oOh!media SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

oOh!media leverages extensive OOH inventory and strong advertiser relationships to capture urban audiences, but faces digital competition and ad-spend cyclicality that pressure margins and growth.

Our full SWOT analysis unpacks strategic opportunities in programmatic OOH, revenue diversification paths, and regulatory risks with data-driven insights and financial context.

Purchase the complete report to receive an editable Word and Excel package—ready for investor decks, strategic planning, or competitive benchmarking.

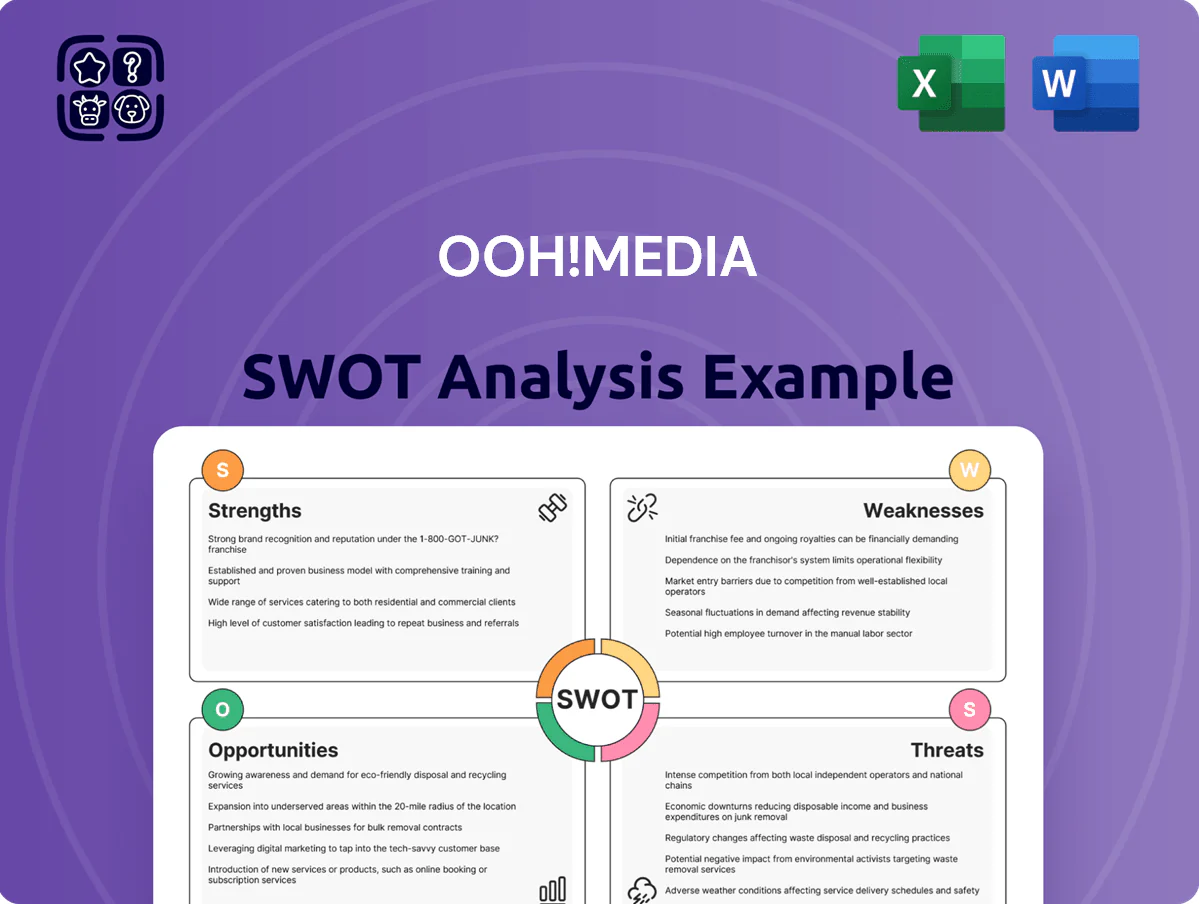

Strengths

Dominant Market Position

oOh!media remains Australia’s leading Out of Home (OOH) provider, with a 2025- end network spanning over 70,000 sites across metro and regional markets, delivering reach into 95% of the Australian population and creating a durable competitive moat versus smaller owners.

