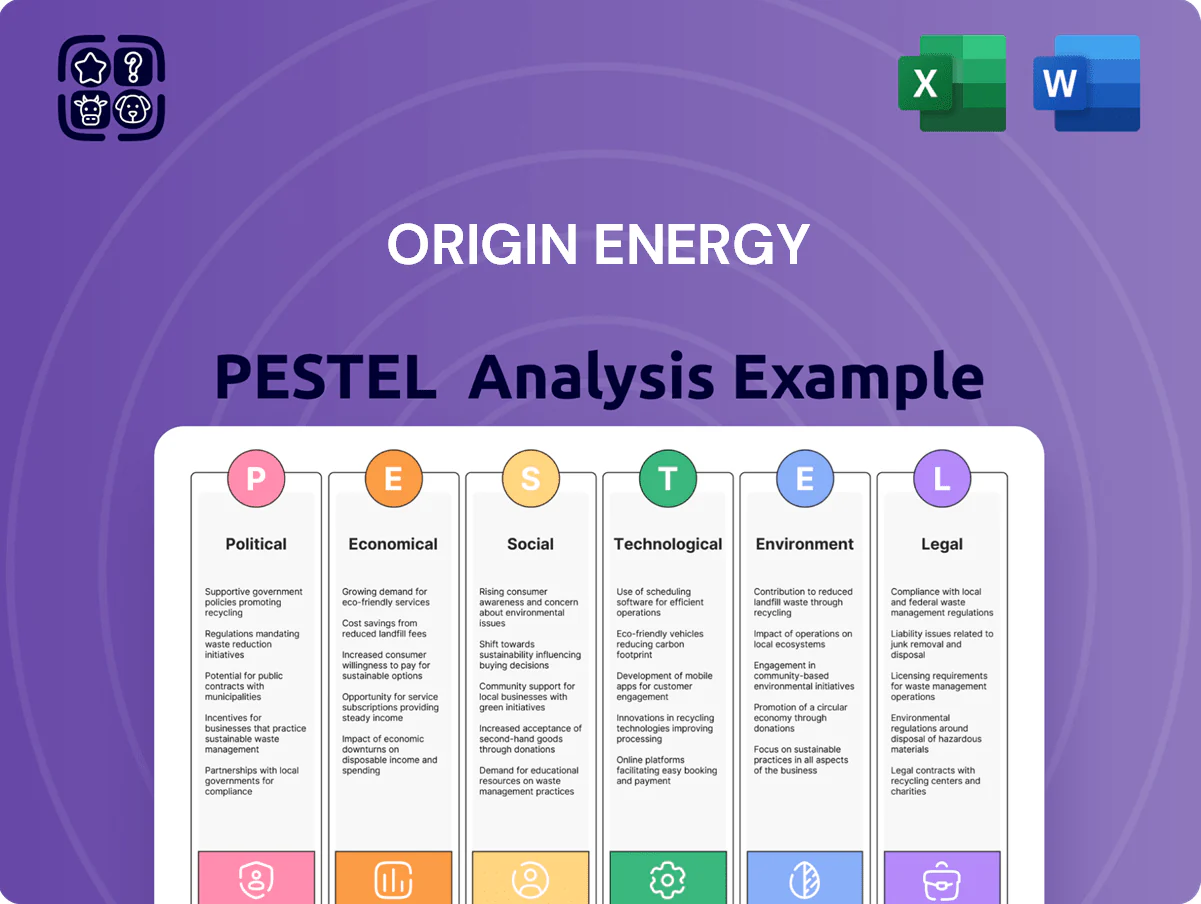

Origin Energy PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE Analysis of Origin Energy—concise, timely insights into political, economic, social, technological, legal, and environmental forces shaping the company’s future; buy the full report to access actionable intelligence and strengthen your decisions.

Political factors

Federal Decarbonization Policy Alignment

The federal government’s strengthened 2030 target—reducing emissions by 43% from 2005 levels—and A$20 billion Rewiring the Nation/renewables funding has forced Origin Energy to accelerate coal phase-out, redirecting capex: Origin committed A$8–10bn to renewables and storage through 2030, prioritizing wind, utility-scale solar and batteries over fossil expansion as policy frameworks now favor low-carbon infrastructure.

