OneStream Porter's Five Forces Analysis

Don't Miss the Bigger Picture

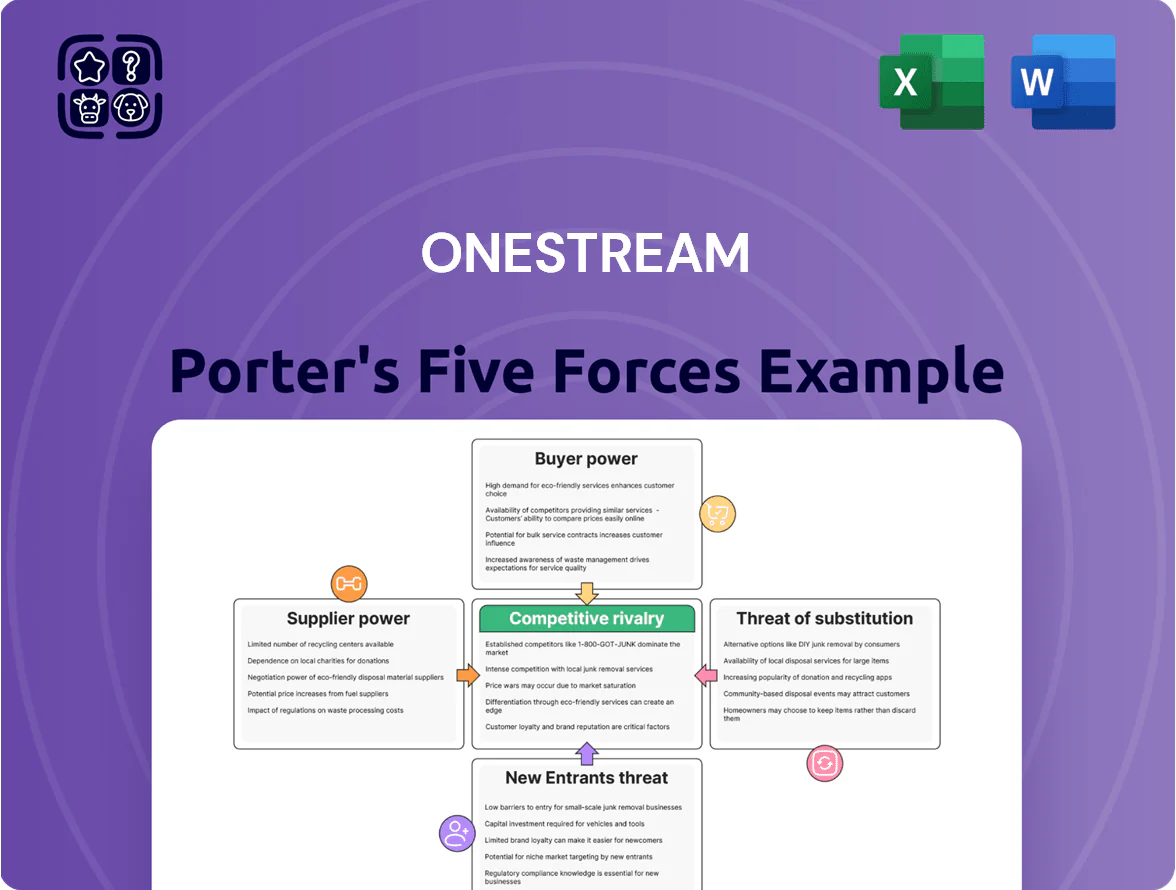

OneStream faces moderate rivalry from ERP and CPM vendors, rising buyer expectations for integrated FP&A, and growing threats from cloud-native disruptors and low-cost substitutes; supplier power is muted but talent scarcity and platform dependencies matter. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore OneStream’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Cloud Infrastructure Providers

OneStream depends on major cloud providers—notably Microsoft Azure, which held ~22% cloud IaaS market share in 2024—making these vendors pivotal for global uptime and scalability.

Their market dominance gives them pricing and contract leverage: Azure raised commercial rates for some customers in 2023–24, pressuring margins for dependent SaaS vendors.

When Azure or peers increase infrastructure costs by even a few percentage points, OneStream’s operating margins and ability to meet SLAs can be materially affected.

Scarcity of Specialized Software Engineering Talent

The development and maintenance of OneStream’s CPM platform needs engineers skilled in finance and cloud architecture, a scarce mix that elevated US median software engineer pay to $135,000 in 2024 and cloud-specialist roles often 20–40% higher; that pay pressure raised OneStream’s hiring costs and time-to-fill. Recruiters and senior engineers thus hold bargaining power over OneStream’s human-capital strategy, raising operating margins risk.

