ONGC PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our concise PESTLE Analysis of ONGC—revealing how political shifts, regulatory pressures, market dynamics, and technology trends shape its outlook; ideal for investors and strategists seeking fast, actionable intelligence. Purchase the full report to access detailed risk assessments, opportunity maps, and editable formats ready for boardrooms and pitch decks.

Political factors

Government Ownership and Strategic Control

As a Maharatna public sector enterprise, ONGC remains a core instrument of India’s energy security, with the government holding ~60.7% stake as of FY2024; state influence shapes strategic priorities and capital allocation. By end-2025, government directives continue to set dividend policy—ONGC paid Rs 27,778 crore in dividends in FY2023—and capex targets aligned to national goals like domestic hydrocarbon self-reliance. Sovereign backing ensures access to policy support and financing but enforces political mandates that can prioritize strategic objectives over pure profit maximization.

Geopolitical Dynamics and Energy Diplomacy

ONGC Videsh Limited (OVL) manages assets in over 20 countries and contributed about 22% of ONGC consolidated crude production in FY2024–25, making it highly sensitive to geopolitical shifts as of late 2025; disruptions in the Middle East or sanctions on partner states could cut overseas output and deferred CAPEX.

Energy Security Mandates and Import Reduction

The Indian government’s push to cut energy imports has intensified pressure on ONGC to raise domestic production, targeting a reduction of oil import dependence from about 82% in 2023 to under 70% by 2025; ONGC is expected to add ~0.2–0.3 mmbpd from new projects. Policies through end-2025 offer fiscal incentives and accelerated bidding for unallocated onshore and deep-water blocks to spur exploration. ONGC’s output and capex execution are closely monitored against self-reliance metrics, influencing its regulatory standing, preferential licensing and access to strategic acreage.

Trade Relations and Global Supply Chains

- India-UAE 2024 energy roadmap impacts JV opportunities

- US LNG exports +12% YoY 2024 alters sourcing

- Oilfield equipment prices +6% in 2024 raises capex risk

- Include political stress-tests in 2025–2030 supply-chain models

Domestic Policy Stability and Fiscal Regime

The stability of the fiscal regime, including production sharing contracts and revenue-sharing models, is critical for ONGC’s capital allocation and exploration timelines; in FY2024 ONGC reported CAPEX of INR 23,000 crore, with planning sensitive to tax predictability.

By late 2025 government decisions on the Windfall Tax and levies on crude production remain central to cash flow projections; a 1% additional levy on oil could reduce annual EBITDA by an estimated INR 2,500–3,000 crore based on 2024 average realizations.

Investors demand policy consistency to mitigate risks from sudden regulatory shifts in the upstream sector, reflected in ONGC’s share volatility around tax announcements—beta of ~1.1 vs Nifty 50 in 2024—affecting financing costs and project IRRs.

- FY2024 CAPEX: INR 23,000 crore

- Estimated EBITDA impact of 1% levy: INR 2,500–3,000 crore

- ONGC beta ~1.1 vs Nifty 50 (2024)

State-led energy play: high dividends, big capex, rising overseas and geopolitical risks

State control (60.7% FY2024) drives strategic priorities, dividends (Rs 27,778 crore FY2023) and capex direction (INR 23,000 crore FY2024); OVL’s ~22% FY2024–25 overseas contribution raises geopolitical exposure; policy pushes to cut oil imports (82% in 2023 → <70% target by 2025) and 2024 India-UAE energy roadmap shape JV/access; 2024: oilfield equipment +6%, US LNG exports +12% YoY.

