Orion Office REIT Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

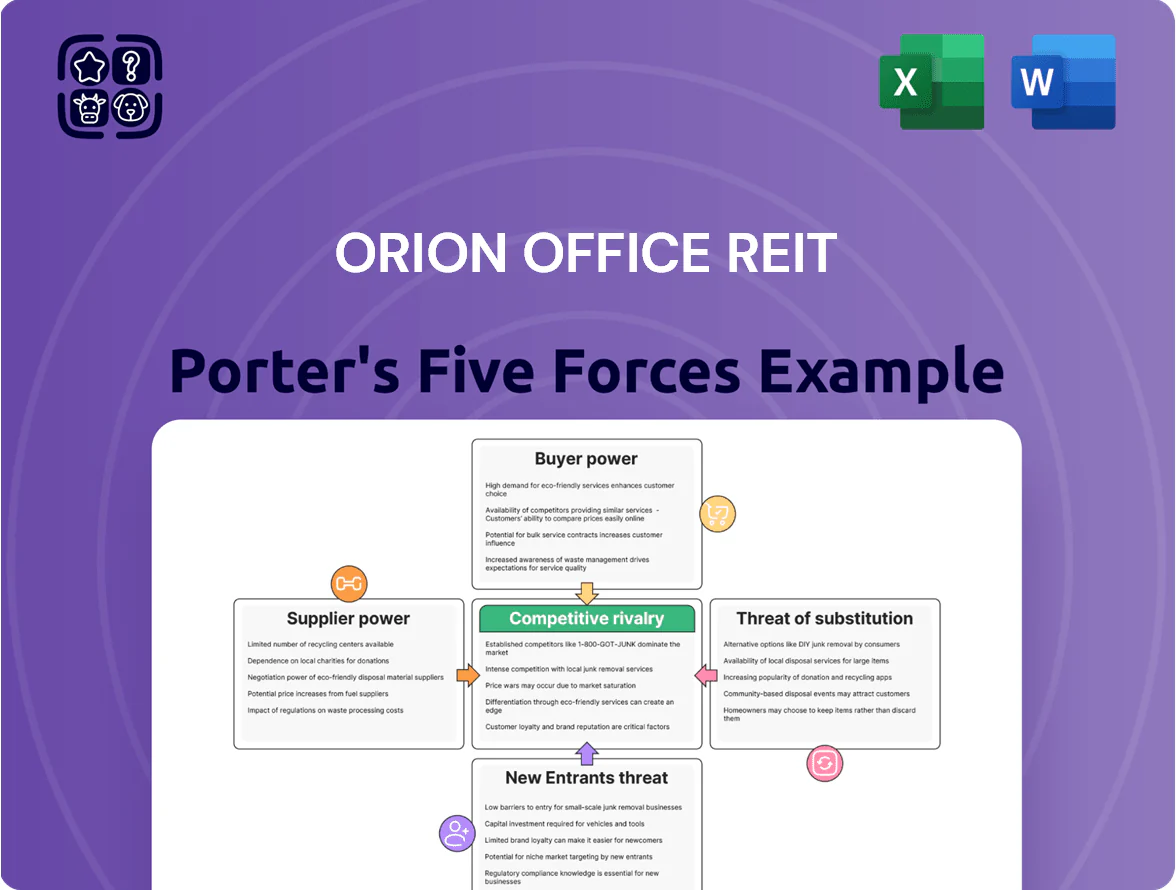

Orion Office REIT faces moderate buyer power amid tenant concentration and rising office vacancies, while supplier and landlord bargaining remains manageable due to long-term leases and specialized property management.

Competitive rivalry is intensifying as hybrid work reshapes demand, and the threat of new entrants is muted by high capital requirements and zoning constraints.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Orion Office REIT’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Debt and Equity Capital

Orion Office REIT depends on banks and capital markets for acquisitions and debt management; as of Q3 2025 its net debt/EBITDA sat near 6.0x, so lenders’ strict underwriting on office assets raises its weighted average cost of capital to roughly 7–8% for new financings.

Maintenance and Property Management Services

As a single-tenant REIT, Orion relies on third-party maintenance, landscaping, and specialty property managers, giving suppliers moderate leverage as regional labor shortages and a 7–12% rise in materials costs in 2025 push service rates higher.

