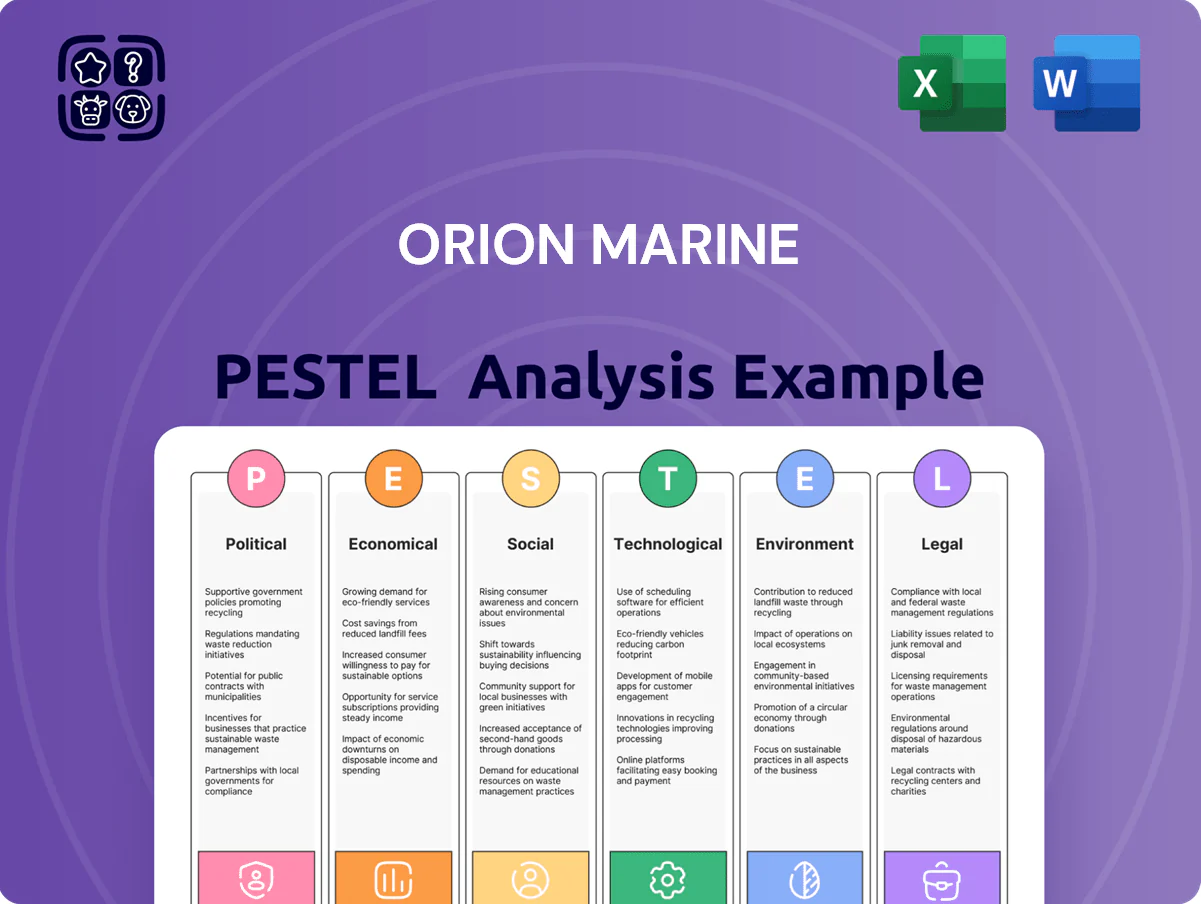

Orion Marine PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and environmental regulations are shaping Orion Marine’s strategic outlook—our concise PESTLE highlights key external forces and what they mean for investors and managers. Buy the full analysis to access detailed risk assessments, growth opportunities, and ready-to-use insights in editable formats for boardrooms or investment pitches.

Political factors

Federal Infrastructure Funding Levels

As of late 2025, continued disbursements from the 1.2 trillion USD Infrastructure Investment and Jobs Act, with roughly 50–60 billion USD allocated to coastal resilience through FY2021–2026, remain a primary driver for Orion’s marine and concrete segments.

U.S. Army Corps of Engineers budget appropriations—about 8.3 billion USD in recent annual totals—directly determine dredging and coastal maintenance contract volume available to Orion.

