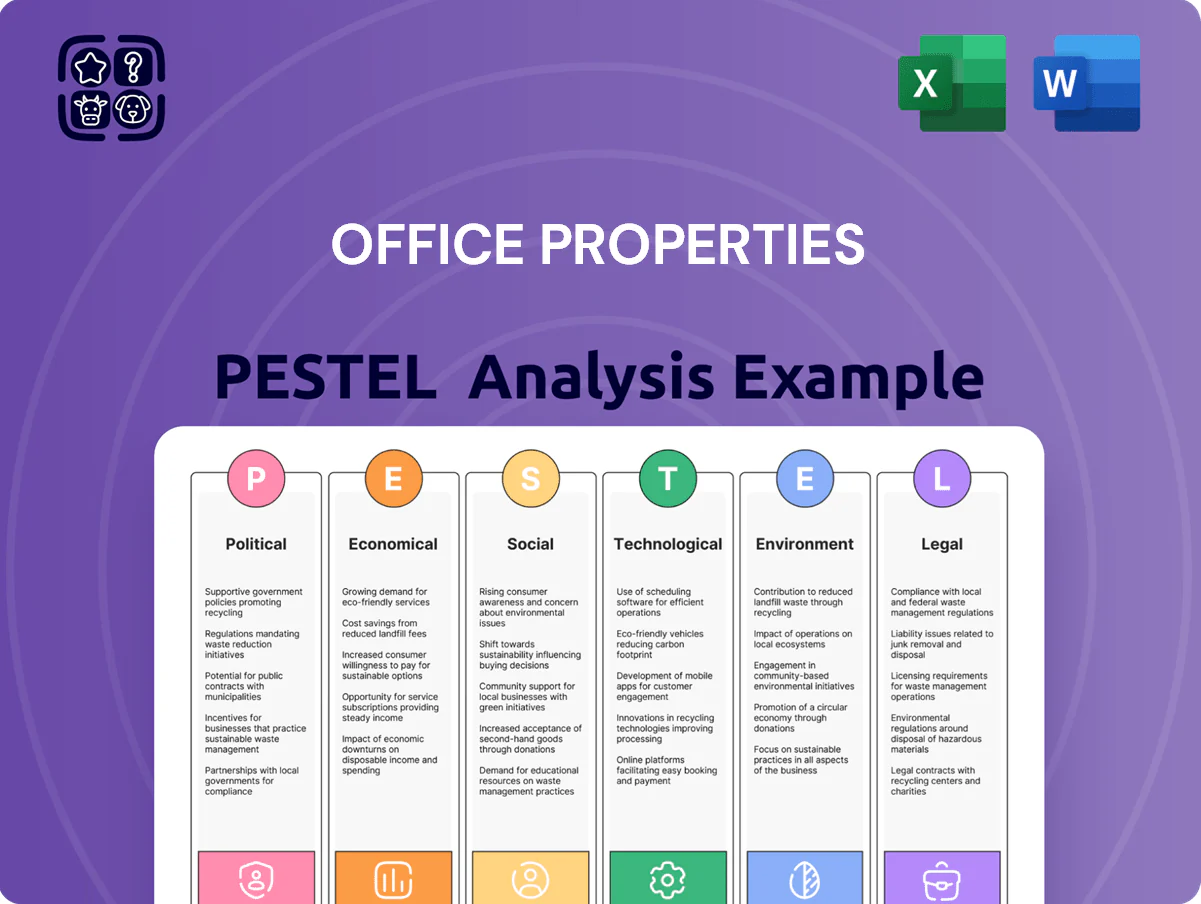

Office Properties PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and technological change are reshaping Office Properties’ prospects—our concise PESTLE highlights the key external forces you need to know. Buy the full analysis for a complete, actionable breakdown with ready-to-use insights for investors, strategists, and advisors. Download now to turn external risks and opportunities into clear strategic moves.