| Metric | Value |

|---|---|

| Govt stake | 60.7% |

| Dividends FY2023 | Rs 27,778 cr |

| CAPEX FY2024 | INR 23,000 cr |

| OVL output share | ~22% |

| Oil import 2023 | 82% |

| OFE prices 2024 | +6% |

What is included in the product

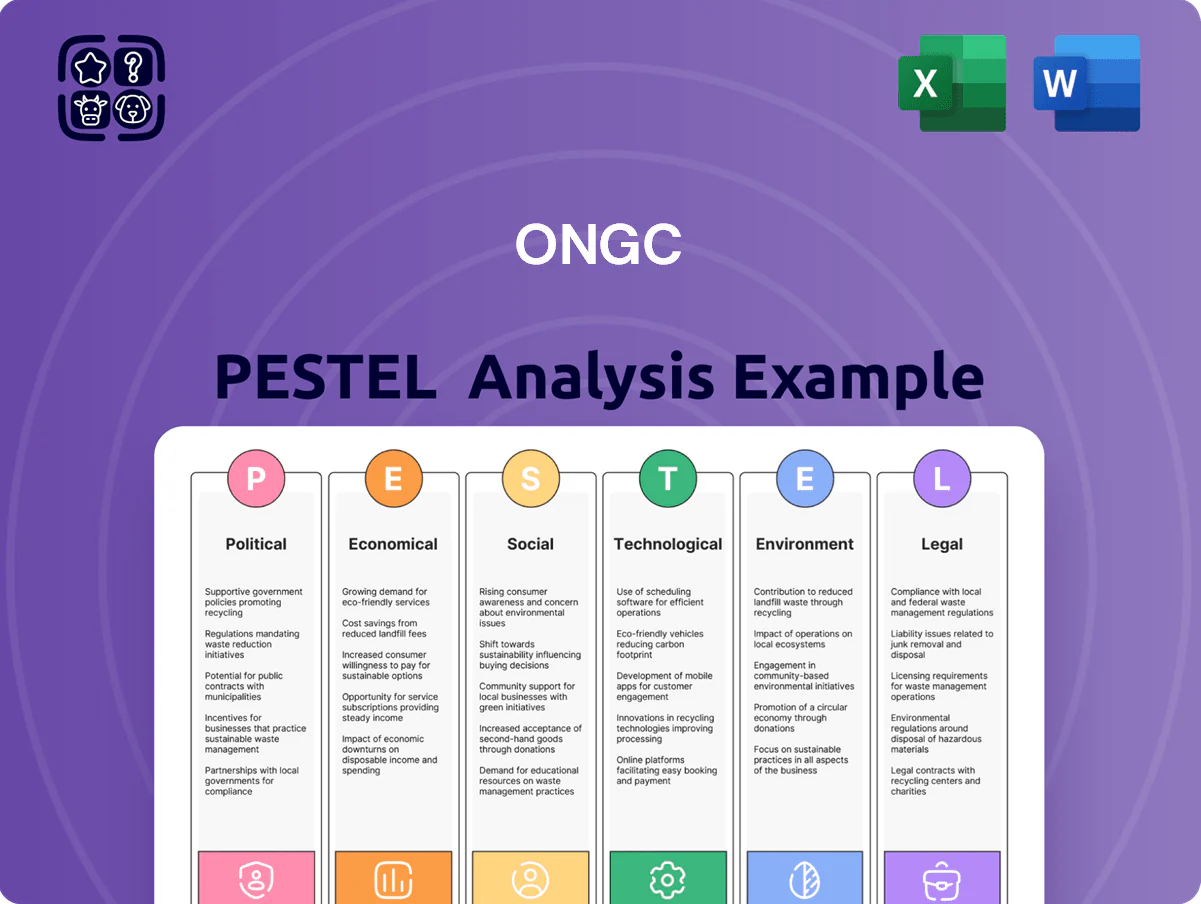

Explores how external macro-environmental factors uniquely affect ONGC across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to identify risks and opportunities for executives, consultants, and investors.

A concise, shareable ONGC PESTLE summary that distills external risks and opportunities into PESTLE categories for quick inclusion in presentations, team alignment, or consultant reports.

