Omnicom Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

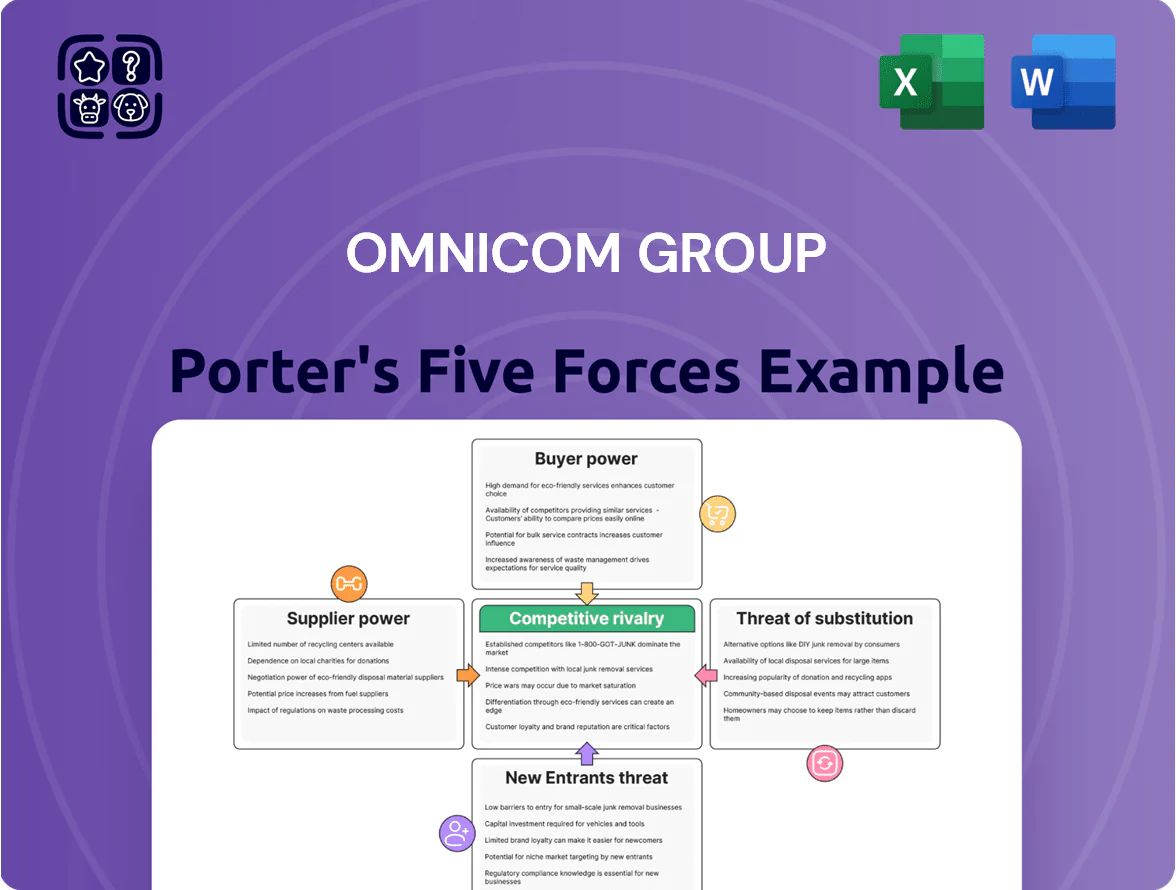

Omnicom Group faces moderate rivalry driven by large global competitors, high buyer bargaining power from major advertisers, and evolving substitute threats from in-house and digital platforms; supplier power and barriers to entry remain mixed due to talent concentration and scale advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Omnicom Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Digital Media Giants

The dominance of Google, Meta, and Amazon—which together sold about 64% of US digital ad spend in 2024 (eMarketer) —gives these suppliers strong leverage over Omnicom; they control most programmatic inventory and set rigid CPMs and auction rules. Their data access policies and walled gardens limit Omnicom’s targeting and measurement, forcing the agency to preserve close partnerships to deliver campaigns and constraining its pricing and negotiation power.

Scarcity of Specialized Creative and Technical Talent

The marketing industry depends on rare human capital—data scientists, AI specialists, and senior creative directors—and by Q4 2025 competition from Big Tech and in-house brand teams pushed median agency tech salaries up ~18% year-over-year, raising Omnicom’s labor spend materially.

Because campaign quality ties directly to those people, single experts and small specialist teams exert strong bargaining power over pay, remote flexibility, and project scope, pressuring margins and prompting retention investments.