Political factors

Government Tenant Dependency and Budgetary Shifts

The trust's 62% government-tenant concentration makes it highly sensitive to federal and state budget cycles; in FY2024–2025 agency relocations and consolidations driven by shifting fiscal priorities reduced public-sector leasing demand by an estimated 7.8%. As of late 2025, changes in political leadership and appropriations bills—Congress cut certain agency facility budgets by roughly $1.3 billion in 2025—raise risk of lease non-renewals or space reductions. Strategic planners should monitor legislative appropriations and agency-level directives to anticipate vacancies and model potential rent loss scenarios.

Federal Remote Work Policies

Federal mandates on in-person work for federal employees shape demand for OPI's specialized properties; after 2024–2025 directive shifts, vacancy in government-leased office space varied, with GSA-reported federal office utilization averaging 48% in 2025 versus 63% pre-pandemic, reducing OPI's government rental income visibility by an estimated 12–18%.

Geopolitical Impact on Corporate Strategy

Global political instability and trade tensions are prompting OPI private-sector multinationals to scale back expansion: 68% of surveyed tenants delayed site selection in 2024, per CBRE, and cross-border leasing inquiries fell 14% YoY. High-credit tenants increasingly avoid long-term commitments, driving average lease term requests down from 7.2 years (2022) to 5.1 years (2024) and boosting demand for flexible termination clauses by 32%.

Urban Policy and Infrastructure Investment

Local political initiatives to revitalize CBDs directly affect OPI's urban asset values; for example, cities allocating >$5bn in 2024–25 to downtown redevelopment saw office vacancy drop ~150–200 bps vs peers, lifting rents and NAV for nearby REITs.

Transit-oriented development incentives and corporate relocation tax breaks (e.g., abatements covering up to 50% of payroll taxes) concentrate demand in targeted clusters, improving lease-up rates and reducing cap-exposure.

Conversely, failure to address urban safety or aging infrastructure can push tenants to suburbs; since 2023 suburban office demand climbed ~6% while CBD leasing fell in select metros, increasing OPI's geographic concentration risk.

- City redevelopment spending >$5bn correlates with -150–200 bps vacancy

- Tax abatements up to 50% boost corporate relocations

- Since 2023 suburban demand +6% vs CBD declines

- Political inaction raises tenant flight and geographic risk

Taxation and REIT Regulatory Environment

Changes to federal tax codes for REITs can materially shift OPI investor after-tax yields; for example, a 1 percentage-point rise in corporate-equivalent taxation could reduce distributable income by roughly 3–5%, impacting 2025 FFO guidance.

Political debate over corporate rates and pass-through treatment remains central in 2025, with proposals in Congress targeting rate adjustments between 21%–25% that analysts model into cash-flow forecasts.

Legislative tightening of REIT qualification or altered depreciation schedules would force OPI to reallocate capital—potentially trimming development spend by mid-single digits of NAV and revising capex plans.

- 2025 congressional proposals: corporate-equivalent rates modeled 21%–25%

- Estimated FFO hit from 1pp tax rise: ~3–5%

- Depreciation schedule changes could lower NAV by mid-single-digit percentage

High gov’t tenant exposure: public demand down 7.8%, tax hikes could cut FFO 3–5%

Government-tenant concentration (62%) exposes OPI to federal/state budget cuts; FY2024–25 agency relocations cut public-sector demand ~7.8% and federal office utilization fell to 48% (2025). City redevelopment (> $5bn) lowered vacancy 150–200 bps; suburban demand +6% since 2023. Proposed tax shifts (21–25%) could trim FFO ~3–5% per 1pp corporate-equivalent rise.

| Metric | Value |

|---|---|

| Govt tenant share | 62% |

| Public demand drop FY24–25 | 7.8% |

| Federal office utilization 2025 | 48% |

| CBD vacancy impact (>$5bn) | -150–200 bps |

| Suburban demand change since 2023 | +6% |

| FFO hit per 1pp tax rise | ~3–5% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Office Properties across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented Office Properties PESTLE summary that can be dropped into presentations or shared across teams to streamline risk discussions and align strategic planning.

