Opendoor PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic advantage with our PESTLE Analysis of Opendoor—unpack how political shifts, economic cycles, social trends, and tech innovation shape its margins and growth prospects; ideal for investors, strategists, and advisors. Purchase the full report to access ready-to-use, editable insights that streamline decision-making and reveal actionable risks and opportunities.

Political factors

Federal housing policy shifts

As of late 2025, federal initiatives — including a $10B Housing Supply Accelerator and expanded first-time buyer tax credits raising average benefits to $15,000 in 2024–25 — boost demand for entry-level homes, aiding Opendoor’s buy-rehab-sell volume (Opendoor reported $7.2B in home sales in 2024). However, rising political pressure to limit institutional single-family rental ownership has prompted proposed federal oversight and potential caps on large digital buyers, threatening Opendoor’s scale advantages.

GSE reform and mortgage backing

The political debate over Fannie Mae and Freddie Mac shapes the secondary mortgage market; proposals in 2024–25 to privatize or recapitalize GSEs could widen interest rate spreads by 25–40 bps, tightening mortgage availability for Opendoor buyers. Changes to conforming loan limits—raised to $766,550 for single-family in 2024 in high-cost areas—and down payment policy shifts would directly impact Opendoor’s resale velocity and addressable buyer pool.

State-level zoning and land use regulations

Legislative reforms in Texas, Arizona, and Florida—where combined population growth topped 6.5 million from 2010–2020—are loosening exclusionary zoning to allow more high-density and smaller units, potentially expanding Opendoor’s addressable supply; Arizona’s recent state bills target ADU expansion while Texas cities pilot transit-oriented upzoning. Opendoor must navigate local politics where some municipalities see iBuying as liquidity—Opendoor transacted $9.8B in homes in 2024—while others cite neighborhood stability concerns. Political stability in these high-growth Sun Belt markets underpins Opendoor’s expansion strategy, with Florida, Texas, and Arizona representing over 30% of U.S. home sales growth in 2023.

Trade policies and construction costs

- Tariff-driven material cost swings; lumber/steel price spikes up to 12% (2023)

- Opendoor average renovation spend ≈ $18,000 per home (2024)

- Stable trade relations critical to predictable margins

Governmental focus on algorithmic transparency

Political pressure is rising: federal and state regulators increased enforcement actions on algorithmic bias in 2024, with HUD issuing guidance on automated valuation models and several states proposing AI fairness bills that could affect Opendoor’s pricing tools.

Opendoor must proactively engage lawmakers and publish audit-ready fairness metrics; in 2025, 42% of real-estate tech firms reported updating models after regulatory reviews.

- Regulatory trend: HUD and state AI bills tightening oversight

- Risk: potential fines, litigation, or restrictions on AVMs

- Action: transparency, audits, policy engagement, equity metrics

Opendoor $7.2B surge vs. rising renovation, lumber costs and looming GSE caps

Federal housing incentives and higher conforming loan limits boosted entry-level demand and Opendoor’s volume ($7.2B sales in 2024), while proposed caps on institutional buyers and GSE reforms (could widen spreads 25–40 bps) threaten financing and scale; trade-driven material cost swings (lumber +12% in 2023) raised average renovation spend (~$18,000 per home in 2024), and tightened AI/AVM oversight after 2024 increases regulatory risk.

