Ooredoo Q.P.S.C Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

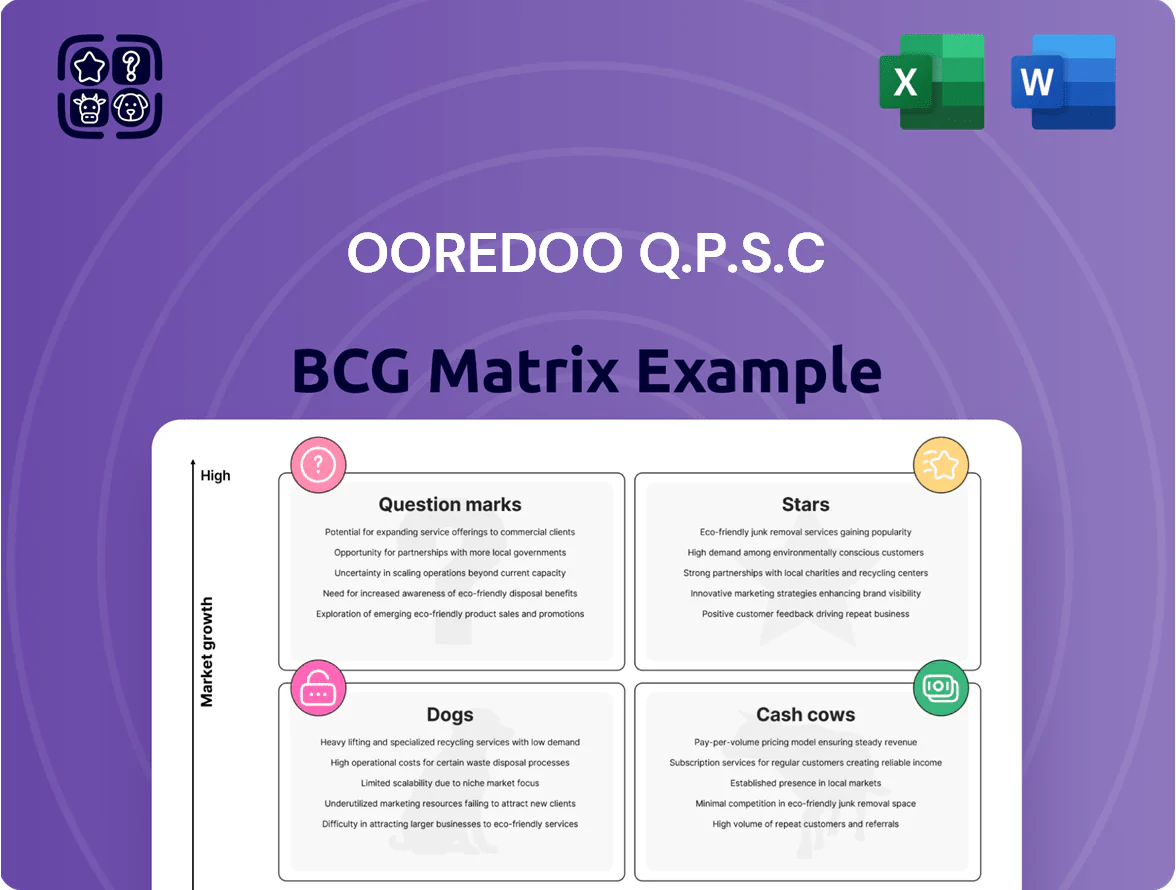

Ooredoo Q.P.S.C.'s BCG Matrix preview highlights its market leaders and potential challengers across telecom services and digital offerings, showing where cash generation, growth investment, or strategic divestment may be needed; this snapshot points to clear priorities but lacks full quadrant detail. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, editable Word and Excel deliverables, and a ready-to-use strategic roadmap to optimize portfolio and capital allocation.

Stars

5G Infrastructure and Services in Qatar

Ooredoo Qatar holds ~55% mobile market share (Q4 2025) and 5G penetration in the country tops 78% of mobile subscriptions, driving strong consumer ARPU growth to QAR 175 in 2025.

Major CAPEX—about QAR 1.2bn planned for 2026—targets network slicing and sub-10ms low-latency upgrades for energy and logistics clients.

The 5G segment is a revenue leader: 2025 service revenue growth ~12% y/y, with premium data and industrial contracts offsetting high cash burn.