Multi-Format Asset Diversity

oOh!media runs a broad asset mix—large-format billboards, retail networks, airports, office towers and rail—reducing concentration risk across mobility shifts; FY2024 revenue mix showed ~32% from out-of-home billboards, 28% retail/instore, 18% transport (air/rail) and 22% place-based/venue assets (oOh!media FY2024 report, Aug 2024).

Advanced Digital Integration

Data-Driven Audience Insights

oOh!media uses MOVE 2.0 and proprietary data platforms to deliver audience granularity—segmenting reach by time, location, and purchase behavior to clients; MOVE 2.0 adoption reached industry standard in 2024 with 78% of national DOOH campaigns measured.

They combine transactional and location data for campaign validation and offer high-level attribution models; internal case studies in 2024 showed average sales uplifts of 6–12% and ROAS improvements of 1.4x–2.1x.

This turns traditional outdoor into a measurable performance channel attractive to institutional advertisers and performance-focused investors.

- MOVE 2.0 coverage: 78% of national DOOH (2024)

- Average sales uplift: 6–12% (2024 cases)

- ROAS improvement: 1.4x–2.1x

- Uses transactional + location data for attribution

Robust Programmatic Infrastructure

oOh!media's programmatic sales engine automates buying of outdoor ad space, attracting digital-native advertisers who favor automated bidding; programmatic made up about 28% of digital revenue by end-2025 and lifted average digital occupancy to ~86%.

This infrastructure turned programmatic into a core revenue driver in 2025, improving yield per screen and reducing manual sales costs by an estimated 18% year-over-year.

Here’s the quick math: programmatic growth drove ~12% revenue uplift across the digital network in 2025; what this hides—regional variation in adoption rates remains.

- Programmatic = 28% of digital revenue (2025)

- Average digital occupancy ~86% (2025)

- Yield per screen +12% (2025)

- Manual sales costs down ~18% YoY

oOh!media: 70k+ sites, 95% reach — digital 62% with programmatic driving +12% yield

oOh!media is Australia’s leading OOH owner with 70,000+ sites reaching 95% of population (end‑2025), diversified assets (billboards 32%, retail 28%, transport 18%, place-based 22% in FY2024), digital = 62% of OOH revenue (Q3 2025), programmatic 28% of digital (2025), digital occupancy ~86% and programmatic-driven yield +12% (2025).

| Metric | Value |

|---|---|

| Sites | 70,000+ |

| Reach | 95% |

| Digital share | 62% |

| Programmatic | 28% |

What is included in the product

Provides a clear SWOT framework for analyzing oOh!media’s business strategy, highlighting internal capabilities, market strengths, operational gaps, growth drivers, and external risks shaping its competitive position.

Provides a concise, visually structured SWOT for oOh!media that speeds stakeholder alignment and simplifies strategic decisions.

Weaknesses

Significant Lease Liabilities

A primary financial burden is oOh!media’s significant lease liabilities—reported operating lease commitments were A$815m as of 30 June 2025—driving high site rents and long-term payments to property owners.

These fixed costs compress margins when ad demand falls, since revenue lags while lease expenses remain; EBITDA fell 12% YoY in H1 FY2025, amplifying the squeeze.

Managing renewals and off‑balance leasing options remains a constant executive challenge to keep the balance sheet lean and free cash flow resilient.

Intensive Capital Expenditure Requirements

Maintaining market leadership forces oOh!media to reinvest heavily in hardware and digitise legacy billboards; management reported A$118m capital expenditure in FY2024, with A$60–80m guidance for 2025 for screen upgrades and site works. This high spend—driven by 4K deployments and physical maintenance—compresses free cash flow, limiting funds for dividends or acquisitions and raising leverage risk if revenue growth slows.

Heavy Reliance on ANZ Market

oOh!media earns about 95% of revenue from Australia and New Zealand (FY2024 group revenue A$403.6m), leaving it highly exposed to local GDP swings and ad-spend cycles; a 1% drop in ANZ ad spend would materially cut top-line given lack of other markets.

Unlike global peers, oOh! lacks geographic diversification to offset a South Pacific recession; this concentration raises volatility versus diversified rivals and limits growth levers outside ANZ.

Regulatory moves or state-level advertising restrictions in ANZ hit the whole business at once—no international buffer—so policy or economic shocks could compress margins and cash flow rapidly.

Margin Pressure from Competitive Tendering

Renewals for major airport and street-furniture contracts often trigger aggressive bidding against global giants, forcing oOh!media to offer lower margins to win.

Competitive tenders raise rent shares to landlords—reported up to 25% of revenue in some airport deals in 2024—compressing operating margins that were 8.2% in FY24.

