Origin Enterprises Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Origin Enterprises operates in a fragmented, input-driven agribusiness sector where supplier bargaining, regulatory shifts, and commodity volatility shape margins; our snapshot highlights key threats like price-sensitive buyers and potential substitutes from integrated agri-platforms. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to Origin Enterprises.

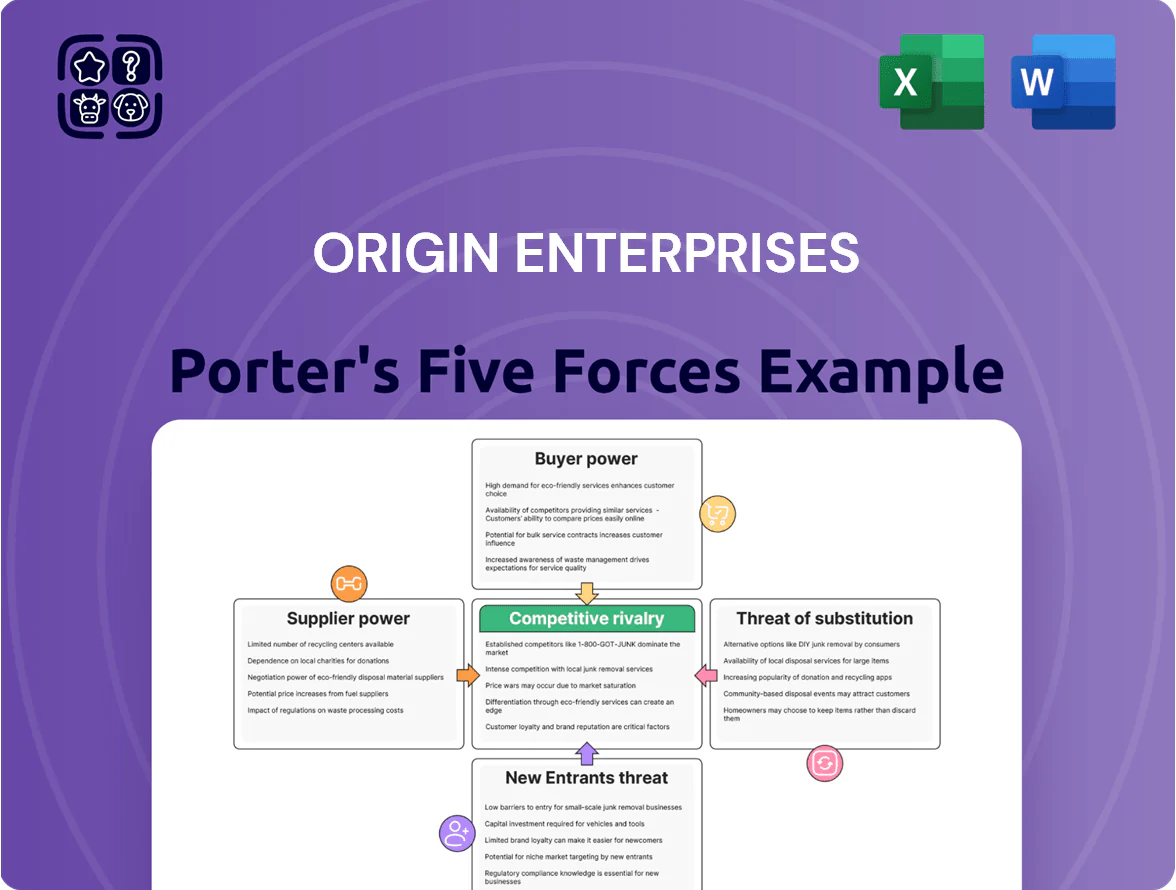

Suppliers Bargaining Power

Concentration of Global Agrochemical Manufacturers

Origin Enterprises depends on a handful of global agrochemical firms for crop protection and specialty seeds, giving suppliers strong pricing power; top five agrochemical companies held about 65% of global crop protection sales in 2024 (source: CRU/industry reports).

Volatility in Raw Material Costs

Fertilizer costs track natural gas and commodity swings; ammonia-linked nitrogen rose 42% in 2022–23 after gas shocks, and global MAP/DAP prices spiked ~30% in 2022, letting NPK suppliers pass increases to distributors like Origin Enterprises plc (IRE:OGN).

During 2022–24 geopolitical instability suppliers exercised pricing power, squeezing Origin’s gross margin — Origin reported a 2023 gross margin decline of ~1.2 percentage points as it absorbed some input inflation.

