Opendoor Porter's Five Forces Analysis

From Overview to Strategy Blueprint

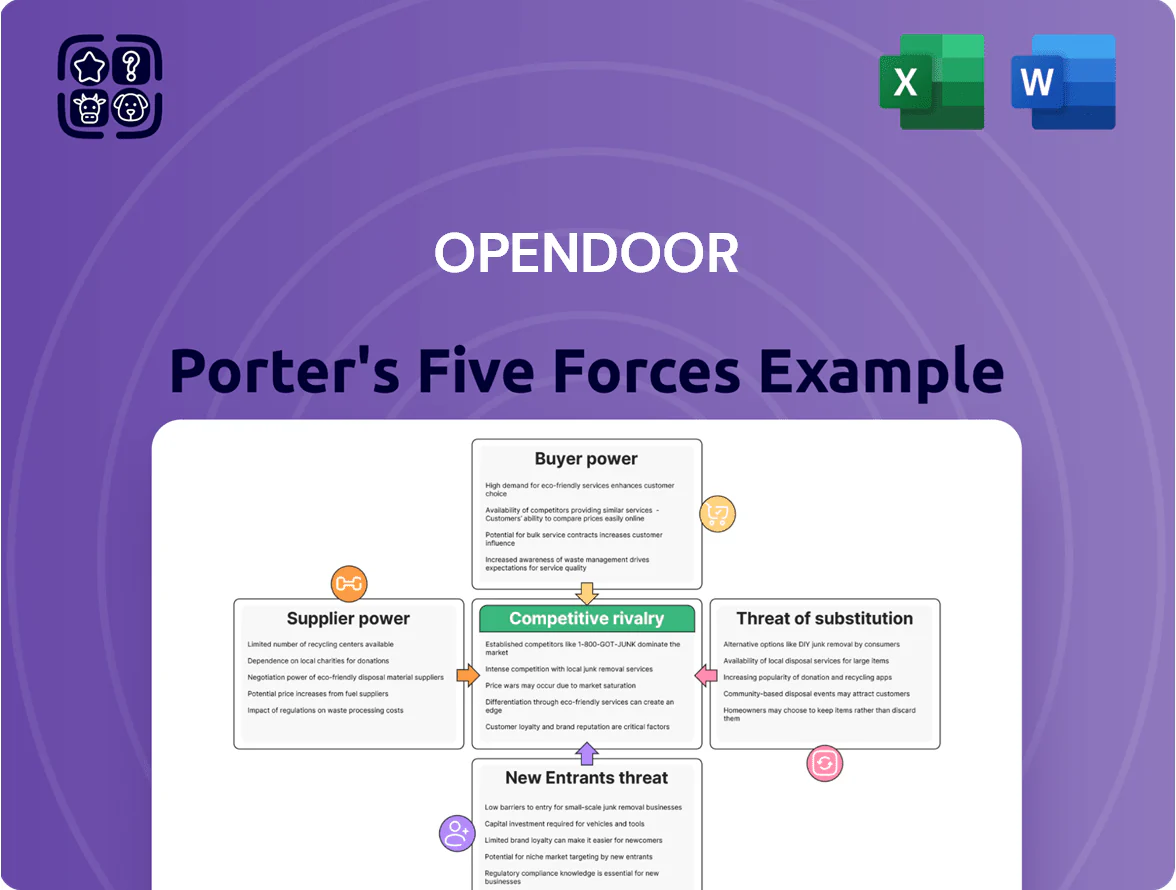

Opendoor faces intense buyer power and growing substitute threats as iBuyers and traditional brokers compete on price and convenience, while capital and regulatory pressures shape supplier and entrant dynamics.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Opendoor’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Capital and Financing Providers

Opendoor depends on debt and credit facilities to finance its inventory; as of Q4 2025 it carried about $3.8 billion of total debt and had drawn revolvers tied to LIBOR/SOFR-based spreads that drive interest expense.

