One PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

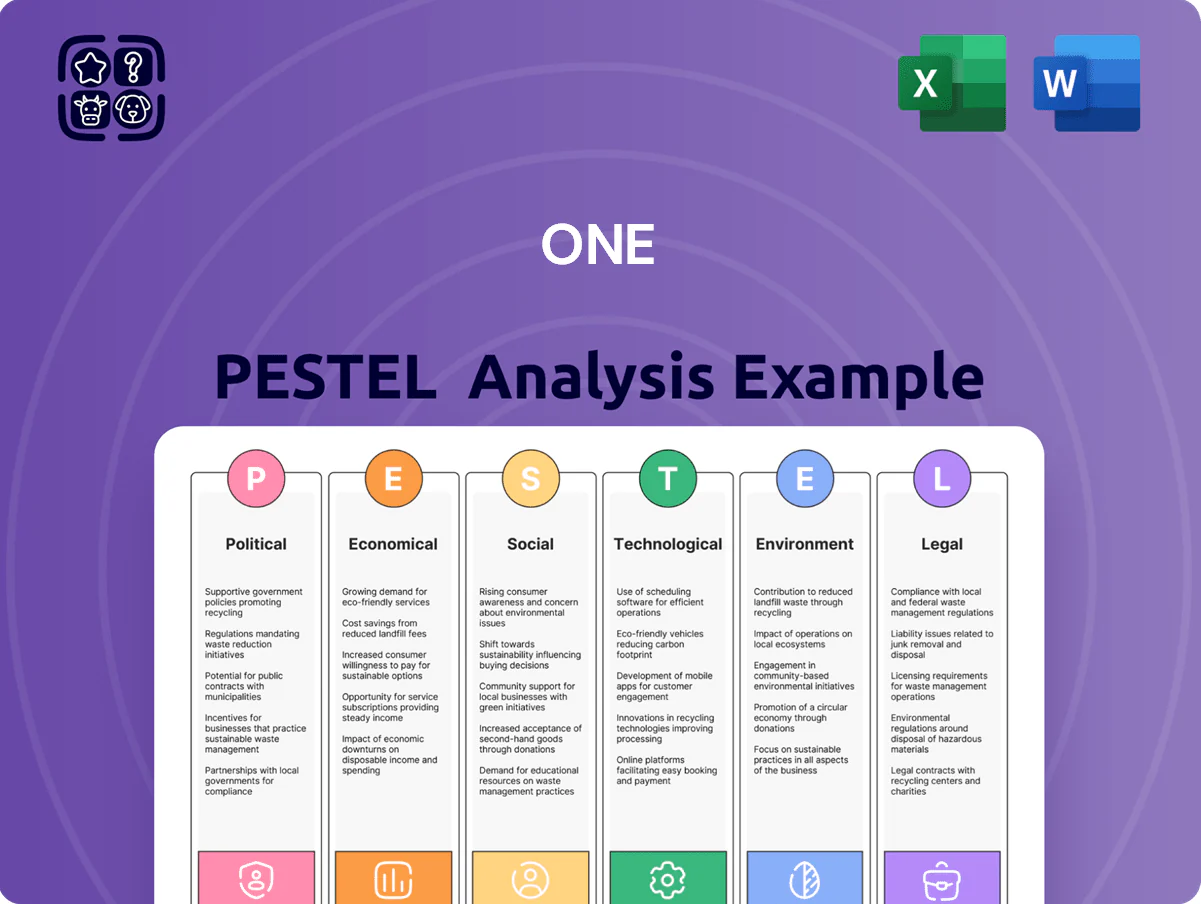

Unlock strategic clarity with our PESTLE Analysis of One—concise, expertly researched, and focused on the political, economic, social, technological, legal, and environmental forces shaping its future; buy the full report to access detailed risks, opportunities, and actionable recommendations you can use in investor decks, strategy sessions, or market due diligence.

Political factors

Geopolitical Stability in the Middle East

The ongoing security situation in Israel materially affects One 1 Ltd, with 2025 defense budgets rising to about NIS 160 billion (approx. USD 43 billion), shifting government procurement toward defense priorities and tightening capital for civilian infrastructure contracts.

