Origin Bank PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock how political shifts, economic cycles, and tech disruption are reshaping Origin Bank’s roadmap with our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable intelligence. Purchase the full PESTLE analysis to access detailed risk assessments, opportunity maps, and ready-to-use slides that accelerate smarter decisions.

Political factors

Federal Regulatory Oversight

The 2024 elections shifted federal oversight priorities, prompting the FDIC and Federal Reserve to signal higher capital buffer expectations for mid-sized banks like Origin Bank, with industry guidance suggesting CET1 targets rising toward 10–11% from prior ~9% levels. Regulatory focus on systemic risk means more frequent stress testing and operational reviews, increasing compliance costs by an estimated 5–8% of annual noninterest expenses for peers. Leadership changes at the FDIC and Fed have correlated with a 20–30% variation in M&A approval timelines, affecting Origin’s deal planning and capital deployment strategies.

Community Reinvestment Act Modernization

Tax Policy Transitions

Potential adjustments to federal corporate tax rates (current statutory rate 21% though proposals in 2024-25 debated increases) and state-level changes in Louisiana (top corporate rate 3.5% phased changes) and Texas (no corporate income tax but franchise margins tax raising effective rates) could cut net margins for Origin Bancorp, Inc. (ticker OBNK) whose 2024 net interest margin was ~3.20%, requiring forecast revisions.

State Legislative Influence

Operating across multiple states requires Origin Bank to manage a complex web of local political environments; in 2024 the bank’s regional loan portfolio grew 6.2% YoY, exposing it to divergent state legislative risks and agendas.

State decisions on infrastructure and incentives—2023 U.S. state capital spending totaled about $140 billion—influence demand for commercial loans and municipal banking services.

Maintaining strong relationships with state policymakers is essential to anticipate regulatory shifts that could affect regional economic stability and credit quality.

- Regional loan portfolio +6.2% YoY (2024)

- U.S. state capital spending ≈ $140B (2023)

- Policy engagement reduces regulatory and credit risk

International Trade and Geopolitics

Though Origin Bank is regional, disruptions in 2024—such as global shipping delays that raised US import costs by ~8% year-over-year and semiconductor shortages—can increase operating costs for its commercial clients, elevating loan default risk.

Political shifts like tariff adjustments or supply-chain sanctions may compress margins for local manufacturers, impacting their debt service capacity; Origin must track such trends to stress-test its C&I loan book.

- 2024 US import cost rise ~8% YoY

- Monitor tariff/sanction changes affecting client margins

- Stress-test C&I portfolio for supply-chain shocks

Political shifts squeeze banks: higher CET1, rising compliance costs, NIM pressure

Political shifts since 2024 raise regulatory capital expectations (CET1 target ~10–11%), increase compliance costs (~5–8% of noninterest expenses), tighten CRA exam intensity (+12%), and create state tax variability that could compress OBNK margins (2024 NIM ~3.20%; regional loans +6.2% YoY).

