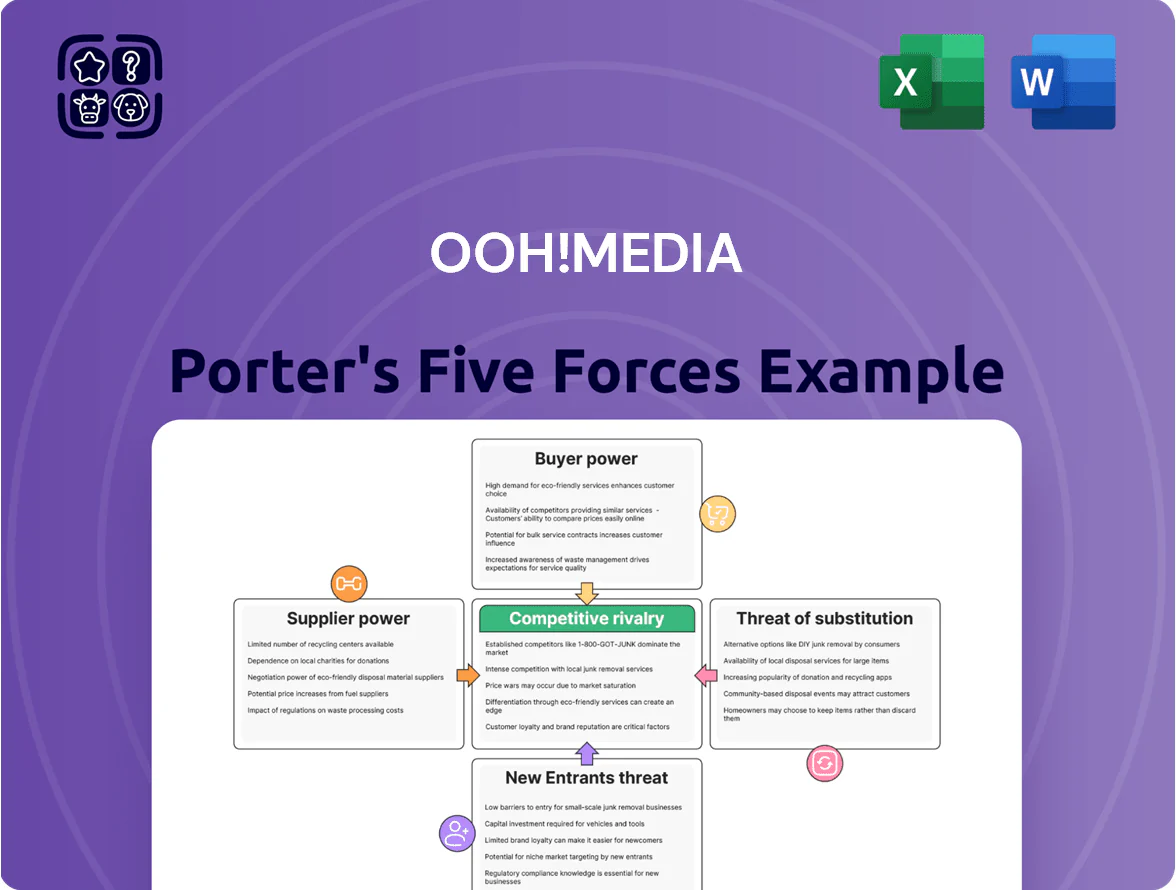

oOh!media Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

oOh!media faces intense buyer scrutiny and evolving ad-tech substitutes, while supplier and new-entrant pressures remain moderate amid high location-specific value; regulatory and digital disruption heighten overall industry rivalry. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore oOh!media’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Key Site Partners

Large site partners like Scentre Group (owner of Westfield centers) and major airports control premium placements that oOh!media cannot easily replace; Scentre reported A$1.9bn net assets at 30 Sep 2024 and Australian airports handled ~110 million pax in 2023, concentration that boosts supplier leverage.

Landlords often push high rents or revenue-share deals—renewal negotiations in 2024 saw billboard landlords seek increases of 5–15%—so oOh!media must keep strong ties with a few dominant partners to preserve its national network.

Scarcity of Premium Digital Real Estate

Local zoning and planning cap premium digital billboards, making high-traffic sites scarce; in Sydney and Melbourne prime street-front spots declined ~12% from 2018–2023 due to tighter permits, shrinking available inventory for oOh!media. Site owners—city councils and large landlords—thus set higher rents and tougher contract terms because few alternatives match weekly reach of 500k+ viewers, boosting supplier bargaining power and compressing margin flexibility for oOh!media.

Specialized Technology and Hardware Providers

As the industry shifts to high-resolution programmatic digital screens, oOh!media depends on a few global manufacturers (Samsung, LG, and Scala partners), concentrating supplier power as 60–70% of premium digital panels use these vendors’ hardware.