Orion’s negotiation of master service agreements—covering ~85% of its portfolio—directly protects operating expense growth and NOI; a 1% cut in service spend would raise annual NOI by roughly $2.4 million based on Orion’s 2025 pro forma revenue of $240 million.

Utility and Energy Providers

Energy costs are a largely non-negotiable operating expense; in 2024 U.S. commercial electricity rose ~5.2% year-over-year, and local utility monopolies give suppliers strong pricing power that can’t be easily bypassed.

Orion Office REIT is pushing energy-efficiency projects and solar installs; a 10% cut in energy use would lower NOI volatility and offset rising utility rates in markets where utilities raised tariffs by 3–7% in 2023–24.

Under triple-net leases utilities are often passed to tenants, but suppliers still affect expense recoveries and capex timing; in gross-lease buildings higher utility inflation directly compresses landlord margins.

Municipalities and Taxing Authorities

- Municipal control: zoning + permits

- Property tax burden: ~1.2%–2.0% of value

- Assessment volatility: local hikes 8%–12% (2024 examples)

- Orion action: active appeals to defend NOI

Construction and Renovation Contractors

- 2024 contractor bid inflation: 12%–18%

- Suburban construction employment growth: 1.5% (2024)

- Metro construction growth: 3.8% (2024)

- Average contractor backlog: 10–14 weeks (2024)

Suppliers exert moderate-to-strong leverage as costs and taxes squeeze Orion

Suppliers hold moderate-to-strong power over Orion: lenders push financing costs (net debt/EBITDA ~6.0x; WACC ~7–8% for new debt), contractors and service vendors raised costs 7–18% (2024–25), utilities and local governments (property taxes 1.2%–2.0%; local tax hikes 8%–12% in 2024) limit pass-throughs, while 85% MSAs and energy projects partially blunt supplier leverage.

| Metric | Value |

|---|---|

| Net debt/EBITDA | ~6.0x (Q3 2025) |

| WACC (new) | 7–8% |

| Contractor inflation | 12–18% (2024) |

| Property tax rate | 1.2%–2.0% (2024) |

What is included in the product

Concise Porter’s Five Forces analysis tailored to Orion Office REIT, highlighting competitive rivalry, tenant bargaining power, supplier influence, threat of new entrants, and substitutes to inform strategic positioning and risk mitigation.

A concise, one-sheet Porter's Five Forces summary tailored for Orion Office REIT—quickly highlights tenant bargaining power, supply risks, and competitive threats to speed strategic decisions.

Customers Bargaining Power

Large Corporate Tenant Concentration

Orion’s portfolio of mostly single-tenant office assets concentrates risk: in 2025 roughly 65% of cash NOI came from tenants with investment-grade ratings, so a single vacancy can wipe 100% of an asset’s income and force lease-up or heavy downtime costs.

Availability of Alternative Office Space

By end-2025 suburban office vacancy stayed elevated at roughly 22% nationally, so tenants face many relocation options and can compare Orion Office REIT’s Class A and B units directly with competing spaces.

This plentiful supply raises tenant bargaining power, as occupiers leverage market choices to demand higher tenant improvement allowances—often 10–30% of annual rent—or rent concessions.

During renewals tenants commonly push for shorter terms and flexible break clauses; Orion faces pressure to match market concessions seen across peer REITs in 2024–25.

Shift Toward Flexible Lease Structures

Modern corporate tenants demand shorter leases and flexibility for hybrid work; US office lease terms average fell from 7.1 years in 2019 to ~4.3 years in 2024 per CBRE, pressuring Orion Office REIT to shift from long-term net leases toward tenant-friendly, shorter agreements.

Orion must offer concessions—rental abatements, tenant improvement allowances, or amenity upgrades—to secure multi-year deals; concessions rose ~18% industry-wide in 2023, raising leasing costs and compressing stabilized NOI for REIT investors.

Credit Quality and Financial Health of Tenants

Orion targets investment-grade tenants, but their strong credit gives them leverage to push for lower base rents or capped escalations; Moody’s and S&P investment-grade firms had default rates of 0.2% in 2024, so landlords pay a premium to secure them.

