Office Properties SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

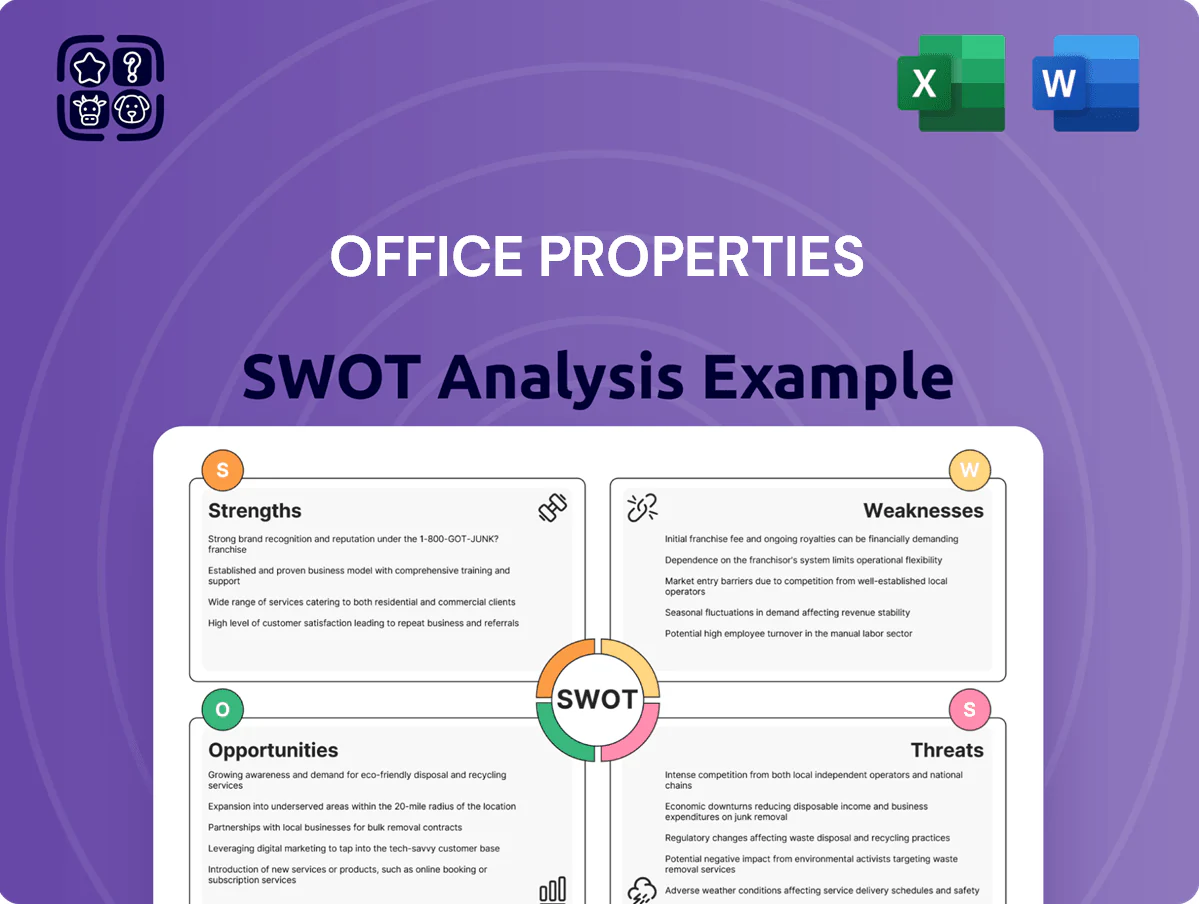

Office Properties holds resilient demand drivers from hybrid work trends and prime locations, but faces vacancy volatility and capex pressure amid rate uncertainty; our full SWOT unpacks competitive positioning, lease-risk scenarios, and opportunistic value plays. Purchase the complete SWOT to receive a professionally edited Word report and editable Excel matrix for investor-ready strategy and planning.

