Oneok Boston Consulting Group Matrix

Download Your Competitive Advantage

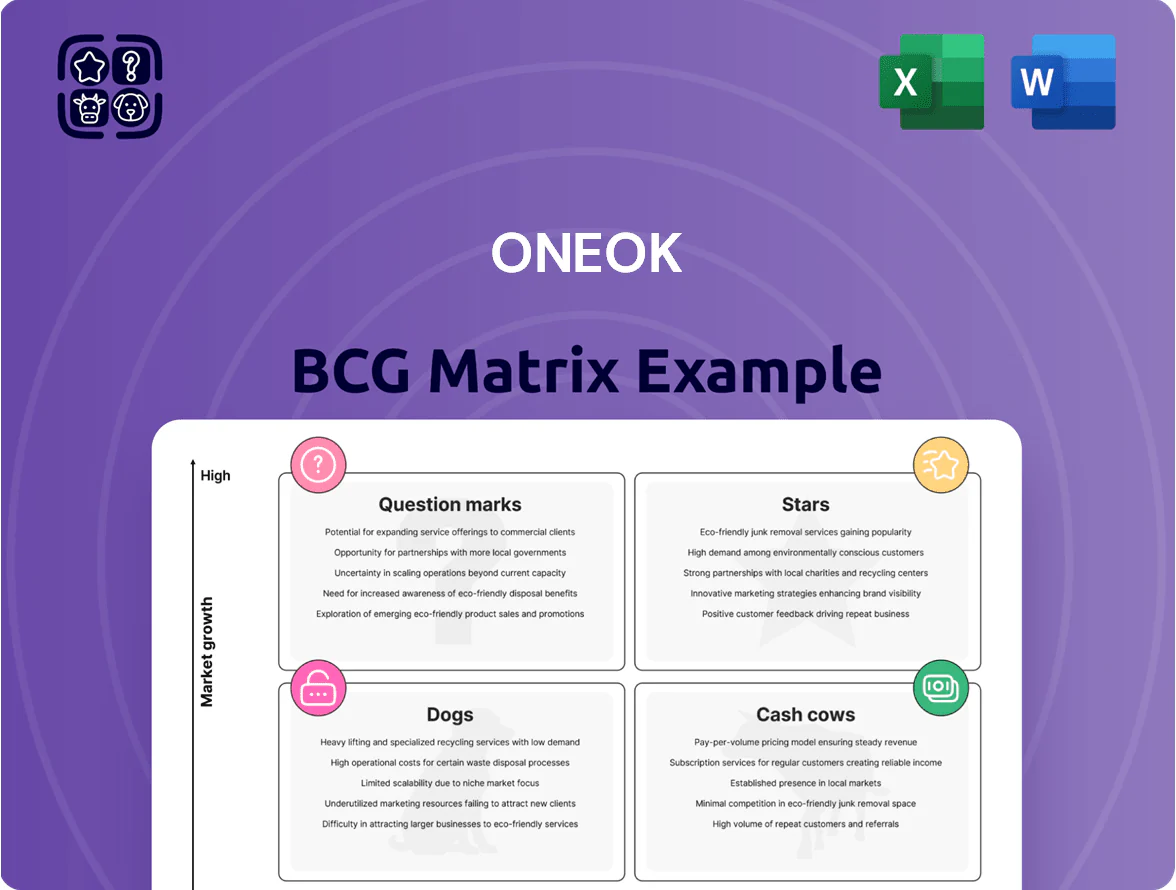

OneOK’s BCG Matrix snapshot highlights how its midstream gas processing and NGL businesses sit against market growth and share—some assets behave like steady Cash Cows, while newer projects could be Question Marks needing capital allocation decisions. This preview outlines key quadrant signals and strategic implications for investors and managers. Purchase the full BCG Matrix to get quadrant-by-quadrant placement, data-driven recommendations, and editable Word + Excel deliverables that guide where to invest, divest, or defend next.

Stars

Permian Basin NGL Expansion

Following integration of Magellan's NGL assets and organic projects completed by Dec 31, 2025, ONEOK holds a leading Permian Basin NGL market share estimated at ~28%, up from 18% in 2022.