Large tenants often self-insure or run in-house facilities teams, reducing Orion’s operational role and bargaining power on service fees and capital improvements.

- 0.2% IG default rate (2024)

- Lower base rents negotiated

- Capped escalations common

- Self-insurance cuts landlord leverage

Impact of Hybrid and Remote Work Trends

Tenants are downsizing as hybrid work becomes permanent, cutting office footprints by 20–40% on renewals; CBRE reported in 2024 that net absorption of US office space was -50 million sq ft, pressuring landlords.

With major leases maturing in 2025–26, many clients renew for a fraction of prior space, letting tenants demand lower rents, higher concessions, and flexible terms while Orion fights to keep occupancy.

Orion under tenant pressure: 65% single-tenant NOI, rising concessions, shorter leases

Orion faces high tenant bargaining power: 65% cash NOI from single tenants (2025), national suburban vacancy ~22% (end-2025), and CBRE 2024 net absorption -50M sq ft. Tenants demand 10–30% TI allowances, concessions +18% (2023), and shorten leases to ~4.3 years (2024), forcing Orion to offer abatements and lower base rents to retain occupancy.

| Metric | Value |

|---|---|

| Concentration (cash NOI) | 65% single-tenant (2025) |

| Suburban vacancy | ~22% (end-2025) |

| Net absorption | -50M sq ft (2024) |

| TI allowances | 10–30% of annual rent |

| Concessions change | +18% (2023) |

| Avg lease term | 4.3 yrs (2024) |

Same Document Delivered

Orion Office REIT Porter's Five Forces Analysis

This preview shows the exact Orion Office REIT Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same fully formatted, professionally written file available for instant download once you complete payment.

No mockups or samples: the content, structure, and recommendations you see are precisely what you'll get, ready for immediate use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Orion Office REIT faces moderate buyer power amid tenant concentration and rising office vacancies, while supplier and landlord bargaining remains manageable due to long-term leases and specialized property management.

Competitive rivalry is intensifying as hybrid work reshapes demand, and the threat of new entrants is muted by high capital requirements and zoning constraints.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Orion Office REIT’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Debt and Equity Capital

Orion Office REIT depends on banks and capital markets for acquisitions and debt management; as of Q3 2025 its net debt/EBITDA sat near 6.0x, so lenders’ strict underwriting on office assets raises its weighted average cost of capital to roughly 7–8% for new financings.

Maintenance and Property Management Services

As a single-tenant REIT, Orion relies on third-party maintenance, landscaping, and specialty property managers, giving suppliers moderate leverage as regional labor shortages and a 7–12% rise in materials costs in 2025 push service rates higher.

Orion’s negotiation of master service agreements—covering ~85% of its portfolio—directly protects operating expense growth and NOI; a 1% cut in service spend would raise annual NOI by roughly $2.4 million based on Orion’s 2025 pro forma revenue of $240 million.

Utility and Energy Providers

Energy costs are a largely non-negotiable operating expense; in 2024 U.S. commercial electricity rose ~5.2% year-over-year, and local utility monopolies give suppliers strong pricing power that can’t be easily bypassed.

Orion Office REIT is pushing energy-efficiency projects and solar installs; a 10% cut in energy use would lower NOI volatility and offset rising utility rates in markets where utilities raised tariffs by 3–7% in 2023–24.

Under triple-net leases utilities are often passed to tenants, but suppliers still affect expense recoveries and capex timing; in gross-lease buildings higher utility inflation directly compresses landlord margins.

Municipalities and Taxing Authorities

- Municipal control: zoning + permits

- Property tax burden: ~1.2%–2.0% of value

- Assessment volatility: local hikes 8%–12% (2024 examples)

- Orion action: active appeals to defend NOI

Construction and Renovation Contractors

- 2024 contractor bid inflation: 12%–18%

- Suburban construction employment growth: 1.5% (2024)

- Metro construction growth: 3.8% (2024)

- Average contractor backlog: 10–14 weeks (2024)

Suppliers exert moderate-to-strong leverage as costs and taxes squeeze Orion

Suppliers hold moderate-to-strong power over Orion: lenders push financing costs (net debt/EBITDA ~6.0x; WACC ~7–8% for new debt), contractors and service vendors raised costs 7–18% (2024–25), utilities and local governments (property taxes 1.2%–2.0%; local tax hikes 8%–12% in 2024) limit pass-throughs, while 85% MSAs and energy projects partially blunt supplier leverage.