Specialized Technology and Digital Integration

Suppliers now bundle proprietary digital platforms and precision tools with inputs, creating technical lock-in that forces Origin Enterprises to keep close ties with key providers to deliver high-tech farm solutions; global ag-tech spending hit about $10.5bn in 2024, boosting supplier leverage. The specialized biological inputs and integrated software raise switching costs and can pressure Origin’s margins and service flexibility.

Logistical and Supply Chain Dependencies

Origin’s reliance on heavy, bulky inputs makes it vulnerable to logistics: ocean freight rates jumped 42% in 2021–22 and container shortages since have increased delivery variability, raising working capital tied to inventory.

Global shipping slowdowns or UK/EU road transport strikes can delay seasonal seed and fertiliser windows by days; a 5–10 day slip often cuts effective planting uptake and revenue.

- High freight cost volatility (+42% spike)

- Narrow seasonal windows amplify delays

- Local transport outages cause outsized service risk

Regulatory Compliance and Product Approval

Suppliers must navigate complex EU and local rules on chemical safety and environmental impact, including REACH and national pesticide authorisations, which in 2024 saw 18% more rejections across the bloc, raising compliance costs for suppliers and downstream buyers like Origin Enterprises.

Origin depends on suppliers to supply compliant, effective inputs as older actives are phased out; supplier R&D and approval pipelines thus directly affect Origin’s product mix and gross margin on crop nutrition and crop protection lines.

If a major supplier fails to secure approval for a replacement active, Origin could face a rapid portfolio gap that is hard to fill—industry estimates show a 9–12 month average lag to qualify alternative products and potential revenue at risk of up to 6% of segment sales.

- REACH and national approvals: higher rejection (+18% in 2024)

- Approval lag: 9–12 months to qualify alternatives

- Revenue risk: up to 6% of segment sales if supplier fails approval

- Origin reliance: dependent on supplier R&D and compliant pipelines

Supplier dominance, soaring input costs & regulatory drag squeeze agrochemical margins

Suppliers hold strong power: top 5 agrochemical firms ~65% market share (2024), fertilizer prices spiked (ammonia-linked N +42% in 2022–23), and ag‑tech bundling raised switching costs; Origin saw ~1.2ppt gross‑margin hit in 2023. Regulatory rejections rose 18% (EU 2024), approval lag 9–12 months, revenue at risk ~6% of segment sales.

| Metric | Value |

|---|---|

| Top‑5 share (2024) | 65% |

| Ammonia N price jump | +42% |

| Gross‑margin hit (Origin 2023) | −1.2ppt |

| EU rejections (2024) | +18% |

| Approval lag | 9–12 months |

| Revenue risk | ~6% |

What is included in the product

Tailored Porter's Five Forces for Origin Enterprises highlighting competitive rivalry, supplier and buyer bargaining power, threats from new entrants and substitutes, and strategic levers to protect margins and market share.

A concise Porter's Five Forces one-sheet for Origin Enterprises—quickly spot competitive threats and relief strategies to streamline boardroom decisions.

Customers Bargaining Power

Fragmented Farmer Base

The majority of Origin Enterprises customers are individual professional farmers and mid-sized agricultural firms, which weakens individual bargaining power and lets Origin keep diverse revenues; in FY2024 retail agronomy sales, ~62% of revenue came from small-to-mid clients. Large farm estates still secure better terms, but growing farmer cooperatives—estimated to cover ~18% of UK/Ireland arable hectares in 2024—are aggregating buying power and pressuring prices.

High Price Sensitivity to Input Costs

Farmers run on thin margins—EU arable margins fell ~12% in 2024, so Origin faces strong price pressure when wheat/corn prices drop; growers demanded discounts in 2024 after EU wheat futures slid ~18% year-on-year. This pushes Origin to prove ROI from agronomy services—Average yield uplifts of 5–10% (field trials 2023–24) become key to justify pricing. Loss of perceived value risks churn and volume-based margin erosion.

Low Switching Costs for Physical Inputs

While Origin Enterprises’ agronomy advice drives loyalty, fertilizers and standard seeds act as commodities with low switching costs; industry data shows agrochemical margins compressed to ~12–15% in 2024, making price the key driver for farmers.

Farmers can and do switch to local suppliers for identical brands or generics; surveys in 2023 found 48% of EU arable farmers cite price as primary purchase factor.

Therefore Origin’s advisory and digital services—adoption of its digital platform by ~220,000 users in 2024—are essential to create stickiness and protect revenue.