Ooredoo Money and Fintech Solutions

Ooredoo Money leads regional mobile financial services with an estimated 28% market share in Qatar and 14% across Ooredoo's MENA markets as of Dec 2025, tapping a digital payments market growing ~18% CAGR (2023–2028).

The platform added micro-lending, digital insurance, and remittances in 2024–25, driving 35% YoY active-user growth and a 22% increase in ARPU in 2025.

To stay a Star, Ooredoo must keep investing in cybersecurity (spent QAR 120m in 2024) and UX upgrades to counter neo-banks gaining ~6% market share in 2025.

Data Center and Cloud Services

Ooredoo Q.P.S.C has rapidly expanded its data center footprint to 16 facilities across Qatar, Oman and Kuwait by 2025, targeting surging demand for localized cloud storage and sovereign data solutions.

This unit captures roughly 28% of the regional carrier-grade infrastructure market, driven by governments and enterprises digitizing services at ~18% CAGR (2022–2025).

CapEx to date exceeds QAR 1.1 billion, but high revenue growth—data center revenues rose 42% YoY in 2024—positions it as a future cash generator.

Managed Security and ICT Solutions

Managed Security and ICT Solutions sit in Ooredoo Q.P.S.C’s Stars quadrant: B2B revenue grew ~18% CAGR from 2020–2024, reaching an estimated QAR 1.2B annual run-rate by 2025 as bundled cybersecurity and managed IT captured ~42% share of large-corporate contracts in Qatar and select regional markets.

The offering leverages Ooredoo’s connectivity to sell unified services, driving gross margins near 48% and recurring ARR expansion; maintaining leadership requires R&D and SOC (security operations center) upgrades to counter evolving threats.

Analysts project 20–25% TAM (total addressable market) CAGR for managed security in MENA through 2025, so continued innovation can convert high-margin growth into sustained market dominance.

- 2024 B2B run-rate ~QAR 1.2B

- Corporate market share ~42%

- Gross margins ~48%

- Projected segment growth 20–25% CAGR to 2025

Digital Entertainment and Streaming Platforms

Ooredoo TV and Play bundle premium rights with fiber, capturing roughly 60% of Qatar’s fixed-broadband video users and adding 18% year-on-year subscribers in 2024, placing this unit in the BCG high-growth, high-share Stars quadrant.

As viewers move to on-demand, the segment shows >20% CAGR regional streaming demand; Ooredoo must keep investing ~QAR 200–300m annually in exclusive content and platform UX to compete with Netflix/OSN and protect churn below 10%.

- Market share ~60% of Qatari fixed-broadband video users

- Subscribers +18% YoY in 2024

- Regional streaming demand CAGR >20%

- Recommended investment QAR 200–300m/yr in content/tech

- Target churn <10% to maintain leadership

Ooredoo’s 5G, Money, Data Centers & TV dominate Qatar—leadership backed by QAR1.2B CAPEX

Ooredoo’s Stars (5G, Ooredoo Money, data centers, Managed Security, Ooredoo TV) show high share and growth: 55% mobile share (Q4 2025), 5G ARPU QAR175 (2025), Ooredoo Money 28% Qatar share (Dec 2025), data centers 16 sites, Managed Security QAR1.2B run-rate (2024), TV 60% fixed-video share (2024); CAPEX ~QAR1.2B (2026) to retain leadership.

| Unit | Share | Key 2024–25 |

|---|---|---|

| Mobile/5G | 55% | ARPU QAR175 |

| Ooredoo Money | 28% | Active users +35% YoY |

| Data centers | — | 16 sites, +42% rev |

What is included in the product

Comprehensive BCG review identifying Ooredoo's Stars, Cash Cows, Question Marks, and Dogs with strategic invest/hold/divest guidance.

One-page overview placing Ooredoo Q.P.S.C business units in a BCG quadrant for fast strategic clarity and prioritization.

Cash Cows

Domestic Mobile Voice and SMS Services

Ooredoo’s domestic mobile voice and SMS in Qatar and Kuwait holds >50% market share (Qatar 2024: 52%, Kuwait 2024: 51%), delivering stable ARPU ~QAR 85 (2024) and steady EBITDA margins ~45%, so it generates predictable cash flow.

Market growth is near 0% for basic voice/SMS; capex needs are low, requiring minimal marketing or new infrastructure, so operating cash is high and consistent.