High switching costs for custom hardware and integrated CMS software give suppliers moderate pricing leverage; replacing a network can cost tens of millions AUD and disrupt revenue streams.

Ongoing maintenance and quarterly software updates create long-term technical dependence, with annual support contracts often 8–12% of initial hardware spend.

Government and Municipal Council Influence

Local councils award long-term, tightly regulated tenders for street furniture and transit ads, giving them high supplier power over oOh!media; councils can change contract terms or environmental specs during bidding, altering project economics.

Losing a major council contract can cut regional market share sharply—example: a single NSW council loss could remove ~8–12% of urban revenue; public-sector ad spend was A$1.1bn in 2024, so contract shifts matter to cash flow.

- Councils set terms, high bargaining power

- Tender changes shift margins and costs

- One major contract loss ≈ 8–12% regional revenue hit

- Public ad spend A$1.1bn (2024)

Energy and Connectivity Costs

oOh!media runs a large digital OOH (out-of-home) network that needs heavy electricity and high-speed data to update content in real time; FY2024 energy spend for Australian digital publishers rose ~12% YoY, squeezing margins.

Multiple utility and telco providers exist, but energy and bandwidth are essential inputs with limited price bargaining as national rates and global oil/gas trends set baseline costs.

Here’s the quick math and risks:

- Digital sites: higher energy intensity — ~10–15% of site OpEx

- Bandwidth: rising with 4K/interactive ads — +20% data use/year

- Price exposure: linked to national tariffs and LNG/gas prices

Supplier Concentration Risks: 8–12% Revenue Hit, 60–70% Panel Share, Costs Rising

Suppliers hold high leverage: few landlords (Westfield, airports) and councils control premium sites—loss of one major contract can cut 8–12% regional revenue; hardware/software vendors (Samsung, LG, Scala) supply 60–70% premium panels, and annual support equals 8–12% of capex; FY2024 energy up ~12% YoY; public ad spend A$1.1bn (2024).

| Metric | Value |

|---|---|

| Public ad spend (2024) | A$1.1bn |

| Panel vendor share | 60–70% |

| Contract loss impact | 8–12% regional rev |

| Support cost | 8–12% capex |

| Energy change FY2024 | +12% YoY |

What is included in the product

Tailored exclusively for oOh!media, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and disruptive threats shaping its market position.

A concise Porter's Five Forces snapshot for oOh!media—quickly assess competitive intensity and revenue risks at a glance to speed boardroom decisions.

Customers Bargaining Power

Dominance of Media Buying Agencies

A few global media-agency holding groups control roughly 60–70% of ad budgets for blue-chip advertisers, consolidating scale that secures volume discounts and net-60+ payment terms; this concentration raises buyer power against suppliers like oOh!media. oOh!media must compete on price, audience guarantees, and creative integrations to get onto agency preferred-partner lists during annual reviews. In 2024 oOh!media reported weaker CPMs where agency-led buys dominated, squeezing margins.

Low Switching Costs for Advertisers

Brands can shift ad spend from Out of Home to digital channels like Meta and Google quickly; global digital ad spend rose to US$517bn in 2023 and marketers reallocated ~10–15% annually toward performance channels, reducing oOh!media’s bargaining power.

Most OOH buys are campaign-based with no long-term lock-in; FY2024 oOh!media reported ~60% revenue from short-term campaigns, so buyers can exit after flights end.

This flexibility forces customers to demand tighter KPIs and lower CPMs; urban street-site CPMs fell ~5–8% in 2023 amid competitive pressure.

Demand for Real-Time Data and Attribution

Advertisers now demand real-time attribution: 68% of global marketers in 2024 said ROI proof is a top buying criterion, so oOh!media risks clients shifting spend if it lags digital platforms' granularity. If oOh! cannot match impression-level targeting and conversion metrics, buyers gain leverage to push for price cuts or bonus inventory, squeezing oOh!'s gross margins. In Australia digital OOH programmatic growth of 24% in 2024 raises buyer options, increasing customer bargaining power.

Price Sensitivity in Economic Downturns

During high inflation and weak consumer confidence in 2024–25, Australian firms cut marketing first; IAB Australia reported digital ad spend growth slowed to 1.2% in H1 2025, pushing clients toward cheaper local options and raising price sensitivity.

oOh!media must use discounts, short-term buys, and flexible CPMs to keep digital and classic billboard occupancy near its 2024 average of ~78% and protect revenue.

- Marketing cuts hit first — ad spend growth fell to 1.2% H1 2025

- Clients shift to local, lower-cost channels

- oOh!media occupancy target ~78% (2024)

- Incentives and flexible CPMs used to retain demand

Availability of Programmatic Buying

The rise of programmatic trading in Out of Home (OOH) lets advertisers buy oOh!media inventory automatically and with finer targeting, cutting the need for long-term upfront deals and increasing buyer control.