Domestic Gas Reservation and Pricing Policies

Geopolitical Influence on LNG Export Markets

Origin Energy depends on stable trade with Asian buyers—China and Japan account for roughly 60% of Australian LNG exports—so diplomatic strains risk demand shocks and price volatility for its ~A$7–10bn export-related asset base.

Shifts in trade policy or sanctions could disrupt supply chains, affecting long-term contracts that underpin ~40–50% of Origin’s projected export cash flows.

State-Level Renewable Energy Zone Planning

The development of Renewable Energy Zones in New South Wales and Queensland determines viable sites for Origin Energy’s new wind, solar and storage projects by providing transmission corridors—NSW REZ roadmap targets 12 GW by 2030 and Queensland aims for ~9 GW by 2035, shaping Origin’s siting choices and timelines.

These state initiatives supply grid build‑out but create competition for limited grid connections and land rights, elevating project bid costs and requiring Origin to secure allocation in auctions and network access agreements.

Aligning Origin’s project pipeline with state infrastructure roadmaps is critical to meet delivery schedules and avoid curtailment; leveraging NSW and QLD REZ timelines can reduce interconnection risk and capex overruns.

- NSW REZ: 12 GW target by 2030; QLD REZ: ~9 GW by 2035

- Increased competition for grid slots raises bid prices and land costs

- Strategic alignment with state roadmaps lowers interconnection and delivery risk

Government Incentives for Green Hydrogen

Political support for a hydrogen economy gives Origin access to subsidies and grants—Australia committed A$2 billion by 2030 to hydrogen industry development, with federal H2Future Fund rounds offering multi‑million-dollar co‑funding for pilots Origin is exploring.

Federal and state programs (e.g., NSW A$70 million Hydrogen Strategy funding) reduce upfront costs for high‑capex pilot projects, improving project IRRs and lowering breakeven for green hydrogen production.

Capturing these incentives is critical for Origin to secure first‑mover advantages in the low‑emissions fuel market and scale green hydrogen capacity ahead of competitors.

- Australia A$2bn federal commitment to 2030 for hydrogen

- NSW A$70m state funding example

- Multi‑million H2Future Fund co‑funding for pilots

- Incentives lower capex barriers and improve pilot project IRRs

Origin pivots: A$8–10bn renewables push amid gas margin, REZ and hydrogen policy risks

Federal 2030 target (‑43% vs 2005) and A$20bn Rewiring the Nation push Origin to allocate A$8–10bn to renewables/storage to 2030; gas price caps/domestic reservation (proposals 10–20%) threaten margins on Origin’s ~35 PJ FY2024 gas and 37.5% APLNG stake; NSW/QLD REZs (NSW 12 GW by 2030; QLD ~9 GW by 2035) shape siting and grid access; A$2bn federal hydrogen pledge plus NSW A$70m funds lower pilot capex.

| Metric | Value |

|---|---|

| Renewables capex commitment | A$8–10bn to 2030 |

| FY2024 gas production | ~35 PJ |

| APLNG stake | 37.5% |

| NSW REZ target | 12 GW by 2030 |

| QLD REZ target | ~9 GW by 2035 |

| Federal hydrogen fund | A$2bn to 2030 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Origin Energy, with each section supported by current data and trends to identify strategic threats and opportunities.

A concise, PESTLE-segmented summary of Origin Energy's external landscape, designed for quick reference in meetings or presentations to streamline risk discussions and strategic planning.

Economic factors

Global Commodity Price Volatility

As a major LNG exporter, Origin Energy faces high exposure to oil and gas benchmark swings—Henry Hub and Brent price moves drove LNG spot prices from ~USD 7/MMBtu in 2023 to spikes above USD 15/MMBtu in 2024, creating revenue volatility for its integrated gas segment. Demand shifts in Asia and Europe can swing annual EBITDA by hundreds of millions; Origin reported net gas revenue sensitivity of ~AUD 200–400m per USD 1/MMBtu in 2024 estimates. Management therefore uses dynamic hedging and contract mix adjustments to shield the balance sheet from sudden international price drops, with reported hedge coverage rising to ~60% of 2025 volumes by end-2024.