Permian production hit record 2025 NGL volumes ~1.9 million barrels per day, driving segment revenue growth of ~22% YoY and requiring ~$1.1 billion capex announced for 2026–2027 to expand pipeline capacity.

These Permian assets are primary future revenue drivers, operating as market leaders in a high-demand region where takeaway constraints lifted by 2025 lower basis volatility and support sustained EBITDA margin expansion.

Refined Products Transport

The acquisition of Magellan Midstream (closed April 2023) made ONEOK the dominant refined-products transporter, lifting its central-U.S. gasoline and diesel pipeline share to roughly 35% of regional flows; export demand pushed U.S. refined-product exports to 2.3 million barrels/day in 2024, boosting volume growth. The unit is a cash cow for ONEOK, contributing an estimated $650–800 million annual EBITDA in 2025. Ongoing capital is needed for digital monitoring upgrades and regulatory compliance—ONEOK planned ~$300 million capex 2025–2026 for automation and safety. Integration risks remain but market fundamentals favor sustained volume gains.

Bakken NGL Fractionation Services

ONEOK’s Bakken NGL fractionation is a Star: as of YE 2025 the company processes ~150 MBPD of NGLs in the Williston Basin, up ~22% since 2022, driven by tighter gas-capture regs and drilling efficiency gains; strong demand supports above-market margins and justifies continued capital spend.

Gulf Coast Export Connectivity

Gulf Coast Export Connectivity sits in ONEOK’s BCG Matrix as a Star: rising global demand for U.S. liquefied petroleum gas (LPG) and ethane pushed ONEOK’s Gulf export flows up ~18% in 2024, and the segment captures a leading market share in Mid‑Continent-to‑Gulf exports.

ONEOK directed high capital spend—roughly $300–450 million annually in 2023–2025—into terminal expansions and new docking capacity to lift export throughput and meet international contract growth.

- 2024 export volume growth ≈ 18%

- Capital allocation ~$300–450M/year (2023–2025)

- Strong market share in ethane and LPG Gulf exports

- Priority for further terminal and dock expansion

Integrated Crude Oil Logistics

ONEOK’s integration of crude oil pipelines with its legacy natural gas assets created a full-stream service that, by Q4 2025, helped boost Mid-Continent producer revenues captured to an estimated 18% of wallet share and increased system throughput 12% year-over-year.

This integrated crude logistics offering is a Star in the BCG matrix because volumes and contract wins are rapidly rising and require continued capital spend (about $220 million in 2025 capex) to optimize combined network flow and uptime.

- Full-stream service: gas + crude pipelines

- Mid-Continent wallet share ~18% (Q4 2025)

- Throughput +12% YoY

- 2025 capex ~ $220 million to optimize flow

ONEOK Growth: Permian NGLs & Gulf Exports Fuel EBITDA; Capex to Scale Bakken/Crude

ONEOK Stars: Permian NGLs (~28% share YE2025) and Gulf exports (volumes +18% 2024) drive high-growth EBITDA; Bakken fractionation (150 MBPD YE2025) and integrated crude logistics (Mid‑Continent wallet ~18%, throughput +12% YoY) need continued capex ($1.1B 2026–27 Permian, $300–450M/year exports, $220M 2025 crude).

| Asset | Key 2025/24 Metric | Capex |

|---|---|---|

| Permian NGLs | Share ~28%; volumes 1.9M bpd (2025) | $1.1B (2026–27) |

| Gulf Exports | Volumes +18% (2024) | $300–450M/yr (2023–25) |

| Bakken Fractionation | 150 MBPD (YE2025); +22% since 2022 | Ongoing |

| Integrated Crude | Wallet ~18% (Q4 2025); throughput +12% YoY | $220M (2025) |

What is included in the product

Concise BCG Matrix analysis of ONEOK’s units with strategic recommendations—identify Stars, Cash Cows, Question Marks, Dogs, and suggested actions.

One-page Oneok BCG Matrix placing each business unit in a quadrant for clear portfolio decisions.

Cash Cows

Natural Gas Gathering and Processing

This mature Natural Gas Gathering and Processing segment delivers steady, fee-based cash flow that anchors ONEOK’s stability; in 2024 it accounted for about 38% of consolidated operating margin, returning roughly $1.1 billion in free cash flow to the parent.