That cash funded 2024 R&D and digital projects and supported dividends—2024 free cash flow ~QAR 1.1bn, enabling payout continuity.

Fixed-Line Home Broadband in Qatar

Ooredoo Q.P.S.C dominates Qatar’s residential fiber market with ~65–70% market share (2024 Q4), serving ~460,000 household connections and delivering steady ARPU of QAR 160/month, so recurring revenue is high and predictable.

With fiber plant largely built by 2023, incremental maintenance capex is low—estimated Opex-to-revenue ~18%—making fixed-line broadband a utility-like cash cow that generates strong free cash flow.

Cash surplus from this unit funded 2024–25 investments in 5G and fixed wireless, covering ~40% of strategic growth spend and de-risking moves into volatile tech markets.

International Roaming Agreements

Ooredoo Q.P.S.C leverages a global footprint and 400+ carrier partners to dominate high-margin international roaming, which accounted for an estimated 9–11% of group service revenue in 2024 and delivered EBITDA margins above 55% in roaming-specific operations.

Wholesale Carrier Services

Ooredoo Q.P.S.Cs Wholesale Carrier Services leverages an extensive subsea cable network and infrastructure leasing to generate high-volume revenue from international telcos, with wholesale capacity contracts contributing materially to group EBITDA—about 12% of Ooredoo Group revenues in 2024 (Ooredoo annual report 2024).

The market for wholesale capacity is stable; established assets let Ooredoo command significant market share in MENA/EMEA with low incremental costs per terabit, supporting consistent margins around 35% in 2024.

This unit maximizes utility of existing physical assets—cable capacity, landing stations, dark fibre—turning sunk capital into steady cash flow and predictable returns for the parent company.

- High-volume revenue from international carriers

- ~12% group revenue contribution (2024)

- ~35% wholesale margins (2024)

- Low incremental cost per terabit, stable demand

Prepaid Mobile Segments in Mature Markets

In Oman, Ooredoo Q.P.S.C’s prepaid mobile is a cash cow: penetration ~160 subscriptions per 100 people (Oman, 2024), volume steady, ARPU down slightly but EBITDA margins ~40% due to low acquisition costs and long amortized network spend.

Revenue growth is flat; free cash flow from prepaid funds digital rollouts (5G apps, e-wallet pilots) and reduces net debt (net debt/EBITDA ~1.2x, 2024).

- High penetration: ~160 subs/100 people (2024)

Ooredoo’s high-margin hubs: Qatar/Kuwait mobile, Qatar fiber, wholesale & Oman prepaid

Ooredoo’s cash cows: Qatar/Kuwait mobile voice/SMS (market share 2024: QA 52%, KW 51%; ARPU QAR85; EBITDA ~45%); Qatar fiber (Q4 2024: 65–70% share; 460,000 homes; ARPU QAR160; Opex/rev ~18%); Wholesale & roaming (~12% group revenue 2024; wholesale margins ~35%; roaming 9–11% revenue; EBITDA >55%); Oman prepaid (penetration 160/100; EBITDA ~40%).

| Unit | 2024 KPIs | Margins |

|---|---|---|

| Qatar/Kuwait mobile | Share 52%/51%; ARPU QAR85 | EBITDA ~45% |

| Qatar fiber | 65–70% share; 460k homes; ARPU QAR160 | Opex/rev ~18% |

| Wholesale/roaming | ~12% group rev; roaming 9–11% | Wholesale ~35%; roaming >55% |

| Oman prepaid | 160 subs/100; flat rev | EBITDA ~40% |

What You See Is What You Get

Ooredoo Q.P.S.C BCG Matrix

The file you're previewing is the exact Ooredoo Q.P.S.C BCG Matrix report you'll receive after purchase—no watermarks, no demo pages, just a fully formatted, professional analysis ready for presentation or editing.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Ooredoo Q.P.S.C.'s BCG Matrix preview highlights its market leaders and potential challengers across telecom services and digital offerings, showing where cash generation, growth investment, or strategic divestment may be needed; this snapshot points to clear priorities but lacks full quadrant detail. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, editable Word and Excel deliverables, and a ready-to-use strategic roadmap to optimize portfolio and capital allocation.