Interest Rate Impact on Capital Projects

As of late 2025, the Reserve Bank of Australia cash rate at 4.50% has pushed corporate borrowing costs higher, raising Origin Energy’s weighted average cost of debt and increasing hurdle rates for renewables and battery projects with capital intensity over A$500m. Higher rates could slow project sanctioning, as financing costs lift levelized costs; Origin must optimize its A$6–8bn multi‑year pipeline financing mix and protect its investment‑grade credit metrics to secure affordable capital.

Retail Margin Pressure and Inflation

Persistently high inflation (Australia CPI 5.4% year‑on‑year to Dec 2024) has raised Origin Energy's retail operating costs across contact centers, field crews and maintenance, squeezing gross margins that fell 120 basis points in FY2024 retail operations.

Simultaneously, cost‑of‑living pressures—household real incomes down and consumer energy bill sensitivity—limit Origin’s ability to fully pass through higher costs without triggering churn; retail customer switching rose ~8% in 2024.

Balancing competitive pricing to retain ~4.1 million customers while restoring healthy retail margins remains a core economic challenge amid elevated inflation and wholesale price volatility.

Exchange Rate Sensitivity

Because LNG sales are largely USD-denominated while many costs are in AUD, a stronger Australian dollar erodes AUD value of export receipts; in 2024 Origin received A$1.1bn from Australia Pacific LNG, a figure sensitive to USD/AUD moves.

Origin must hedge currency exposure to protect margins and dividend flows to shareholders; a 10% AUD appreciation versus USD in 2024 would cut USD-linked earnings by roughly A$110m on that A$1.1bn base.

- USD pricing vs AUD costs

- A$1.1bn 2024 receipts from APLNG

- 10% AUD appreciation ≈ A$110m impact

- Hedging needed for dividend stability

Investment in Virtual Power Plants

The economic viability of Virtual Power Plants lets Origin Energy aggregate household solar and batteries—Origin reported managing 60+ MW of distributed energy resources by 2024—reducing exposure to wholesale peak prices which spiked to over AUD 300/MWh during some 2023 summer intervals.

By leveraging customer assets, Origin lowers marginal supply costs and defers large centralized generation CAPEX, improving customer asset value and cutting wholesale procurement spend.

- Origin managing 60+ MW DER by 2024

- Wholesale peaks > AUD 300/MWh in 2023 summer

- Reduced CAPEX versus new centralized plants

Origin faces LNG price swings, AUD impact and higher rates squeezing project returns

Origin’s LNG revenue swings with Henry Hub/Brent; ~USD 7→15/MMBtu 2023–24 drove volatility, net gas revenue sensitivity ~AUD 200–400m per USD 1/MMBtu and hedge coverage ~60% for 2025. RBA cash rate 4.50% (late 2025) raises WACC, impacting A$6–8bn project pipeline; CPI 5.4% (Dec 2024) squeezed retail margins down ~120bps. APLNG receipts A$1.1bn (2024); 10% AUD appreciation ≈ A$110m hit; Origin managed 60+ MW DER by 2024, reducing peak procurement exposure.

| Metric | Value |

|---|---|

| Gas price move 2023–24 | USD 7→15/MMBtu |

| Revenue sensitivity | AUD 200–400m per USD 1/MMBtu |

| Hedge coverage (end‑2024) | ~60% of 2025 volumes |

| RBA cash rate (late 2025) | 4.50% |

| CPI (Dec 2024) | 5.4% YoY |

| APLNG receipts (2024) | A$1.1bn |

| DER managed (2024) | 60+ MW |

Same Document Delivered

Origin Energy PESTLE Analysis

The preview shown here is the exact Origin Energy PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible are identical to the downloadable file, with no placeholders or teasers.

What you see is the final, professionally structured report available instantly after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE Analysis of Origin Energy—concise, timely insights into political, economic, social, technological, legal, and environmental forces shaping the company’s future; buy the full report to access actionable intelligence and strengthen your decisions.