Political shifts during the 2024–2025 Washington cycle slowed some project approvals but increased emphasis on domestic maritime resilience, accelerating funding prioritization for hurricane mitigation and port modernization projects relevant to Orion.

Geopolitical Stability in the Caribbean

Orion's Caribbean operations are exposed to shifts in U.S.–regional diplomatic ties; a 2024 uptick in bilateral trade agreements raised port investment inquiries by 18% year-over-year, while political unrest in 2 major Caribbean states in 2023 delayed $120m in terminal projects. Changes to trade pacts could swing demand for port expansions by an estimated 10–25% across the basin. Strategic infrastructure investments align with U.S. nearshoring and supply-chain-security aims, which accounted for $3.4bn in regional logistics funding in 2025.

Defense Spending and Naval Infrastructure

Orion Marine depends heavily on DoD contracts for naval base and port work, with defense construction budgets totaling about $43.5 billion in FY2025 and shipyard/port allocations driving a sizable share of its backlog. Shifts in Congressional priorities on Pacific versus Atlantic fleet posture alter multi-year project pipelines, affecting bid opportunities and timelines. Passage of annual defense appropriations—FY2024 enacted at $858 billion and FY2025 at $839 billion—serves as a leading indicator of revenue stability for the marine segment.

Public-Private Partnership Legislation

State and federal P3 legislation affects Orion’s access to large infrastructure work; 28 states had enabling P3 laws by 2025, widening potential markets for bridge and highway concrete contracts worth an estimated $120–180 billion in the US 2024–2026 pipeline.

Shifts in political appetite for private financing can quickly alter bid volumes—federal Infrastructure Investment and Jobs Act allocations plus state P3s drove a 12% rise in highway project awards in 2024, improving Orion’s backlog visibility.

Streamlined legislative frameworks for multi-year, bundled bidding reduce procurement risk and improve cashflow forecasting; jurisdictions with standardized P3 rules cut procurement time by ~30%, aiding Orion’s operational planning.

- 28 states with P3 laws by 2025

- $120–180B US bridge/highway pipeline (2024–2026)

- 12% increase in 2024 highway awards linked to P3 activity

- ~30% faster procurement where P3 rules standardized

Trade Policy and Port Development

Tariff adjustments and trade deals like USMCA and individual tariffs affect cargo volumes at U.S./Canadian ports; U.S. container throughput fell 2.1% in 2023 while Gulf ports handled a record 370 million short tons of bulk cargo in 2024, raising dredging and maintenance demand.

Federal and state policies promoting reshoring and LNG exports drove Gulf Coast industrial expansion—U.S. LNG export capacity rose to ~13.7 Bcf/d by end-2024—prompting private clients to plan dock upgrades.

Escalating trade tensions and new blocs (e.g., CPTPP dynamics) can redirect investment geographically, shifting port infrastructure spending toward resilient, deepwater facilities.

- Tariffs/trade deals change cargo flow and dredging needs

- Gulf industrial growth tied to reshoring and 13.7 Bcf/d LNG capacity

- 2024 Gulf bulk throughput ~370M short tons, increasing maintenance demand

- Trade shifts redirect port investment to deepwater/expanded docks

Big Federal Bets: $100B+ Infrastructure & Defense Drive Ports, Resilience, and LNG Growth

Political factors: federal Infrastructure Investment & Jobs Act disbursements (50–60B coastal resilience FY21–26), USACE annual appropriations ~8.3B, defense construction budgets $43.5B (FY25) with DoD overall appropriations $839B (FY25), 28 states P3 laws, US bridge/highway pipeline $120–180B (2024–26), Gulf bulk throughput ~370M short tons (2024), US LNG capacity ~13.7 Bcf/d (end-2024).

| Metric | Value |

|---|---|

| Coastal resilience funding (FY21–26) | 50–60B USD |

| USACE annual appropriations | ~8.3B USD |

| Defense construction (FY25) | 43.5B USD |

| Federal defense appropriations (FY25) | 839B USD |

| States with P3 laws (2025) | 28 |

| US bridge/highway pipeline (2024–26) | 120–180B USD |

| Gulf bulk throughput (2024) | ~370M short tons |

| US LNG export capacity (end-2024) | ~13.7 Bcf/d |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Orion Marine, with each section supported by current data and industry trends to identify risks, opportunities, and strategic implications.

A concise, visually segmented PESTLE summary for Orion Marine that distills external risks and opportunities into a shareable, presentation-ready format—ideal for quick alignment, meeting discussions, and client reports.