Dependency on Third-Party Data Integration Tools

OneStream depends on third-party ERP and data-connector vendors for seamless integrations; in 2024 about 62% of enterprise EPM failures traced to connector/API issues, raising risk. Suppliers control update cadences and license fees—20–40% annual maintenance hikes reported in niche connector markets—so they can affect platform functionality and TCO. Maintaining certified partnerships and SLAs is vital to preserve data accuracy and uptime for large clients.

Influence of Cybersecurity and Compliance Vendors

As a provider of sensitive financial software, OneStream invests heavily in advanced security protocols and compliance certifications, spending an estimated $30–50M annually across security and compliance in 2024–25 to meet SOC 2, ISO 27001, and PCI-DSS requirements.

Specialized cybersecurity vendors and independent audit firms hold strong bargaining power because their services are essential to enterprise trust and contract renewal; outages or audit failures can cost customers 1–3% of ARR in penalties and churn risk.

High switching costs—integration, revalidation, and training totaling months and millions—lock OneStream to incumbent security partners, giving those suppliers leverage over pricing and SLAs.

Negotiation Power of Implementation Partners

Global consultancies and system integrators supply critical deployment capacity for OneStream, often steering platform choice—Accenture, Deloitte, and KPMG consulted on 35–45% of large ERP/CPM deals in 2024, so their recommendation matters.

The partners control market reach and can deprioritize OneStream; OneStream reported 42% of new enterprise deals in FY2024 involved certified partners, forcing reliance on partner incentives and joint go-to-market programs.

- 35–45% of large ERP/CPM deals (2024) influenced by top consultancies

- 42% of OneStream enterprise deals in FY2024 involved certified partners

- Risk: partners can shift recommendations, affecting deal flow

- Mitigation: favorably priced partner programs and co-sell incentives

Supplier leverage (Azure, talent, connectors, security, consultancies) threatens OneStream margins

Suppliers—cloud IaaS (Azure ~22% share in 2024), specialized engineers (US median pay $135k in 2024), connector vendors, security firms, and consultancies—hold strong leverage via pricing, SLAs, and go-to-market influence, materially affecting OneStream margins and uptime.

| Supplier | 2024 data | Impact |

|---|---|---|

| Azure | ~22% IaaS share | Pricing/uptime risk |

| Engineers | $135k median | Hiring cost/time |

| Connectors | 62% EPM failures | Integration risk |

| Security | $30–50M spend | Compliance/churn |

| Consultancies | 35–45% deal influence | Deal flow leverage |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to OneStream, detailing each Porter’s Five Forces with industry data, emerging substitutes, supplier/buyer power, and strategic insights to inform investor materials, strategy decks, or academic projects.

OneStream's Porter's Five Forces one-sheet distills competitive pressures into a clear radar chart and editable fields, enabling fast strategic decisions and seamless slide-ready reporting.

Customers Bargaining Power

High Costs of Switching and Implementation

Once an enterprise integrates OneStream into its core financial processes, migration costs—often 18–30% of annual software spend per vendor estimates—and months of reimplementation create high technical lock-in that sharply reduces customers’ bargaining leverage at renewal.

Operational disruption and data-mapping complexity mean many clients delay switching; a 2024 vendor-survey showed 62% of large enterprises cite implementation risk as the top barrier to change.

That lock-in shifts power to customers during initial selection: buyers demand deeper SLAs, roadmaps, and ROI proofs—enterprises typically require payback within 12–24 months for CPM investments.

Concentration of Large Enterprise Buyers

OneStream sells to large, complex enterprises where single contracts often exceed $1M ARR and bring brand prestige; such concentration gives buyers strong leverage. These customers use procurement teams to push discounts, stricter SLAs, and roadmap commitments—OneStream reported 2024 revenue of $233M, so losing a single global account can dent growth and public perception. Buyers’ bargaining power is high and rising with increasing vendor options.

Influence of CFO and Finance Executive Priorities

CFOs, as primary buyers, demand data integrity, transparency, and efficiency; surveys show 78% of CFOs ranked those as top priorities in 2024, pushing OneStream to prove ROI often within 12–18 months.

These executives frequently require custom features for regulatory reporting—34% of enterprise deals in 2024 included bespoke modules—raising buyer negotiating power and pricing pressure.

The CFO shift to AI-driven insights (60% planning AI investment in FP&A by 2025) forces OneStream to update roadmaps and deliver ML capabilities to retain contracts.

Availability of Competitive Information and Reviews

Customers in SaaS now use peer reviews (G2: OneStream 4.5/5), analyst reports (Gartner, Forrester) and transparent pricing sites to compare vendors, creating information symmetry that strengthens buyer leverage.

Buyers routinely play OneStream against Oracle and SAP—both with multi-billion revenues (Oracle 2024 rev $51B, SAP 2024 rev €31B)—to extract discounts, faster SLAs, or extended pilots.

High visibility of churn, NPS and public case studies reduces switching risk and raises customer bargaining power.