Cost of capital remains decisive: a 200 basis-point rise in borrowing costs in 2025 would cut gross margins materially given thin iBuying spreads (average hold-time margin ~4.5%).

If institutional lenders tighten covenants or raise rates, Opendoor’s scaling is constrained and refinancing risk rises, limiting purchase throughput and capital deployment.

Renovation and Maintenance Contractors

Opendoor relies on local renovation contractors and material suppliers to complete light fixes on acquired homes; in 2024 Opendoor reported spending roughly $420 million on home repair and capital improvements, underscoring this dependence.

Supplier fragmentation generally favors Opendoor by enabling competitive bids, but U.S. construction labor shortages—with the National Association of Home Builders noting a 21% contractor deficit in some metros in 2023—can boost contractor pricing power.

Regional spikes in wage rates or material lead times can delay turn times and raise per-unit renovation costs, squeezing Opendoor’s margin on re-sales and iBuyer holding-costs.

Real Estate Data and Tech Providers

Access to accurate, real-time MLS and third-party housing data is critical for Opendoor’s pricing algorithms; in 2024 Opendoor reported ~60% of transactions relying on automated valuation models (AVMs) tuned to these feeds.

Multiple sources exist, but high-quality proprietary datasets and licensed MLS feeds give providers moderate bargaining power; a 20–50% licensing price spike could raise Opendoor’s cost per transaction materially.

Any disruption or license loss would cut AVM accuracy and could increase pricing errors beyond the company’s historical ±3–4% median absolute error, hurting margins and sale velocity.

Institutional Home Sellers

Institutional sellers—REITs, builders, and funds—provide bulk inventory and wield higher bargaining power than individuals; in 2024 institutional transactions made up ~12% of U.S. resale volume, letting them press for price premiums or tighter terms versus Opendoor.

These sellers can demand higher offers or pause sales if Opendoor’s yields fall below their required return (often 8–12% target IRR), reducing Opendoor’s margin and forcing price concessions or inventory gaps.

- Institutional share ~12% of resale market (2024)

- Typical institutional target IRR 8–12%

- They negotiate volume discounts or hold assets

Technology Infrastructure and Cloud Services

Opendoor depends on major cloud providers such as Amazon Web Services and Google Cloud for its core operations; in 2024 Opendoor disclosed cloud costs rising ~18% year-over-year, signaling material dependency.

High switching costs and need for GPU/AI-specialized infrastructure give these providers strong bargaining power, limiting Opendoor’s ability to negotiate lower rates or bespoke SLAs.

Opendoor’s leverage is further constrained by scale: top cloud vendors control ~60–70% of global cloud IaaS market (2024), so alternatives are limited.

- 2024 cloud spend growth ~18%

- Top vendors hold ~60–70% market share

- High GPU/AI infra raises switching cost

Supplier costs and rate shocks threaten Opendoor’s slim 4.5% hold-time margin

Suppliers (credit providers, contractors, MLS/data vendors, cloud providers, institutional sellers) exert moderate-to-high bargaining power over Opendoor via interest-costs, renovation pricing, data licensing, cloud fees, and bulk-inventory terms; shocks (200bps rate rise, 20–50% license jump, 18% cloud spend growth) materially compress Opendoor’s ~4.5% hold-time margin and raise refinancing and throughput risk.

| Supplier | 2024–25 metric | Impact |

|---|---|---|

| Debt | $3.8B total debt (Q4 2025) | Rate ↑ 200bps → margin squeeze |

| Renovation | $420M spend (2024) | Labor shortages ↑ costs |

| Data/AVM | 60% tx rely on AVMs (2024) | License ↑20–50% → higher CPT |

| Cloud | Spend ↑18% (2024) | High switching cost, limited negotiation |

| Institutional sellers | ~12% resale market (2024) | Negotiate price/terms, seek 8–12% IRR |

What is included in the product

Tailored Porter's Five Forces analysis for Opendoor that uncovers competitive intensity, buyer/supplier leverage, threat of substitutes and entrants, and industry rivalry—with strategic commentary on disruptive threats and implications for pricing and profitability.

