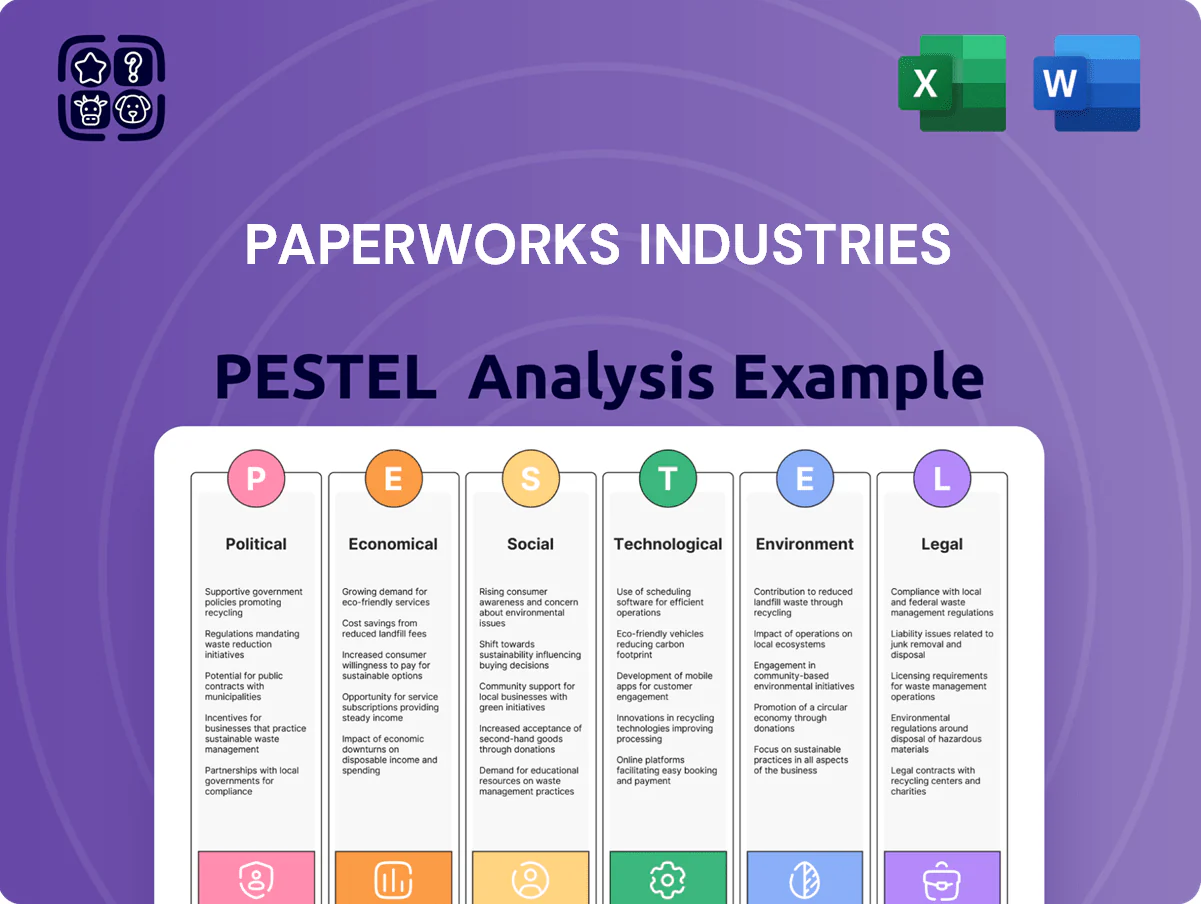

PaperWorks Industries PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our targeted PESTLE Analysis of PaperWorks Industries—uncover how regulatory shifts, market cycles, and sustainability trends are shaping strategic choices and operational risk; buy the full report to access in-depth, actionable insights and ready-to-use slides for investors and planners.

Political factors

Trade tariffs and North American relations

PaperWorks depends on integrated US-Canada supply chains; in 2024 cross-border paper trade between the two totaled about $3.8 billion, exposing the company to tariff risk. Changes to agreements or new tariffs on pulp and paper could raise input costs by an estimated 5–12%, squeezing 2025 EBITDA margins. Strategic planning must incorporate late-2025 geopolitical shifts, including US-Canada trade talks and tariff threat scenarios.