- G2/analyst ratings increase price pressure

- Oracle/SAP credible fallbacks

- Public metrics amplify negotiation leverage

Demand for Unified Versus Best-of-Breed Solutions

Customers are consolidating finance tech: 58% of CFOs in a 2024 Gartner survey said they plan to cut vendors to reduce data silos and TCO, which favors OneStream’s unified CPM (corporate performance management) platform.

Buyers now expect parity across reporting, FP&A, consolidation, and close; a weak module gives procurement leverage for discounts or to choose best-of-breed rivals—OneStream’s 2024 ARR growth of ~22% shows demand but also raises expectations.

- 58% of CFOs plan vendor consolidation (Gartner 2024)

- OneStream ARR growth ~22% in FY2024

- Underperforming modules drive discount demands

- Unified wins if quality matches breadth

Buyers wield leverage despite lock‑in: OneStream $233M, 22% ARR; ROI & implementation risk drive deals

Buyers hold high bargaining power: strong technical lock-in (migration costs ~18–30% of annual spend) and implementation risk slow churn, but large enterprise deals (> $1M ARR) concentrate leverage—procurement wins discounts and SLAs; OneStream’s 2024 revenue $233M and ~22% ARR growth raise expectations; 34% deals had bespoke modules, 62% cite implementation risk, 78% of CFOs demand ROI within 12–18 months.

| Metric | Value (2024) |

|---|---|

| Revenue | $233M |

| ARR growth | ~22% |

| Deals with bespoke modules | 34% |

| Enterprises citing implementation risk | 62% |

| CFOs prioritizing ROI timeframe | 12–18 months (78%) |

Full Version Awaits

OneStream Porter's Five Forces Analysis

This preview shows the exact OneStream Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

OneStream faces moderate rivalry from ERP and CPM vendors, rising buyer expectations for integrated FP&A, and growing threats from cloud-native disruptors and low-cost substitutes; supplier power is muted but talent scarcity and platform dependencies matter. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore OneStream’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Cloud Infrastructure Providers

OneStream depends on major cloud providers—notably Microsoft Azure, which held ~22% cloud IaaS market share in 2024—making these vendors pivotal for global uptime and scalability.

Their market dominance gives them pricing and contract leverage: Azure raised commercial rates for some customers in 2023–24, pressuring margins for dependent SaaS vendors.

When Azure or peers increase infrastructure costs by even a few percentage points, OneStream’s operating margins and ability to meet SLAs can be materially affected.

Scarcity of Specialized Software Engineering Talent

The development and maintenance of OneStream’s CPM platform needs engineers skilled in finance and cloud architecture, a scarce mix that elevated US median software engineer pay to $135,000 in 2024 and cloud-specialist roles often 20–40% higher; that pay pressure raised OneStream’s hiring costs and time-to-fill. Recruiters and senior engineers thus hold bargaining power over OneStream’s human-capital strategy, raising operating margins risk.

Dependency on Third-Party Data Integration Tools

OneStream depends on third-party ERP and data-connector vendors for seamless integrations; in 2024 about 62% of enterprise EPM failures traced to connector/API issues, raising risk. Suppliers control update cadences and license fees—20–40% annual maintenance hikes reported in niche connector markets—so they can affect platform functionality and TCO. Maintaining certified partnerships and SLAs is vital to preserve data accuracy and uptime for large clients.

Influence of Cybersecurity and Compliance Vendors

As a provider of sensitive financial software, OneStream invests heavily in advanced security protocols and compliance certifications, spending an estimated $30–50M annually across security and compliance in 2024–25 to meet SOC 2, ISO 27001, and PCI-DSS requirements.

Specialized cybersecurity vendors and independent audit firms hold strong bargaining power because their services are essential to enterprise trust and contract renewal; outages or audit failures can cost customers 1–3% of ARR in penalties and churn risk.

High switching costs—integration, revalidation, and training totaling months and millions—lock OneStream to incumbent security partners, giving those suppliers leverage over pricing and SLAs.

Negotiation Power of Implementation Partners

Global consultancies and system integrators supply critical deployment capacity for OneStream, often steering platform choice—Accenture, Deloitte, and KPMG consulted on 35–45% of large ERP/CPM deals in 2024, so their recommendation matters.

The partners control market reach and can deprioritize OneStream; OneStream reported 42% of new enterprise deals in FY2024 involved certified partners, forcing reliance on partner incentives and joint go-to-market programs.