Stars

5G Infrastructure and Services in Qatar

Ooredoo Qatar holds ~55% mobile market share (Q4 2025) and 5G penetration in the country tops 78% of mobile subscriptions, driving strong consumer ARPU growth to QAR 175 in 2025.

Major CAPEX—about QAR 1.2bn planned for 2026—targets network slicing and sub-10ms low-latency upgrades for energy and logistics clients.

The 5G segment is a revenue leader: 2025 service revenue growth ~12% y/y, with premium data and industrial contracts offsetting high cash burn.

Ooredoo Money and Fintech Solutions

Ooredoo Money leads regional mobile financial services with an estimated 28% market share in Qatar and 14% across Ooredoo's MENA markets as of Dec 2025, tapping a digital payments market growing ~18% CAGR (2023–2028).

The platform added micro-lending, digital insurance, and remittances in 2024–25, driving 35% YoY active-user growth and a 22% increase in ARPU in 2025.

To stay a Star, Ooredoo must keep investing in cybersecurity (spent QAR 120m in 2024) and UX upgrades to counter neo-banks gaining ~6% market share in 2025.

Data Center and Cloud Services

Ooredoo Q.P.S.C has rapidly expanded its data center footprint to 16 facilities across Qatar, Oman and Kuwait by 2025, targeting surging demand for localized cloud storage and sovereign data solutions.

This unit captures roughly 28% of the regional carrier-grade infrastructure market, driven by governments and enterprises digitizing services at ~18% CAGR (2022–2025).

CapEx to date exceeds QAR 1.1 billion, but high revenue growth—data center revenues rose 42% YoY in 2024—positions it as a future cash generator.

Managed Security and ICT Solutions

Managed Security and ICT Solutions sit in Ooredoo Q.P.S.C’s Stars quadrant: B2B revenue grew ~18% CAGR from 2020–2024, reaching an estimated QAR 1.2B annual run-rate by 2025 as bundled cybersecurity and managed IT captured ~42% share of large-corporate contracts in Qatar and select regional markets.

The offering leverages Ooredoo’s connectivity to sell unified services, driving gross margins near 48% and recurring ARR expansion; maintaining leadership requires R&D and SOC (security operations center) upgrades to counter evolving threats.

Analysts project 20–25% TAM (total addressable market) CAGR for managed security in MENA through 2025, so continued innovation can convert high-margin growth into sustained market dominance.

- 2024 B2B run-rate ~QAR 1.2B

- Corporate market share ~42%

- Gross margins ~48%

- Projected segment growth 20–25% CAGR to 2025

Digital Entertainment and Streaming Platforms

Ooredoo TV and Play bundle premium rights with fiber, capturing roughly 60% of Qatar’s fixed-broadband video users and adding 18% year-on-year subscribers in 2024, placing this unit in the BCG high-growth, high-share Stars quadrant.

As viewers move to on-demand, the segment shows >20% CAGR regional streaming demand; Ooredoo must keep investing ~QAR 200–300m annually in exclusive content and platform UX to compete with Netflix/OSN and protect churn below 10%.

- Market share ~60% of Qatari fixed-broadband video users

- Subscribers +18% YoY in 2024

- Regional streaming demand CAGR >20%

- Recommended investment QAR 200–300m/yr in content/tech

- Target churn <10% to maintain leadership

Ooredoo’s 5G, Money, Data Centers & TV dominate Qatar—leadership backed by QAR1.2B CAPEX

Ooredoo’s Stars (5G, Ooredoo Money, data centers, Managed Security, Ooredoo TV) show high share and growth: 55% mobile share (Q4 2025), 5G ARPU QAR175 (2025), Ooredoo Money 28% Qatar share (Dec 2025), data centers 16 sites, Managed Security QAR1.2B run-rate (2024), TV 60% fixed-video share (2024); CAPEX ~QAR1.2B (2026) to retain leadership.

| Unit | Share | Key 2024–25 |

|---|---|---|

| Mobile/5G | 55% | ARPU QAR175 |

| Ooredoo Money | 28% | Active users +35% YoY |

| Data centers | — | 16 sites, +42% rev |

What is included in the product

Comprehensive BCG review identifying Ooredoo's Stars, Cash Cows, Question Marks, and Dogs with strategic invest/hold/divest guidance.

One-page overview placing Ooredoo Q.P.S.C business units in a BCG quadrant for fast strategic clarity and prioritization.