Reserve duties reduced available workforce—IDF mobilizations in 2025 averaged tens of thousands monthly—raising overtime costs and pushing operational contingency spending up an estimated 8–12% for firms like One 1 Ltd.

Investor sentiment showed volatility: Tel Aviv 35 index fell 6.7% during major flare-ups in 2025, underscoring the need for One 1 Ltd to continuously monitor government stability when bidding multi-year infrastructure projects.

Government Digital Transformation Initiatives

The Israeli government remains a primary client for large-scale IT integration and cloud migration projects, spending an estimated NIS 6.2 billion on digital services in 2024; One 1 Ltd benefits directly from national policies targeting 30% cloud migration of public workloads by 2026 and the Digital Israel 2030 roadmap; maintaining strong ties with ministries is critical to secure high-value, multi-year contracts often worth NIS 50–200 million each.

International Trade Relations and Export Controls

As an Israeli entity, One 1 Ltd faces export controls and dual-use rules; Israel’s 2024 defense exports hit $11.5bn, highlighting stringent oversight that can restrict sensitive cybersecurity tech transfers.

Shifts in diplomatic ties—e.g., normalization with 7 Arab states since 2020 or tensions with EU/US—affect sourcing: 2023 Israeli ICT imports were $19.2bn, showing dependency on foreign hardware.

Compliance with EU/US dual-use regimes and Israeli Defense Export Controls is critical for its cybersecurity and data management units to avoid fines, license denials, or market bans.

Defense and National Security Procurement

A significant share of Israel's IT spend flows to defense tech; defense procurement rose to about $25.8 billion in 2024, keeping demand for secure IT high.

One 1 Ltd's system integration and cybersecurity capabilities make it a key supplier to the defense establishment, supporting classified projects and secure infrastructure deployments.

Changes in the national security budget—up 3.2% year-on-year in 2024—directly affect demand for One 1 Ltd's specialized tech services.

- 2024 Israeli defense procurement ≈ $25.8bn; +3.2% YoY

- One 1 Ltd strength: system integration, cybersecurity for classified programs

- Budget shifts produce proportional demand changes for secure infrastructure

Public Sector Budgetary Allocations

The company’s revenue is highly sensitive to Israeli state fiscal health; in 2025 Israel’s public IT budget for health and education was reported at roughly ILS 4.3 billion, and austerity or reallocation could delay projects that form ~35% of the firm’s public-sector pipeline.

Economic shocks or shifting political priorities can accelerate or postpone major healthcare and education IT contracts; tracking the annual budget approval (Knesset votes, typically passed by March) is critical to forecasting project timing and revenue recognition.

- Public IT budget 2025 ~ ILS 4.3bn

- ~35% of company pipeline tied to public projects

- Budget approval timing (Knesset, by March) impacts contract start

- Monitor fiscal shifts and ministry allocations monthly

One 1 Ltd faces defense-driven procurement shift, higher costs and export limits

Political risks for One 1 Ltd: higher 2025 defense budget ~NIS 160bn (~$43bn) shifts procurement to defense; reserve mobilization raised operational costs ~8–12%; public IT budget 2025 ~ILS 4.3bn with ~35% of pipeline public; export controls and dual-use regimes constrain cybersecurity exports.

| Metric | 2024–25 |

|---|---|

| Defense budget | NIS 160bn (~$43bn) |

| Defense procurement | $25.8bn (2024) |

| Public IT budget | ILS 4.3bn (2025) |

| Pipeline exposure | ~35% public |

What is included in the product

Explores how external macro-environmental factors uniquely affect the One across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to highlight risks and opportunities.

Condenses a full PESTLE into a clean, shareable snapshot that teams can drop into presentations or planning sessions to align quickly on external risks and opportunities.

Economic factors

Interest Rate Environment and Cost of Capital

The Bank of Israel policy rate rose to 4.25% in 2024, lifting One 1 Ltd’s marginal borrowing cost and making debt-funded M&A and capex more expensive; higher rates curtailed inorganic growth plans as debt service burdens increased.