Political factors

Federal Decarbonization Policy Alignment

The federal government’s strengthened 2030 target—reducing emissions by 43% from 2005 levels—and A$20 billion Rewiring the Nation/renewables funding has forced Origin Energy to accelerate coal phase-out, redirecting capex: Origin committed A$8–10bn to renewables and storage through 2030, prioritizing wind, utility-scale solar and batteries over fossil expansion as policy frameworks now favor low-carbon infrastructure.

Domestic Gas Reservation and Pricing Policies

Geopolitical Influence on LNG Export Markets

Origin Energy depends on stable trade with Asian buyers—China and Japan account for roughly 60% of Australian LNG exports—so diplomatic strains risk demand shocks and price volatility for its ~A$7–10bn export-related asset base.

Shifts in trade policy or sanctions could disrupt supply chains, affecting long-term contracts that underpin ~40–50% of Origin’s projected export cash flows.

State-Level Renewable Energy Zone Planning

The development of Renewable Energy Zones in New South Wales and Queensland determines viable sites for Origin Energy’s new wind, solar and storage projects by providing transmission corridors—NSW REZ roadmap targets 12 GW by 2030 and Queensland aims for ~9 GW by 2035, shaping Origin’s siting choices and timelines.

These state initiatives supply grid build‑out but create competition for limited grid connections and land rights, elevating project bid costs and requiring Origin to secure allocation in auctions and network access agreements.

Aligning Origin’s project pipeline with state infrastructure roadmaps is critical to meet delivery schedules and avoid curtailment; leveraging NSW and QLD REZ timelines can reduce interconnection risk and capex overruns.

- NSW REZ: 12 GW target by 2030; QLD REZ: ~9 GW by 2035

- Increased competition for grid slots raises bid prices and land costs

- Strategic alignment with state roadmaps lowers interconnection and delivery risk

Government Incentives for Green Hydrogen

Political support for a hydrogen economy gives Origin access to subsidies and grants—Australia committed A$2 billion by 2030 to hydrogen industry development, with federal H2Future Fund rounds offering multi‑million-dollar co‑funding for pilots Origin is exploring.

Federal and state programs (e.g., NSW A$70 million Hydrogen Strategy funding) reduce upfront costs for high‑capex pilot projects, improving project IRRs and lowering breakeven for green hydrogen production.

Capturing these incentives is critical for Origin to secure first‑mover advantages in the low‑emissions fuel market and scale green hydrogen capacity ahead of competitors.

- Australia A$2bn federal commitment to 2030 for hydrogen

- NSW A$70m state funding example

- Multi‑million H2Future Fund co‑funding for pilots

- Incentives lower capex barriers and improve pilot project IRRs

Origin pivots: A$8–10bn renewables push amid gas margin, REZ and hydrogen policy risks

Federal 2030 target (‑43% vs 2005) and A$20bn Rewiring the Nation push Origin to allocate A$8–10bn to renewables/storage to 2030; gas price caps/domestic reservation (proposals 10–20%) threaten margins on Origin’s ~35 PJ FY2024 gas and 37.5% APLNG stake; NSW/QLD REZs (NSW 12 GW by 2030; QLD ~9 GW by 2035) shape siting and grid access; A$2bn federal hydrogen pledge plus NSW A$70m funds lower pilot capex.

| Metric | Value |

|---|---|

| Renewables capex commitment | A$8–10bn to 2030 |

| FY2024 gas production | ~35 PJ |

| APLNG stake | 37.5% |

| NSW REZ target | 12 GW by 2030 |

| QLD REZ target | ~9 GW by 2035 |

| Federal hydrogen fund | A$2bn to 2030 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Origin Energy, with each section supported by current data and trends to identify strategic threats and opportunities.

A concise, PESTLE-segmented summary of Origin Energy's external landscape, designed for quick reference in meetings or presentations to streamline risk discussions and strategic planning.