| Metric | Value |

|---|---|

| Opendoor home sales (2024) | $7.2B |

| Avg renovation spend (2024) | $18,000 |

| Lumber price spike (2023) | +12% |

| GSE spread risk | +25–40 bps |

What is included in the product

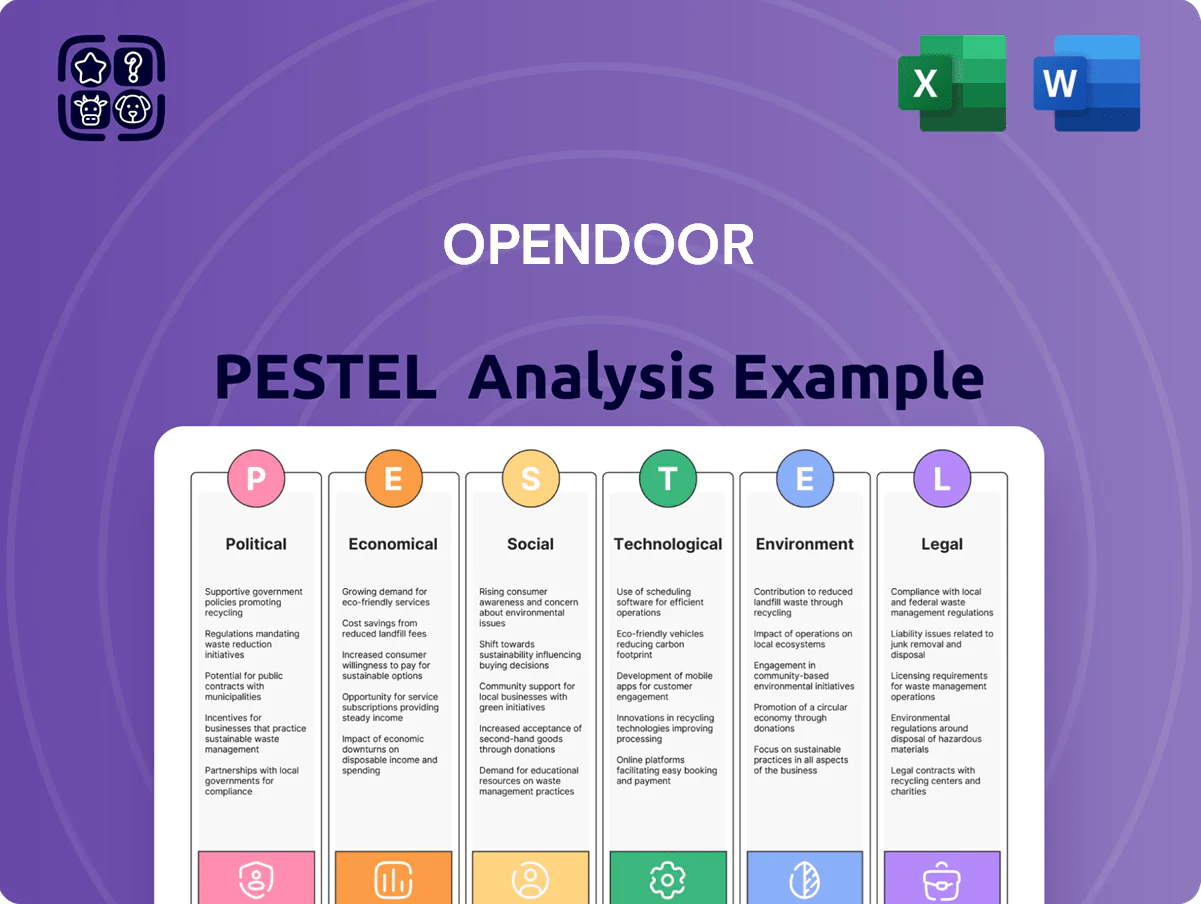

Explores how macro-environmental factors uniquely affect Opendoor across Political, Economic, Social, Technological, Environmental, and Legal dimensions, each backed by data and current trends to identify risks and opportunities.

A concise Opendoor PESTLE snapshot that distills regulatory, economic, social, technological, legal, and environmental factors into a ready-to-use slide or handout for fast alignment in strategy meetings.

Economic factors

Interest rate environment and cost of capital

By end-2025 the Fed's path remains Opendoor's key economic lever: a 25–50bps hike in 2024–25 would raise interest on its $2.5B asset-backed facilities, increasing financing expense and compressing gross margins.