Economic factors

Interest Rate Environment and Capital Costs

By end-2025, rising global benchmark rates pushed US 10-year Treasury to ~4.3% and average prime rates near 8.5%, raising Orion’s equipment financing costs and increasing weighted average cost of capital for heavy machinery purchases.

High borrowing costs have contributed to a 12–18% slowdown in US commercial concrete project starts in 2024–25, delaying private terminal expansions that directly reduce near-term demand for Orion’s services.

Conversely, if the Federal Reserve signals rate stabilization—markets priced ~50% chance of cuts by H2‑2026—industrial and building sector clients are more likely to resume long-term CAPEX, improving Orion’s medium-term contract pipeline.

Inflationary Pressures on Material Inputs

Fluctuations in cement, steel and fuel—steel spot prices rose ~18% YoY in 2024 and bunker fuel averaged $620/ton in 2024—compress margins on Orion Marine's fixed-price dredging contracts, prompting inclusion of escalation clauses. Commodity volatility drove industry hedging uptake; Orion needs forward fuel purchase and steel futures to stabilize costs. Managing specialized marine fuel costs remains critical for dredge fleet efficiency and EBITDA protection.

Labor Market Dynamics and Specialized Skills

The construction sector faces a 2024 skilled labor shortfall—the US had a 7% contractor vacancy rate and concrete specialists in short supply—pushing average construction wages up 4.5% year-over-year; Orion Marine faces higher labor costs and bidding pressure as competition for engineers/project managers raises overhead and limits scaling on >$50M marine projects. Investing in training/retention (2–4% of revenue) is a required trade-off.

Energy Sector Capital Expenditure

Orion’s industrial revenues track energy capex cycles; global oil & gas capex fell ~5% in 2024 but LNG export projects surged, with US LNG export capacity rising to ~14 Bcf/d by end-2025, boosting demand for marine construction.

Offshore wind investment reached $50–60bn globally in 2024, driving Gulf Coast port upgrades and dredging opportunities; private maintenance/expansion work in the Gulf is highly correlated to oil prices and rig counts.

- US LNG capacity ~14 Bcf/d (end-2025)

- Global offshore wind spend ~$50–60bn (2024)

- Oil & gas capex down ~5% (2024)

Currency Exchange Rate Volatility

Operating across Canada and the Caribbean exposes Orion Marine to FX volatility that can sway international contract valuations; CAD versus USD and regional currencies moved 6–8% on average in 2024, affecting revenue recognition.

Economic instability in some Caribbean markets has led to supplier payment delays and local cost inflation—materials and labor rose ~7% YoY in several islands in 2024, increasing project costs.

Active hedging and multi-currency invoicing are essential to shield margins from adverse CAD moves and regional currency swings; effective currency management reduced FX losses by an estimated 1.2% of revenue in peer cases.

- CAD vs USD/region 6–8% volatility in 2024

- Local labor/materials ~7% YoY rise in some Caribbean markets (2024)

- Hedging can cut FX losses ~1.2% of revenue

Higher rates squeeze Orion margins amid cost inflation; offshore energy fuels medium‑term dredging demand

Higher global rates (US 10y ~4.3%, prime ~8.5% end‑2025) raise Orion’s financing costs and WACC; steel +18% YoY (2024) and bunker ~$620/ton compress fixed‑price margins; US commercial concrete starts down 12–18% (2024–25) delaying terminal work; US LNG capacity ~14 Bcf/d (end‑2025) and $50–60bn offshore wind (2024) create medium‑term dredging demand.

| Metric | Value |

|---|---|

| US 10y (end‑2025) | ~4.3% |

| Prime rate | ~8.5% |

| Steel (2024 YoY) | +18% |

| Bunker fuel (2024 avg) | $620/ton |

| US LNG cap (end‑2025) | ~14 Bcf/d |

| Offshore wind spend (2024) | $50–60bn |

Preview the Actual Deliverable

Orion Marine PESTLE Analysis

The preview shown here is the exact Orion Marine PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and environmental regulations are shaping Orion Marine’s strategic outlook—our concise PESTLE highlights key external forces and what they mean for investors and managers. Buy the full analysis to access detailed risk assessments, growth opportunities, and ready-to-use insights in editable formats for boardrooms or investment pitches.