Losing one major contract can cut national market share by several percentage points instantly; a single airport loss in 2023 reduced oOh!s reach by ~3%.

- Aggressive bidding vs global players

- Landlord rents up to 25% of revenue

- Operating margin pressure from 8.2% FY24

- Single contract loss ≈ 3% market reach hit

Exposure to Discretionary Ad Spend

oOh!media faces revenue volatility because Out-of-Home (OOH) is a premium ad channel often cut early in downturns; Australian ad spend fell 6.2% in 2023 and OOH advertising revenue contracted similarly, highlighting sensitivity to macro swings and consumer confidence drops.

Digital formats add pricing agility, but over 65% of oOh!media’s FY2024 revenue remained tied to corporate marketing budgets, keeping the business cyclical and exposed to reduced discretionary spend during recessions.

- High sensitivity to macro: ad spend fell 6.2% in 2023

- 65%+ FY2024 revenue linked to corporate marketing

- Digital helps but core remains cyclical

High lease burden and capex squeeze margins; ANZ concentration heightens policy risk

Heavy lease liabilities (A$815m oper. leases as at 30 Jun 2025) and high capex (A$118m FY2024; A$60–80m guidance 2025) compress FCF and margins (8.2% FY24), while 95% ANZ revenue concentration and 65% reliance on corporate marketing raise macro and policy exposure; competitive tenders push landlord rent shares up to 25% and single contract losses cut ~3% reach.

| Metric | Value |

|---|---|

| Operating leases | A$815m (30‑Jun‑2025) |

| Capex | A$118m FY2024; A$60–80m 2025 |

| ANZ revenue | 95% |

| Operating margin | 8.2% FY24 |

| Landlord rent share | Up to 25% |

Same Document Delivered

oOh!media SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

oOh!media leverages extensive OOH inventory and strong advertiser relationships to capture urban audiences, but faces digital competition and ad-spend cyclicality that pressure margins and growth.

Our full SWOT analysis unpacks strategic opportunities in programmatic OOH, revenue diversification paths, and regulatory risks with data-driven insights and financial context.

Purchase the complete report to receive an editable Word and Excel package—ready for investor decks, strategic planning, or competitive benchmarking.

Strengths

Dominant Market Position

oOh!media remains Australia’s leading Out of Home (OOH) provider, with a 2025- end network spanning over 70,000 sites across metro and regional markets, delivering reach into 95% of the Australian population and creating a durable competitive moat versus smaller owners.

Multi-Format Asset Diversity

oOh!media runs a broad asset mix—large-format billboards, retail networks, airports, office towers and rail—reducing concentration risk across mobility shifts; FY2024 revenue mix showed ~32% from out-of-home billboards, 28% retail/instore, 18% transport (air/rail) and 22% place-based/venue assets (oOh!media FY2024 report, Aug 2024).

Advanced Digital Integration

Data-Driven Audience Insights

oOh!media uses MOVE 2.0 and proprietary data platforms to deliver audience granularity—segmenting reach by time, location, and purchase behavior to clients; MOVE 2.0 adoption reached industry standard in 2024 with 78% of national DOOH campaigns measured.

They combine transactional and location data for campaign validation and offer high-level attribution models; internal case studies in 2024 showed average sales uplifts of 6–12% and ROAS improvements of 1.4x–2.1x.

This turns traditional outdoor into a measurable performance channel attractive to institutional advertisers and performance-focused investors.

- MOVE 2.0 coverage: 78% of national DOOH (2024)

- Average sales uplift: 6–12% (2024 cases)

- ROAS improvement: 1.4x–2.1x

- Uses transactional + location data for attribution

Robust Programmatic Infrastructure

oOh!media's programmatic sales engine automates buying of outdoor ad space, attracting digital-native advertisers who favor automated bidding; programmatic made up about 28% of digital revenue by end-2025 and lifted average digital occupancy to ~86%.

This infrastructure turned programmatic into a core revenue driver in 2025, improving yield per screen and reducing manual sales costs by an estimated 18% year-over-year.

Here’s the quick math: programmatic growth drove ~12% revenue uplift across the digital network in 2025; what this hides—regional variation in adoption rates remains.