Higher mortgage rates—US 30‑yr avg ~6.7% in early 2025 vs ~3% in 2021—have reduced buyer demand, lengthening Opendoor's average holding period and raising carrying costs.

Longer holds increase exposure to local price depreciation; a 1% market pullback on a $300k home erodes equity by $3k, magnifying losses when financing costs are elevated.

Housing inventory levels and market liquidity

Housing supply-demand balance controls Opendoor's turnover: in 2024 U.S. active listings fell ~20% year-over-year, constraining iBuyer acquisitions and compressing purchase discounts. Low-inventory markets impede sourcing homes at target margins, while high-inventory periods risk longer holding times—NAR reported months' supply rose to 3.9 in 2023 from 3.1 in 2021. Persistently low mortgage rates (average 30-year ~6.7% in 2024) can lock owners into existing loans, reducing transaction volume available to iBuyers.

Labor market health and wage growth

Consumer confidence tracks employment and real wages; US real average hourly earnings rose 1.2% year-over-year in 2024 Q4, supporting move-up buyers who favor Opendoor’s quick-sale model.

Strong payroll gains—monthly nonfarm payrolls averaged +210k in 2024—correlate with higher relocation for jobs, boosting demand for Opendoor convenience.

During downturns, rising unemployment (peak 2020 aside) and stagnant real wages push households toward traditional listings to seek maximum sale price.

Inflationary pressures on renovation services

Persistent U.S. services inflation—4.0% YoY in the CPI Services less energy and shelter as of Dec 2025—raises contractor labor costs Opendoor pays for repairs, squeezing contribution margin per home as volume scales.

Rising commodity costs: residential roofing up ~12% YoY, HVAC components +9% and flooring materials +7% in 2024–2025 increased average repair spend per home, reducing net resale proceeds.

Operational leverage and procurement scale determine whether Opendoor can offset these increases via negotiated contractor rates, shorter holding times, or price adjustments.

- Services inflation 4.0% YoY (Dec 2025)

- Roofing +12%, HVAC +9%, flooring +7% (2024–2025)

- Higher variable repair costs lower contribution margin per home

- Scale, procurement, and holding time key to mitigation

Institutional investor sentiment and funding

Opendoor depends on equity and debt markets to fund its capital-intensive home-buying model; in 2024 it reported $1.7 billion of inventory financing capacity and raised $350 million in equity-like convertible notes in 2023, but tighter 2024 market conditions compressed growth-stage valuations and increased cost of capital.

Reduced investor appetite for tech growth and volatility in 2024-25 could limit liquidity, while a weakened residential securitization market—US RMBS issuance fell ~20% y/y in 2024—would impair Opendoor’s ability to offload risk and recycle capital.

- 2024 inventory financing capacity: $1.7B

- 2023 convertible raise: $350M

- US residential securitization issuance down ~20% y/y in 2024

Higher rates, tighter financing squeeze margins and inventory — home repairs amplify losses

Fed hikes raise cost on $2.5B facilities; 25–50bps in 2024–25 compresses margins. 30‑yr avg ~6.7% in early 2025 lengthened holds and increased carrying costs; a 1% price drop on $300k home = $3k equity loss. Inventory financing capacity $1.7B (2024); RMBS issuance down ~20% y/y (2024) limits capital recycling, while services inflation and repair cost rises (roof +12%, HVAC +9%) squeeze contribution per home.

| Metric | Value |

|---|---|

| 30-yr mortgage (early 2025) | ~6.7% |

| Inventory financing (2024) | $1.7B |

| RMBS issuance change (2024) | -20% y/y |

| Services inflation (Dec 2025) | 4.0% YoY |

| Roof/HVAC/flooring (2024–25) | +12%/+9%/+7% |

Preview the Actual Deliverable

Opendoor PESTLE Analysis

The preview shown here is the exact Opendoor PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic advantage with our PESTLE Analysis of Opendoor—unpack how political shifts, economic cycles, social trends, and tech innovation shape its margins and growth prospects; ideal for investors, strategists, and advisors. Purchase the full report to access ready-to-use, editable insights that streamline decision-making and reveal actionable risks and opportunities.