Political factors

Federal Infrastructure Funding Levels

As of late 2025, continued disbursements from the 1.2 trillion USD Infrastructure Investment and Jobs Act, with roughly 50–60 billion USD allocated to coastal resilience through FY2021–2026, remain a primary driver for Orion’s marine and concrete segments.

U.S. Army Corps of Engineers budget appropriations—about 8.3 billion USD in recent annual totals—directly determine dredging and coastal maintenance contract volume available to Orion.

Political shifts during the 2024–2025 Washington cycle slowed some project approvals but increased emphasis on domestic maritime resilience, accelerating funding prioritization for hurricane mitigation and port modernization projects relevant to Orion.

Geopolitical Stability in the Caribbean

Orion's Caribbean operations are exposed to shifts in U.S.–regional diplomatic ties; a 2024 uptick in bilateral trade agreements raised port investment inquiries by 18% year-over-year, while political unrest in 2 major Caribbean states in 2023 delayed $120m in terminal projects. Changes to trade pacts could swing demand for port expansions by an estimated 10–25% across the basin. Strategic infrastructure investments align with U.S. nearshoring and supply-chain-security aims, which accounted for $3.4bn in regional logistics funding in 2025.

Defense Spending and Naval Infrastructure

Orion Marine depends heavily on DoD contracts for naval base and port work, with defense construction budgets totaling about $43.5 billion in FY2025 and shipyard/port allocations driving a sizable share of its backlog. Shifts in Congressional priorities on Pacific versus Atlantic fleet posture alter multi-year project pipelines, affecting bid opportunities and timelines. Passage of annual defense appropriations—FY2024 enacted at $858 billion and FY2025 at $839 billion—serves as a leading indicator of revenue stability for the marine segment.

Public-Private Partnership Legislation

State and federal P3 legislation affects Orion’s access to large infrastructure work; 28 states had enabling P3 laws by 2025, widening potential markets for bridge and highway concrete contracts worth an estimated $120–180 billion in the US 2024–2026 pipeline.

Shifts in political appetite for private financing can quickly alter bid volumes—federal Infrastructure Investment and Jobs Act allocations plus state P3s drove a 12% rise in highway project awards in 2024, improving Orion’s backlog visibility.

Streamlined legislative frameworks for multi-year, bundled bidding reduce procurement risk and improve cashflow forecasting; jurisdictions with standardized P3 rules cut procurement time by ~30%, aiding Orion’s operational planning.

- 28 states with P3 laws by 2025

- $120–180B US bridge/highway pipeline (2024–2026)

- 12% increase in 2024 highway awards linked to P3 activity

- ~30% faster procurement where P3 rules standardized

Trade Policy and Port Development

Tariff adjustments and trade deals like USMCA and individual tariffs affect cargo volumes at U.S./Canadian ports; U.S. container throughput fell 2.1% in 2023 while Gulf ports handled a record 370 million short tons of bulk cargo in 2024, raising dredging and maintenance demand.

Federal and state policies promoting reshoring and LNG exports drove Gulf Coast industrial expansion—U.S. LNG export capacity rose to ~13.7 Bcf/d by end-2024—prompting private clients to plan dock upgrades.

Escalating trade tensions and new blocs (e.g., CPTPP dynamics) can redirect investment geographically, shifting port infrastructure spending toward resilient, deepwater facilities.

- Tariffs/trade deals change cargo flow and dredging needs

- Gulf industrial growth tied to reshoring and 13.7 Bcf/d LNG capacity

- 2024 Gulf bulk throughput ~370M short tons, increasing maintenance demand

- Trade shifts redirect port investment to deepwater/expanded docks

Big Federal Bets: $100B+ Infrastructure & Defense Drive Ports, Resilience, and LNG Growth

Political factors: federal Infrastructure Investment & Jobs Act disbursements (50–60B coastal resilience FY21–26), USACE annual appropriations ~8.3B, defense construction budgets $43.5B (FY25) with DoD overall appropriations $839B (FY25), 28 states P3 laws, US bridge/highway pipeline $120–180B (2024–26), Gulf bulk throughput ~370M short tons (2024), US LNG capacity ~13.7 Bcf/d (end-2024).

| Metric | Value |

|---|---|

| Coastal resilience funding (FY21–26) | 50–60B USD |

| USACE annual appropriations | ~8.3B USD |

| Defense construction (FY25) | 43.5B USD |

| Federal defense appropriations (FY25) | 839B USD |

| States with P3 laws (2025) | 28 |

| US bridge/highway pipeline (2024–26) | 120–180B USD |

| Gulf bulk throughput (2024) | ~370M short tons |

| US LNG export capacity (end-2024) | ~13.7 Bcf/d |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Orion Marine, with each section supported by current data and industry trends to identify risks, opportunities, and strategic implications.