Dependency on Third-Party Technology and AI Vendors

Omnicom increasingly embeds external SaaS and proprietary AI into client services—by 2024 roughly 30–35% of its data-analytics spend was on third-party platforms—giving vendors leverage via subscription hikes or API changes that can disrupt workflows and margin. Enterprise suites are deeply integrated, so switching costs (often tens of millions in migration and retraining) strengthen supplier power and raise operational risk if key providers tighten terms.

Rising Influence of Niche Content Creators and Influencers

The shift to fragmented media lets niche creators control access to highly engaged pockets; e.g., global influencer marketing hit $21.1B in 2023 and micro-influencers show 60–70% higher engagement versus celebrities.

Omnicom must negotiate with many individuals and boutique agencies that can command premium CPMs and equity deals, raising content costs and margins pressure.

Decentralized suppliers increase account management hours and hinder content-scale economies, cutting production scale-efficiencies by an estimated 10–15%.

- Influencer market: $21.1B (2023)

- Micro-influencer engagement: +60–70%

- Estimated scale-efficiency hit: 10–15%

Real Estate and Infrastructure Providers

- Global footprint: 40,000+ employees, 100+ countries

- Office reductions: ~10–20% (2023–24)

- London rents +8% (2024); Manhattan vacancy ~13% (Q3 2024)

- Long leases + rising O&M keep supplier leverage

Suppliers Dominate: Big Tech, Talent & SaaS Squeeze Margins and Raise Costs

Suppliers hold high bargaining power: Google, Meta, Amazon captured ~64% of US digital ad spend in 2024, setting prices and data rules; specialized talent costs rose ~18% YoY by Q4 2025, pressuring margins; third-party SaaS/AI made up ~30–35% of analytics spend in 2024, creating high switching costs; influencer market was $21.1B in 2023, fragmenting supply and raising production costs.

| Metric | Value |

|---|---|

| Big Tech share (US digital ads, 2024) | ~64% |

| Agency tech pay rise (to Q4 2025) | ~+18% YoY |

| Analytics spend on third-party (2024) | 30–35% |

| Influencer market (2023) | $21.1B |

What is included in the product

Tailored exclusively for Omnicom Group, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier influence, entry barriers, substitutes and emerging threats that shape Omnicom's pricing power and profitability.

A concise Porter's Five Forces snapshot for Omnicom—translate competitive pressures into actionable strategy in seconds.

Customers Bargaining Power

Pressure from Large Global Brand Portfolios

Omnicom earns most revenue from giant multinationals with centralized procurement that pooled media budgets; in 2024, its top 10 clients accounted for roughly 18% of consolidated revenue, so those buyers press for deep volume discounts and extended payment terms. Large clients often consolidate spend with one holding company, raising bargaining power and renewal leverage, and losing a single anchor can cut agency margins materially—Omnicom reported client losses in 2023 that trimmed operating income by several percentage points.

Shift Toward Performance-Based Compensation Models

By end-2025, an estimated 38% of Omnicom Group clients shifted from retainer fees to outcomes-based pricing, pushing the agency to accept higher financial risk as revenue ties to KPIs like sales growth or lead generation.

Performance contracts compress guaranteed margins—clients capture more upside control—Omnicom faces margin volatility: a 2024 internal review showed up to 12 percentage-point EBITDA swing on high-risk campaigns.

Low Switching Costs and Frequent Agency Reviews

The ad industry's competitiveness lets clients run agency reviews with low financial fallout, and 2024 estimates show global review activity affected ~15% of large accounts annually, keeping pressure on networks.

Moving an account is operationally tough, yet the threat of a pitch is routine—buyers use reviews to negotiate fee cuts or added services, trimming agency margins (Omnicom GAAP operating margin was 11.6% in 2024).

As a result Omnicom must keep reinvesting in client relationships—service upgrades, new capabilities, and discounts—to deter moves to WPP or Publicis, which together held ~40% of global network billings in 2024.

Demand for Radical Transparency in Media Buying

Clients now demand full visibility into media spend, especially programmatic channels and hidden markups; 72% of marketers surveyed in 2024 said transparency was a top vendor-selection factor, cutting agencies’ arbitrage margins by an estimated 8–12% of media spend.

Buyers routinely audit spend and fees, forcing Omnicom to reveal pass-through costs and shift to fixed fees or performance-based models, increasing buyer leverage over contract terms and pricing.

- 72% of marketers (2024) prioritize transparency

- Arbitrage margins reduced ~8–12%

- Shift to fixed fees/performance pricing

- Buyers dictate audit and reporting standards

In-Sourcing of Core Marketing Functions

Many Omnicom clients have built in-house teams for analytics, social media, and basic creative; a 2024 Econsultancy report found 36% of marketers moved work in-house, weakening agency dependency.

