PaperWorks Industries Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

PaperWorks Industries faces moderate supplier power and intense rivalry amid paper commoditization, while digital substitution and fluctuating raw-material costs pressure margins; yet scale, distribution reach, and product diversification offer defensive advantages. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PaperWorks Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

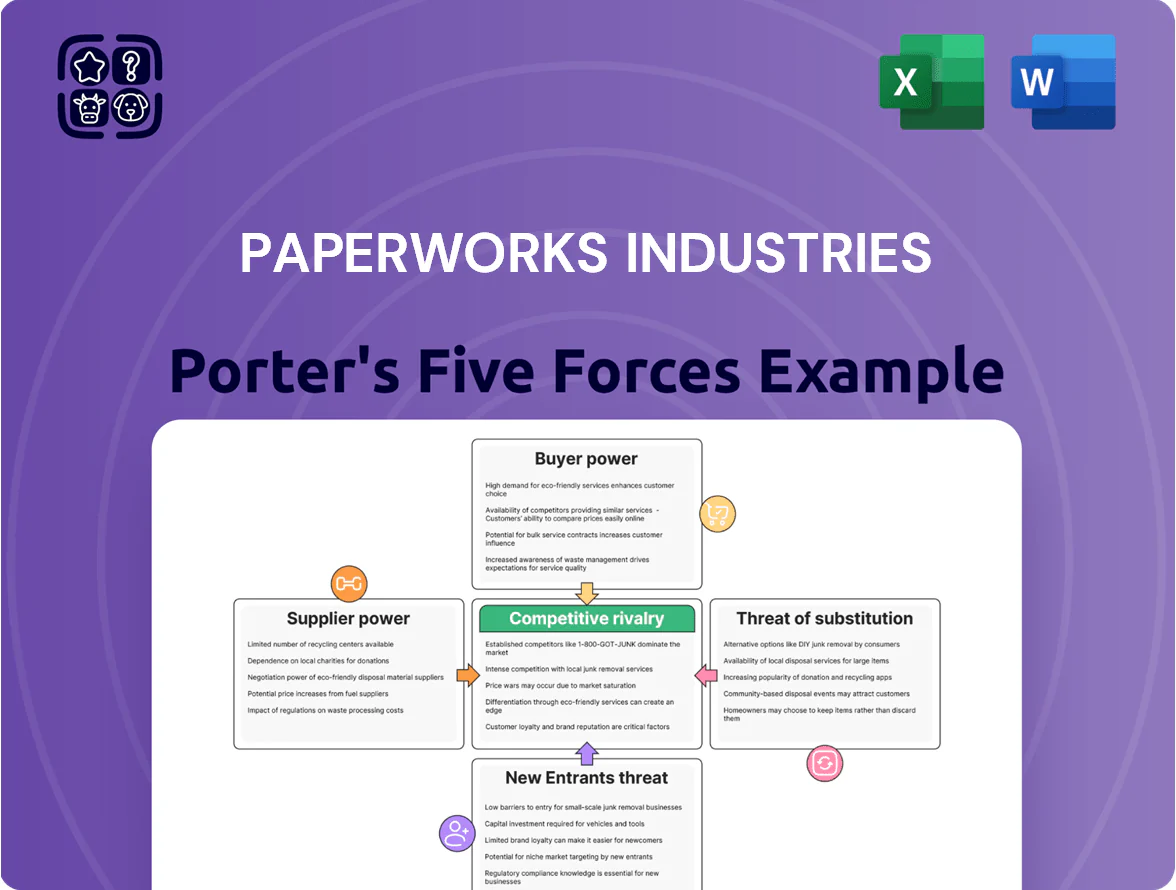

Suppliers Bargaining Power

Recycled Fiber Market Volatility

Recovered paper—chiefly old corrugated containers and mixed paper—remains PaperWorks Industries’ main input; as of late 2025 supplier power is moderate-to-high because US curbside collection fell ~4% year-on-year and global recycled fiber prices rose ~18% in 2025, tightening supply.

Large waste managers control ~60% of export-ready bales and can steer prices; when China and Southeast Asian demand spikes, domestic mill consumption faces spot-price swings of $20–$40/ton within months.