A concise, visually segmented PESTLE summary for Orion Marine that distills external risks and opportunities into a shareable, presentation-ready format—ideal for quick alignment, meeting discussions, and client reports.

Economic factors

Interest Rate Environment and Capital Costs

By end-2025, rising global benchmark rates pushed US 10-year Treasury to ~4.3% and average prime rates near 8.5%, raising Orion’s equipment financing costs and increasing weighted average cost of capital for heavy machinery purchases.

High borrowing costs have contributed to a 12–18% slowdown in US commercial concrete project starts in 2024–25, delaying private terminal expansions that directly reduce near-term demand for Orion’s services.

Conversely, if the Federal Reserve signals rate stabilization—markets priced ~50% chance of cuts by H2‑2026—industrial and building sector clients are more likely to resume long-term CAPEX, improving Orion’s medium-term contract pipeline.

Inflationary Pressures on Material Inputs

Fluctuations in cement, steel and fuel—steel spot prices rose ~18% YoY in 2024 and bunker fuel averaged $620/ton in 2024—compress margins on Orion Marine's fixed-price dredging contracts, prompting inclusion of escalation clauses. Commodity volatility drove industry hedging uptake; Orion needs forward fuel purchase and steel futures to stabilize costs. Managing specialized marine fuel costs remains critical for dredge fleet efficiency and EBITDA protection.

Labor Market Dynamics and Specialized Skills

The construction sector faces a 2024 skilled labor shortfall—the US had a 7% contractor vacancy rate and concrete specialists in short supply—pushing average construction wages up 4.5% year-over-year; Orion Marine faces higher labor costs and bidding pressure as competition for engineers/project managers raises overhead and limits scaling on >$50M marine projects. Investing in training/retention (2–4% of revenue) is a required trade-off.

Energy Sector Capital Expenditure

Orion’s industrial revenues track energy capex cycles; global oil & gas capex fell ~5% in 2024 but LNG export projects surged, with US LNG export capacity rising to ~14 Bcf/d by end-2025, boosting demand for marine construction.

Offshore wind investment reached $50–60bn globally in 2024, driving Gulf Coast port upgrades and dredging opportunities; private maintenance/expansion work in the Gulf is highly correlated to oil prices and rig counts.

- US LNG capacity ~14 Bcf/d (end-2025)

- Global offshore wind spend ~$50–60bn (2024)

- Oil & gas capex down ~5% (2024)

Currency Exchange Rate Volatility

Operating across Canada and the Caribbean exposes Orion Marine to FX volatility that can sway international contract valuations; CAD versus USD and regional currencies moved 6–8% on average in 2024, affecting revenue recognition.

Economic instability in some Caribbean markets has led to supplier payment delays and local cost inflation—materials and labor rose ~7% YoY in several islands in 2024, increasing project costs.

Active hedging and multi-currency invoicing are essential to shield margins from adverse CAD moves and regional currency swings; effective currency management reduced FX losses by an estimated 1.2% of revenue in peer cases.

- CAD vs USD/region 6–8% volatility in 2024

- Local labor/materials ~7% YoY rise in some Caribbean markets (2024)

- Hedging can cut FX losses ~1.2% of revenue

Higher rates squeeze Orion margins amid cost inflation; offshore energy fuels medium‑term dredging demand

Higher global rates (US 10y ~4.3%, prime ~8.5% end‑2025) raise Orion’s financing costs and WACC; steel +18% YoY (2024) and bunker ~$620/ton compress fixed‑price margins; US commercial concrete starts down 12–18% (2024–25) delaying terminal work; US LNG capacity ~14 Bcf/d (end‑2025) and $50–60bn offshore wind (2024) create medium‑term dredging demand.

| Metric | Value |

|---|---|

| US 10y (end‑2025) | ~4.3% |

| Prime rate | ~8.5% |

| Steel (2024 YoY) | +18% |

| Bunker fuel (2024 avg) | $620/ton |

| US LNG cap (end‑2025) | ~14 Bcf/d |

| Offshore wind spend (2024) | $50–60bn |

Preview the Actual Deliverable

Orion Marine PESTLE Analysis

The preview shown here is the exact Orion Marine PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis and decision-making.