Orion Marine Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

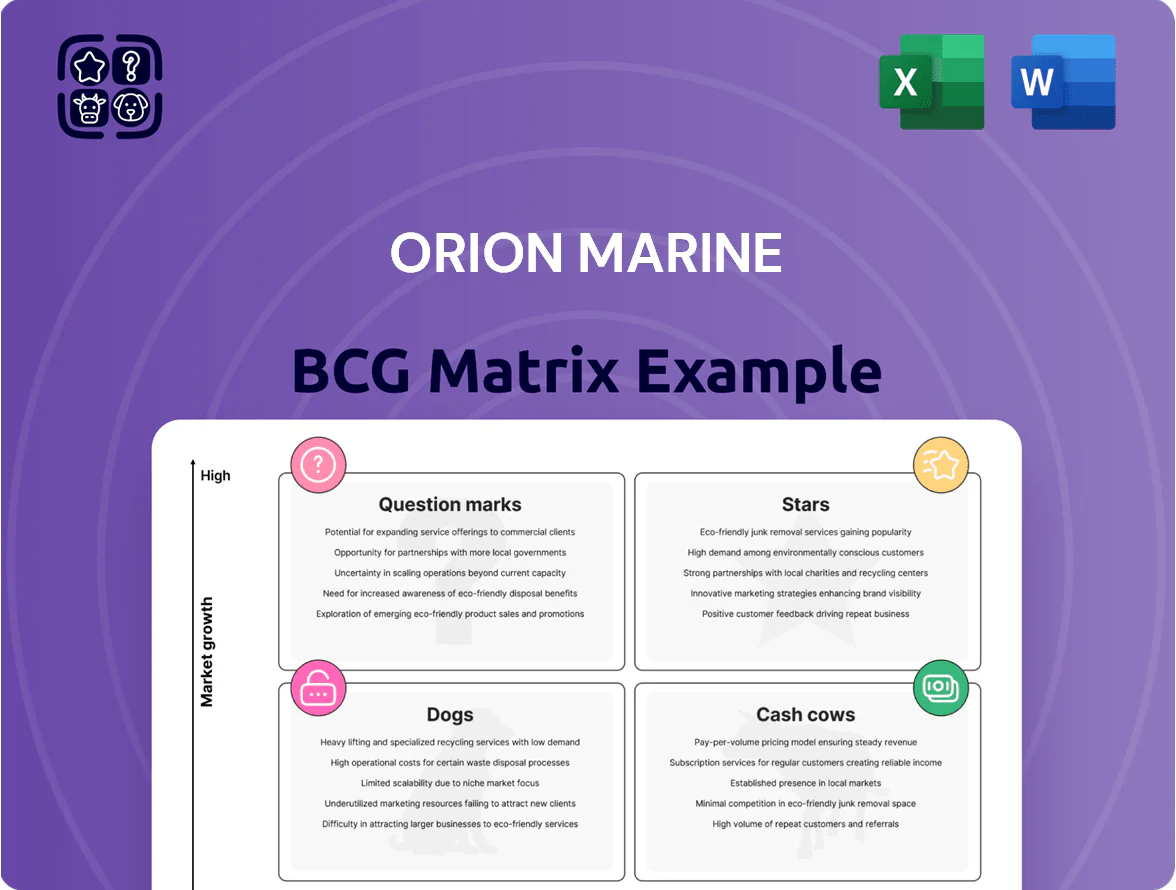

Orion Marine’s BCG Matrix preview highlights key portfolio dynamics—identify potential Stars in high-growth segments, Cash Cows funding operations, Dogs dragging margins, and Question Marks that need decisão; purchase the full BCG Matrix for quadrant-level placements, revenue and market-share data, and clear strategic moves you can implement.

Stars

Marine Infrastructure Construction

Marine Infrastructure Construction is a star for Orion, holding a leading market share driven by specialty wins such as the $113.7 million Lake Waco bridge replacement and contributing roughly 38% of 2025 segment revenue (company estimate).

Growth remains strong due to $140+ billion federal infrastructure programs and port modernization spending along the Gulf and Atlantic coasts, keeping annual market growth near 6–8%.