Government subsidies for recycling infrastructure

Federal and state grants and tax incentives grew 28% in 2024, with the EPA and Bipartisan Infrastructure Law directing over $6.5 billion toward recycling and domestic processing; PaperWorks Industries can tap these funds to finance plant upgrades and scale its 100% recycled paperboard lines, potentially offsetting 20–40% of capex per facility; prioritizing grant application processes and compliance-ready reporting is a strategic imperative.

Waste management and circular economy policies

Legislative bodies across the EU and US are tightening circular economy rules, with the EU requiring 30% recycled content in certain packaging by 2030 and several US states adopting similar mandates, boosting demand for PaperWorks Industries’ recycled paperboard now representing ~45% of its sales in 2024.

Political pressure to cut landfill volumes—EU targets to halve municipal waste to 2035 and US landfill diversion goals—increases market pull for the company’s products, supporting a 12% CAGR in recycled-paperboard volumes since 2020.

Maintaining proactive relationships with policymakers has enabled PaperWorks to influence standards and stay ahead of recycling mandates, reducing regulatory risk and preserving gross margins near 18% despite rising compliance costs.

Impact of international forestry agreements

International forestry agreements like the 2023 Global Forest Finance Pledge and ongoing EU Due Diligence rules tighten supply of certified virgin fiber, increasing pulp prices by about 12% in 2024 and boosting recycled fiber demand—benefiting PaperWorks’ recycled-focused margins.

Political instability in key fiber exporters (e.g., 2024 unrest in Indonesia) pushed spot pulp premiums 8–15%, raising recycled alternatives’ relative value and reducing raw-material cost volatility for PaperWorks.

Continuous monitoring of treaty shifts and export-risk indices is essential to sustain PaperWorks’ competitive pricing in packaging, where recycled-content premiums rose ~6% in 2024.

- 2024 pulp price rise ~12% due to stricter global forestry rules

- Spot pulp premiums up 8–15% from regional instability

- Recycled-content pricing advantage increased ~6% in 2024

Corporate tax reforms and industrial policy

Changes in corporate tax rates and investment tax credits for manufacturing directly affect PaperWorks Industries’ capex timing; the US federal corporate tax rate remains 21% with proposed incentives under the 2024 CHIPS+EDA-style packages offering up to 10% ITC for domestic manufacturing equipment.

Political trends toward reshoring—US manufacturing investment rose 8.2% in 2024—favor domestic producers like PaperWorks, improving utilization forecasts and reducing supply-chain risk premiums.

Financial models should embed evolving tax credits and scenario-based capex schedules; a 10% ITC can improve after-tax IRR by 150–300 basis points on typical paper mill projects.

- 21% federal rate; up to 10% manufacturing ITC available

- 2024 US manufacturing investment +8.2%

- 10% ITC → +150–300 bps after-tax IRR uplift

Policy, pulp & reshoring reshuffle 2025 EBITDA ±5–12% and lift IRR 150–300bps

Political shifts (trade/tariffs, incentives, recycling mandates) raised 2024 pulp prices ~12%, spot premiums 8–15%, and recycled-content price edge ~6%; federal corporate rate 21% with up to 10% manufacturing ITC; US reshoring boosted manufacturing investment +8.2% in 2024—these factors can alter 2025 EBITDA by ±5–12% and lift after-tax IRR 150–300 bps.

| Metric | 2024/Impact |

|---|---|

| Pulp price change | +12% |

| Spot premiums | 8–15% |

| Recycled price edge | +6% |

| Fed tax rate | 21% |

| ITC | up to 10% |

| US mfg investment | +8.2% |

What is included in the product

Explores how macro-environmental factors uniquely affect PaperWorks Industries across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify risks and opportunities.

Condenses PaperWorks Industries' PESTLE into a clear, shareable brief that teams can drop into presentations or planning docs for fast alignment on external risks and strategic implications.

Economic factors

Fluctuations in recovered fiber pricing

Recovered fiber accounts for roughly 40–60% of PaperWorks Industries' raw-material cost; US OCC prices swung from about $85/ton in 2020 to peaks near $230/ton in 2021–22 and averaged ~$150/ton in 2024, linking margins to volatile wastepaper markets.

Economic cycles that influence consumer disposal—US municipal solid waste generation fell ~1.5% in 2023 vs 2022—directly alter available supply and push input prices up during rebounds in consumption.