| Metric | Value |

|---|---|

| Target CET1 | 10–11% |

| Compliance cost rise | 5–8% |

| CRA exam intensity | +12% (2024) |

| OBNK NIM (2024) | ~3.20% |

| Regional loans YoY | +6.2% |

What is included in the product

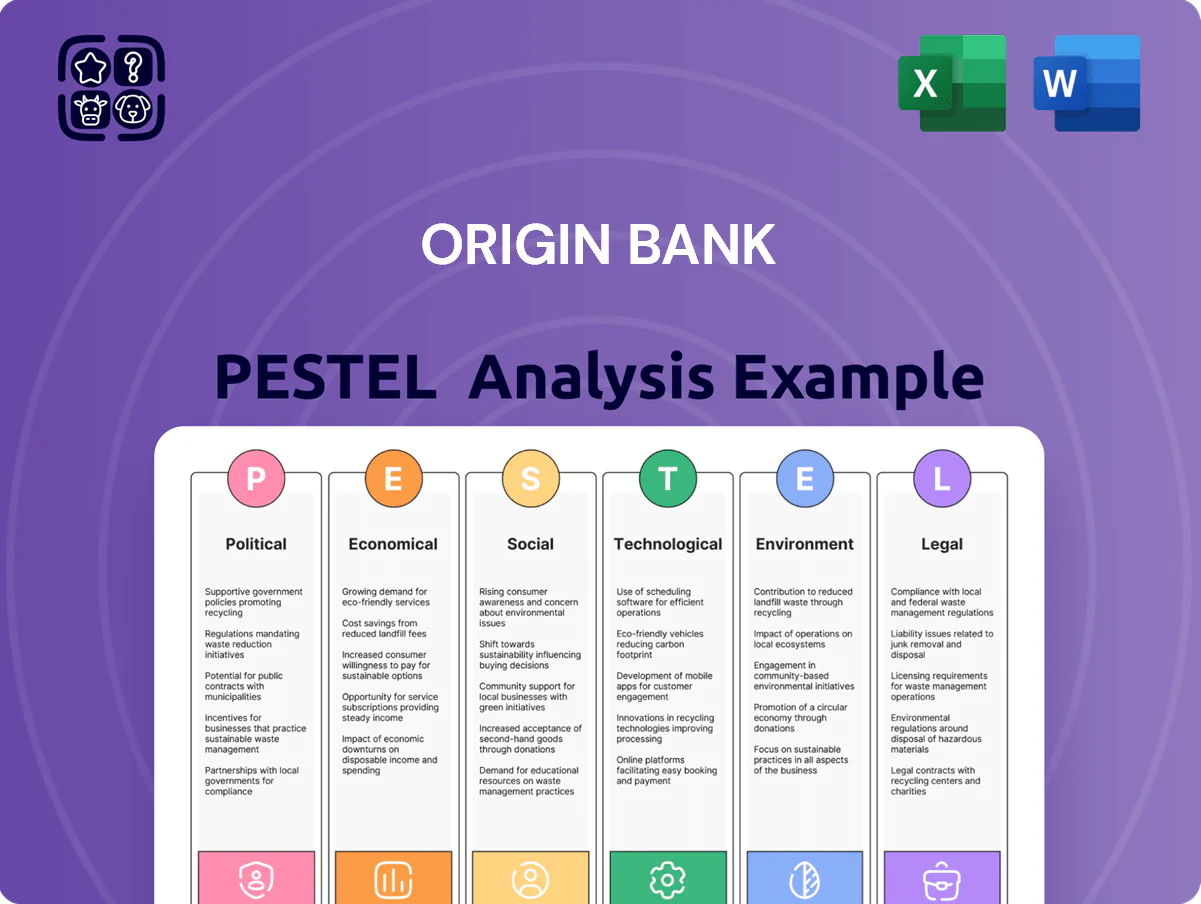

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Origin Bank, with data-driven insights and region-specific trends to identify risks and opportunities for executives, consultants, and investors.

Concise PESTLE summary tailored for Origin Bank that distills regulatory, economic, social, technological, legal, and environmental impacts into a single-slide-ready format to streamline strategic discussions and decision-making.

Economic factors

Interest Rate Environment

As of end-2025, the Fed’s pause left the effective federal funds rate near 5.25–5.50%, keeping Origin Bank’s net interest margin under pressure; industry NIMs averaged ~3.10% in 2025 vs 2.80% in 2022, highlighting yield compression. Changes in the funds rate directly shift deposit costs and loan yields across Origin’s commercial, consumer, and CRE portfolios. Origin must price deposits competitively—retail savings rate offers rose ~80–120 bps in 2024–25—while protecting margins in a maturing cycle.

Regional Economic Resilience

Origin Bank’s growth is closely tied to Gulf South economic resilience; Texas and Louisiana accounted for over 60% of its commercial loan book as of 2025, driven by energy, healthcare and tech expansion. The energy sector’s rebound—U.S. Gulf Coast oil production up ~8% YoY in 2024—and strong regional healthcare employment (Louisiana healthcare jobs +2.4% in 2024) fuel lending demand. Localized downturns, however, could raise nonperforming assets above the bank’s 0.9% NPA level and slow asset growth.