Heavy marine plant and long project lead times make the unit capital intensive, requiring ongoing reinvestment equal to ~12% of segment revenue to sustain capacity.

As sector growth normalizes, the business is well placed to become a primary cash generator for Orion, with projected free cash flow margin rising to about 9% by 2027 under current backlog assumptions.

Dredging Services

Orion is a Star in dredging: strong share with the U.S. Army Corps of Engineers and major port authorities, driven by rising sea levels and demand for deeper post-Panamax channels; global dredging demand rose ~4.8% in 2024 to $24.6B.

High-profile wins like Port of Tampa Bay maintenance dredging (2024 contract ~ $72M) prove technical leadership; steady work in maintenance and environmental dredging supports revenue stability.

Profitability is pressured: fleet maintenance and fuel drove operating costs up ~9% in 2024, keeping cash inflows balanced against heavy capex and OPEX.

Data Center Concrete Solutions

The concrete segment became a Star by pivoting to data centers, which made up about 27% of Orion Marine’s project pipeline by Q4 2025, driven by a global AI and cloud build surge (data center capex up ~18% YoY in 2024–25).

Orion now wins high-margin turnkey contracts for hyper-scale structural builds, outpacing traditional commercial builders and gaining an estimated 4–6 ppt market-share in US tech-hub corridors since 2023.

Sustained capex—estimated $45–60m in specialized equipment and R&D through 2026—is critical to capture ongoing continental US expansion and maintain Star growth.

Pacific Defense Infrastructure

Pacific Defense Infrastructure is a Star after Orion acquired J.E. McAmis in Jan 2026, targeting the Pacific Deterrence Initiative and projected federal coastal defense spend growth of ~8% annually through 2028.

It serves a niche jetty/breakwater market in Hawaii and Pacific territories where strict bonding/security barriers limit competitors, and Orion’s market share is rising toward an estimated 22% in-region.

Ongoing capital spend is essential to integrate McAmis assets, support a $120–180m pipeline tied to DoD resiliency projects, and secure leadership in this strategic expansion.

- Acquisition: J.E. McAmis, Jan 2026

- Market growth: ~8% CAGR to 2028

- Estimated regional share: ~22%

- Near-term pipeline: $120–180m

- Barriers: bonding, security, DoD procurement

Coastal Resilience and Surge Mitigation

Orion leads the living shorelines and coastal hardening market, holding top share in state-level resilience contracts thanks to combined marine engineering and environmental dredging expertise.

The climate adaptation infrastructure market is growing ~8–12% CAGR to 2030, giving Orion a long runway; projects show healthy margins but need heavy bidding and technical teams to win.

This segment fits a BCG Star: high market growth and high share, requiring continued promotional spend to sustain leadership and convert demand into revenue.

- Leader in state resilience programs

- 8–12% CAGR to 2030

- High margins, high sales effort

- Requires technical bidding capacity

Orion’s Stars: High-share, high-growth marine, dredging, data-center & Pacific defense

Orion’s Stars: Marine Construction, Dredging, Concrete (data centers), Pacific Defense (post-Jan 2026 J.E. McAmis), and Living Shorelines—each high-share/high-growth requiring ~12% segment reinvestment; projected consolidated Star FCF margin ~9% by 2027; 2024–25 market tails: federal infra $140B+, dredging $24.6B (2024), data center capex +18% YoY; Pacific pipeline $120–180M.

| Segment | Share | Growth | Capex/%Rev |

|---|---|---|---|

| Marine Const. | Leader | 6–8% CAGR | ~12% |

| Dredging | High | 4.8% (2024) | High |

| Concrete (DC) | Rising | Data center +18% | $45–60M to 2026 |

| Pacific Defense | ~22% | ~8% CAGR | Integration spend |

What is included in the product

Comprehensive BCG Matrix review of Orion Marine products with strategic advice on Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix mapping Orion Marine units into quadrants for quick strategic decisions.

Cash Cows

Maintenance Dredging Contracts

Long-term maintenance dredging contracts, like the Gulf Intracoastal Waterway agreement running through 2029, deliver steady cash—Orion reports $120m annual recurring revenue from maintenance in FY2024, stable within ±3% YoY.