Economic factors

Global Crude Oil and Natural Gas Pricing

ONGC's revenue remains highly sensitive to international Brent crude and global gas benchmarks; Brent averaged about 88 USD/bbl in 2024 and traded near 80–90 USD/bbl through Dec 2025, directly affecting realized realizations and EBITDA. Volatility in these markets compresses margins and can render ultradeep and frontier exploration uneconomic given ONGC's lifting costs around 12–18 USD/bbl. Economic recovery in India, China, and OECD countries—global oil demand rose ~1.2 mb/d in 2024—influences price realizations for ONGC's crude and gas output.

Inflationary Pressure and Operating Costs

Rising labor, raw material and specialized oilfield service costs eroded ONGC’s operating margins in 2025, with reported opex per boe up about 12% year-on-year and services inflation near 14% in India’s energy sector.

Currency Exchange Rate Fluctuations

As a company with extensive international operations and about $3.1 billion of foreign currency debt (FY2024), ONGC is exposed to USD/INR swings; INR depreciation (rupee fell ~6% vs USD in 2023–24) raises imported technology and debt servicing costs while boosting INR value of dollar-priced oil revenues. Analysts track net translation and transaction effects to estimate impact on consolidated PAT and hedge needs.

Domestic Economic Growth and Energy Demand

India's GDP grew about 7.3% in FY2023–24 and IMF projects ~6.8% for 2025, underpinning rising domestic energy consumption that directly drives ONGC's sales volumes.

By end-2025, industrial and transport sectors—responsible for roughly 60% of oil demand—will largely determine off-take from ONGC fields and refineries.

A robust economy supports a stable demand floor for crude, natural gas and LPG, aiding ONGC's revenue predictability and asset utilization.

- GDP ~6.8% projected for 2025 (IMF)

- Industry+transport ≈60% of oil demand

- Stronger growth → higher off-take, improved utilization

Capital Market Access and Interest Rates

The Reserve Bank of India policy rate stood at 6.5% in Dec 2025 and global rates remain elevated versus 2021 lows, raising ONGC’s weighted average cost of debt and increasing financing costs for its ~Rs 1.2 trillion capex plan through 2026; higher rates also make refinancing its ~Rs 60,000 crore debt stock more expensive.

- RBI repo: 6.5% (Dec 2025)

- Capex plan: ~Rs 1.2 trillion to 2026

- Debt stock: ~Rs 60,000 crore

- Market access key for refinancing and strategic flexibility

ONGC Outlook: Brent $80–90, lifting cost $12–18, opex +12%, capex Rs1.2tn, debt Rs60kcr

ONGC revenue tied to Brent (~80–90 USD/bbl in 2025) and gas benchmarks; lifting costs ~12–18 USD/bbl; 2024 global oil demand +1.2 mb/d. Opex/boe +12% YoY, services inflation ~14% (2025); FY2024 FX debt $3.1bn; INR fell ~6% 2023–24. India GDP ~6.8% (IMF 2025); RBI repo 6.5% (Dec 2025); capex ~Rs 1.2tn to 2026; debt ~Rs 60,000cr.

| Metric | Value |

|---|---|

| Brent (2025) | 80–90 USD/bbl |

| Lifting cost | 12–18 USD/bbl |

| Opex/boe change (2025) | +12% YoY |

| Services inflation (India) | ~14% |

| FX debt (FY2024) | $3.1bn |

| INR change (2023–24) | -6% vs USD |

| India GDP (2025 IMF) | ~6.8% |

| RBI repo (Dec 2025) | 6.5% |

| Capex to 2026 | ~Rs 1.2tn |

| Debt stock | ~Rs 60,000cr |

Same Document Delivered

ONGC PESTLE Analysis

The preview shown here is the exact ONGC PESTLE document you’ll receive after purchase—fully formatted and ready to use.

The content and structure visible are the same file you’ll download immediately after payment, with no placeholders or teasers.

What you see is the final, professionally structured report, complete with political, economic, social, technological, legal, and environmental analysis for ONGC.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our concise PESTLE Analysis of ONGC—revealing how political shifts, regulatory pressures, market dynamics, and technology trends shape its outlook; ideal for investors and strategists seeking fast, actionable intelligence. Purchase the full report to access detailed risk assessments, opportunity maps, and editable formats ready for boardrooms and pitch decks.