Economic factors

Interest Rate Volatility and Debt Refinancing

As of late 2025, the US Fed funds target sits near 5.25–5.50%, keeping commercial mortgage spreads elevated; OPI faces higher cost of capital, with average borrowing costs for office REITs around 6.5–7.5% in 2024–25. High rates complicate refinancing of $1.2B of OPI maturing debt through 2026, pushing cap rates up ~75–150 bps and risking property value compression. Investors should stress-test OPI’s debt ladder and short-term liquidity against tighter credit conditions.

Inflationary Pressure on Operating Expenses

Persistent inflation raises property management costs—US CPI rose 3.4% in 2024, pushing labor, maintenance materials and utilities up; construction material costs were still ~7% above 2021 levels as of 2025Q1. Although many OPI leases include expense pass-throughs, sharp operating cost spikes can strain tenant relations or compress NOI on gross leases. Efficient operations and cost controls are vital to protect OPI’s dividends, given sector average NOI margins fell ~120 bps in 2024.

Corporate Footprint Rationalization

Corporate footprint rationalization is shrinking demand for traditional office space as 62% of S&P 500 firms reported plans to reduce real estate in 2025, driving vacancy rates up—US CBD office vacancy reached 18.3% in Q4 2024. OPI faces pressure to retain tenants shedding underutilized square footage by offering concessions; average tenant incentive packages rose to 8.5 months’ free rent in 2024. Competing requires targeted capex allowances and flexible lease terms to secure renewals.

Employment Trends in Professional Services

Employment in professional services—finance, tech, law—directly drives office demand; US professional and business services added 178,000 jobs in 2024, supporting leasing in core markets.

Sector-specific slowdowns trigger immediate halt in expansions and rising sublease: sublease availability in Manhattan rose ~22% YoY in 2024 amid finance layoffs.

Track regional job growth where OPI operates—MSA-level professional job growth is a reliable leading indicator for leasing pipelines and rent trajectory.

- US professional job gains: +178,000 (2024)

- Manhattan sublease availability: +22% YoY (2024)

- MSA-level professional job growth predicts leasing demand

Capital Market Liquidity and Asset Divestiture

OPI's capital recycling hinges on CRE market liquidity; in 2025 bid-ask spreads widened, slowing transactions—US office cap rates averaged ~7.5% mid-2025 versus sellers' expectations near 6.0%, reducing disposals at target prices.

Delayed asset sales impede OPI's deleveraging: Q1–Q3 2025 office transaction volumes fell ~28% YoY, constraining proceeds needed for debt paydown and funding of new initiatives.

- 2025 office transaction volumes down ~28% YoY

- Average office cap rate ~7.5% mid-2025 vs sellers' 6.0% target

- Asset sale success essential for deleveraging and funding strategy

High rates squeeze office REITs: rising cap rates, record CBD vacancies

High rates (Fed 5.25–5.50% in late 2025) raised office REIT borrowing to ~6.5–7.5%, stressing OPI’s $1.2B maturing debt through 2026 and pushing cap rates ~75–150bps higher; US CBD vacancy 18.3% (Q4 2024) with tenant incentives ~8.5 months; professional jobs +178,000 (2024) support leasing; 2025 transaction volumes -28% YoY, avg cap rate ~7.5% mid-2025.

| Metric | Value |

|---|---|

| Fed funds (late 2025) | 5.25–5.50% |

| Office REIT borrowing | 6.5–7.5% |

| CBD vacancy | 18.3% Q4 2024 |

| Tenant incentives | 8.5 months (2024) |

| Prof. jobs | +178,000 (2024) |

| Trans. volume | -28% YoY (2025) |

| Avg cap rate | ~7.5% mid-2025 |

Full Version Awaits

Office Properties PESTLE Analysis

The preview shown here is the exact Office Properties PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible here are the same document you’ll download immediately after payment.

Everything displayed is part of the final product, so what you see is precisely what you’ll own after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and technological change are reshaping Office Properties’ prospects—our concise PESTLE highlights the key external forces you need to know. Buy the full analysis for a complete, actionable breakdown with ready-to-use insights for investors, strategists, and advisors. Download now to turn external risks and opportunities into clear strategic moves.