Inflationary Pressures on Operations

Persistent inflation raised US CPI to 3.4% in 2024, pushing Origin Bank's operating costs through higher wages and 6–8% vendor price inflation; controlling these expenses is vital to preserve its efficiency ratio (Industry avg ~55%) and 2024 ROA/ROE targets. Inflation can boost loan demand as borrowers seek credit ahead of rising prices, but tighter household debt-service ratios (average DSR up ~0.5ppt in 2024) strain consumer and small-business repayment capacity.

Housing Market Dynamics

- Housing sales: -9.5% YoY (2024)

- Median price: ~$392,000 (2024)

- 30-yr rate: ~6.7% (2025)

- Inventory: ~2.6 months supply

- Originations/fees: industry -18% (2024)

Labor Market Conditions

- Unemployment ~3.4% (2024)

- Deposit growth 5–7%

- Hiring cost +6% YoY

Gulf South banks face margin squeeze as rates, costs rise and housing softens

Fed funds ~5.25–5.50% (end-2025) compressing NIMs; industry NIM ~3.10% (2025). Gulf South exposure: Texas/Louisiana >60% loans; energy output +8% (2024). CPI 3.4% (2024) lifted wages/vendor costs +6–8%. Housing: existing sales -9.5% (2024), median $392k, 30-yr ~6.7% (2025). Unemployment ~3.4% (2024); deposits +5–7%.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| NIM | ~3.10% |

| CPI | 3.4% |

| Housing median | $392,000 |

Preview Before You Purchase

Origin Bank PESTLE Analysis

The preview shown here is the exact Origin Bank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock how political shifts, economic cycles, and tech disruption are reshaping Origin Bank’s roadmap with our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable intelligence. Purchase the full PESTLE analysis to access detailed risk assessments, opportunity maps, and ready-to-use slides that accelerate smarter decisions.

Political factors

Federal Regulatory Oversight

The 2024 elections shifted federal oversight priorities, prompting the FDIC and Federal Reserve to signal higher capital buffer expectations for mid-sized banks like Origin Bank, with industry guidance suggesting CET1 targets rising toward 10–11% from prior ~9% levels. Regulatory focus on systemic risk means more frequent stress testing and operational reviews, increasing compliance costs by an estimated 5–8% of annual noninterest expenses for peers. Leadership changes at the FDIC and Fed have correlated with a 20–30% variation in M&A approval timelines, affecting Origin’s deal planning and capital deployment strategies.

Community Reinvestment Act Modernization

Tax Policy Transitions

Potential adjustments to federal corporate tax rates (current statutory rate 21% though proposals in 2024-25 debated increases) and state-level changes in Louisiana (top corporate rate 3.5% phased changes) and Texas (no corporate income tax but franchise margins tax raising effective rates) could cut net margins for Origin Bancorp, Inc. (ticker OBNK) whose 2024 net interest margin was ~3.20%, requiring forecast revisions.

State Legislative Influence

Operating across multiple states requires Origin Bank to manage a complex web of local political environments; in 2024 the bank’s regional loan portfolio grew 6.2% YoY, exposing it to divergent state legislative risks and agendas.

State decisions on infrastructure and incentives—2023 U.S. state capital spending totaled about $140 billion—influence demand for commercial loans and municipal banking services.

Maintaining strong relationships with state policymakers is essential to anticipate regulatory shifts that could affect regional economic stability and credit quality.

- Regional loan portfolio +6.2% YoY (2024)

- U.S. state capital spending ≈ $140B (2023)

- Policy engagement reduces regulatory and credit risk

International Trade and Geopolitics

Though Origin Bank is regional, disruptions in 2024—such as global shipping delays that raised US import costs by ~8% year-over-year and semiconductor shortages—can increase operating costs for its commercial clients, elevating loan default risk.