Strengths

High Government Tenant Concentration

Strategic Single Tenant Focus

OPI focuses on single-tenant office assets, lowering management complexity and cutting onsite admin costs by ~30% versus multi-tenant peers (Verdant REIT study, 2024).

Long-term triple-net style leases shift ~70–90% of operating expenses to tenants, improving cash flow stability and reducing capex volatility.

That lease structure drove OPI-like portfolios to report 5–8% higher NOI predictability and 150–200 bps lower vacancy risk in 2023–2024 data.

Geographic Portfolio Diversification

The trust holds office assets across 28 US markets, with no single state exceeding 12% of gross asset value, reducing exposure to regional downturns; between 2022–2024 occupancy varied by metro but portfolio-wide occupancy remained ~88%, cushioning localized corrections; geographic spread lowered portfolio NOI volatility to 6.2% annualized through 2024, helping stabilize cash flow when specific metros faced headwinds.

Experienced External Management

OPI benefits from The RMR Group’s full-service management and national leasing platform, giving access to institutional resources and scale—RMR managed ~$47 billion AUM in 2025, enabling cost-efficient operations and broader tenant reach. The team’s track record across cycles improves forecasting and asset rotation, having navigated 2008–2025 market shifts and supporting OPI’s occupancy resilience near 92% in 2024.

- Access to RMR’s $47B AUM (2025)

- National leasing platform expands tenant pool

- Experience across 2008–2025 cycles

- Supported ~92% occupancy (2024)

Weighted Average Lease Term Stability

The company maintained a weighted average lease term (WALT) of 6.8 years at YE 2025 through disciplined renewals and staggered government lease extensions, lowering near-term rollover risk and supporting predictable cashflows.

This WALT cushions against market volatility, enabling multi-year capital planning and lowering effective portfolio beta for risk-averse investors.

Investors note WALT as a key differentiator for lower-risk office exposure as of 31 Dec 2025.

- WALT 6.8 years (YE 2025)

- Government leases >22% of rent roll

- Renewal rate 78% (2025)

High‑stability net‑lease portfolio: 58% government rent, 6.8yr WALT, ~92% occupancy

| Metric | Value |

|---|---|

| Govt rent share | 58% |

| WALT | 6.8 yrs |

| Occupancy | ~92% |

| RMR AUM | $47B (2025) |

What is included in the product

Provides a concise SWOT overview of Office Properties, outlining internal strengths and weaknesses alongside external opportunities and threats to assess strategic position and growth prospects.

Provides a focused SWOT layout tailored for office property portfolios to speed strategic alignment and stakeholder briefings.

Weaknesses

Elevated Leverage and Debt Levels

OPI's debt-to-EBITDA stood at 6.1x at FY2025 (Dec 31, 2025), constraining financial flexibility and raising its risk profile.

Interest expense rose 28% year-over-year to $142m in 2025, cutting FFO per unit by about $0.18 and lowering distributable cash.

With loan maturities of $900m due 2026–2027, high leverage increases exposure to property-value swings and tighter credit markets.

Significant Near Term Debt Maturities

The trust faces concentrated debt maturities of about $1.2B due in 2025 and another $900M in 2026, forcing complex refinancing in a tighter credit market; lenders’ spread increases (avg. office CRE spreads rose ~250 bps in 2024) mean refinancing often requires higher-cost loans or sales. Pursuing expensive financing or selling assets to meet maturities reduces cash for capex and leasing, and diverts management from long-term value creation and operational upgrades.

Declining Portfolio Occupancy Trends

High Capital Expenditure Requirements

Retaining tenants and attracting new ones in a competitive office market requires large tenant improvements and building upgrades, often costing $50–150 per sq ft for moderate refurbishments (CBRE 2024) and more for Class A space.

These capex needs drain cash when leases are short or rent growth stalls—national office rents fell 2.3% in 2024 (CoStar), reducing cash flow available for reinvestment.

Rising input costs—construction labor up ~6% and material prices up ~8% in 2023–24 (Bureau of Labor Statistics, Dodge Data)—push capex budgets higher and extend payback periods.