Political factors

Government Tenant Dependency and Budgetary Shifts

The trust's 62% government-tenant concentration makes it highly sensitive to federal and state budget cycles; in FY2024–2025 agency relocations and consolidations driven by shifting fiscal priorities reduced public-sector leasing demand by an estimated 7.8%. As of late 2025, changes in political leadership and appropriations bills—Congress cut certain agency facility budgets by roughly $1.3 billion in 2025—raise risk of lease non-renewals or space reductions. Strategic planners should monitor legislative appropriations and agency-level directives to anticipate vacancies and model potential rent loss scenarios.

Federal Remote Work Policies

Federal mandates on in-person work for federal employees shape demand for OPI's specialized properties; after 2024–2025 directive shifts, vacancy in government-leased office space varied, with GSA-reported federal office utilization averaging 48% in 2025 versus 63% pre-pandemic, reducing OPI's government rental income visibility by an estimated 12–18%.

Geopolitical Impact on Corporate Strategy

Global political instability and trade tensions are prompting OPI private-sector multinationals to scale back expansion: 68% of surveyed tenants delayed site selection in 2024, per CBRE, and cross-border leasing inquiries fell 14% YoY. High-credit tenants increasingly avoid long-term commitments, driving average lease term requests down from 7.2 years (2022) to 5.1 years (2024) and boosting demand for flexible termination clauses by 32%.

Urban Policy and Infrastructure Investment

Local political initiatives to revitalize CBDs directly affect OPI's urban asset values; for example, cities allocating >$5bn in 2024–25 to downtown redevelopment saw office vacancy drop ~150–200 bps vs peers, lifting rents and NAV for nearby REITs.

Transit-oriented development incentives and corporate relocation tax breaks (e.g., abatements covering up to 50% of payroll taxes) concentrate demand in targeted clusters, improving lease-up rates and reducing cap-exposure.

Conversely, failure to address urban safety or aging infrastructure can push tenants to suburbs; since 2023 suburban office demand climbed ~6% while CBD leasing fell in select metros, increasing OPI's geographic concentration risk.

- City redevelopment spending >$5bn correlates with -150–200 bps vacancy

- Tax abatements up to 50% boost corporate relocations

- Since 2023 suburban demand +6% vs CBD declines

- Political inaction raises tenant flight and geographic risk

Taxation and REIT Regulatory Environment

Changes to federal tax codes for REITs can materially shift OPI investor after-tax yields; for example, a 1 percentage-point rise in corporate-equivalent taxation could reduce distributable income by roughly 3–5%, impacting 2025 FFO guidance.

Political debate over corporate rates and pass-through treatment remains central in 2025, with proposals in Congress targeting rate adjustments between 21%–25% that analysts model into cash-flow forecasts.

Legislative tightening of REIT qualification or altered depreciation schedules would force OPI to reallocate capital—potentially trimming development spend by mid-single digits of NAV and revising capex plans.

- 2025 congressional proposals: corporate-equivalent rates modeled 21%–25%

- Estimated FFO hit from 1pp tax rise: ~3–5%

- Depreciation schedule changes could lower NAV by mid-single-digit percentage

High gov’t tenant exposure: public demand down 7.8%, tax hikes could cut FFO 3–5%

Government-tenant concentration (62%) exposes OPI to federal/state budget cuts; FY2024–25 agency relocations cut public-sector demand ~7.8% and federal office utilization fell to 48% (2025). City redevelopment (> $5bn) lowered vacancy 150–200 bps; suburban demand +6% since 2023. Proposed tax shifts (21–25%) could trim FFO ~3–5% per 1pp corporate-equivalent rise.

| Metric | Value |

|---|---|

| Govt tenant share | 62% |

| Public demand drop FY24–25 | 7.8% |

| Federal office utilization 2025 | 48% |

| CBD vacancy impact (>$5bn) | -150–200 bps |

| Suburban demand change since 2023 | +6% |

| FFO hit per 1pp tax rise | ~3–5% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Office Properties across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented Office Properties PESTLE summary that can be dropped into presentations or shared across teams to streamline risk discussions and align strategic planning.