Energy and Utility Requirements

Paperboard manufacturing uses heavy electricity and natural gas; utilities made up ~25–35% of mill operating costs in 2024 for U.S. paperboard plants, giving suppliers leverage as mills shift to cleaner fuels to hit 2026 carbon targets.

Energy market volatility pushed natural gas spot prices 40% higher in 2022–24, directly lifting COGS and compressing margins for PaperWorks Industries, which lacks scale to secure long-term fixed rates without large volume commitments.

Specialty Chemical and Adhesive Providers

The production of high-quality folding cartons needs specific coatings, inks, and adhesives that meet food-safety and eco standards; only about 8–12 globally certified suppliers can deliver these at scale, so supplier concentration raises bargaining power. In 2024, specialty chemical margins averaged 18–22% and raw-material cost volatility hit 12% YoY, so switching to unproven alternatives risks product recalls, regulatory fines, and lost contracts.

Logistics and Transportation Constraints

Suppliers of freight and logistics wield strong leverage over PaperWorks due to the need to move heavy paperboard rolls and finished packaging; truck capacity tightness and contract concentration raise switching costs.

Trucking labor costs rose ~12% from 2020–2024 and 2025 EU/US emission rules pushed carrier rates up ~6–9%, increasing PaperWorks’ shipping expense and margin pressure.

Dependence on third-party just-in-time delivery for CPG clients makes PaperWorks sensitive to service-price hikes and capacity disruptions.

- High supplier leverage: concentrated carriers

- Labor costs +12% (2020–24)

- 2025 emission rules raised rates 6–9%

- JIT reliance increases disruption risk

Technological and Machinery Providers

The global market for paperboard converting machinery is concentrated among 5 major engineering firms, giving suppliers strong leverage through proprietary designs and exclusive spare-parts networks; long-term service contracts often tie mills into 5–10 year commitments.

Upgrading to high-efficiency or automation by 2026 typically requires CAPEX of $10–40 million per line and continued dependence on vendor technical support, creating switching costs and supplier bargaining power.

- 5 main suppliers dominate global supply

- Service contracts: 5–10 years

- Upgrade CAPEX: $10–40M per production line

- High switching costs due to proprietary parts

Suppliers wield strong leverage: tight recovered fiber, high energy & CAPEX pressure

Suppliers hold moderate-to-high power: recovered-fiber tightness (US curbside -4% YoY; recycled fiber +18% in 2025), large waste managers control ~60% export bales, energy = 25–35% of mill costs, natural gas +40% (2022–24), 8–12 certified specialty-chemical suppliers, trucking labor +12% (2020–24), 5 major machinery vendors (CAPEX $10–40M/line).

| Metric | Value |

|---|---|

| Curbside collection | -4% YoY (2025) |

| Recycled fiber price | +18% (2025) |

| Export-ready bales | 60% controlled |

| Energy share | 25–35% of costs (2024) |

| Gas price move | +40% (2022–24) |

| Specialty suppliers | 8–12 global |

| Machinery vendors | 5 major; CAPEX $10–40M |

What is included in the product

Tailored Porter's Five Forces analysis for PaperWorks Industries, revealing key competitive drivers, buyer and supplier power, substitution risks, and entry barriers that shape pricing and profitability.

One-sheet Porter's Five Forces summary for PaperWorks Industries—instantly highlights competitive pressures so leaders can make fast, informed strategic decisions.

Customers Bargaining Power

Concentration of Large CPG Brands

Low Switching Costs for Standard Packaging

While custom designs give PaperWorks some insulation, recycled paperboard for folding cartons trades like a semi-commodity; roughly 60% of North American carton buyers view substrate cost as the top purchase driver (2024 SmithPack survey). Low switching costs let customers shift to other integrated producers for a 3–7% price or 3–5 day lead-time improvement, so PaperWorks must keep on-time delivery above 95% and match market pricing to retain accounts.

Demand for Sustainable Innovation

By end-2025, 62% of packaging buyers surveyed prioritize plastic-free barriers and 45% require carbon-neutral supply chains, shifting procurement toward innovation over price. This raises customer bargaining power as buyers award contracts to firms with certified sustainable tech, pressuring margins. PaperWorks must boost R&D spend (industry median 2.3% revenue; consider 3–4%+) to retain share or risk losing accounts to rivals with advanced sustainable offerings.