Access to Market Information

- Real-time pricing reduces info gap

- 42% seek multiple quotes (2024, EU/UK)

- Pressure on Origin margins and transparency

- Need for published price breakdowns

Adoption of Direct-to-Farm Digital Sales

The rise of direct-to-farm digital marketplaces lets farmers bypass distributors for standardized inputs; online platforms grew 28% YoY in agri-input sales in 2024, pressuring Origin Enterprises’ margins.

Tech-savvy farmers now seek advisory from Origin but buy bulk inputs cheaper online, with 42% of UK arable farmers using e‑commerce in 2024; Origin must bundle services and products to retain loyalty.

- Online agri-input sales +28% in 2024

- 42% UK arable farmers used e‑commerce in 2024

- Bundle advisory with inputs to protect margin

Rising farmer price power and online sales force Origin to bundle services to protect margins

Customers’ bargaining power is rising: 42% of EU/UK arable farmers sought multiple quotes in 2024 and 48% cite price as top factor, while online agri‑input sales grew 28% YoY; Origin offsets this with advisory stickiness—220,000 digital users in 2024—and must bundle services to protect margins (fertilizer margins ~12–15% in 2024).

| Metric | 2024 |

|---|---|

| Multi‑quote farmers | 42% |

| Price‑first farmers | 48% |

| Online input sales YoY | +28% |

| Digital users | 220,000 |

| Agrochemical margins | 12–15% |

Preview the Actual Deliverable

Origin Enterprises Porter's Five Forces Analysis

This preview shows the exact Origin Enterprises Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you buy; it contains the complete Five Forces assessment, supporting evidence, and concise implications for strategy and valuation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Origin Enterprises operates in a fragmented, input-driven agribusiness sector where supplier bargaining, regulatory shifts, and commodity volatility shape margins; our snapshot highlights key threats like price-sensitive buyers and potential substitutes from integrated agri-platforms. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to Origin Enterprises.

Suppliers Bargaining Power

Concentration of Global Agrochemical Manufacturers

Origin Enterprises depends on a handful of global agrochemical firms for crop protection and specialty seeds, giving suppliers strong pricing power; top five agrochemical companies held about 65% of global crop protection sales in 2024 (source: CRU/industry reports).

Volatility in Raw Material Costs

Fertilizer costs track natural gas and commodity swings; ammonia-linked nitrogen rose 42% in 2022–23 after gas shocks, and global MAP/DAP prices spiked ~30% in 2022, letting NPK suppliers pass increases to distributors like Origin Enterprises plc (IRE:OGN).

During 2022–24 geopolitical instability suppliers exercised pricing power, squeezing Origin’s gross margin — Origin reported a 2023 gross margin decline of ~1.2 percentage points as it absorbed some input inflation.

Specialized Technology and Digital Integration

Suppliers now bundle proprietary digital platforms and precision tools with inputs, creating technical lock-in that forces Origin Enterprises to keep close ties with key providers to deliver high-tech farm solutions; global ag-tech spending hit about $10.5bn in 2024, boosting supplier leverage. The specialized biological inputs and integrated software raise switching costs and can pressure Origin’s margins and service flexibility.

Logistical and Supply Chain Dependencies

Origin’s reliance on heavy, bulky inputs makes it vulnerable to logistics: ocean freight rates jumped 42% in 2021–22 and container shortages since have increased delivery variability, raising working capital tied to inventory.

Global shipping slowdowns or UK/EU road transport strikes can delay seasonal seed and fertiliser windows by days; a 5–10 day slip often cuts effective planting uptake and revenue.

- High freight cost volatility (+42% spike)

- Narrow seasonal windows amplify delays

- Local transport outages cause outsized service risk

Regulatory Compliance and Product Approval

Suppliers must navigate complex EU and local rules on chemical safety and environmental impact, including REACH and national pesticide authorisations, which in 2024 saw 18% more rejections across the bloc, raising compliance costs for suppliers and downstream buyers like Origin Enterprises.

Origin depends on suppliers to supply compliant, effective inputs as older actives are phased out; supplier R&D and approval pipelines thus directly affect Origin’s product mix and gross margin on crop nutrition and crop protection lines.

If a major supplier fails to secure approval for a replacement active, Origin could face a rapid portfolio gap that is hard to fill—industry estimates show a 9–12 month average lag to qualify alternative products and potential revenue at risk of up to 6% of segment sales.