Political factors

Government Ownership and Strategic Control

As a Maharatna public sector enterprise, ONGC remains a core instrument of India’s energy security, with the government holding ~60.7% stake as of FY2024; state influence shapes strategic priorities and capital allocation. By end-2025, government directives continue to set dividend policy—ONGC paid Rs 27,778 crore in dividends in FY2023—and capex targets aligned to national goals like domestic hydrocarbon self-reliance. Sovereign backing ensures access to policy support and financing but enforces political mandates that can prioritize strategic objectives over pure profit maximization.

Geopolitical Dynamics and Energy Diplomacy

ONGC Videsh Limited (OVL) manages assets in over 20 countries and contributed about 22% of ONGC consolidated crude production in FY2024–25, making it highly sensitive to geopolitical shifts as of late 2025; disruptions in the Middle East or sanctions on partner states could cut overseas output and deferred CAPEX.

Energy Security Mandates and Import Reduction

The Indian government’s push to cut energy imports has intensified pressure on ONGC to raise domestic production, targeting a reduction of oil import dependence from about 82% in 2023 to under 70% by 2025; ONGC is expected to add ~0.2–0.3 mmbpd from new projects. Policies through end-2025 offer fiscal incentives and accelerated bidding for unallocated onshore and deep-water blocks to spur exploration. ONGC’s output and capex execution are closely monitored against self-reliance metrics, influencing its regulatory standing, preferential licensing and access to strategic acreage.

Trade Relations and Global Supply Chains

- India-UAE 2024 energy roadmap impacts JV opportunities

- US LNG exports +12% YoY 2024 alters sourcing

- Oilfield equipment prices +6% in 2024 raises capex risk

- Include political stress-tests in 2025–2030 supply-chain models

Domestic Policy Stability and Fiscal Regime

The stability of the fiscal regime, including production sharing contracts and revenue-sharing models, is critical for ONGC’s capital allocation and exploration timelines; in FY2024 ONGC reported CAPEX of INR 23,000 crore, with planning sensitive to tax predictability.

By late 2025 government decisions on the Windfall Tax and levies on crude production remain central to cash flow projections; a 1% additional levy on oil could reduce annual EBITDA by an estimated INR 2,500–3,000 crore based on 2024 average realizations.

Investors demand policy consistency to mitigate risks from sudden regulatory shifts in the upstream sector, reflected in ONGC’s share volatility around tax announcements—beta of ~1.1 vs Nifty 50 in 2024—affecting financing costs and project IRRs.

- FY2024 CAPEX: INR 23,000 crore

- Estimated EBITDA impact of 1% levy: INR 2,500–3,000 crore

- ONGC beta ~1.1 vs Nifty 50 (2024)

State-led energy play: high dividends, big capex, rising overseas and geopolitical risks

State control (60.7% FY2024) drives strategic priorities, dividends (Rs 27,778 crore FY2023) and capex direction (INR 23,000 crore FY2024); OVL’s ~22% FY2024–25 overseas contribution raises geopolitical exposure; policy pushes to cut oil imports (82% in 2023 → <70% target by 2025) and 2024 India-UAE energy roadmap shape JV/access; 2024: oilfield equipment +6%, US LNG exports +12% YoY.

| Metric | Value |

|---|---|

| Govt stake | 60.7% |

| Dividends FY2023 | Rs 27,778 cr |

| CAPEX FY2024 | INR 23,000 cr |

| OVL output share | ~22% |

| Oil import 2023 | 82% |

| OFE prices 2024 | +6% |

What is included in the product

Explores how external macro-environmental factors uniquely affect ONGC across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to identify risks and opportunities for executives, consultants, and investors.

A concise, shareable ONGC PESTLE summary that distills external risks and opportunities into PESTLE categories for quick inclusion in presentations, team alignment, or consultant reports.