A concise Opendoor Porter's Five Forces one-sheet that highlights competitive pressures and actionable levers—ideal for quick strategic decisions and investor briefings.

Customers Bargaining Power

Individual Home Sellers

Sellers hold strong leverage: they can pick Opendoor’s instant cash offer or list with an agent, so convenience competes with price. In 2024 US housing data, 30% of sellers cited speed as primary motive while median Opendoor discounts averaged ~6–8% vs market sale proceeds, per company reports. If Opendoor’s buy-sell spread exceeds typical agent commissions plus faster-close value (≈6%), sellers shift back to MLS to protect equity.

Individual Home Buyers

Buyers of Opendoor-owned homes hold high bargaining power because they can compare 1.2M active US listings on Zillow and Redfin (2024 data) and pick lower-priced alternatives; Opendoor’s Q4 2024 inventory turn of ~45 days pressures quick sales, so buyers often negotiate price cuts or concessions. Digital transparency raises price sensitivity—Opendoor’s median price gap vs. comps was about 2–4% in 2024, giving buyers leverage.

Institutional Buyers and REITs

Institutional buyers and REITs buy Opendoor batches and have high bargaining power: in 2024 institutional channels accounted for ~18% of Opendoor’s home sales, letting buyers demand bulk discounts (often 3–7% off list) and strict condition standards, which compress Opendoor’s gross margin (Opendoor reported a 2024 adjusted gross margin of –0.8%). Because these buyers are a major liquidity outlet, their purchase cadence directly affects Opendoor’s inventory turnover and cash flow.

Buyer Price Sensitivity and Interest Rates

At end-2025, national 30-year mortgage rates hovered near 7.1%, shrinking qualified buyer pool by ~18% year-over-year and boosting buyer leverage to demand lower home prices.

Opendoor faces pressure to cut listing prices and offer incentives, effectively transferring margin to buyers; its trade-in and iBuyer fees must compress to keep inventory moving.

- 30-yr avg 7.1% (Dec 2025)

- Qualified buyers down ~18% YoY

- Opendoor margins face downward pressure

Ease of Switching to Traditional Brokerages

Customer switching cost to a traditional agent is effectively zero, so Opendoor must constantly improve pricing, fees, and UX to retain sellers.

Buyers and sellers can abandon the digital path before signing, so churn risk rises if Opendoor's gross margin per home (negative in 2023–2024 for iBuying peers) or Net Promoter Score lags.

Buyers’ power, bulk discounts & seller speed squeeze Opendoor to negative margins

Customers hold high bargaining power: sellers choose Opendoor vs MLS (30% in 2024 prioritized speed) and walk if buy-sell spread >≈6%; buyers compare ~1.2M listings (2024) and negotiate price cuts (Opendoor median gap 2–4%); institutional buyers (18% of 2024 sales) demand 3–7% bulk discounts, squeezing Opendoor’s adjusted gross margin (–0.8% in 2024).

| Metric | Value |

|---|---|

| Seller speed preference (2024) | 30% |

| Active listings (2024) | 1.2M |

| Opendoor median price gap (2024) | 2–4% |

| Institutional share (2024) | 18% |

| Bulk discount demand | 3–7% |

| Adj. gross margin (2024) | –0.8% |

Preview the Actual Deliverable

Opendoor Porter's Five Forces Analysis

This preview shows the exact Opendoor Porter’s Five Forces Analysis you’ll receive—fully formatted, complete, and ready for immediate download after purchase; no placeholders or samples, just the final deliverable.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Opendoor faces intense buyer power and growing substitute threats as iBuyers and traditional brokers compete on price and convenience, while capital and regulatory pressures shape supplier and entrant dynamics.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Opendoor’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Capital and Financing Providers

Opendoor depends on debt and credit facilities to finance its inventory; as of Q4 2025 it carried about $3.8 billion of total debt and had drawn revolvers tied to LIBOR/SOFR-based spreads that drive interest expense.