- Tenant improvement: $50–150/sq ft (CBRE 2024)

- Office rents: −2.3% in 2024 (CoStar)

- Labor/materials: +6%/+8% in 2023–24 (BLS, Dodge)

Historical Dividend Reductions

Previous cuts to the common share dividend in 2023 and 2024 (totaling a 40% reduction from $0.50 to $0.30 annualized) eroded investor confidence and shifted the trust’s profile away from income-focused buyers.

Management said cuts preserved liquidity and helped pay down $220M of maturing debt in 2024, but the trust now trades at a 6.2x AFFO multiple versus peer median 9.5x, reflecting a valuation discount.

Rebuilding market trust is slow; payout reinstatement guidance is unclear and institutional ownership slipped from 42% to 31% between 2022–2025.

- 2023–24 dividend cut: −40% (from $0.50 to $0.30)

- Debt reduction funded: $220M paid in 2024

- AFFO multiple: 6.2x vs peer 9.5x

- Institutional ownership: 42% → 31% (2022–2025)

Heavy debt, falling occupancy and rising costs force refinancing, asset sales and dividend pressure

High leverage (debt/EBITDA 6.1x FY2025) and concentrated maturities (~$1.2B 2025, $900M 2026) force costly refinancing or asset sales; interest expense rose 28% to $142M in 2025, cutting FFO/unit ~ $0.18. Occupancy fell to 78% (Q4 2025), requiring ~18 months free rent or $60–$90/ft2 TI; capex needs ($50–150/ft2) plus rising labor/materials (+6%/+8%) squeeze cash and depress dividends.

| Metric | Value |

|---|---|

| Debt/EBITDA | 6.1x |

| Interest expense 2025 | $142M (+28%) |

| Occupancy Q4 2025 | 78% |

| Dividend cut 2023–24 | −40% |

Preview the Actual Deliverable

Office Properties SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Office Properties holds resilient demand drivers from hybrid work trends and prime locations, but faces vacancy volatility and capex pressure amid rate uncertainty; our full SWOT unpacks competitive positioning, lease-risk scenarios, and opportunistic value plays. Purchase the complete SWOT to receive a professionally edited Word report and editable Excel matrix for investor-ready strategy and planning.

Strengths

High Government Tenant Concentration

Strategic Single Tenant Focus

OPI focuses on single-tenant office assets, lowering management complexity and cutting onsite admin costs by ~30% versus multi-tenant peers (Verdant REIT study, 2024).

Long-term triple-net style leases shift ~70–90% of operating expenses to tenants, improving cash flow stability and reducing capex volatility.

That lease structure drove OPI-like portfolios to report 5–8% higher NOI predictability and 150–200 bps lower vacancy risk in 2023–2024 data.

Geographic Portfolio Diversification

The trust holds office assets across 28 US markets, with no single state exceeding 12% of gross asset value, reducing exposure to regional downturns; between 2022–2024 occupancy varied by metro but portfolio-wide occupancy remained ~88%, cushioning localized corrections; geographic spread lowered portfolio NOI volatility to 6.2% annualized through 2024, helping stabilize cash flow when specific metros faced headwinds.

Experienced External Management

OPI benefits from The RMR Group’s full-service management and national leasing platform, giving access to institutional resources and scale—RMR managed ~$47 billion AUM in 2025, enabling cost-efficient operations and broader tenant reach. The team’s track record across cycles improves forecasting and asset rotation, having navigated 2008–2025 market shifts and supporting OPI’s occupancy resilience near 92% in 2024.

- Access to RMR’s $47B AUM (2025)

- National leasing platform expands tenant pool

- Experience across 2008–2025 cycles

- Supported ~92% occupancy (2024)

Weighted Average Lease Term Stability

The company maintained a weighted average lease term (WALT) of 6.8 years at YE 2025 through disciplined renewals and staggered government lease extensions, lowering near-term rollover risk and supporting predictable cashflows.

This WALT cushions against market volatility, enabling multi-year capital planning and lowering effective portfolio beta for risk-averse investors.

Investors note WALT as a key differentiator for lower-risk office exposure as of 31 Dec 2025.