Political factors

Federal housing policy shifts

As of late 2025, federal initiatives — including a $10B Housing Supply Accelerator and expanded first-time buyer tax credits raising average benefits to $15,000 in 2024–25 — boost demand for entry-level homes, aiding Opendoor’s buy-rehab-sell volume (Opendoor reported $7.2B in home sales in 2024). However, rising political pressure to limit institutional single-family rental ownership has prompted proposed federal oversight and potential caps on large digital buyers, threatening Opendoor’s scale advantages.

GSE reform and mortgage backing

The political debate over Fannie Mae and Freddie Mac shapes the secondary mortgage market; proposals in 2024–25 to privatize or recapitalize GSEs could widen interest rate spreads by 25–40 bps, tightening mortgage availability for Opendoor buyers. Changes to conforming loan limits—raised to $766,550 for single-family in 2024 in high-cost areas—and down payment policy shifts would directly impact Opendoor’s resale velocity and addressable buyer pool.

State-level zoning and land use regulations

Legislative reforms in Texas, Arizona, and Florida—where combined population growth topped 6.5 million from 2010–2020—are loosening exclusionary zoning to allow more high-density and smaller units, potentially expanding Opendoor’s addressable supply; Arizona’s recent state bills target ADU expansion while Texas cities pilot transit-oriented upzoning. Opendoor must navigate local politics where some municipalities see iBuying as liquidity—Opendoor transacted $9.8B in homes in 2024—while others cite neighborhood stability concerns. Political stability in these high-growth Sun Belt markets underpins Opendoor’s expansion strategy, with Florida, Texas, and Arizona representing over 30% of U.S. home sales growth in 2023.

Trade policies and construction costs

- Tariff-driven material cost swings; lumber/steel price spikes up to 12% (2023)

- Opendoor average renovation spend ≈ $18,000 per home (2024)

- Stable trade relations critical to predictable margins

Governmental focus on algorithmic transparency

Political pressure is rising: federal and state regulators increased enforcement actions on algorithmic bias in 2024, with HUD issuing guidance on automated valuation models and several states proposing AI fairness bills that could affect Opendoor’s pricing tools.

Opendoor must proactively engage lawmakers and publish audit-ready fairness metrics; in 2025, 42% of real-estate tech firms reported updating models after regulatory reviews.

- Regulatory trend: HUD and state AI bills tightening oversight

- Risk: potential fines, litigation, or restrictions on AVMs

- Action: transparency, audits, policy engagement, equity metrics

Opendoor $7.2B surge vs. rising renovation, lumber costs and looming GSE caps

Federal housing incentives and higher conforming loan limits boosted entry-level demand and Opendoor’s volume ($7.2B sales in 2024), while proposed caps on institutional buyers and GSE reforms (could widen spreads 25–40 bps) threaten financing and scale; trade-driven material cost swings (lumber +12% in 2023) raised average renovation spend (~$18,000 per home in 2024), and tightened AI/AVM oversight after 2024 increases regulatory risk.

| Metric | Value |

|---|---|

| Opendoor home sales (2024) | $7.2B |

| Avg renovation spend (2024) | $18,000 |

| Lumber price spike (2023) | +12% |

| GSE spread risk | +25–40 bps |

What is included in the product

Explores how macro-environmental factors uniquely affect Opendoor across Political, Economic, Social, Technological, Environmental, and Legal dimensions, each backed by data and current trends to identify risks and opportunities.

A concise Opendoor PESTLE snapshot that distills regulatory, economic, social, technological, legal, and environmental factors into a ready-to-use slide or handout for fast alignment in strategy meetings.

Economic factors

Interest rate environment and cost of capital

By end-2025 the Fed's path remains Opendoor's key economic lever: a 25–50bps hike in 2024–25 would raise interest on its $2.5B asset-backed facilities, increasing financing expense and compressing gross margins.

