–5%.

While meant to protect local industry, shortages of domestically sourced parts have created bottlenecks impacting output by up to 6% in peak months; Olympic Group maintains active coordination with trade authorities and suppliers to secure priority clearance for critical inputs.

- Customs delays 12–18 days (2024)

- Working capital impact 3–5%

- Production shortfall up to 6% in peak months

- Ongoing dialogue with trade authorities for priority clearance

Political support for industrial zones

The Egyptian government’s push for industrial zones and the New Administrative Capital gives Olympic Group access to modern infrastructure and faster administrative clearances; the government announced 2024 investments of $10.4bn in new industrial zones and NAC utilities, improving manufacturing capacity.

Large-scale transport and logistics projects—$8.2bn in 2023–24 road and rail spending—lower distribution times and cut operating costs, supporting scale efficiencies and supply-chain resilience for Olympic Group.

Egypt targets 15–20% appliance import cut by 2025; exports up 12%, logistics raise costs

Government localization targets aim to cut appliance import bills 15–20% by 2025, backing Olympic Group with tariff exemptions and EGP 500–700m capex support; 2024 customs delays averaged 12–18 days, lifting working capital needs 3–5% and causing up to 6% peak-month output shortfalls; exports benefited from COMESA/GAFTA access as Egyptian appliance exports rose 12% to $210m in 2024; Red Sea freight rates +35% y/y raised regional shipping costs ~10–15%.

| Metric | Value (2024/2025) |

|---|---|

| Localization target | 15–20% import reduction by 2025 |

| Capex guidance | EGP 500–700m |

| Customs delays | 12–18 days |

| Working capital impact | 3–5% |

| Peak output shortfall | Up to 6% |

| Appliance exports | $210m (+12% y/y) |

| Red Sea freight rates | +35% y/y (costs +10–15%) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Olympic Group across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and current trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses Olympic Group's PESTLE into a clear, slide-ready summary that highlights key external risks and opportunities for fast alignment in meetings or strategy sessions.

Economic factors

Currency exchange rate fluctuations

The Egyptian Pound's 2024–2025 volatility—moving from ~30 EGP/USD in early 2024 to averages near 40 EGP/USD by late 2025—raised import costs for Olympic Group, increasing input bills for electronics by an estimated 25–35%, pressuring margins while local affordability remained key. The firm expanded hedging (FX forwards covering ~40% of annual import needs) and pushed local sourcing to ~28% of components to mitigate pass-through price shocks.

Inflationary pressure on household budgets

High inflation in Egypt (annual CPI ~39% in 2023, easing to ~25% by 2025) has squeezed household disposable income, reducing demand for durable goods; Olympic Group responded with financing plans (0%–18% instalments) and budget product lines, helping sustain sales volumes. In 2024 Olympic’s value-focused SKUs contributed an estimated 40% of unit sales, making price competitiveness a critical driver of market share in this price-sensitive environment.

Interest rates and consumer credit

Prevailing Central Bank of Egypt rates, at 23.25% (Dec 2024 policy rate), raise Olympic Group’s borrowing costs and tighten consumer lending; elevated rates reduce installment demand for appliances, a key sales driver—Egyptian consumer credit growth slowed to 7% YoY in 2024. Olympic Group mitigates this by partnering with banks and BNPL providers to offer subsidized financing, preserving affordability and supporting sales volumes.

Raw material price volatility

Global steel, plastic and copper price swings raised Olympic Group’s input costs by about 8% in 2023–24, with steel up ~22% YoY and copper averaging $9,200/tonne in 2024; as a large appliance maker, Olympic is exposed to these international cycle-driven commodity moves.

The company uses strategic procurement, forward contracts and inventory buffers—inventory days rose to 95 in FY2024—to mitigate sudden global price spikes and protect margins.

- 2023–24 input cost rise ~8%

Foreign direct investment climate

Egypt's 2024 FDI inflows rose to about $9.7bn, improving ease-of-doing-business metrics and drawing manufacturers; this climate benefits Olympic Group as a domestic market leader for attracting joint ventures and strategic partners.

Olympic Group's scale and 2023–24 revenue resilience position it to secure capital for tech upgrades and plant expansions amid government incentives and a positive GDP growth forecast near 4% for 2025.

- FDI 2024 ≈ $9.7bn; GDP growth ~4% (2025 forecast)

- Leader status = higher JV/PE interest for capex

- Access to funds supports tech upgrades and facility expansion

EGP ≈40, CPI easing to 25%, high rates squeeze demand as imports, hedges & FDI shape 2025

FX depreciation to ~40 EGP/USD by late 2025 raised import costs ~25–35%, hedging covers ~40% of imports; CPI eased from ~39% (2023) to ~25% (2025) hurting durable demand; CBE policy rate 23.25% (Dec 2024) tightened credit while BNPL/0%–18% instalments supported sales; commodity-driven input rise ~8% (2023–24); FDI 2024 ≈ $9.7bn, GDP ~4% (2025 forecast).

| Metric | Value |

|---|---|

| EGP/USD (late 2025) | ~40 |

| CPI (2025) | ~25% |

| CBE rate (Dec 2024) | 23.25% |

| Hedging coverage | ~40% |

| Input cost rise (2023–24) | ~8% |

| FDI 2024 | $9.7bn |

| GDP growth (2025 forecast) | ~4% |

What You See Is What You Get

Olympic Group PESTLE Analysis

The preview shown here is the exact Olympic Group PESTLE document you’ll receive after purchase—fully formatted and ready to use.

No placeholders or teasers: the layout, content, and structure visible here are exactly what you’ll download immediately after buying.

This is the real, finished file—professionally structured and delivered as shown, ready for analysis and presentation.