Long-Haul Natural Gas Pipelines

ONEOK’s FERC-regulated long-haul interstate pipelines move gas from mature basins to utility hubs, generating roughly $1.1–1.3 billion EBITDA annually (2024 reported), and facing ~1–2% volumetric growth—classic low-growth cash cows.

High barriers to entry—regulatory permits, right-of-way, and $8–12 billion replacement-value networks—secure market share and support predictable fee-based revenue with maintenance capex near 5–8% of EBITDA.

Ethane Storage and Storage Services

Oneok’s ethane storage caverns at Mont Belvieu (Texas) and Conway (Kansas) give it a dominant market share in a mature, utility-like storage market; Mont Belvieu alone handles roughly 20+ million barrels of NGL capacity across the region. Storage services deliver steady, high-margin cash flows—Oneok reported ~18% adjusted EBITDA margin for its NGL storage and services in 2024—insulating profits from commodity price swings. This segment needs minimal promotional spend and low capital growth; maintenance and turnarounds drive most capex, under 10% of segment cash generation. As a cash cow in the BCG matrix, it funds Oneok’s higher-growth projects while sustaining robust free cash flow.

Fractionation Assets in Mid-Continent

ONEOKs fractionation assets in Kansas and Oklahoma dominate a mature mid-continent NGL (natural gas liquids) market, processing ~350 MBPD (thousand barrels per day) combined capacity and achieving >40% regional market share as of 2025.

Scale and proximity to Permian and Midcontinent production give a structural margin advantage; EBITDA margins for fractionation were ~36% in FY2024, generating excess free cash flow used to pay down debt.

These cash cows funded ONEOKs net debt reduction of ~$1.1 billion in 2024 and supported its BBB+ investment-grade rating from S&P (2025 review), as cash from operations exceeded capital expenditure.

- Combined capacity ~350 MBPD (2025)

- Regional market share >40% (2025)

- Fractionation EBITDA margin ~36% (FY2024)

- Net debt cut ~$1.1B (2024)

- S&P rating BBB+ (2025 review)

Legacy NGL Pipeline Networks

Legacy NGL pipeline networks at ONEOK (OKE) have run for decades, carrying propane, butane and natural gasoline under long-term contracts and generating steady fee-based cash flows; in 2024 these midstream tolls helped ONEOK report adjusted EBITDA of about $2.1 billion through core liquids operations.

With most pipeline capex fully depreciated, margins per barrel are very high — ONEOK’s liquids segment posted operating margins near 55% in 2024 — turning former growth Stars into reliable cash cows that fund dividends and buybacks.

- Decades of operation, long-term contracts

- Most assets depreciated → high margin per barrel

- 2024 liquids adjusted EBITDA ≈ $2.1B

- 2024 liquids operating margin ≈ 55%

ONEOK: $2.1B liquids EBITDA, 36% frac margin, 20M+ bbl storage, $1.1B debt cut, BBB+

ONEOK’s mature NGL and interstate gas-gathering assets generate steady, fee-based cash flow—2024 core liquids adjusted EBITDA ≈ $2.1B; fractionation EBITDA margin ~36% (FY2024); Mont Belvieu storage ~20M+ bbl capacity—these cash cows funded ~$1.1B net debt reduction in 2024 and support a BBB+ rating (S&P 2025).

| Metric | Value |

|---|---|

| Liquids EBITDA (2024) | $2.1B |

| Fractionation margin (FY2024) | ~36% |

| Mont Belvieu capacity | 20M+ bbl |

| Net debt reduction (2024) | $1.1B |

| S&P rating (2025) | BBB+ |

Full Transparency, Always

Oneok BCG Matrix

The file you're previewing is the final Oneok BCG Matrix you'll receive after purchase — no watermarks, no demo content, just a fully formatted, analysis-ready report tailored for strategic clarity and professional presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

OneOK’s BCG Matrix snapshot highlights how its midstream gas processing and NGL businesses sit against market growth and share—some assets behave like steady Cash Cows, while newer projects could be Question Marks needing capital allocation decisions. This preview outlines key quadrant signals and strategic implications for investors and managers. Purchase the full BCG Matrix to get quadrant-by-quadrant placement, data-driven recommendations, and editable Word + Excel deliverables that guide where to invest, divest, or defend next.