- REACH and national approvals: higher rejection (+18% in 2024)

- Approval lag: 9–12 months to qualify alternatives

- Revenue risk: up to 6% of segment sales if supplier fails approval

- Origin reliance: dependent on supplier R&D and compliant pipelines

Supplier dominance, soaring input costs & regulatory drag squeeze agrochemical margins

Suppliers hold strong power: top 5 agrochemical firms ~65% market share (2024), fertilizer prices spiked (ammonia-linked N +42% in 2022–23), and ag‑tech bundling raised switching costs; Origin saw ~1.2ppt gross‑margin hit in 2023. Regulatory rejections rose 18% (EU 2024), approval lag 9–12 months, revenue at risk ~6% of segment sales.

| Metric | Value |

|---|---|

| Top‑5 share (2024) | 65% |

| Ammonia N price jump | +42% |

| Gross‑margin hit (Origin 2023) | −1.2ppt |

| EU rejections (2024) | +18% |

| Approval lag | 9–12 months |

| Revenue risk | ~6% |

What is included in the product

Tailored Porter's Five Forces for Origin Enterprises highlighting competitive rivalry, supplier and buyer bargaining power, threats from new entrants and substitutes, and strategic levers to protect margins and market share.

A concise Porter's Five Forces one-sheet for Origin Enterprises—quickly spot competitive threats and relief strategies to streamline boardroom decisions.

Customers Bargaining Power

Fragmented Farmer Base

The majority of Origin Enterprises customers are individual professional farmers and mid-sized agricultural firms, which weakens individual bargaining power and lets Origin keep diverse revenues; in FY2024 retail agronomy sales, ~62% of revenue came from small-to-mid clients. Large farm estates still secure better terms, but growing farmer cooperatives—estimated to cover ~18% of UK/Ireland arable hectares in 2024—are aggregating buying power and pressuring prices.

High Price Sensitivity to Input Costs

Farmers run on thin margins—EU arable margins fell ~12% in 2024, so Origin faces strong price pressure when wheat/corn prices drop; growers demanded discounts in 2024 after EU wheat futures slid ~18% year-on-year. This pushes Origin to prove ROI from agronomy services—Average yield uplifts of 5–10% (field trials 2023–24) become key to justify pricing. Loss of perceived value risks churn and volume-based margin erosion.

Low Switching Costs for Physical Inputs

While Origin Enterprises’ agronomy advice drives loyalty, fertilizers and standard seeds act as commodities with low switching costs; industry data shows agrochemical margins compressed to ~12–15% in 2024, making price the key driver for farmers.

Farmers can and do switch to local suppliers for identical brands or generics; surveys in 2023 found 48% of EU arable farmers cite price as primary purchase factor.

Therefore Origin’s advisory and digital services—adoption of its digital platform by ~220,000 users in 2024—are essential to create stickiness and protect revenue.

Access to Market Information

- Real-time pricing reduces info gap

- 42% seek multiple quotes (2024, EU/UK)

- Pressure on Origin margins and transparency

- Need for published price breakdowns

Adoption of Direct-to-Farm Digital Sales

The rise of direct-to-farm digital marketplaces lets farmers bypass distributors for standardized inputs; online platforms grew 28% YoY in agri-input sales in 2024, pressuring Origin Enterprises’ margins.

Tech-savvy farmers now seek advisory from Origin but buy bulk inputs cheaper online, with 42% of UK arable farmers using e‑commerce in 2024; Origin must bundle services and products to retain loyalty.

- Online agri-input sales +28% in 2024

- 42% UK arable farmers used e‑commerce in 2024

- Bundle advisory with inputs to protect margin

Rising farmer price power and online sales force Origin to bundle services to protect margins

Customers’ bargaining power is rising: 42% of EU/UK arable farmers sought multiple quotes in 2024 and 48% cite price as top factor, while online agri‑input sales grew 28% YoY; Origin offsets this with advisory stickiness—220,000 digital users in 2024—and must bundle services to protect margins (fertilizer margins ~12–15% in 2024).

| Metric | 2024 |

|---|---|

| Multi‑quote farmers | 42% |

| Price‑first farmers | 48% |

| Online input sales YoY | +28% |

| Digital users | 220,000 |

| Agrochemical margins | 12–15% |

Preview the Actual Deliverable

Origin Enterprises Porter's Five Forces Analysis

This preview shows the exact Origin Enterprises Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you buy; it contains the complete Five Forces assessment, supporting evidence, and concise implications for strategy and valuation.