If rates stabilize near 3.75–4.00% by late 2025 as some forecasts projected, One 1 Ltd may reallocate capital toward R&D and digital infrastructure, favoring internally funded projects over leveraged expansion.

Currency Fluctuations of the Israeli Shekel

One 1 Ltd sources hardware and global software licenses in USD/EUR while selling mainly in ILS; the shekel depreciated ~7% vs USD in 2024 and was ~3% stronger YTD Jan 2026, increasing input-cost volatility and squeezing gross margins by an estimated 150–300 bps for unhedged sales.

Currency swings reduce pricing competitiveness abroad and force frequent repricing of end-to-end solutions; in 2024 around 60% of procurement volume was USD-denominated, raising FX exposure.

Management routinely uses forward contracts and FX options—hedging covered roughly 70% of forecasted forex exposure in 2025—limiting earnings volatility but adding hedging costs of ~0.5–1.0% of procurement spend.

Inflationary Pressures on Operational Costs

Rising energy prices—UK industrial electricity up ~45% year-on-year in 2023 and global LNG up ~30% in 2024—plus commercial rent inflation averaging 6–8% and 12% wage growth for specialized tech roles are compressing One 1 Ltd’s margins; these pressures can raise operating costs by an estimated 5–12% annually. One 1 Ltd must adjust pricing strategically to reflect inflation without ceding share to nimble competitors. Rigorous cost-control, automation and supplier renegotiation are essential to sustain profitability amid volatility.

Tech Sector Labor Market Dynamics

The demand for highly skilled IT professionals in Israel remains intense, with tech sector vacancies up 18% in 2024 and average senior software engineer salaries reaching approximately ILS 500-700k annually, intensifying wage competition.

One 1 Ltd faces challenges attracting and retaining top-tier software development and cybersecurity talent while managing payroll, which can exceed 60% of operating costs for similar-sized firms.

Availability of skilled workforce is critical for delivering complex digital transformation projects; Israel's pool of certified cybersecurity specialists grew ~12% in 2023 but remains concentrated in major hubs.

- Tech vacancies +18% (2024)

- Senior engineer pay ILS 500-700k/year

- Payroll >60% of operating costs (peers)

- Cybersecurity specialists +12% (2023)

Consumer and Enterprise Spending Trends

The retail sector's recovery—UK retail sales up 3.8% y/y in 2025 Q4—alongside finance sector profit growth (EU banks ROE ~8.5% in 2025) will drive discretionary IT spend, lifting demand for upgrades and analytics.

Enterprise confidence improved in late 2025 (OECD business confidence index +4 points y/y), likely increasing spend on data management and cloud services; cloud market grew ~22% in 2025 to $420bn globally.

One 1 Ltd's diversified client mix across retail, finance and SMEs reduces revenue concentration risk and buffers localized sector downturns, with top-5 clients accounting for under 28% of revenue in FY2025.

- Retail sales +3.8% y/y (UK 2025 Q4)

- EU banks ROE ~8.5% (2025)

- OECD confidence +4 pts (2025)

- Cloud market ~$420bn, +22% (2025)

- Top-5 clients <28% revenue (One 1 Ltd FY2025)

Higher rates, FX hit margins; easing by 2025 may shift capex to R&D

Higher BoI rates (4.25% 2024) raised borrowing costs; if rates ease to ~3.75–4.00% by late 2025, capex may shift to R&D. FX volatility (ILS vs USD ~+7% depreciation in 2024; +3% stronger YTD Jan 2026) and 60% USD procurement cut gross margins ~150–300bps; hedging covered ~70% in 2025 at ~0.5–1.0% cost. Wage, energy and rent inflation lift operating costs 5–12% annually.

| Metric | Value |

|---|---|

| BoI rate 2024 | 4.25% |

| FX move 2024 | ILS -7% vs USD |

| Hedged 2025 | 70% |

| Operating cost rise | 5–12% |

Full Version Awaits

One PESTLE Analysis

The preview shown here is the exact One PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of One—concise, expertly researched, and focused on the political, economic, social, technological, legal, and environmental forces shaping its future; buy the full report to access detailed risks, opportunities, and actionable recommendations you can use in investor decks, strategy sessions, or market due diligence.