Political shifts like tariff adjustments or supply-chain sanctions may compress margins for local manufacturers, impacting their debt service capacity; Origin must track such trends to stress-test its C&I loan book.

- 2024 US import cost rise ~8% YoY

- Monitor tariff/sanction changes affecting client margins

- Stress-test C&I portfolio for supply-chain shocks

Political shifts squeeze banks: higher CET1, rising compliance costs, NIM pressure

Political shifts since 2024 raise regulatory capital expectations (CET1 target ~10–11%), increase compliance costs (~5–8% of noninterest expenses), tighten CRA exam intensity (+12%), and create state tax variability that could compress OBNK margins (2024 NIM ~3.20%; regional loans +6.2% YoY).

| Metric | Value |

|---|---|

| Target CET1 | 10–11% |

| Compliance cost rise | 5–8% |

| CRA exam intensity | +12% (2024) |

| OBNK NIM (2024) | ~3.20% |

| Regional loans YoY | +6.2% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Origin Bank, with data-driven insights and region-specific trends to identify risks and opportunities for executives, consultants, and investors.

Concise PESTLE summary tailored for Origin Bank that distills regulatory, economic, social, technological, legal, and environmental impacts into a single-slide-ready format to streamline strategic discussions and decision-making.

Economic factors

Interest Rate Environment

As of end-2025, the Fed’s pause left the effective federal funds rate near 5.25–5.50%, keeping Origin Bank’s net interest margin under pressure; industry NIMs averaged ~3.10% in 2025 vs 2.80% in 2022, highlighting yield compression. Changes in the funds rate directly shift deposit costs and loan yields across Origin’s commercial, consumer, and CRE portfolios. Origin must price deposits competitively—retail savings rate offers rose ~80–120 bps in 2024–25—while protecting margins in a maturing cycle.

Regional Economic Resilience

Origin Bank’s growth is closely tied to Gulf South economic resilience; Texas and Louisiana accounted for over 60% of its commercial loan book as of 2025, driven by energy, healthcare and tech expansion. The energy sector’s rebound—U.S. Gulf Coast oil production up ~8% YoY in 2024—and strong regional healthcare employment (Louisiana healthcare jobs +2.4% in 2024) fuel lending demand. Localized downturns, however, could raise nonperforming assets above the bank’s 0.9% NPA level and slow asset growth.

Inflationary Pressures on Operations

Persistent inflation raised US CPI to 3.4% in 2024, pushing Origin Bank's operating costs through higher wages and 6–8% vendor price inflation; controlling these expenses is vital to preserve its efficiency ratio (Industry avg ~55%) and 2024 ROA/ROE targets. Inflation can boost loan demand as borrowers seek credit ahead of rising prices, but tighter household debt-service ratios (average DSR up ~0.5ppt in 2024) strain consumer and small-business repayment capacity.

Housing Market Dynamics

- Housing sales: -9.5% YoY (2024)

- Median price: ~$392,000 (2024)

- 30-yr rate: ~6.7% (2025)

- Inventory: ~2.6 months supply

- Originations/fees: industry -18% (2024)

Labor Market Conditions

- Unemployment ~3.4% (2024)

- Deposit growth 5–7%

- Hiring cost +6% YoY

Gulf South banks face margin squeeze as rates, costs rise and housing softens

Fed funds ~5.25–5.50% (end-2025) compressing NIMs; industry NIM ~3.10% (2025). Gulf South exposure: Texas/Louisiana >60% loans; energy output +8% (2024). CPI 3.4% (2024) lifted wages/vendor costs +6–8%. Housing: existing sales -9.5% (2024), median $392k, 30-yr ~6.7% (2025). Unemployment ~3.4% (2024); deposits +5–7%.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| NIM | ~3.10% |

| CPI | 3.4% |

| Housing median | $392,000 |

Preview Before You Purchase

Origin Bank PESTLE Analysis

The preview shown here is the exact Origin Bank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.