Economic factors

Global Commodity Price Volatility

As a major LNG exporter, Origin Energy faces high exposure to oil and gas benchmark swings—Henry Hub and Brent price moves drove LNG spot prices from ~USD 7/MMBtu in 2023 to spikes above USD 15/MMBtu in 2024, creating revenue volatility for its integrated gas segment. Demand shifts in Asia and Europe can swing annual EBITDA by hundreds of millions; Origin reported net gas revenue sensitivity of ~AUD 200–400m per USD 1/MMBtu in 2024 estimates. Management therefore uses dynamic hedging and contract mix adjustments to shield the balance sheet from sudden international price drops, with reported hedge coverage rising to ~60% of 2025 volumes by end-2024.

Interest Rate Impact on Capital Projects

As of late 2025, the Reserve Bank of Australia cash rate at 4.50% has pushed corporate borrowing costs higher, raising Origin Energy’s weighted average cost of debt and increasing hurdle rates for renewables and battery projects with capital intensity over A$500m. Higher rates could slow project sanctioning, as financing costs lift levelized costs; Origin must optimize its A$6–8bn multi‑year pipeline financing mix and protect its investment‑grade credit metrics to secure affordable capital.

Retail Margin Pressure and Inflation

Persistently high inflation (Australia CPI 5.4% year‑on‑year to Dec 2024) has raised Origin Energy's retail operating costs across contact centers, field crews and maintenance, squeezing gross margins that fell 120 basis points in FY2024 retail operations.

Simultaneously, cost‑of‑living pressures—household real incomes down and consumer energy bill sensitivity—limit Origin’s ability to fully pass through higher costs without triggering churn; retail customer switching rose ~8% in 2024.

Balancing competitive pricing to retain ~4.1 million customers while restoring healthy retail margins remains a core economic challenge amid elevated inflation and wholesale price volatility.

Exchange Rate Sensitivity

Because LNG sales are largely USD-denominated while many costs are in AUD, a stronger Australian dollar erodes AUD value of export receipts; in 2024 Origin received A$1.1bn from Australia Pacific LNG, a figure sensitive to USD/AUD moves.

Origin must hedge currency exposure to protect margins and dividend flows to shareholders; a 10% AUD appreciation versus USD in 2024 would cut USD-linked earnings by roughly A$110m on that A$1.1bn base.

- USD pricing vs AUD costs

- A$1.1bn 2024 receipts from APLNG

- 10% AUD appreciation ≈ A$110m impact

- Hedging needed for dividend stability

Investment in Virtual Power Plants

The economic viability of Virtual Power Plants lets Origin Energy aggregate household solar and batteries—Origin reported managing 60+ MW of distributed energy resources by 2024—reducing exposure to wholesale peak prices which spiked to over AUD 300/MWh during some 2023 summer intervals.

By leveraging customer assets, Origin lowers marginal supply costs and defers large centralized generation CAPEX, improving customer asset value and cutting wholesale procurement spend.

- Origin managing 60+ MW DER by 2024

- Wholesale peaks > AUD 300/MWh in 2023 summer

- Reduced CAPEX versus new centralized plants

Origin faces LNG price swings, AUD impact and higher rates squeezing project returns

Origin’s LNG revenue swings with Henry Hub/Brent; ~USD 7→15/MMBtu 2023–24 drove volatility, net gas revenue sensitivity ~AUD 200–400m per USD 1/MMBtu and hedge coverage ~60% for 2025. RBA cash rate 4.50% (late 2025) raises WACC, impacting A$6–8bn project pipeline; CPI 5.4% (Dec 2024) squeezed retail margins down ~120bps. APLNG receipts A$1.1bn (2024); 10% AUD appreciation ≈ A$110m hit; Origin managed 60+ MW DER by 2024, reducing peak procurement exposure.

| Metric | Value |

|---|---|

| Gas price move 2023–24 | USD 7→15/MMBtu |

| Revenue sensitivity | AUD 200–400m per USD 1/MMBtu |

| Hedge coverage (end‑2024) | ~60% of 2025 volumes |

| RBA cash rate (late 2025) | 4.50% |

| CPI (Dec 2024) | 5.4% YoY |

| APLNG receipts (2024) | A$1.1bn |

| DER managed (2024) | 60+ MW |

Same Document Delivered

Origin Energy PESTLE Analysis

The preview shown here is the exact Origin Energy PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible are identical to the downloadable file, with no placeholders or teasers.

What you see is the final, professionally structured report available instantly after checkout.