Price Sensitivity in Retail Markets

- Inflation drives pass-through demands

- Suppliers asked to absorb 30–50% of material hikes

- 68% of CPGs use multi-sourcing (2023)

- Margin compression ~200–400 bps

Access to Market Information

Buyers now see live recycled fiber and paperboard indices—e.g., US OCC prices fell 12% in 2024, cutting supplier markup power—so customers quickly dispute hikes that lack spot-market support.

Procurement teams use dashboards and APIs to tie contracts to commodity cycles; 68% of large buyers reported renegotiating terms within 90 days in 2024.

- Real-time index access lowers info asymmetry

- 2024 US OCC down 12%: weaker supplier leverage

- 68% buyers renegotiated contracts within 90 days

CPGs dominate volumes, force cost absorption; sustainability rules compress margins 200–400bps

Large CPGs (60–70% volume) wield high leverage: single accounts = 5–15% plant revenue, 68% dual-source (2023), buyers forced PaperWorks to absorb 30–50% material hikes (2024); recycled-content and carbon rules in 70% contracts (2025) shift wins to sustainability leaders, compressing margins ~200–400 bps; 95% OTIF target and 3–4%+ R&D needed to defend share.

| Metric | Value |

|---|---|

| CPG volume share | 60–70% |

| Dual-sourcing | 68% (2023) |

| Account revenue | 5–15% |

| Material absorption | 30–50% (2024) |

| Margin pressure | 200–400 bps |

| Contracts w/ sustainability | 70% (2025) |

Full Version Awaits

PaperWorks Industries Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for PaperWorks Industries you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed is fully formatted and ready to download and use the moment you buy, covering competitive rivalry, supplier and buyer power, substitutes, and barriers to entry.

You're viewing the final deliverable; upon payment you'll get instant access to this same comprehensive, professionally written file.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

PaperWorks Industries faces moderate supplier power and intense rivalry amid paper commoditization, while digital substitution and fluctuating raw-material costs pressure margins; yet scale, distribution reach, and product diversification offer defensive advantages. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PaperWorks Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Recycled Fiber Market Volatility

Recovered paper—chiefly old corrugated containers and mixed paper—remains PaperWorks Industries’ main input; as of late 2025 supplier power is moderate-to-high because US curbside collection fell ~4% year-on-year and global recycled fiber prices rose ~18% in 2025, tightening supply.

Large waste managers control ~60% of export-ready bales and can steer prices; when China and Southeast Asian demand spikes, domestic mill consumption faces spot-price swings of $20–$40/ton within months.

Energy and Utility Requirements

Paperboard manufacturing uses heavy electricity and natural gas; utilities made up ~25–35% of mill operating costs in 2024 for U.S. paperboard plants, giving suppliers leverage as mills shift to cleaner fuels to hit 2026 carbon targets.

Energy market volatility pushed natural gas spot prices 40% higher in 2022–24, directly lifting COGS and compressing margins for PaperWorks Industries, which lacks scale to secure long-term fixed rates without large volume commitments.

Specialty Chemical and Adhesive Providers

The production of high-quality folding cartons needs specific coatings, inks, and adhesives that meet food-safety and eco standards; only about 8–12 globally certified suppliers can deliver these at scale, so supplier concentration raises bargaining power. In 2024, specialty chemical margins averaged 18–22% and raw-material cost volatility hit 12% YoY, so switching to unproven alternatives risks product recalls, regulatory fines, and lost contracts.

Logistics and Transportation Constraints

Suppliers of freight and logistics wield strong leverage over PaperWorks due to the need to move heavy paperboard rolls and finished packaging; truck capacity tightness and contract concentration raise switching costs.

Trucking labor costs rose ~12% from 2020–2024 and 2025 EU/US emission rules pushed carrier rates up ~6–9%, increasing PaperWorks’ shipping expense and margin pressure.

Dependence on third-party just-in-time delivery for CPG clients makes PaperWorks sensitive to service-price hikes and capacity disruptions.

- High supplier leverage: concentrated carriers

- Labor costs +12% (2020–24)

- 2025 emission rules raised rates 6–9%

- JIT reliance increases disruption risk

Technological and Machinery Providers

The global market for paperboard converting machinery is concentrated among 5 major engineering firms, giving suppliers strong leverage through proprietary designs and exclusive spare-parts networks; long-term service contracts often tie mills into 5–10 year commitments.