Cost of capital remains decisive: a 200 basis-point rise in borrowing costs in 2025 would cut gross margins materially given thin iBuying spreads (average hold-time margin ~4.5%).

If institutional lenders tighten covenants or raise rates, Opendoor’s scaling is constrained and refinancing risk rises, limiting purchase throughput and capital deployment.

Renovation and Maintenance Contractors

Opendoor relies on local renovation contractors and material suppliers to complete light fixes on acquired homes; in 2024 Opendoor reported spending roughly $420 million on home repair and capital improvements, underscoring this dependence.

Supplier fragmentation generally favors Opendoor by enabling competitive bids, but U.S. construction labor shortages—with the National Association of Home Builders noting a 21% contractor deficit in some metros in 2023—can boost contractor pricing power.

Regional spikes in wage rates or material lead times can delay turn times and raise per-unit renovation costs, squeezing Opendoor’s margin on re-sales and iBuyer holding-costs.

Real Estate Data and Tech Providers

Access to accurate, real-time MLS and third-party housing data is critical for Opendoor’s pricing algorithms; in 2024 Opendoor reported ~60% of transactions relying on automated valuation models (AVMs) tuned to these feeds.

Multiple sources exist, but high-quality proprietary datasets and licensed MLS feeds give providers moderate bargaining power; a 20–50% licensing price spike could raise Opendoor’s cost per transaction materially.

Any disruption or license loss would cut AVM accuracy and could increase pricing errors beyond the company’s historical ±3–4% median absolute error, hurting margins and sale velocity.

Institutional Home Sellers

Institutional sellers—REITs, builders, and funds—provide bulk inventory and wield higher bargaining power than individuals; in 2024 institutional transactions made up ~12% of U.S. resale volume, letting them press for price premiums or tighter terms versus Opendoor.

These sellers can demand higher offers or pause sales if Opendoor’s yields fall below their required return (often 8–12% target IRR), reducing Opendoor’s margin and forcing price concessions or inventory gaps.

- Institutional share ~12% of resale market (2024)

- Typical institutional target IRR 8–12%

- They negotiate volume discounts or hold assets

Technology Infrastructure and Cloud Services

Opendoor depends on major cloud providers such as Amazon Web Services and Google Cloud for its core operations; in 2024 Opendoor disclosed cloud costs rising ~18% year-over-year, signaling material dependency.

High switching costs and need for GPU/AI-specialized infrastructure give these providers strong bargaining power, limiting Opendoor’s ability to negotiate lower rates or bespoke SLAs.

Opendoor’s leverage is further constrained by scale: top cloud vendors control ~60–70% of global cloud IaaS market (2024), so alternatives are limited.

- 2024 cloud spend growth ~18%

- Top vendors hold ~60–70% market share

- High GPU/AI infra raises switching cost

Supplier costs and rate shocks threaten Opendoor’s slim 4.5% hold-time margin

Suppliers (credit providers, contractors, MLS/data vendors, cloud providers, institutional sellers) exert moderate-to-high bargaining power over Opendoor via interest-costs, renovation pricing, data licensing, cloud fees, and bulk-inventory terms; shocks (200bps rate rise, 20–50% license jump, 18% cloud spend growth) materially compress Opendoor’s ~4.5% hold-time margin and raise refinancing and throughput risk.

| Supplier | 2024–25 metric | Impact |

|---|---|---|

| Debt | $3.8B total debt (Q4 2025) | Rate ↑ 200bps → margin squeeze |

| Renovation | $420M spend (2024) | Labor shortages ↑ costs |

| Data/AVM | 60% tx rely on AVMs (2024) | License ↑20–50% → higher CPT |

| Cloud | Spend ↑18% (2024) | High switching cost, limited negotiation |

| Institutional sellers | ~12% resale market (2024) | Negotiate price/terms, seek 8–12% IRR |

What is included in the product

Tailored Porter's Five Forces analysis for Opendoor that uncovers competitive intensity, buyer/supplier leverage, threat of substitutes and entrants, and industry rivalry—with strategic commentary on disruptive threats and implications for pricing and profitability.