Stars

Permian Basin NGL Expansion

Following integration of Magellan's NGL assets and organic projects completed by Dec 31, 2025, ONEOK holds a leading Permian Basin NGL market share estimated at ~28%, up from 18% in 2022.

Permian production hit record 2025 NGL volumes ~1.9 million barrels per day, driving segment revenue growth of ~22% YoY and requiring ~$1.1 billion capex announced for 2026–2027 to expand pipeline capacity.

These Permian assets are primary future revenue drivers, operating as market leaders in a high-demand region where takeaway constraints lifted by 2025 lower basis volatility and support sustained EBITDA margin expansion.

Refined Products Transport

The acquisition of Magellan Midstream (closed April 2023) made ONEOK the dominant refined-products transporter, lifting its central-U.S. gasoline and diesel pipeline share to roughly 35% of regional flows; export demand pushed U.S. refined-product exports to 2.3 million barrels/day in 2024, boosting volume growth. The unit is a cash cow for ONEOK, contributing an estimated $650–800 million annual EBITDA in 2025. Ongoing capital is needed for digital monitoring upgrades and regulatory compliance—ONEOK planned ~$300 million capex 2025–2026 for automation and safety. Integration risks remain but market fundamentals favor sustained volume gains.

Bakken NGL Fractionation Services

ONEOK’s Bakken NGL fractionation is a Star: as of YE 2025 the company processes ~150 MBPD of NGLs in the Williston Basin, up ~22% since 2022, driven by tighter gas-capture regs and drilling efficiency gains; strong demand supports above-market margins and justifies continued capital spend.

Gulf Coast Export Connectivity

Gulf Coast Export Connectivity sits in ONEOK’s BCG Matrix as a Star: rising global demand for U.S. liquefied petroleum gas (LPG) and ethane pushed ONEOK’s Gulf export flows up ~18% in 2024, and the segment captures a leading market share in Mid‑Continent-to‑Gulf exports.

ONEOK directed high capital spend—roughly $300–450 million annually in 2023–2025—into terminal expansions and new docking capacity to lift export throughput and meet international contract growth.

- 2024 export volume growth ≈ 18%

- Capital allocation ~$300–450M/year (2023–2025)

- Strong market share in ethane and LPG Gulf exports

- Priority for further terminal and dock expansion

Integrated Crude Oil Logistics

ONEOK’s integration of crude oil pipelines with its legacy natural gas assets created a full-stream service that, by Q4 2025, helped boost Mid-Continent producer revenues captured to an estimated 18% of wallet share and increased system throughput 12% year-over-year.

This integrated crude logistics offering is a Star in the BCG matrix because volumes and contract wins are rapidly rising and require continued capital spend (about $220 million in 2025 capex) to optimize combined network flow and uptime.

- Full-stream service: gas + crude pipelines

- Mid-Continent wallet share ~18% (Q4 2025)

- Throughput +12% YoY

- 2025 capex ~ $220 million to optimize flow

ONEOK Growth: Permian NGLs & Gulf Exports Fuel EBITDA; Capex to Scale Bakken/Crude

ONEOK Stars: Permian NGLs (~28% share YE2025) and Gulf exports (volumes +18% 2024) drive high-growth EBITDA; Bakken fractionation (150 MBPD YE2025) and integrated crude logistics (Mid‑Continent wallet ~18%, throughput +12% YoY) need continued capex ($1.1B 2026–27 Permian, $300–450M/year exports, $220M 2025 crude).

| Asset | Key 2025/24 Metric | Capex |

|---|---|---|

| Permian NGLs | Share ~28%; volumes 1.9M bpd (2025) | $1.1B (2026–27) |

| Gulf Exports | Volumes +18% (2024) | $300–450M/yr (2023–25) |

| Bakken Fractionation | 150 MBPD (YE2025); +22% since 2022 | Ongoing |

| Integrated Crude | Wallet ~18% (Q4 2025); throughput +12% YoY | $220M (2025) |

What is included in the product

Concise BCG Matrix analysis of ONEOK’s units with strategic recommendations—identify Stars, Cash Cows, Question Marks, Dogs, and suggested actions.