Programmatic increases price transparency and cross-network competition; industry data shows programmatic OOH spend grew ~45% YoY to US$1.1bn globally in 2024, pressuring CPMs and margins for legacy sellers like oOh!media.

- Buyers gain timing/location control

- Programmatic reduces upfront commitments

- Higher price transparency raises competition

- 2024 programmatic OOH spend ~US$1.1bn (+45% YoY)

Agency power, programmatic surge: oOh! cuts CPMs to defend 78% occupancy

Buyers hold strong leverage: agency holding groups control ~60–70% of blue‑chip budgets and demand lower CPMs, real‑time attribution, and short campaigns (oOh! FY2024 ~60% campaign revenue), while programmatic OOH spend rose ~45% YoY to US$1.1bn in 2024, increasing price transparency and switching. oOh! uses discounts and flexible CPMs to keep occupancy near 78% (2024) amid slow ad growth (IAB Australia H1 2025 +1.2%).

| Metric | Value |

|---|---|

| Agency share of blue‑chip budgets | 60–70% |

| oOh! campaign revenue (FY2024) | ~60% |

| oOh! occupancy (2024) | ~78% |

| Programmatic OOH spend (2024) | US$1.1bn (+45% YoY) |

| Australia ad growth (H1 2025) | +1.2% |

Same Document Delivered

oOh!media Porter's Five Forces Analysis

This preview shows the exact oOh!media Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed is the same professionally written, fully formatted file you'll be able to download and use the moment you buy.

No mockups or samples—this is the final deliverable, ready for immediate use without customization.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

oOh!media faces intense buyer scrutiny and evolving ad-tech substitutes, while supplier and new-entrant pressures remain moderate amid high location-specific value; regulatory and digital disruption heighten overall industry rivalry. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore oOh!media’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Key Site Partners

Large site partners like Scentre Group (owner of Westfield centers) and major airports control premium placements that oOh!media cannot easily replace; Scentre reported A$1.9bn net assets at 30 Sep 2024 and Australian airports handled ~110 million pax in 2023, concentration that boosts supplier leverage.

Landlords often push high rents or revenue-share deals—renewal negotiations in 2024 saw billboard landlords seek increases of 5–15%—so oOh!media must keep strong ties with a few dominant partners to preserve its national network.

Scarcity of Premium Digital Real Estate

Local zoning and planning cap premium digital billboards, making high-traffic sites scarce; in Sydney and Melbourne prime street-front spots declined ~12% from 2018–2023 due to tighter permits, shrinking available inventory for oOh!media. Site owners—city councils and large landlords—thus set higher rents and tougher contract terms because few alternatives match weekly reach of 500k+ viewers, boosting supplier bargaining power and compressing margin flexibility for oOh!media.

Specialized Technology and Hardware Providers

As the industry shifts to high-resolution programmatic digital screens, oOh!media depends on a few global manufacturers (Samsung, LG, and Scala partners), concentrating supplier power as 60–70% of premium digital panels use these vendors’ hardware.

High switching costs for custom hardware and integrated CMS software give suppliers moderate pricing leverage; replacing a network can cost tens of millions AUD and disrupt revenue streams.

Ongoing maintenance and quarterly software updates create long-term technical dependence, with annual support contracts often 8–12% of initial hardware spend.

Government and Municipal Council Influence

Local councils award long-term, tightly regulated tenders for street furniture and transit ads, giving them high supplier power over oOh!media; councils can change contract terms or environmental specs during bidding, altering project economics.

Losing a major council contract can cut regional market share sharply—example: a single NSW council loss could remove ~8–12% of urban revenue; public-sector ad spend was A$1.1bn in 2024, so contract shifts matter to cash flow.

- Councils set terms, high bargaining power

- Tender changes shift margins and costs

- One major contract loss ≈ 8–12% regional revenue hit

- Public ad spend A$1.1bn (2024)

Energy and Connectivity Costs

oOh!media runs a large digital OOH (out-of-home) network that needs heavy electricity and high-speed data to update content in real time; FY2024 energy spend for Australian digital publishers rose ~12% YoY, squeezing margins.

Multiple utility and telco providers exist, but energy and bandwidth are essential inputs with limited price bargaining as national rates and global oil/gas trends set baseline costs.