Cash Cows

Domestic Mobile Voice and SMS Services

Ooredoo’s domestic mobile voice and SMS in Qatar and Kuwait holds >50% market share (Qatar 2024: 52%, Kuwait 2024: 51%), delivering stable ARPU ~QAR 85 (2024) and steady EBITDA margins ~45%, so it generates predictable cash flow.

Market growth is near 0% for basic voice/SMS; capex needs are low, requiring minimal marketing or new infrastructure, so operating cash is high and consistent.

That cash funded 2024 R&D and digital projects and supported dividends—2024 free cash flow ~QAR 1.1bn, enabling payout continuity.

Fixed-Line Home Broadband in Qatar

Ooredoo Q.P.S.C dominates Qatar’s residential fiber market with ~65–70% market share (2024 Q4), serving ~460,000 household connections and delivering steady ARPU of QAR 160/month, so recurring revenue is high and predictable.

With fiber plant largely built by 2023, incremental maintenance capex is low—estimated Opex-to-revenue ~18%—making fixed-line broadband a utility-like cash cow that generates strong free cash flow.

Cash surplus from this unit funded 2024–25 investments in 5G and fixed wireless, covering ~40% of strategic growth spend and de-risking moves into volatile tech markets.

International Roaming Agreements

Ooredoo Q.P.S.C leverages a global footprint and 400+ carrier partners to dominate high-margin international roaming, which accounted for an estimated 9–11% of group service revenue in 2024 and delivered EBITDA margins above 55% in roaming-specific operations.

Wholesale Carrier Services

Ooredoo Q.P.S.Cs Wholesale Carrier Services leverages an extensive subsea cable network and infrastructure leasing to generate high-volume revenue from international telcos, with wholesale capacity contracts contributing materially to group EBITDA—about 12% of Ooredoo Group revenues in 2024 (Ooredoo annual report 2024).

The market for wholesale capacity is stable; established assets let Ooredoo command significant market share in MENA/EMEA with low incremental costs per terabit, supporting consistent margins around 35% in 2024.

This unit maximizes utility of existing physical assets—cable capacity, landing stations, dark fibre—turning sunk capital into steady cash flow and predictable returns for the parent company.

- High-volume revenue from international carriers

- ~12% group revenue contribution (2024)

- ~35% wholesale margins (2024)

- Low incremental cost per terabit, stable demand

Prepaid Mobile Segments in Mature Markets

In Oman, Ooredoo Q.P.S.C’s prepaid mobile is a cash cow: penetration ~160 subscriptions per 100 people (Oman, 2024), volume steady, ARPU down slightly but EBITDA margins ~40% due to low acquisition costs and long amortized network spend.

Revenue growth is flat; free cash flow from prepaid funds digital rollouts (5G apps, e-wallet pilots) and reduces net debt (net debt/EBITDA ~1.2x, 2024).

- High penetration: ~160 subs/100 people (2024)

Ooredoo’s high-margin hubs: Qatar/Kuwait mobile, Qatar fiber, wholesale & Oman prepaid

Ooredoo’s cash cows: Qatar/Kuwait mobile voice/SMS (market share 2024: QA 52%, KW 51%; ARPU QAR85; EBITDA ~45%); Qatar fiber (Q4 2024: 65–70% share; 460,000 homes; ARPU QAR160; Opex/rev ~18%); Wholesale & roaming (~12% group revenue 2024; wholesale margins ~35%; roaming 9–11% revenue; EBITDA >55%); Oman prepaid (penetration 160/100; EBITDA ~40%).

| Unit | 2024 KPIs | Margins |

|---|---|---|

| Qatar/Kuwait mobile | Share 52%/51%; ARPU QAR85 | EBITDA ~45% |

| Qatar fiber | 65–70% share; 460k homes; ARPU QAR160 | Opex/rev ~18% |

| Wholesale/roaming | ~12% group rev; roaming 9–11% | Wholesale ~35%; roaming >55% |

| Oman prepaid | 160 subs/100; flat rev | EBITDA ~40% |

What You See Is What You Get

Ooredoo Q.P.S.C BCG Matrix

The file you're previewing is the exact Ooredoo Q.P.S.C BCG Matrix report you'll receive after purchase—no watermarks, no demo pages, just a fully formatted, professional analysis ready for presentation or editing.