Higher mortgage rates—US 30‑yr avg ~6.7% in early 2025 vs ~3% in 2021—have reduced buyer demand, lengthening Opendoor's average holding period and raising carrying costs.

Longer holds increase exposure to local price depreciation; a 1% market pullback on a $300k home erodes equity by $3k, magnifying losses when financing costs are elevated.

Housing inventory levels and market liquidity

Housing supply-demand balance controls Opendoor's turnover: in 2024 U.S. active listings fell ~20% year-over-year, constraining iBuyer acquisitions and compressing purchase discounts. Low-inventory markets impede sourcing homes at target margins, while high-inventory periods risk longer holding times—NAR reported months' supply rose to 3.9 in 2023 from 3.1 in 2021. Persistently low mortgage rates (average 30-year ~6.7% in 2024) can lock owners into existing loans, reducing transaction volume available to iBuyers.

Labor market health and wage growth

Consumer confidence tracks employment and real wages; US real average hourly earnings rose 1.2% year-over-year in 2024 Q4, supporting move-up buyers who favor Opendoor’s quick-sale model.

Strong payroll gains—monthly nonfarm payrolls averaged +210k in 2024—correlate with higher relocation for jobs, boosting demand for Opendoor convenience.

During downturns, rising unemployment (peak 2020 aside) and stagnant real wages push households toward traditional listings to seek maximum sale price.

Inflationary pressures on renovation services

Persistent U.S. services inflation—4.0% YoY in the CPI Services less energy and shelter as of Dec 2025—raises contractor labor costs Opendoor pays for repairs, squeezing contribution margin per home as volume scales.

Rising commodity costs: residential roofing up ~12% YoY, HVAC components +9% and flooring materials +7% in 2024–2025 increased average repair spend per home, reducing net resale proceeds.

Operational leverage and procurement scale determine whether Opendoor can offset these increases via negotiated contractor rates, shorter holding times, or price adjustments.

- Services inflation 4.0% YoY (Dec 2025)

- Roofing +12%, HVAC +9%, flooring +7% (2024–2025)

- Higher variable repair costs lower contribution margin per home

- Scale, procurement, and holding time key to mitigation

Institutional investor sentiment and funding

Opendoor depends on equity and debt markets to fund its capital-intensive home-buying model; in 2024 it reported $1.7 billion of inventory financing capacity and raised $350 million in equity-like convertible notes in 2023, but tighter 2024 market conditions compressed growth-stage valuations and increased cost of capital.

Reduced investor appetite for tech growth and volatility in 2024-25 could limit liquidity, while a weakened residential securitization market—US RMBS issuance fell ~20% y/y in 2024—would impair Opendoor’s ability to offload risk and recycle capital.

- 2024 inventory financing capacity: $1.7B

- 2023 convertible raise: $350M

- US residential securitization issuance down ~20% y/y in 2024

Higher rates, tighter financing squeeze margins and inventory — home repairs amplify losses

Fed hikes raise cost on $2.5B facilities; 25–50bps in 2024–25 compresses margins. 30‑yr avg ~6.7% in early 2025 lengthened holds and increased carrying costs; a 1% price drop on $300k home = $3k equity loss. Inventory financing capacity $1.7B (2024); RMBS issuance down ~20% y/y (2024) limits capital recycling, while services inflation and repair cost rises (roof +12%, HVAC +9%) squeeze contribution per home.

| Metric | Value |

|---|---|

| 30-yr mortgage (early 2025) | ~6.7% |

| Inventory financing (2024) | $1.7B |

| RMBS issuance change (2024) | -20% y/y |

| Services inflation (Dec 2025) | 4.0% YoY |

| Roof/HVAC/flooring (2024–25) | +12%/+9%/+7% |

Preview the Actual Deliverable

Opendoor PESTLE Analysis

The preview shown here is the exact Opendoor PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.