Economic factors

Interest Rate Volatility and Debt Refinancing

As of late 2025, the US Fed funds target sits near 5.25–5.50%, keeping commercial mortgage spreads elevated; OPI faces higher cost of capital, with average borrowing costs for office REITs around 6.5–7.5% in 2024–25. High rates complicate refinancing of $1.2B of OPI maturing debt through 2026, pushing cap rates up ~75–150 bps and risking property value compression. Investors should stress-test OPI’s debt ladder and short-term liquidity against tighter credit conditions.

Inflationary Pressure on Operating Expenses

Persistent inflation raises property management costs—US CPI rose 3.4% in 2024, pushing labor, maintenance materials and utilities up; construction material costs were still ~7% above 2021 levels as of 2025Q1. Although many OPI leases include expense pass-throughs, sharp operating cost spikes can strain tenant relations or compress NOI on gross leases. Efficient operations and cost controls are vital to protect OPI’s dividends, given sector average NOI margins fell ~120 bps in 2024.

Corporate Footprint Rationalization

Corporate footprint rationalization is shrinking demand for traditional office space as 62% of S&P 500 firms reported plans to reduce real estate in 2025, driving vacancy rates up—US CBD office vacancy reached 18.3% in Q4 2024. OPI faces pressure to retain tenants shedding underutilized square footage by offering concessions; average tenant incentive packages rose to 8.5 months’ free rent in 2024. Competing requires targeted capex allowances and flexible lease terms to secure renewals.

Employment Trends in Professional Services

Employment in professional services—finance, tech, law—directly drives office demand; US professional and business services added 178,000 jobs in 2024, supporting leasing in core markets.

Sector-specific slowdowns trigger immediate halt in expansions and rising sublease: sublease availability in Manhattan rose ~22% YoY in 2024 amid finance layoffs.

Track regional job growth where OPI operates—MSA-level professional job growth is a reliable leading indicator for leasing pipelines and rent trajectory.

- US professional job gains: +178,000 (2024)

- Manhattan sublease availability: +22% YoY (2024)

- MSA-level professional job growth predicts leasing demand

Capital Market Liquidity and Asset Divestiture

OPI's capital recycling hinges on CRE market liquidity; in 2025 bid-ask spreads widened, slowing transactions—US office cap rates averaged ~7.5% mid-2025 versus sellers' expectations near 6.0%, reducing disposals at target prices.

Delayed asset sales impede OPI's deleveraging: Q1–Q3 2025 office transaction volumes fell ~28% YoY, constraining proceeds needed for debt paydown and funding of new initiatives.

- 2025 office transaction volumes down ~28% YoY

- Average office cap rate ~7.5% mid-2025 vs sellers' 6.0% target

- Asset sale success essential for deleveraging and funding strategy

High rates squeeze office REITs: rising cap rates, record CBD vacancies

High rates (Fed 5.25–5.50% in late 2025) raised office REIT borrowing to ~6.5–7.5%, stressing OPI’s $1.2B maturing debt through 2026 and pushing cap rates ~75–150bps higher; US CBD vacancy 18.3% (Q4 2024) with tenant incentives ~8.5 months; professional jobs +178,000 (2024) support leasing; 2025 transaction volumes -28% YoY, avg cap rate ~7.5% mid-2025.

| Metric | Value |

|---|---|

| Fed funds (late 2025) | 5.25–5.50% |

| Office REIT borrowing | 6.5–7.5% |

| CBD vacancy | 18.3% Q4 2024 |

| Tenant incentives | 8.5 months (2024) |

| Prof. jobs | +178,000 (2024) |

| Trans. volume | -28% YoY (2025) |

| Avg cap rate | ~7.5% mid-2025 |

Full Version Awaits

Office Properties PESTLE Analysis

The preview shown here is the exact Office Properties PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible here are the same document you’ll download immediately after payment.

Everything displayed is part of the final product, so what you see is precisely what you’ll own after checkout.