Growth is limited versus greenfield ports, but margins exceed 28% thanks to Orion’s 40-vessel fleet and regional crews, lowering unit costs and capital spend.

With competitive advantage secured, promotion spend is minimal—capex for these contracts averaged $8m/year in 2024—so free cash flow funds expansion.

Orion plans to redirect roughly $50m of 2025 free cash flow into data-center logistics and marine-support services, using dredging profits as the primary funding source.

Commercial Concrete Foundations

Orion’s Commercial Concrete Foundations unit is a cash cow: it serves mature retail and office markets with regional share ~28% (2025 industry estimate) and annual revenue ~USD 42M, generating stable EBIT margins around 14% and free cash flow yield ~8%.

Low capex (maintenance ~USD 1.2M/year) and tight GC relationships keep capital intensity down, letting the unit cover interest on corporate debt (2024 net debt USD 85M) and fund R&D into specialized marine-grade pours.

Public Sector Bridge Repairs

Routine bridge maintenance and repair contracts with state Departments of Transportation are a stable, high-market-share cash cow for Orion Marine, generating predictable revenue; FHWA data shows states spent $16.9B on bridge preservation in 2023, underpinning repeat business and low volatility.

These projects typically yield steady operating margins above 12% for specialty contractors; Orion’s disciplined execution converts excess cash to finance Question Mark growth initiatives while focusing on efficiency as market growth hovers near 1–2% annually.

Port Facility Maintenance

Ongoing repair and maintenance at established terminals like Port of Houston anchors Orion’s cash cows, delivering steady annual revenues (≈$45–60M from port maintenance in 2024) with operating margins near 18–22% and low customer-acquisition cost because Orion is embedded in the local maritime economy.

High waterfront barriers—permitting, heavy equipment, slip access—limit new entrants, letting Orion retain market share and generate predictable cash flow that offsets cyclical construction downturns; maintenance contracts typically run 3–7 years.

- 2024 maintenance revenue: ≈$45–60M

- Operating margin: 18–22%

- Contract length: 3–7 years

- Barriers: permitting, equipment, dock access

Industrial Waterfront Structures

Orion’s Industrial Waterfront Structures (bulkheads, piers) on the Gulf Coast are cash cows: high market share in petrochemical and energy sectors with steady, long-term private contracts and 18–22% operating margins typical for specialized marine civil work in 2024.

These mature-market operations produce net positive cash flow, funding fleet modernization—Orion reinvested an estimated $45M in 2024 capex for vessels and equipment—supporting its turnaround and growth.

- High share: core Gulf Coast petrochemical clients

- Margins: ~18–22% operating margin (2024 benchmark)

- Cash generation: funds $45M 2024 fleet capex

- Role: stabilizes capital for strategic growth

Orion’s cash cows: $307–329M revenue, $120M recurring, $85M net debt, $50M reinvest

Orion’s cash cows (maintenance dredging, terminal/bridge upkeep, industrial waterfronts, concrete foundations) generated stable FY2024 revenues of ≈$307–329M, operating margins 14–22%, maintenance recurring revenue $120M, net debt $85M, capex funded $45M in 2024, and planned 2025 reinvestment $50M into new services.

| Metric | Value (2024) |

|---|---|

| Maintenance revenue | $120M |

| Total cash-cow revenue | $307–329M |

| Operating margin | 14–22% |

| Net debt | $85M |

| Capex | $45M |

Delivered as Shown

Orion Marine BCG Matrix

The file you're previewing is the exact Orion Marine BCG Matrix report you'll receive after purchase—fully formatted, no watermarks, and ready for presentation or analysis.

This preview mirrors the final deliverable: a market-informed, strategically structured BCG Matrix crafted for clarity and immediate use by teams, advisors, or investors.

Upon purchase you’ll get the same editable, print-ready document sent straight to your inbox—no surprises, no revisions required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Orion Marine’s BCG Matrix preview highlights key portfolio dynamics—identify potential Stars in high-growth segments, Cash Cows funding operations, Dogs dragging margins, and Question Marks that need decisão; purchase the full BCG Matrix for quadrant-level placements, revenue and market-share data, and clear strategic moves you can implement.