This in-housing offers a viable alternative, letting clients retain Omnicom only for complex campaigns and reducing project scope and revenue per client.

With internal cost visibility, buyers negotiate harder; Omnicom’s pricing power falls as margin-sensitive clients demand lower fees or outcome-based models.

- 36% of marketers moved work in-house (Econsultancy 2024)

- Clients cherry-pick complex services, cutting agency scope

- Greater cost transparency lowers agencies’ price leverage

Client power, fee shifts and transparency squeeze Omnicom margins—18% top clients, 11.6% GAAP

Buyers hold high power: Omnicom’s top 10 clients were ~18% of revenue in 2024, 38% of clients moved to outcomes-based fees by end-2025, and 36% of marketers in 2024 in-housed work; transparency demand (72% in 2024) cut arbitrage margins ~8–12%, driving fee pressure and margin volatility (Omnicom GAAP operating margin 11.6% in 2024).

| Metric | Value |

|---|---|

| Top-10 client share (2024) | ~18% |

| Outcomes-based clients (end-2025) | 38% |

| In-housing rate (2024) | 36% |

| Transparency priority (2024) | 72% |

| Arbitrage margin loss | 8–12% |

| GAAP operating margin (Omnicom 2024) | 11.6% |

Full Version Awaits

Omnicom Group Porter's Five Forces Analysis

This preview shows the exact Omnicom Group Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy. You're looking at the actual, professionally formatted file; once you complete your purchase, you’ll get instant access to this same document. No mockups or samples—what you see is what you'll be able to download.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Omnicom Group faces moderate rivalry driven by large global competitors, high buyer bargaining power from major advertisers, and evolving substitute threats from in-house and digital platforms; supplier power and barriers to entry remain mixed due to talent concentration and scale advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Omnicom Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Digital Media Giants

The dominance of Google, Meta, and Amazon—which together sold about 64% of US digital ad spend in 2024 (eMarketer) —gives these suppliers strong leverage over Omnicom; they control most programmatic inventory and set rigid CPMs and auction rules. Their data access policies and walled gardens limit Omnicom’s targeting and measurement, forcing the agency to preserve close partnerships to deliver campaigns and constraining its pricing and negotiation power.

Scarcity of Specialized Creative and Technical Talent

The marketing industry depends on rare human capital—data scientists, AI specialists, and senior creative directors—and by Q4 2025 competition from Big Tech and in-house brand teams pushed median agency tech salaries up ~18% year-over-year, raising Omnicom’s labor spend materially.

Because campaign quality ties directly to those people, single experts and small specialist teams exert strong bargaining power over pay, remote flexibility, and project scope, pressuring margins and prompting retention investments.

Dependency on Third-Party Technology and AI Vendors

Omnicom increasingly embeds external SaaS and proprietary AI into client services—by 2024 roughly 30–35% of its data-analytics spend was on third-party platforms—giving vendors leverage via subscription hikes or API changes that can disrupt workflows and margin. Enterprise suites are deeply integrated, so switching costs (often tens of millions in migration and retraining) strengthen supplier power and raise operational risk if key providers tighten terms.

Rising Influence of Niche Content Creators and Influencers

The shift to fragmented media lets niche creators control access to highly engaged pockets; e.g., global influencer marketing hit $21.1B in 2023 and micro-influencers show 60–70% higher engagement versus celebrities.

Omnicom must negotiate with many individuals and boutique agencies that can command premium CPMs and equity deals, raising content costs and margins pressure.

Decentralized suppliers increase account management hours and hinder content-scale economies, cutting production scale-efficiencies by an estimated 10–15%.

- Influencer market: $21.1B (2023)

- Micro-influencer engagement: +60–70%

- Estimated scale-efficiency hit: 10–15%

Real Estate and Infrastructure Providers

- Global footprint: 40,000+ employees, 100+ countries

- Office reductions: ~10–20% (2023–24)

- London rents +8% (2024); Manhattan vacancy ~13% (Q3 2024)

- Long leases + rising O&M keep supplier leverage

Suppliers Dominate: Big Tech, Talent & SaaS Squeeze Margins and Raise Costs

Suppliers hold high bargaining power: Google, Meta, Amazon captured ~64% of US digital ad spend in 2024, setting prices and data rules; specialized talent costs rose ~18% YoY by Q4 2025, pressuring margins; third-party SaaS/AI made up ~30–35% of analytics spend in 2024, creating high switching costs; influencer market was $21.1B in 2023, fragmenting supply and raising production costs.

| Metric | Value |

|---|---|

| Big Tech share (US digital ads, 2024) | ~64% |

| Agency tech pay rise (to Q4 2025) | ~+18% YoY |

| Analytics spend on third-party (2024) | 30–35% |

| Influencer market (2023) | $21.1B |

What is included in the product

Tailored exclusively for Omnicom Group, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier influence, entry barriers, substitutes and emerging threats that shape Omnicom's pricing power and profitability.