One-page Oneok BCG Matrix placing each business unit in a quadrant for clear portfolio decisions.

Cash Cows

Natural Gas Gathering and Processing

This mature Natural Gas Gathering and Processing segment delivers steady, fee-based cash flow that anchors ONEOK’s stability; in 2024 it accounted for about 38% of consolidated operating margin, returning roughly $1.1 billion in free cash flow to the parent.

Long-Haul Natural Gas Pipelines

ONEOK’s FERC-regulated long-haul interstate pipelines move gas from mature basins to utility hubs, generating roughly $1.1–1.3 billion EBITDA annually (2024 reported), and facing ~1–2% volumetric growth—classic low-growth cash cows.

High barriers to entry—regulatory permits, right-of-way, and $8–12 billion replacement-value networks—secure market share and support predictable fee-based revenue with maintenance capex near 5–8% of EBITDA.

Ethane Storage and Storage Services

Oneok’s ethane storage caverns at Mont Belvieu (Texas) and Conway (Kansas) give it a dominant market share in a mature, utility-like storage market; Mont Belvieu alone handles roughly 20+ million barrels of NGL capacity across the region. Storage services deliver steady, high-margin cash flows—Oneok reported ~18% adjusted EBITDA margin for its NGL storage and services in 2024—insulating profits from commodity price swings. This segment needs minimal promotional spend and low capital growth; maintenance and turnarounds drive most capex, under 10% of segment cash generation. As a cash cow in the BCG matrix, it funds Oneok’s higher-growth projects while sustaining robust free cash flow.

Fractionation Assets in Mid-Continent

ONEOKs fractionation assets in Kansas and Oklahoma dominate a mature mid-continent NGL (natural gas liquids) market, processing ~350 MBPD (thousand barrels per day) combined capacity and achieving >40% regional market share as of 2025.

Scale and proximity to Permian and Midcontinent production give a structural margin advantage; EBITDA margins for fractionation were ~36% in FY2024, generating excess free cash flow used to pay down debt.

These cash cows funded ONEOKs net debt reduction of ~$1.1 billion in 2024 and supported its BBB+ investment-grade rating from S&P (2025 review), as cash from operations exceeded capital expenditure.

- Combined capacity ~350 MBPD (2025)

- Regional market share >40% (2025)

- Fractionation EBITDA margin ~36% (FY2024)

- Net debt cut ~$1.1B (2024)

- S&P rating BBB+ (2025 review)

Legacy NGL Pipeline Networks

Legacy NGL pipeline networks at ONEOK (OKE) have run for decades, carrying propane, butane and natural gasoline under long-term contracts and generating steady fee-based cash flows; in 2024 these midstream tolls helped ONEOK report adjusted EBITDA of about $2.1 billion through core liquids operations.

With most pipeline capex fully depreciated, margins per barrel are very high — ONEOK’s liquids segment posted operating margins near 55% in 2024 — turning former growth Stars into reliable cash cows that fund dividends and buybacks.

- Decades of operation, long-term contracts

- Most assets depreciated → high margin per barrel

- 2024 liquids adjusted EBITDA ≈ $2.1B

- 2024 liquids operating margin ≈ 55%

ONEOK: $2.1B liquids EBITDA, 36% frac margin, 20M+ bbl storage, $1.1B debt cut, BBB+

ONEOK’s mature NGL and interstate gas-gathering assets generate steady, fee-based cash flow—2024 core liquids adjusted EBITDA ≈ $2.1B; fractionation EBITDA margin ~36% (FY2024); Mont Belvieu storage ~20M+ bbl capacity—these cash cows funded ~$1.1B net debt reduction in 2024 and support a BBB+ rating (S&P 2025).

| Metric | Value |

|---|---|

| Liquids EBITDA (2024) | $2.1B |

| Fractionation margin (FY2024) | ~36% |

| Mont Belvieu capacity | 20M+ bbl |

| Net debt reduction (2024) | $1.1B |

| S&P rating (2025) | BBB+ |

Full Transparency, Always

Oneok BCG Matrix

The file you're previewing is the final Oneok BCG Matrix you'll receive after purchase — no watermarks, no demo content, just a fully formatted, analysis-ready report tailored for strategic clarity and professional presentation.