Upgrading to high-efficiency or automation by 2026 typically requires CAPEX of $10–40 million per line and continued dependence on vendor technical support, creating switching costs and supplier bargaining power.

- 5 main suppliers dominate global supply

- Service contracts: 5–10 years

- Upgrade CAPEX: $10–40M per production line

- High switching costs due to proprietary parts

Suppliers wield strong leverage: tight recovered fiber, high energy & CAPEX pressure

Suppliers hold moderate-to-high power: recovered-fiber tightness (US curbside -4% YoY; recycled fiber +18% in 2025), large waste managers control ~60% export bales, energy = 25–35% of mill costs, natural gas +40% (2022–24), 8–12 certified specialty-chemical suppliers, trucking labor +12% (2020–24), 5 major machinery vendors (CAPEX $10–40M/line).

| Metric | Value |

|---|---|

| Curbside collection | -4% YoY (2025) |

| Recycled fiber price | +18% (2025) |

| Export-ready bales | 60% controlled |

| Energy share | 25–35% of costs (2024) |

| Gas price move | +40% (2022–24) |

| Specialty suppliers | 8–12 global |

| Machinery vendors | 5 major; CAPEX $10–40M |

What is included in the product

Tailored Porter's Five Forces analysis for PaperWorks Industries, revealing key competitive drivers, buyer and supplier power, substitution risks, and entry barriers that shape pricing and profitability.

One-sheet Porter's Five Forces summary for PaperWorks Industries—instantly highlights competitive pressures so leaders can make fast, informed strategic decisions.

Customers Bargaining Power

Concentration of Large CPG Brands

Low Switching Costs for Standard Packaging

While custom designs give PaperWorks some insulation, recycled paperboard for folding cartons trades like a semi-commodity; roughly 60% of North American carton buyers view substrate cost as the top purchase driver (2024 SmithPack survey). Low switching costs let customers shift to other integrated producers for a 3–7% price or 3–5 day lead-time improvement, so PaperWorks must keep on-time delivery above 95% and match market pricing to retain accounts.

Demand for Sustainable Innovation

By end-2025, 62% of packaging buyers surveyed prioritize plastic-free barriers and 45% require carbon-neutral supply chains, shifting procurement toward innovation over price. This raises customer bargaining power as buyers award contracts to firms with certified sustainable tech, pressuring margins. PaperWorks must boost R&D spend (industry median 2.3% revenue; consider 3–4%+) to retain share or risk losing accounts to rivals with advanced sustainable offerings.

Price Sensitivity in Retail Markets

- Inflation drives pass-through demands

- Suppliers asked to absorb 30–50% of material hikes

- 68% of CPGs use multi-sourcing (2023)

- Margin compression ~200–400 bps

Access to Market Information

Buyers now see live recycled fiber and paperboard indices—e.g., US OCC prices fell 12% in 2024, cutting supplier markup power—so customers quickly dispute hikes that lack spot-market support.

Procurement teams use dashboards and APIs to tie contracts to commodity cycles; 68% of large buyers reported renegotiating terms within 90 days in 2024.

- Real-time index access lowers info asymmetry

- 2024 US OCC down 12%: weaker supplier leverage

- 68% buyers renegotiated contracts within 90 days

CPGs dominate volumes, force cost absorption; sustainability rules compress margins 200–400bps

Large CPGs (60–70% volume) wield high leverage: single accounts = 5–15% plant revenue, 68% dual-source (2023), buyers forced PaperWorks to absorb 30–50% material hikes (2024); recycled-content and carbon rules in 70% contracts (2025) shift wins to sustainability leaders, compressing margins ~200–400 bps; 95% OTIF target and 3–4%+ R&D needed to defend share.

| Metric | Value |

|---|---|

| CPG volume share | 60–70% |

| Dual-sourcing | 68% (2023) |

| Account revenue | 5–15% |

| Material absorption | 30–50% (2024) |

| Margin pressure | 200–400 bps |

| Contracts w/ sustainability | 70% (2025) |

Full Version Awaits

PaperWorks Industries Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for PaperWorks Industries you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed is fully formatted and ready to download and use the moment you buy, covering competitive rivalry, supplier and buyer power, substitutes, and barriers to entry.

You're viewing the final deliverable; upon payment you'll get instant access to this same comprehensive, professionally written file.