Economic factors

Global Crude Oil and Natural Gas Pricing

ONGC's revenue remains highly sensitive to international Brent crude and global gas benchmarks; Brent averaged about 88 USD/bbl in 2024 and traded near 80–90 USD/bbl through Dec 2025, directly affecting realized realizations and EBITDA. Volatility in these markets compresses margins and can render ultradeep and frontier exploration uneconomic given ONGC's lifting costs around 12–18 USD/bbl. Economic recovery in India, China, and OECD countries—global oil demand rose ~1.2 mb/d in 2024—influences price realizations for ONGC's crude and gas output.

Inflationary Pressure and Operating Costs

Rising labor, raw material and specialized oilfield service costs eroded ONGC’s operating margins in 2025, with reported opex per boe up about 12% year-on-year and services inflation near 14% in India’s energy sector.

Currency Exchange Rate Fluctuations

As a company with extensive international operations and about $3.1 billion of foreign currency debt (FY2024), ONGC is exposed to USD/INR swings; INR depreciation (rupee fell ~6% vs USD in 2023–24) raises imported technology and debt servicing costs while boosting INR value of dollar-priced oil revenues. Analysts track net translation and transaction effects to estimate impact on consolidated PAT and hedge needs.

Domestic Economic Growth and Energy Demand

India's GDP grew about 7.3% in FY2023–24 and IMF projects ~6.8% for 2025, underpinning rising domestic energy consumption that directly drives ONGC's sales volumes.

By end-2025, industrial and transport sectors—responsible for roughly 60% of oil demand—will largely determine off-take from ONGC fields and refineries.

A robust economy supports a stable demand floor for crude, natural gas and LPG, aiding ONGC's revenue predictability and asset utilization.

- GDP ~6.8% projected for 2025 (IMF)

- Industry+transport ≈60% of oil demand

- Stronger growth → higher off-take, improved utilization

Capital Market Access and Interest Rates

The Reserve Bank of India policy rate stood at 6.5% in Dec 2025 and global rates remain elevated versus 2021 lows, raising ONGC’s weighted average cost of debt and increasing financing costs for its ~Rs 1.2 trillion capex plan through 2026; higher rates also make refinancing its ~Rs 60,000 crore debt stock more expensive.

- RBI repo: 6.5% (Dec 2025)

- Capex plan: ~Rs 1.2 trillion to 2026

- Debt stock: ~Rs 60,000 crore

- Market access key for refinancing and strategic flexibility

ONGC Outlook: Brent $80–90, lifting cost $12–18, opex +12%, capex Rs1.2tn, debt Rs60kcr

ONGC revenue tied to Brent (~80–90 USD/bbl in 2025) and gas benchmarks; lifting costs ~12–18 USD/bbl; 2024 global oil demand +1.2 mb/d. Opex/boe +12% YoY, services inflation ~14% (2025); FY2024 FX debt $3.1bn; INR fell ~6% 2023–24. India GDP ~6.8% (IMF 2025); RBI repo 6.5% (Dec 2025); capex ~Rs 1.2tn to 2026; debt ~Rs 60,000cr.

| Metric | Value |

|---|---|

| Brent (2025) | 80–90 USD/bbl |

| Lifting cost | 12–18 USD/bbl |

| Opex/boe change (2025) | +12% YoY |

| Services inflation (India) | ~14% |

| FX debt (FY2024) | $3.1bn |

| INR change (2023–24) | -6% vs USD |

| India GDP (2025 IMF) | ~6.8% |

| RBI repo (Dec 2025) | 6.5% |

| Capex to 2026 | ~Rs 1.2tn |

| Debt stock | ~Rs 60,000cr |

Same Document Delivered

ONGC PESTLE Analysis

The preview shown here is the exact ONGC PESTLE document you’ll receive after purchase—fully formatted and ready to use.

The content and structure visible are the same file you’ll download immediately after payment, with no placeholders or teasers.

What you see is the final, professionally structured report, complete with political, economic, social, technological, legal, and environmental analysis for ONGC.