A concise Porter's Five Forces snapshot for Omnicom—translate competitive pressures into actionable strategy in seconds.

Customers Bargaining Power

Pressure from Large Global Brand Portfolios

Omnicom earns most revenue from giant multinationals with centralized procurement that pooled media budgets; in 2024, its top 10 clients accounted for roughly 18% of consolidated revenue, so those buyers press for deep volume discounts and extended payment terms. Large clients often consolidate spend with one holding company, raising bargaining power and renewal leverage, and losing a single anchor can cut agency margins materially—Omnicom reported client losses in 2023 that trimmed operating income by several percentage points.

Shift Toward Performance-Based Compensation Models

By end-2025, an estimated 38% of Omnicom Group clients shifted from retainer fees to outcomes-based pricing, pushing the agency to accept higher financial risk as revenue ties to KPIs like sales growth or lead generation.

Performance contracts compress guaranteed margins—clients capture more upside control—Omnicom faces margin volatility: a 2024 internal review showed up to 12 percentage-point EBITDA swing on high-risk campaigns.

Low Switching Costs and Frequent Agency Reviews

The ad industry's competitiveness lets clients run agency reviews with low financial fallout, and 2024 estimates show global review activity affected ~15% of large accounts annually, keeping pressure on networks.

Moving an account is operationally tough, yet the threat of a pitch is routine—buyers use reviews to negotiate fee cuts or added services, trimming agency margins (Omnicom GAAP operating margin was 11.6% in 2024).

As a result Omnicom must keep reinvesting in client relationships—service upgrades, new capabilities, and discounts—to deter moves to WPP or Publicis, which together held ~40% of global network billings in 2024.

Demand for Radical Transparency in Media Buying

Clients now demand full visibility into media spend, especially programmatic channels and hidden markups; 72% of marketers surveyed in 2024 said transparency was a top vendor-selection factor, cutting agencies’ arbitrage margins by an estimated 8–12% of media spend.

Buyers routinely audit spend and fees, forcing Omnicom to reveal pass-through costs and shift to fixed fees or performance-based models, increasing buyer leverage over contract terms and pricing.

- 72% of marketers (2024) prioritize transparency

- Arbitrage margins reduced ~8–12%

- Shift to fixed fees/performance pricing

- Buyers dictate audit and reporting standards

In-Sourcing of Core Marketing Functions

Many Omnicom clients have built in-house teams for analytics, social media, and basic creative; a 2024 Econsultancy report found 36% of marketers moved work in-house, weakening agency dependency.

This in-housing offers a viable alternative, letting clients retain Omnicom only for complex campaigns and reducing project scope and revenue per client.

With internal cost visibility, buyers negotiate harder; Omnicom’s pricing power falls as margin-sensitive clients demand lower fees or outcome-based models.

- 36% of marketers moved work in-house (Econsultancy 2024)

- Clients cherry-pick complex services, cutting agency scope

- Greater cost transparency lowers agencies’ price leverage

Client power, fee shifts and transparency squeeze Omnicom margins—18% top clients, 11.6% GAAP

Buyers hold high power: Omnicom’s top 10 clients were ~18% of revenue in 2024, 38% of clients moved to outcomes-based fees by end-2025, and 36% of marketers in 2024 in-housed work; transparency demand (72% in 2024) cut arbitrage margins ~8–12%, driving fee pressure and margin volatility (Omnicom GAAP operating margin 11.6% in 2024).

| Metric | Value |

|---|---|

| Top-10 client share (2024) | ~18% |

| Outcomes-based clients (end-2025) | 38% |

| In-housing rate (2024) | 36% |

| Transparency priority (2024) | 72% |

| Arbitrage margin loss | 8–12% |

| GAAP operating margin (Omnicom 2024) | 11.6% |

Full Version Awaits

Omnicom Group Porter's Five Forces Analysis

This preview shows the exact Omnicom Group Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy. You're looking at the actual, professionally formatted file; once you complete your purchase, you’ll get instant access to this same document. No mockups or samples—what you see is what you'll be able to download.