| Metric | Value |

|---|---|

| Net debt/EBITDA | ~6.0x (Q3 2025) |

| WACC (new) | 7–8% |

| Contractor inflation | 12–18% (2024) |

| Property tax rate | 1.2%–2.0% (2024) |

What is included in the product

Concise Porter’s Five Forces analysis tailored to Orion Office REIT, highlighting competitive rivalry, tenant bargaining power, supplier influence, threat of new entrants, and substitutes to inform strategic positioning and risk mitigation.

A concise, one-sheet Porter's Five Forces summary tailored for Orion Office REIT—quickly highlights tenant bargaining power, supply risks, and competitive threats to speed strategic decisions.

Customers Bargaining Power

Large Corporate Tenant Concentration

Orion’s portfolio of mostly single-tenant office assets concentrates risk: in 2025 roughly 65% of cash NOI came from tenants with investment-grade ratings, so a single vacancy can wipe 100% of an asset’s income and force lease-up or heavy downtime costs.

Availability of Alternative Office Space

By end-2025 suburban office vacancy stayed elevated at roughly 22% nationally, so tenants face many relocation options and can compare Orion Office REIT’s Class A and B units directly with competing spaces.

This plentiful supply raises tenant bargaining power, as occupiers leverage market choices to demand higher tenant improvement allowances—often 10–30% of annual rent—or rent concessions.

During renewals tenants commonly push for shorter terms and flexible break clauses; Orion faces pressure to match market concessions seen across peer REITs in 2024–25.

Shift Toward Flexible Lease Structures

Modern corporate tenants demand shorter leases and flexibility for hybrid work; US office lease terms average fell from 7.1 years in 2019 to ~4.3 years in 2024 per CBRE, pressuring Orion Office REIT to shift from long-term net leases toward tenant-friendly, shorter agreements.

Orion must offer concessions—rental abatements, tenant improvement allowances, or amenity upgrades—to secure multi-year deals; concessions rose ~18% industry-wide in 2023, raising leasing costs and compressing stabilized NOI for REIT investors.

Credit Quality and Financial Health of Tenants

Orion targets investment-grade tenants, but their strong credit gives them leverage to push for lower base rents or capped escalations; Moody’s and S&P investment-grade firms had default rates of 0.2% in 2024, so landlords pay a premium to secure them.

Large tenants often self-insure or run in-house facilities teams, reducing Orion’s operational role and bargaining power on service fees and capital improvements.

- 0.2% IG default rate (2024)

- Lower base rents negotiated

- Capped escalations common

- Self-insurance cuts landlord leverage

Impact of Hybrid and Remote Work Trends

Tenants are downsizing as hybrid work becomes permanent, cutting office footprints by 20–40% on renewals; CBRE reported in 2024 that net absorption of US office space was -50 million sq ft, pressuring landlords.

With major leases maturing in 2025–26, many clients renew for a fraction of prior space, letting tenants demand lower rents, higher concessions, and flexible terms while Orion fights to keep occupancy.

Orion under tenant pressure: 65% single-tenant NOI, rising concessions, shorter leases

Orion faces high tenant bargaining power: 65% cash NOI from single tenants (2025), national suburban vacancy ~22% (end-2025), and CBRE 2024 net absorption -50M sq ft. Tenants demand 10–30% TI allowances, concessions +18% (2023), and shorten leases to ~4.3 years (2024), forcing Orion to offer abatements and lower base rents to retain occupancy.

| Metric | Value |

|---|---|

| Concentration (cash NOI) | 65% single-tenant (2025) |

| Suburban vacancy | ~22% (end-2025) |

| Net absorption | -50M sq ft (2024) |

| TI allowances | 10–30% of annual rent |

| Concessions change | +18% (2023) |

| Avg lease term | 4.3 yrs (2024) |

Same Document Delivered

Orion Office REIT Porter's Five Forces Analysis

This preview shows the exact Orion Office REIT Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same fully formatted, professionally written file available for instant download once you complete payment.

No mockups or samples: the content, structure, and recommendations you see are precisely what you'll get, ready for immediate use.