Political factors

Geopolitical Stability in the Middle East

The ongoing security situation in Israel materially affects One 1 Ltd, with 2025 defense budgets rising to about NIS 160 billion (approx. USD 43 billion), shifting government procurement toward defense priorities and tightening capital for civilian infrastructure contracts.

Reserve duties reduced available workforce—IDF mobilizations in 2025 averaged tens of thousands monthly—raising overtime costs and pushing operational contingency spending up an estimated 8–12% for firms like One 1 Ltd.

Investor sentiment showed volatility: Tel Aviv 35 index fell 6.7% during major flare-ups in 2025, underscoring the need for One 1 Ltd to continuously monitor government stability when bidding multi-year infrastructure projects.

Government Digital Transformation Initiatives

The Israeli government remains a primary client for large-scale IT integration and cloud migration projects, spending an estimated NIS 6.2 billion on digital services in 2024; One 1 Ltd benefits directly from national policies targeting 30% cloud migration of public workloads by 2026 and the Digital Israel 2030 roadmap; maintaining strong ties with ministries is critical to secure high-value, multi-year contracts often worth NIS 50–200 million each.

International Trade Relations and Export Controls

As an Israeli entity, One 1 Ltd faces export controls and dual-use rules; Israel’s 2024 defense exports hit $11.5bn, highlighting stringent oversight that can restrict sensitive cybersecurity tech transfers.

Shifts in diplomatic ties—e.g., normalization with 7 Arab states since 2020 or tensions with EU/US—affect sourcing: 2023 Israeli ICT imports were $19.2bn, showing dependency on foreign hardware.

Compliance with EU/US dual-use regimes and Israeli Defense Export Controls is critical for its cybersecurity and data management units to avoid fines, license denials, or market bans.

Defense and National Security Procurement

A significant share of Israel's IT spend flows to defense tech; defense procurement rose to about $25.8 billion in 2024, keeping demand for secure IT high.

One 1 Ltd's system integration and cybersecurity capabilities make it a key supplier to the defense establishment, supporting classified projects and secure infrastructure deployments.

Changes in the national security budget—up 3.2% year-on-year in 2024—directly affect demand for One 1 Ltd's specialized tech services.

- 2024 Israeli defense procurement ≈ $25.8bn; +3.2% YoY

- One 1 Ltd strength: system integration, cybersecurity for classified programs

- Budget shifts produce proportional demand changes for secure infrastructure

Public Sector Budgetary Allocations

The company’s revenue is highly sensitive to Israeli state fiscal health; in 2025 Israel’s public IT budget for health and education was reported at roughly ILS 4.3 billion, and austerity or reallocation could delay projects that form ~35% of the firm’s public-sector pipeline.

Economic shocks or shifting political priorities can accelerate or postpone major healthcare and education IT contracts; tracking the annual budget approval (Knesset votes, typically passed by March) is critical to forecasting project timing and revenue recognition.

- Public IT budget 2025 ~ ILS 4.3bn

- ~35% of company pipeline tied to public projects

- Budget approval timing (Knesset, by March) impacts contract start

- Monitor fiscal shifts and ministry allocations monthly

One 1 Ltd faces defense-driven procurement shift, higher costs and export limits

Political risks for One 1 Ltd: higher 2025 defense budget ~NIS 160bn (~$43bn) shifts procurement to defense; reserve mobilization raised operational costs ~8–12%; public IT budget 2025 ~ILS 4.3bn with ~35% of pipeline public; export controls and dual-use regimes constrain cybersecurity exports.

| Metric | 2024–25 |

|---|---|

| Defense budget | NIS 160bn (~$43bn) |

| Defense procurement | $25.8bn (2024) |

| Public IT budget | ILS 4.3bn (2025) |

| Pipeline exposure | ~35% public |

What is included in the product

Explores how external macro-environmental factors uniquely affect the One across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to highlight risks and opportunities.

Condenses a full PESTLE into a clean, shareable snapshot that teams can drop into presentations or planning sessions to align quickly on external risks and opportunities.