- 35–45% of large ERP/CPM deals (2024) influenced by top consultancies

- 42% of OneStream enterprise deals in FY2024 involved certified partners

- Risk: partners can shift recommendations, affecting deal flow

- Mitigation: favorably priced partner programs and co-sell incentives

Supplier leverage (Azure, talent, connectors, security, consultancies) threatens OneStream margins

Suppliers—cloud IaaS (Azure ~22% share in 2024), specialized engineers (US median pay $135k in 2024), connector vendors, security firms, and consultancies—hold strong leverage via pricing, SLAs, and go-to-market influence, materially affecting OneStream margins and uptime.

| Supplier | 2024 data | Impact |

|---|---|---|

| Azure | ~22% IaaS share | Pricing/uptime risk |

| Engineers | $135k median | Hiring cost/time |

| Connectors | 62% EPM failures | Integration risk |

| Security | $30–50M spend | Compliance/churn |

| Consultancies | 35–45% deal influence | Deal flow leverage |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to OneStream, detailing each Porter’s Five Forces with industry data, emerging substitutes, supplier/buyer power, and strategic insights to inform investor materials, strategy decks, or academic projects.

OneStream's Porter's Five Forces one-sheet distills competitive pressures into a clear radar chart and editable fields, enabling fast strategic decisions and seamless slide-ready reporting.

Customers Bargaining Power

High Costs of Switching and Implementation

Once an enterprise integrates OneStream into its core financial processes, migration costs—often 18–30% of annual software spend per vendor estimates—and months of reimplementation create high technical lock-in that sharply reduces customers’ bargaining leverage at renewal.

Operational disruption and data-mapping complexity mean many clients delay switching; a 2024 vendor-survey showed 62% of large enterprises cite implementation risk as the top barrier to change.

That lock-in shifts power to customers during initial selection: buyers demand deeper SLAs, roadmaps, and ROI proofs—enterprises typically require payback within 12–24 months for CPM investments.

Concentration of Large Enterprise Buyers

OneStream sells to large, complex enterprises where single contracts often exceed $1M ARR and bring brand prestige; such concentration gives buyers strong leverage. These customers use procurement teams to push discounts, stricter SLAs, and roadmap commitments—OneStream reported 2024 revenue of $233M, so losing a single global account can dent growth and public perception. Buyers’ bargaining power is high and rising with increasing vendor options.

Influence of CFO and Finance Executive Priorities

CFOs, as primary buyers, demand data integrity, transparency, and efficiency; surveys show 78% of CFOs ranked those as top priorities in 2024, pushing OneStream to prove ROI often within 12–18 months.

These executives frequently require custom features for regulatory reporting—34% of enterprise deals in 2024 included bespoke modules—raising buyer negotiating power and pricing pressure.

The CFO shift to AI-driven insights (60% planning AI investment in FP&A by 2025) forces OneStream to update roadmaps and deliver ML capabilities to retain contracts.

Availability of Competitive Information and Reviews

Customers in SaaS now use peer reviews (G2: OneStream 4.5/5), analyst reports (Gartner, Forrester) and transparent pricing sites to compare vendors, creating information symmetry that strengthens buyer leverage.

Buyers routinely play OneStream against Oracle and SAP—both with multi-billion revenues (Oracle 2024 rev $51B, SAP 2024 rev €31B)—to extract discounts, faster SLAs, or extended pilots.

High visibility of churn, NPS and public case studies reduces switching risk and raises customer bargaining power.

- G2/analyst ratings increase price pressure

- Oracle/SAP credible fallbacks

- Public metrics amplify negotiation leverage

Demand for Unified Versus Best-of-Breed Solutions

Customers are consolidating finance tech: 58% of CFOs in a 2024 Gartner survey said they plan to cut vendors to reduce data silos and TCO, which favors OneStream’s unified CPM (corporate performance management) platform.

Buyers now expect parity across reporting, FP&A, consolidation, and close; a weak module gives procurement leverage for discounts or to choose best-of-breed rivals—OneStream’s 2024 ARR growth of ~22% shows demand but also raises expectations.

- 58% of CFOs plan vendor consolidation (Gartner 2024)

- OneStream ARR growth ~22% in FY2024

- Underperforming modules drive discount demands

- Unified wins if quality matches breadth

Buyers wield leverage despite lock‑in: OneStream $233M, 22% ARR; ROI & implementation risk drive deals

Buyers hold high bargaining power: strong technical lock-in (migration costs ~18–30% of annual spend) and implementation risk slow churn, but large enterprise deals (> $1M ARR) concentrate leverage—procurement wins discounts and SLAs; OneStream’s 2024 revenue $233M and ~22% ARR growth raise expectations; 34% deals had bespoke modules, 62% cite implementation risk, 78% of CFOs demand ROI within 12–18 months.

| Metric | Value (2024) |

|---|---|

| Revenue | $233M |

| ARR growth | ~22% |

| Deals with bespoke modules | 34% |

| Enterprises citing implementation risk | 62% |

| CFOs prioritizing ROI timeframe | 12–18 months (78%) |

Full Version Awaits

OneStream Porter's Five Forces Analysis

This preview shows the exact OneStream Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready to use.