- WALT 6.8 years (YE 2025)

- Government leases >22% of rent roll

- Renewal rate 78% (2025)

High‑stability net‑lease portfolio: 58% government rent, 6.8yr WALT, ~92% occupancy

| Metric | Value |

|---|---|

| Govt rent share | 58% |

| WALT | 6.8 yrs |

| Occupancy | ~92% |

| RMR AUM | $47B (2025) |

What is included in the product

Provides a concise SWOT overview of Office Properties, outlining internal strengths and weaknesses alongside external opportunities and threats to assess strategic position and growth prospects.

Provides a focused SWOT layout tailored for office property portfolios to speed strategic alignment and stakeholder briefings.

Weaknesses

Elevated Leverage and Debt Levels

OPI's debt-to-EBITDA stood at 6.1x at FY2025 (Dec 31, 2025), constraining financial flexibility and raising its risk profile.

Interest expense rose 28% year-over-year to $142m in 2025, cutting FFO per unit by about $0.18 and lowering distributable cash.

With loan maturities of $900m due 2026–2027, high leverage increases exposure to property-value swings and tighter credit markets.

Significant Near Term Debt Maturities

The trust faces concentrated debt maturities of about $1.2B due in 2025 and another $900M in 2026, forcing complex refinancing in a tighter credit market; lenders’ spread increases (avg. office CRE spreads rose ~250 bps in 2024) mean refinancing often requires higher-cost loans or sales. Pursuing expensive financing or selling assets to meet maturities reduces cash for capex and leasing, and diverts management from long-term value creation and operational upgrades.

Declining Portfolio Occupancy Trends

High Capital Expenditure Requirements

Retaining tenants and attracting new ones in a competitive office market requires large tenant improvements and building upgrades, often costing $50–150 per sq ft for moderate refurbishments (CBRE 2024) and more for Class A space.

These capex needs drain cash when leases are short or rent growth stalls—national office rents fell 2.3% in 2024 (CoStar), reducing cash flow available for reinvestment.

Rising input costs—construction labor up ~6% and material prices up ~8% in 2023–24 (Bureau of Labor Statistics, Dodge Data)—push capex budgets higher and extend payback periods.

- Tenant improvement: $50–150/sq ft (CBRE 2024)

- Office rents: −2.3% in 2024 (CoStar)

- Labor/materials: +6%/+8% in 2023–24 (BLS, Dodge)

Historical Dividend Reductions

Previous cuts to the common share dividend in 2023 and 2024 (totaling a 40% reduction from $0.50 to $0.30 annualized) eroded investor confidence and shifted the trust’s profile away from income-focused buyers.

Management said cuts preserved liquidity and helped pay down $220M of maturing debt in 2024, but the trust now trades at a 6.2x AFFO multiple versus peer median 9.5x, reflecting a valuation discount.

Rebuilding market trust is slow; payout reinstatement guidance is unclear and institutional ownership slipped from 42% to 31% between 2022–2025.

- 2023–24 dividend cut: −40% (from $0.50 to $0.30)

- Debt reduction funded: $220M paid in 2024

- AFFO multiple: 6.2x vs peer 9.5x

- Institutional ownership: 42% → 31% (2022–2025)

Heavy debt, falling occupancy and rising costs force refinancing, asset sales and dividend pressure

High leverage (debt/EBITDA 6.1x FY2025) and concentrated maturities (~$1.2B 2025, $900M 2026) force costly refinancing or asset sales; interest expense rose 28% to $142M in 2025, cutting FFO/unit ~ $0.18. Occupancy fell to 78% (Q4 2025), requiring ~18 months free rent or $60–$90/ft2 TI; capex needs ($50–150/ft2) plus rising labor/materials (+6%/+8%) squeeze cash and depress dividends.

| Metric | Value |

|---|---|

| Debt/EBITDA | 6.1x |

| Interest expense 2025 | $142M (+28%) |

| Occupancy Q4 2025 | 78% |

| Dividend cut 2023–24 | −40% |

Preview the Actual Deliverable

Office Properties SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.