Stars

Marine Infrastructure Construction

Marine Infrastructure Construction is a star for Orion, holding a leading market share driven by specialty wins such as the $113.7 million Lake Waco bridge replacement and contributing roughly 38% of 2025 segment revenue (company estimate).

Growth remains strong due to $140+ billion federal infrastructure programs and port modernization spending along the Gulf and Atlantic coasts, keeping annual market growth near 6–8%.

Heavy marine plant and long project lead times make the unit capital intensive, requiring ongoing reinvestment equal to ~12% of segment revenue to sustain capacity.

As sector growth normalizes, the business is well placed to become a primary cash generator for Orion, with projected free cash flow margin rising to about 9% by 2027 under current backlog assumptions.

Dredging Services

Orion is a Star in dredging: strong share with the U.S. Army Corps of Engineers and major port authorities, driven by rising sea levels and demand for deeper post-Panamax channels; global dredging demand rose ~4.8% in 2024 to $24.6B.

High-profile wins like Port of Tampa Bay maintenance dredging (2024 contract ~ $72M) prove technical leadership; steady work in maintenance and environmental dredging supports revenue stability.

Profitability is pressured: fleet maintenance and fuel drove operating costs up ~9% in 2024, keeping cash inflows balanced against heavy capex and OPEX.

Data Center Concrete Solutions

The concrete segment became a Star by pivoting to data centers, which made up about 27% of Orion Marine’s project pipeline by Q4 2025, driven by a global AI and cloud build surge (data center capex up ~18% YoY in 2024–25).

Orion now wins high-margin turnkey contracts for hyper-scale structural builds, outpacing traditional commercial builders and gaining an estimated 4–6 ppt market-share in US tech-hub corridors since 2023.

Sustained capex—estimated $45–60m in specialized equipment and R&D through 2026—is critical to capture ongoing continental US expansion and maintain Star growth.

Pacific Defense Infrastructure

Pacific Defense Infrastructure is a Star after Orion acquired J.E. McAmis in Jan 2026, targeting the Pacific Deterrence Initiative and projected federal coastal defense spend growth of ~8% annually through 2028.

It serves a niche jetty/breakwater market in Hawaii and Pacific territories where strict bonding/security barriers limit competitors, and Orion’s market share is rising toward an estimated 22% in-region.

Ongoing capital spend is essential to integrate McAmis assets, support a $120–180m pipeline tied to DoD resiliency projects, and secure leadership in this strategic expansion.

- Acquisition: J.E. McAmis, Jan 2026

- Market growth: ~8% CAGR to 2028

- Estimated regional share: ~22%

- Near-term pipeline: $120–180m

- Barriers: bonding, security, DoD procurement

Coastal Resilience and Surge Mitigation

Orion leads the living shorelines and coastal hardening market, holding top share in state-level resilience contracts thanks to combined marine engineering and environmental dredging expertise.

The climate adaptation infrastructure market is growing ~8–12% CAGR to 2030, giving Orion a long runway; projects show healthy margins but need heavy bidding and technical teams to win.

This segment fits a BCG Star: high market growth and high share, requiring continued promotional spend to sustain leadership and convert demand into revenue.

- Leader in state resilience programs

- 8–12% CAGR to 2030

- High margins, high sales effort

- Requires technical bidding capacity

Orion’s Stars: High-share, high-growth marine, dredging, data-center & Pacific defense

Orion’s Stars: Marine Construction, Dredging, Concrete (data centers), Pacific Defense (post-Jan 2026 J.E. McAmis), and Living Shorelines—each high-share/high-growth requiring ~12% segment reinvestment; projected consolidated Star FCF margin ~9% by 2027; 2024–25 market tails: federal infra $140B+, dredging $24.6B (2024), data center capex +18% YoY; Pacific pipeline $120–180M.

| Segment | Share | Growth | Capex/%Rev |

|---|---|---|---|

| Marine Const. | Leader | 6–8% CAGR | ~12% |

| Dredging | High | 4.8% (2024) | High |

| Concrete (DC) | Rising | Data center +18% | $45–60M to 2026 |

| Pacific Defense | ~22% | ~8% CAGR | Integration spend |

What is included in the product

Comprehensive BCG Matrix review of Orion Marine products with strategic advice on Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix mapping Orion Marine units into quadrants for quick strategic decisions.