Effective hedging, multi-supplier contracts and inventory optimization reduced fiber-cost volatility exposure by an estimated 10–15% in industry peers; for PaperWorks, similar measures are critical to protect margins.

Energy costs and manufacturing efficiency

Paperboard production is highly energy-intensive, with energy typically comprising 10–20% of operating costs; exposure to US natural gas and industrial electricity price swings (natural gas up ~35% 2021–2023; US industrial electricity ~8% rise 2022–2024) directly pressures margins. Transitioning to renewables can cut long-term energy spend volatility—capex often 5–15% of plant value—but requires sizable upfront investment. Continuous energy-market monitoring is essential to protect margins in a competitive market.

Consumer spending on packaged goods

Demand for folding cartons tracks consumer packaged goods health; US CPG spending rose 2.1% in 2024 after 2023’s 0.8% real decline, affecting packaging volumes reported by Smithers as global corrugated demand up 1.5% in 2024.

Inflationary pressure—US CPI 3.4% in 2024—can compress household discretionary spend, reducing packaging for nonessentials, while food/beverage packaging remained resilient, growing ~3% in 2024.

Diversifying clients across essentials and discretionary reduced PaperWorks-like peers’ revenue volatility; firms with ≥40% essential-packaging mix showed 6–8% higher revenue stability during 2022–24 downturns.

Interest rates and capital investment

The current US prime rate at 8.25% and average commercial loan spreads mean PaperWorks faces borrowing costs often exceeding 9–10%, constraining financing for large-scale equipment upgrades.

At these rates, projected ROI on new converting or paperboard machines can be pushed beyond 5–7 years versus target 3–4 years, delaying productivity gains and cash payback.

Financial teams must model cost of capital (WACC now commonly 9–11% for mid-cap manufacturers) against estimated efficiency improvements of 10–25% before approving capex.

- Borrowing costs ~9–10% for equipment loans

- Typical ROI pushed to 5–7 years vs target 3–4 years

- WACC for mid-cap manufacturing ~9–11%

- Expected efficiency gains 10–25% needed to justify spend

Labor market dynamics and wage inflation

The manufacturing sector faces a 2024 labor shortfall with 900,000+ unfilled US manufacturing jobs and average hourly wage growth of 4.5% year-over-year, pressuring PaperWorks Industries’ margins and scheduling.

Competition for skilled technicians/plant operators drives localized wage premiums up to 10–15%, increasing operating costs and downtime risk.

Capital allocation toward automation (robotics ROI improving; 2023 CAPEX up 6%) and retention programs (reducing turnover by 20–30%) is economically necessary.

- 900,000+ unfilled US manufacturing jobs (2024)

- 4.5% avg hourly wage growth YoY (2024)

- Wage premiums 10–15% for skilled roles

- Automation CAPEX +6% (2023) with 20–30% turnover reduction from retention programs

Packaging resilience offsets input volatility as high rates push automation capex

Volatile recovered-fiber (avg ~$150/ton in 2024) and energy (natural gas +35% 2021–23) drive margin swings; high borrowing costs (prime 8.25%, equipment loans ~9–10%, WACC 9–11%) delay capex payback to 5–7 years; demand resilience concentrated in essentials (food/bev packaging +3% 2024) offsets discretionary weakness; labor shortages (900k+ unfilled, wages +4.5% 2024) push automation CAPEX.

| Metric | 2024 / Range |

|---|---|

| Recovered fiber | ~$150/ton |

| Natural gas change | +35% (2021–23) |

| Prime rate | 8.25% |

| Equipment loan rates | ~9–10% |

| WACC (mid-cap) | 9–11% |

| Food/bev packaging demand | +3% (2024) |

| Unfilled manufacturing jobs | 900,000+ |

Preview the Actual Deliverable

PaperWorks Industries PESTLE Analysis

The preview shown here is the exact PaperWorks Industries PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the downloadable file you’ll get immediately after checkout—no placeholders, no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our targeted PESTLE Analysis of PaperWorks Industries—uncover how regulatory shifts, market cycles, and sustainability trends are shaping strategic choices and operational risk; buy the full report to access in-depth, actionable insights and ready-to-use slides for investors and planners.