- Programmatic = 28% of digital revenue (2025)

- Average digital occupancy ~86% (2025)

- Yield per screen +12% (2025)

- Manual sales costs down ~18% YoY

oOh!media: 70k+ sites, 95% reach — digital 62% with programmatic driving +12% yield

oOh!media is Australia’s leading OOH owner with 70,000+ sites reaching 95% of population (end‑2025), diversified assets (billboards 32%, retail 28%, transport 18%, place-based 22% in FY2024), digital = 62% of OOH revenue (Q3 2025), programmatic 28% of digital (2025), digital occupancy ~86% and programmatic-driven yield +12% (2025).

| Metric | Value |

|---|---|

| Sites | 70,000+ |

| Reach | 95% |

| Digital share | 62% |

| Programmatic | 28% |

What is included in the product

Provides a clear SWOT framework for analyzing oOh!media’s business strategy, highlighting internal capabilities, market strengths, operational gaps, growth drivers, and external risks shaping its competitive position.

Provides a concise, visually structured SWOT for oOh!media that speeds stakeholder alignment and simplifies strategic decisions.

Weaknesses

Significant Lease Liabilities

A primary financial burden is oOh!media’s significant lease liabilities—reported operating lease commitments were A$815m as of 30 June 2025—driving high site rents and long-term payments to property owners.

These fixed costs compress margins when ad demand falls, since revenue lags while lease expenses remain; EBITDA fell 12% YoY in H1 FY2025, amplifying the squeeze.

Managing renewals and off‑balance leasing options remains a constant executive challenge to keep the balance sheet lean and free cash flow resilient.

Intensive Capital Expenditure Requirements

Maintaining market leadership forces oOh!media to reinvest heavily in hardware and digitise legacy billboards; management reported A$118m capital expenditure in FY2024, with A$60–80m guidance for 2025 for screen upgrades and site works. This high spend—driven by 4K deployments and physical maintenance—compresses free cash flow, limiting funds for dividends or acquisitions and raising leverage risk if revenue growth slows.

Heavy Reliance on ANZ Market

oOh!media earns about 95% of revenue from Australia and New Zealand (FY2024 group revenue A$403.6m), leaving it highly exposed to local GDP swings and ad-spend cycles; a 1% drop in ANZ ad spend would materially cut top-line given lack of other markets.

Unlike global peers, oOh! lacks geographic diversification to offset a South Pacific recession; this concentration raises volatility versus diversified rivals and limits growth levers outside ANZ.

Regulatory moves or state-level advertising restrictions in ANZ hit the whole business at once—no international buffer—so policy or economic shocks could compress margins and cash flow rapidly.

Margin Pressure from Competitive Tendering

Renewals for major airport and street-furniture contracts often trigger aggressive bidding against global giants, forcing oOh!media to offer lower margins to win.

Competitive tenders raise rent shares to landlords—reported up to 25% of revenue in some airport deals in 2024—compressing operating margins that were 8.2% in FY24.

Losing one major contract can cut national market share by several percentage points instantly; a single airport loss in 2023 reduced oOh!s reach by ~3%.

- Aggressive bidding vs global players

- Landlord rents up to 25% of revenue

- Operating margin pressure from 8.2% FY24

- Single contract loss ≈ 3% market reach hit

Exposure to Discretionary Ad Spend

oOh!media faces revenue volatility because Out-of-Home (OOH) is a premium ad channel often cut early in downturns; Australian ad spend fell 6.2% in 2023 and OOH advertising revenue contracted similarly, highlighting sensitivity to macro swings and consumer confidence drops.

Digital formats add pricing agility, but over 65% of oOh!media’s FY2024 revenue remained tied to corporate marketing budgets, keeping the business cyclical and exposed to reduced discretionary spend during recessions.

- High sensitivity to macro: ad spend fell 6.2% in 2023

- 65%+ FY2024 revenue linked to corporate marketing

- Digital helps but core remains cyclical

High lease burden and capex squeeze margins; ANZ concentration heightens policy risk

Heavy lease liabilities (A$815m oper. leases as at 30 Jun 2025) and high capex (A$118m FY2024; A$60–80m guidance 2025) compress FCF and margins (8.2% FY24), while 95% ANZ revenue concentration and 65% reliance on corporate marketing raise macro and policy exposure; competitive tenders push landlord rent shares up to 25% and single contract losses cut ~3% reach.

| Metric | Value |

|---|---|

| Operating leases | A$815m (30‑Jun‑2025) |

| Capex | A$118m FY2024; A$60–80m 2025 |

| ANZ revenue | 95% |

| Operating margin | 8.2% FY24 |

| Landlord rent share | Up to 25% |

Same Document Delivered

oOh!media SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.