Here’s the quick math and risks:

- Digital sites: higher energy intensity — ~10–15% of site OpEx

- Bandwidth: rising with 4K/interactive ads — +20% data use/year

- Price exposure: linked to national tariffs and LNG/gas prices

Supplier Concentration Risks: 8–12% Revenue Hit, 60–70% Panel Share, Costs Rising

Suppliers hold high leverage: few landlords (Westfield, airports) and councils control premium sites—loss of one major contract can cut 8–12% regional revenue; hardware/software vendors (Samsung, LG, Scala) supply 60–70% premium panels, and annual support equals 8–12% of capex; FY2024 energy up ~12% YoY; public ad spend A$1.1bn (2024).

| Metric | Value |

|---|---|

| Public ad spend (2024) | A$1.1bn |

| Panel vendor share | 60–70% |

| Contract loss impact | 8–12% regional rev |

| Support cost | 8–12% capex |

| Energy change FY2024 | +12% YoY |

What is included in the product

Tailored exclusively for oOh!media, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and disruptive threats shaping its market position.

A concise Porter's Five Forces snapshot for oOh!media—quickly assess competitive intensity and revenue risks at a glance to speed boardroom decisions.

Customers Bargaining Power

Dominance of Media Buying Agencies

A few global media-agency holding groups control roughly 60–70% of ad budgets for blue-chip advertisers, consolidating scale that secures volume discounts and net-60+ payment terms; this concentration raises buyer power against suppliers like oOh!media. oOh!media must compete on price, audience guarantees, and creative integrations to get onto agency preferred-partner lists during annual reviews. In 2024 oOh!media reported weaker CPMs where agency-led buys dominated, squeezing margins.

Low Switching Costs for Advertisers

Brands can shift ad spend from Out of Home to digital channels like Meta and Google quickly; global digital ad spend rose to US$517bn in 2023 and marketers reallocated ~10–15% annually toward performance channels, reducing oOh!media’s bargaining power.

Most OOH buys are campaign-based with no long-term lock-in; FY2024 oOh!media reported ~60% revenue from short-term campaigns, so buyers can exit after flights end.

This flexibility forces customers to demand tighter KPIs and lower CPMs; urban street-site CPMs fell ~5–8% in 2023 amid competitive pressure.

Demand for Real-Time Data and Attribution

Advertisers now demand real-time attribution: 68% of global marketers in 2024 said ROI proof is a top buying criterion, so oOh!media risks clients shifting spend if it lags digital platforms' granularity. If oOh! cannot match impression-level targeting and conversion metrics, buyers gain leverage to push for price cuts or bonus inventory, squeezing oOh!'s gross margins. In Australia digital OOH programmatic growth of 24% in 2024 raises buyer options, increasing customer bargaining power.

Price Sensitivity in Economic Downturns

During high inflation and weak consumer confidence in 2024–25, Australian firms cut marketing first; IAB Australia reported digital ad spend growth slowed to 1.2% in H1 2025, pushing clients toward cheaper local options and raising price sensitivity.

oOh!media must use discounts, short-term buys, and flexible CPMs to keep digital and classic billboard occupancy near its 2024 average of ~78% and protect revenue.

- Marketing cuts hit first — ad spend growth fell to 1.2% H1 2025

- Clients shift to local, lower-cost channels

- oOh!media occupancy target ~78% (2024)

- Incentives and flexible CPMs used to retain demand

Availability of Programmatic Buying

The rise of programmatic trading in Out of Home (OOH) lets advertisers buy oOh!media inventory automatically and with finer targeting, cutting the need for long-term upfront deals and increasing buyer control.

Programmatic increases price transparency and cross-network competition; industry data shows programmatic OOH spend grew ~45% YoY to US$1.1bn globally in 2024, pressuring CPMs and margins for legacy sellers like oOh!media.

- Buyers gain timing/location control

- Programmatic reduces upfront commitments

- Higher price transparency raises competition

- 2024 programmatic OOH spend ~US$1.1bn (+45% YoY)

Agency power, programmatic surge: oOh! cuts CPMs to defend 78% occupancy

Buyers hold strong leverage: agency holding groups control ~60–70% of blue‑chip budgets and demand lower CPMs, real‑time attribution, and short campaigns (oOh! FY2024 ~60% campaign revenue), while programmatic OOH spend rose ~45% YoY to US$1.1bn in 2024, increasing price transparency and switching. oOh! uses discounts and flexible CPMs to keep occupancy near 78% (2024) amid slow ad growth (IAB Australia H1 2025 +1.2%).

| Metric | Value |

|---|---|

| Agency share of blue‑chip budgets | 60–70% |

| oOh! campaign revenue (FY2024) | ~60% |

| oOh! occupancy (2024) | ~78% |

| Programmatic OOH spend (2024) | US$1.1bn (+45% YoY) |

| Australia ad growth (H1 2025) | +1.2% |

Same Document Delivered

oOh!media Porter's Five Forces Analysis

This preview shows the exact oOh!media Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed is the same professionally written, fully formatted file you'll be able to download and use the moment you buy.

No mockups or samples—this is the final deliverable, ready for immediate use without customization.