Political factors

Trade tariffs and North American relations

PaperWorks depends on integrated US-Canada supply chains; in 2024 cross-border paper trade between the two totaled about $3.8 billion, exposing the company to tariff risk. Changes to agreements or new tariffs on pulp and paper could raise input costs by an estimated 5–12%, squeezing 2025 EBITDA margins. Strategic planning must incorporate late-2025 geopolitical shifts, including US-Canada trade talks and tariff threat scenarios.

Government subsidies for recycling infrastructure

Federal and state grants and tax incentives grew 28% in 2024, with the EPA and Bipartisan Infrastructure Law directing over $6.5 billion toward recycling and domestic processing; PaperWorks Industries can tap these funds to finance plant upgrades and scale its 100% recycled paperboard lines, potentially offsetting 20–40% of capex per facility; prioritizing grant application processes and compliance-ready reporting is a strategic imperative.

Waste management and circular economy policies

Legislative bodies across the EU and US are tightening circular economy rules, with the EU requiring 30% recycled content in certain packaging by 2030 and several US states adopting similar mandates, boosting demand for PaperWorks Industries’ recycled paperboard now representing ~45% of its sales in 2024.

Political pressure to cut landfill volumes—EU targets to halve municipal waste to 2035 and US landfill diversion goals—increases market pull for the company’s products, supporting a 12% CAGR in recycled-paperboard volumes since 2020.

Maintaining proactive relationships with policymakers has enabled PaperWorks to influence standards and stay ahead of recycling mandates, reducing regulatory risk and preserving gross margins near 18% despite rising compliance costs.

Impact of international forestry agreements

International forestry agreements like the 2023 Global Forest Finance Pledge and ongoing EU Due Diligence rules tighten supply of certified virgin fiber, increasing pulp prices by about 12% in 2024 and boosting recycled fiber demand—benefiting PaperWorks’ recycled-focused margins.

Political instability in key fiber exporters (e.g., 2024 unrest in Indonesia) pushed spot pulp premiums 8–15%, raising recycled alternatives’ relative value and reducing raw-material cost volatility for PaperWorks.

Continuous monitoring of treaty shifts and export-risk indices is essential to sustain PaperWorks’ competitive pricing in packaging, where recycled-content premiums rose ~6% in 2024.

- 2024 pulp price rise ~12% due to stricter global forestry rules

- Spot pulp premiums up 8–15% from regional instability

- Recycled-content pricing advantage increased ~6% in 2024

Corporate tax reforms and industrial policy

Changes in corporate tax rates and investment tax credits for manufacturing directly affect PaperWorks Industries’ capex timing; the US federal corporate tax rate remains 21% with proposed incentives under the 2024 CHIPS+EDA-style packages offering up to 10% ITC for domestic manufacturing equipment.

Political trends toward reshoring—US manufacturing investment rose 8.2% in 2024—favor domestic producers like PaperWorks, improving utilization forecasts and reducing supply-chain risk premiums.

Financial models should embed evolving tax credits and scenario-based capex schedules; a 10% ITC can improve after-tax IRR by 150–300 basis points on typical paper mill projects.

- 21% federal rate; up to 10% manufacturing ITC available

- 2024 US manufacturing investment +8.2%

- 10% ITC → +150–300 bps after-tax IRR uplift

Policy, pulp & reshoring reshuffle 2025 EBITDA ±5–12% and lift IRR 150–300bps

Political shifts (trade/tariffs, incentives, recycling mandates) raised 2024 pulp prices ~12%, spot premiums 8–15%, and recycled-content price edge ~6%; federal corporate rate 21% with up to 10% manufacturing ITC; US reshoring boosted manufacturing investment +8.2% in 2024—these factors can alter 2025 EBITDA by ±5–12% and lift after-tax IRR 150–300 bps.

| Metric | 2024/Impact |

|---|---|

| Pulp price change | +12% |

| Spot premiums | 8–15% |

| Recycled price edge | +6% |

| Fed tax rate | 21% |

| ITC | up to 10% |

| US mfg investment | +8.2% |

What is included in the product

Explores how macro-environmental factors uniquely affect PaperWorks Industries across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify risks and opportunities.

Condenses PaperWorks Industries' PESTLE into a clear, shareable brief that teams can drop into presentations or planning docs for fast alignment on external risks and strategic implications.