Economic factors

Interest Rate Environment and Cost of Capital

The Bank of Israel policy rate rose to 4.25% in 2024, lifting One 1 Ltd’s marginal borrowing cost and making debt-funded M&A and capex more expensive; higher rates curtailed inorganic growth plans as debt service burdens increased.

If rates stabilize near 3.75–4.00% by late 2025 as some forecasts projected, One 1 Ltd may reallocate capital toward R&D and digital infrastructure, favoring internally funded projects over leveraged expansion.

Currency Fluctuations of the Israeli Shekel

One 1 Ltd sources hardware and global software licenses in USD/EUR while selling mainly in ILS; the shekel depreciated ~7% vs USD in 2024 and was ~3% stronger YTD Jan 2026, increasing input-cost volatility and squeezing gross margins by an estimated 150–300 bps for unhedged sales.

Currency swings reduce pricing competitiveness abroad and force frequent repricing of end-to-end solutions; in 2024 around 60% of procurement volume was USD-denominated, raising FX exposure.

Management routinely uses forward contracts and FX options—hedging covered roughly 70% of forecasted forex exposure in 2025—limiting earnings volatility but adding hedging costs of ~0.5–1.0% of procurement spend.

Inflationary Pressures on Operational Costs

Rising energy prices—UK industrial electricity up ~45% year-on-year in 2023 and global LNG up ~30% in 2024—plus commercial rent inflation averaging 6–8% and 12% wage growth for specialized tech roles are compressing One 1 Ltd’s margins; these pressures can raise operating costs by an estimated 5–12% annually. One 1 Ltd must adjust pricing strategically to reflect inflation without ceding share to nimble competitors. Rigorous cost-control, automation and supplier renegotiation are essential to sustain profitability amid volatility.

Tech Sector Labor Market Dynamics

The demand for highly skilled IT professionals in Israel remains intense, with tech sector vacancies up 18% in 2024 and average senior software engineer salaries reaching approximately ILS 500-700k annually, intensifying wage competition.

One 1 Ltd faces challenges attracting and retaining top-tier software development and cybersecurity talent while managing payroll, which can exceed 60% of operating costs for similar-sized firms.

Availability of skilled workforce is critical for delivering complex digital transformation projects; Israel's pool of certified cybersecurity specialists grew ~12% in 2023 but remains concentrated in major hubs.

- Tech vacancies +18% (2024)

- Senior engineer pay ILS 500-700k/year

- Payroll >60% of operating costs (peers)

- Cybersecurity specialists +12% (2023)

Consumer and Enterprise Spending Trends

The retail sector's recovery—UK retail sales up 3.8% y/y in 2025 Q4—alongside finance sector profit growth (EU banks ROE ~8.5% in 2025) will drive discretionary IT spend, lifting demand for upgrades and analytics.

Enterprise confidence improved in late 2025 (OECD business confidence index +4 points y/y), likely increasing spend on data management and cloud services; cloud market grew ~22% in 2025 to $420bn globally.

One 1 Ltd's diversified client mix across retail, finance and SMEs reduces revenue concentration risk and buffers localized sector downturns, with top-5 clients accounting for under 28% of revenue in FY2025.

- Retail sales +3.8% y/y (UK 2025 Q4)

- EU banks ROE ~8.5% (2025)

- OECD confidence +4 pts (2025)

- Cloud market ~$420bn, +22% (2025)

- Top-5 clients <28% revenue (One 1 Ltd FY2025)

Higher rates, FX hit margins; easing by 2025 may shift capex to R&D

Higher BoI rates (4.25% 2024) raised borrowing costs; if rates ease to ~3.75–4.00% by late 2025, capex may shift to R&D. FX volatility (ILS vs USD ~+7% depreciation in 2024; +3% stronger YTD Jan 2026) and 60% USD procurement cut gross margins ~150–300bps; hedging covered ~70% in 2025 at ~0.5–1.0% cost. Wage, energy and rent inflation lift operating costs 5–12% annually.

| Metric | Value |

|---|---|

| BoI rate 2024 | 4.25% |

| FX move 2024 | ILS -7% vs USD |

| Hedged 2025 | 70% |

| Operating cost rise | 5–12% |

Full Version Awaits

One PESTLE Analysis

The preview shown here is the exact One PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.