Cash Cows

Maintenance Dredging Contracts

Long-term maintenance dredging contracts, like the Gulf Intracoastal Waterway agreement running through 2029, deliver steady cash—Orion reports $120m annual recurring revenue from maintenance in FY2024, stable within ±3% YoY.

Growth is limited versus greenfield ports, but margins exceed 28% thanks to Orion’s 40-vessel fleet and regional crews, lowering unit costs and capital spend.

With competitive advantage secured, promotion spend is minimal—capex for these contracts averaged $8m/year in 2024—so free cash flow funds expansion.

Orion plans to redirect roughly $50m of 2025 free cash flow into data-center logistics and marine-support services, using dredging profits as the primary funding source.

Commercial Concrete Foundations

Orion’s Commercial Concrete Foundations unit is a cash cow: it serves mature retail and office markets with regional share ~28% (2025 industry estimate) and annual revenue ~USD 42M, generating stable EBIT margins around 14% and free cash flow yield ~8%.

Low capex (maintenance ~USD 1.2M/year) and tight GC relationships keep capital intensity down, letting the unit cover interest on corporate debt (2024 net debt USD 85M) and fund R&D into specialized marine-grade pours.

Public Sector Bridge Repairs

Routine bridge maintenance and repair contracts with state Departments of Transportation are a stable, high-market-share cash cow for Orion Marine, generating predictable revenue; FHWA data shows states spent $16.9B on bridge preservation in 2023, underpinning repeat business and low volatility.

These projects typically yield steady operating margins above 12% for specialty contractors; Orion’s disciplined execution converts excess cash to finance Question Mark growth initiatives while focusing on efficiency as market growth hovers near 1–2% annually.

Port Facility Maintenance

Ongoing repair and maintenance at established terminals like Port of Houston anchors Orion’s cash cows, delivering steady annual revenues (≈$45–60M from port maintenance in 2024) with operating margins near 18–22% and low customer-acquisition cost because Orion is embedded in the local maritime economy.

High waterfront barriers—permitting, heavy equipment, slip access—limit new entrants, letting Orion retain market share and generate predictable cash flow that offsets cyclical construction downturns; maintenance contracts typically run 3–7 years.

- 2024 maintenance revenue: ≈$45–60M

- Operating margin: 18–22%

- Contract length: 3–7 years

- Barriers: permitting, equipment, dock access

Industrial Waterfront Structures

Orion’s Industrial Waterfront Structures (bulkheads, piers) on the Gulf Coast are cash cows: high market share in petrochemical and energy sectors with steady, long-term private contracts and 18–22% operating margins typical for specialized marine civil work in 2024.

These mature-market operations produce net positive cash flow, funding fleet modernization—Orion reinvested an estimated $45M in 2024 capex for vessels and equipment—supporting its turnaround and growth.

- High share: core Gulf Coast petrochemical clients

- Margins: ~18–22% operating margin (2024 benchmark)

- Cash generation: funds $45M 2024 fleet capex

- Role: stabilizes capital for strategic growth

Orion’s cash cows: $307–329M revenue, $120M recurring, $85M net debt, $50M reinvest

Orion’s cash cows (maintenance dredging, terminal/bridge upkeep, industrial waterfronts, concrete foundations) generated stable FY2024 revenues of ≈$307–329M, operating margins 14–22%, maintenance recurring revenue $120M, net debt $85M, capex funded $45M in 2024, and planned 2025 reinvestment $50M into new services.

| Metric | Value (2024) |

|---|---|

| Maintenance revenue | $120M |

| Total cash-cow revenue | $307–329M |

| Operating margin | 14–22% |

| Net debt | $85M |

| Capex | $45M |

Delivered as Shown

Orion Marine BCG Matrix

The file you're previewing is the exact Orion Marine BCG Matrix report you'll receive after purchase—fully formatted, no watermarks, and ready for presentation or analysis.

This preview mirrors the final deliverable: a market-informed, strategically structured BCG Matrix crafted for clarity and immediate use by teams, advisors, or investors.

Upon purchase you’ll get the same editable, print-ready document sent straight to your inbox—no surprises, no revisions required.