Economic factors

Fluctuations in recovered fiber pricing

Recovered fiber accounts for roughly 40–60% of PaperWorks Industries' raw-material cost; US OCC prices swung from about $85/ton in 2020 to peaks near $230/ton in 2021–22 and averaged ~$150/ton in 2024, linking margins to volatile wastepaper markets.

Economic cycles that influence consumer disposal—US municipal solid waste generation fell ~1.5% in 2023 vs 2022—directly alter available supply and push input prices up during rebounds in consumption.

Effective hedging, multi-supplier contracts and inventory optimization reduced fiber-cost volatility exposure by an estimated 10–15% in industry peers; for PaperWorks, similar measures are critical to protect margins.

Energy costs and manufacturing efficiency

Paperboard production is highly energy-intensive, with energy typically comprising 10–20% of operating costs; exposure to US natural gas and industrial electricity price swings (natural gas up ~35% 2021–2023; US industrial electricity ~8% rise 2022–2024) directly pressures margins. Transitioning to renewables can cut long-term energy spend volatility—capex often 5–15% of plant value—but requires sizable upfront investment. Continuous energy-market monitoring is essential to protect margins in a competitive market.

Consumer spending on packaged goods

Demand for folding cartons tracks consumer packaged goods health; US CPG spending rose 2.1% in 2024 after 2023’s 0.8% real decline, affecting packaging volumes reported by Smithers as global corrugated demand up 1.5% in 2024.

Inflationary pressure—US CPI 3.4% in 2024—can compress household discretionary spend, reducing packaging for nonessentials, while food/beverage packaging remained resilient, growing ~3% in 2024.

Diversifying clients across essentials and discretionary reduced PaperWorks-like peers’ revenue volatility; firms with ≥40% essential-packaging mix showed 6–8% higher revenue stability during 2022–24 downturns.

Interest rates and capital investment

The current US prime rate at 8.25% and average commercial loan spreads mean PaperWorks faces borrowing costs often exceeding 9–10%, constraining financing for large-scale equipment upgrades.

At these rates, projected ROI on new converting or paperboard machines can be pushed beyond 5–7 years versus target 3–4 years, delaying productivity gains and cash payback.

Financial teams must model cost of capital (WACC now commonly 9–11% for mid-cap manufacturers) against estimated efficiency improvements of 10–25% before approving capex.

- Borrowing costs ~9–10% for equipment loans

- Typical ROI pushed to 5–7 years vs target 3–4 years

- WACC for mid-cap manufacturing ~9–11%

- Expected efficiency gains 10–25% needed to justify spend

Labor market dynamics and wage inflation

The manufacturing sector faces a 2024 labor shortfall with 900,000+ unfilled US manufacturing jobs and average hourly wage growth of 4.5% year-over-year, pressuring PaperWorks Industries’ margins and scheduling.

Competition for skilled technicians/plant operators drives localized wage premiums up to 10–15%, increasing operating costs and downtime risk.

Capital allocation toward automation (robotics ROI improving; 2023 CAPEX up 6%) and retention programs (reducing turnover by 20–30%) is economically necessary.

- 900,000+ unfilled US manufacturing jobs (2024)

- 4.5% avg hourly wage growth YoY (2024)

- Wage premiums 10–15% for skilled roles

- Automation CAPEX +6% (2023) with 20–30% turnover reduction from retention programs

Packaging resilience offsets input volatility as high rates push automation capex

Volatile recovered-fiber (avg ~$150/ton in 2024) and energy (natural gas +35% 2021–23) drive margin swings; high borrowing costs (prime 8.25%, equipment loans ~9–10%, WACC 9–11%) delay capex payback to 5–7 years; demand resilience concentrated in essentials (food/bev packaging +3% 2024) offsets discretionary weakness; labor shortages (900k+ unfilled, wages +4.5% 2024) push automation CAPEX.

| Metric | 2024 / Range |

|---|---|

| Recovered fiber | ~$150/ton |

| Natural gas change | +35% (2021–23) |

| Prime rate | 8.25% |

| Equipment loan rates | ~9–10% |

| WACC (mid-cap) | 9–11% |

| Food/bev packaging demand | +3% (2024) |

| Unfilled manufacturing jobs | 900,000+ |

Preview the Actual Deliverable

PaperWorks Industries PESTLE Analysis

The preview shown here is the exact PaperWorks Industries PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the downloadable file you’ll get immediately after checkout—no placeholders, no surprises.