A concise Opendoor Porter's Five Forces one-sheet that highlights competitive pressures and actionable levers—ideal for quick strategic decisions and investor briefings.

Customers Bargaining Power

Individual Home Sellers

Sellers hold strong leverage: they can pick Opendoor’s instant cash offer or list with an agent, so convenience competes with price. In 2024 US housing data, 30% of sellers cited speed as primary motive while median Opendoor discounts averaged ~6–8% vs market sale proceeds, per company reports. If Opendoor’s buy-sell spread exceeds typical agent commissions plus faster-close value (≈6%), sellers shift back to MLS to protect equity.

Individual Home Buyers

Buyers of Opendoor-owned homes hold high bargaining power because they can compare 1.2M active US listings on Zillow and Redfin (2024 data) and pick lower-priced alternatives; Opendoor’s Q4 2024 inventory turn of ~45 days pressures quick sales, so buyers often negotiate price cuts or concessions. Digital transparency raises price sensitivity—Opendoor’s median price gap vs. comps was about 2–4% in 2024, giving buyers leverage.

Institutional Buyers and REITs

Institutional buyers and REITs buy Opendoor batches and have high bargaining power: in 2024 institutional channels accounted for ~18% of Opendoor’s home sales, letting buyers demand bulk discounts (often 3–7% off list) and strict condition standards, which compress Opendoor’s gross margin (Opendoor reported a 2024 adjusted gross margin of –0.8%). Because these buyers are a major liquidity outlet, their purchase cadence directly affects Opendoor’s inventory turnover and cash flow.

Buyer Price Sensitivity and Interest Rates

At end-2025, national 30-year mortgage rates hovered near 7.1%, shrinking qualified buyer pool by ~18% year-over-year and boosting buyer leverage to demand lower home prices.

Opendoor faces pressure to cut listing prices and offer incentives, effectively transferring margin to buyers; its trade-in and iBuyer fees must compress to keep inventory moving.

- 30-yr avg 7.1% (Dec 2025)

- Qualified buyers down ~18% YoY

- Opendoor margins face downward pressure

Ease of Switching to Traditional Brokerages

Customer switching cost to a traditional agent is effectively zero, so Opendoor must constantly improve pricing, fees, and UX to retain sellers.

Buyers and sellers can abandon the digital path before signing, so churn risk rises if Opendoor's gross margin per home (negative in 2023–2024 for iBuying peers) or Net Promoter Score lags.

Buyers’ power, bulk discounts & seller speed squeeze Opendoor to negative margins

Customers hold high bargaining power: sellers choose Opendoor vs MLS (30% in 2024 prioritized speed) and walk if buy-sell spread >≈6%; buyers compare ~1.2M listings (2024) and negotiate price cuts (Opendoor median gap 2–4%); institutional buyers (18% of 2024 sales) demand 3–7% bulk discounts, squeezing Opendoor’s adjusted gross margin (–0.8% in 2024).

| Metric | Value |

|---|---|

| Seller speed preference (2024) | 30% |

| Active listings (2024) | 1.2M |

| Opendoor median price gap (2024) | 2–4% |

| Institutional share (2024) | 18% |

| Bulk discount demand | 3–7% |

| Adj. gross margin (2024) | –0.8% |

Preview the Actual Deliverable

Opendoor Porter's Five Forces Analysis

This preview shows the exact Opendoor Porter’s Five Forces Analysis you’ll receive—fully formatted, complete, and ready for immediate download after purchase; no placeholders or samples, just the final deliverable.