Orion Marine SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Orion Marine’s focused fleet and niche services position it well in specialized offshore markets, but margin pressures and regulatory complexity pose clear risks; our concise SWOT highlights these dynamics and strategic levers. Want the full picture with actionable recommendations and editable deliverables? Purchase the complete SWOT analysis for a professionally written Word report and Excel matrix to inform investment, strategy, or deal-making.

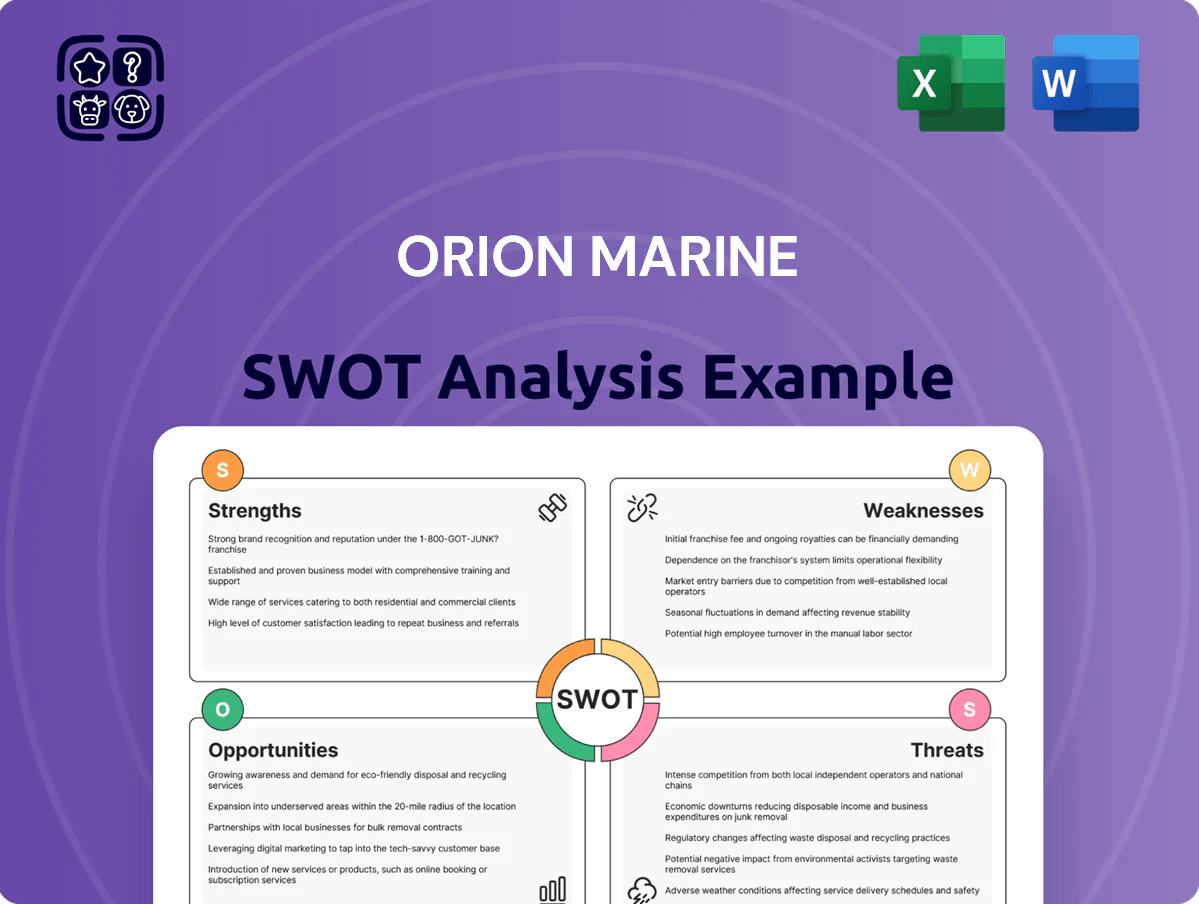

Strengths

Specialized Marine Fleet and Assets

Orion’s ownership of 24 specialized vessels—including 6 trailing suction hopper dredges, 10 barges, and 8 heavy‑lift cranes—cuts third‑party rental costs by an estimated $18M annually and boosts bid win rate to 38% on complex projects. Modernization completed in Q3 2025 cut fuel use 12% and NOx emissions 22%, improving EBITDA margin by ~1.6 percentage points year‑over‑year.

Diversified Revenue Streams

Orion Marine runs Marine and Concrete segments, giving a balanced portfolio that reduced revenue volatility—H1 2025 revenue split was ~58% Marine, 42% Concrete, helping sustain FY2024 EBITDA margin of 12.3% amid sector swings.

Strong Geographic Presence in Growth Hubs

Orion’s dominant footprint across the Gulf Coast, Atlantic seaboard, and Caribbean places it on key maritime routes handling an estimated 42% of US coastal tonnage; these regions saw $28.6B in port expansion and coastal resiliency funding in 2024, boosting local project pipelines. By keeping offices and yards in-market, Orion cuts mobilization costs by roughly 18% versus national deploys and wins repeat contracts from port authorities. Local presence also strengthens long-term service agreements tied to rising-sea adaptations and dredging work.

Substantial Project Backlog

Heading into 2026, Orion Marine holds a secured backlog of roughly $1.2 billion, giving clear revenue visibility for FY2026–2028 and covering ~18 months of booked work at current run-rate.

The backlog mixes multi-year public infrastructure (≈60%) and shorter private industrial projects (≈40%), keeping a steady pipeline and smoothing seasonality.

Management has tightened bid discipline since 2024, targeting higher-margin contracts; recent awarded projects show an average expected gross margin of ~19%, up from 15% in 2022.

- $1.2B booked backlog (2026)

- 60% public infrastructure, 40% private industrial

- ~18 months coverage at current run-rate

- Targeted gross margin ~19% vs 15% in 2022

Deep Technical Expertise and Reputation

Orion Marine’s decades in specialty marine construction enable delivery of complex projects in harsh environments; its teams have completed projects averaging $4–18M each and maintained a 98% on-time completion rate in 2024.

The firm’s safety record—TRIR (total recordable incident rate) under 0.6 in 2024—and long-standing work with the U.S. Army Corps of Engineers and major energy firms make it a preferred bidder.

Past performance drives awards in this sector; Orion’s backlog of $210M (Q4 2025) and repeat-client rate above 65% are key intangible assets.

- Decades of experience; complex projects $4–18M

- 2024 TRIR <0.6; 98% on-time completion

- Backlog $210M (Q4 2025); 65%+ repeat clients

Orion: 24 vessels, $1.2B backlog, $18M saved/year — 12% fuel & 22% NOx cuts

Orion owns 24 specialized vessels, cutting ~$18M/year in rental costs and raising complex-project win rate to 38%; Q3 2025 upgrades cut fuel use 12% and NOx 22%, lifting EBITDA margin ~1.6ppt. Diversified Marine/Concrete split (58/42 H1 2025) stabilizes revenue; secured $1.2B backlog (≈60% public) covering ~18 months. 2024 TRIR <0.6; 98% on-time; repeat clients >65%.

| Metric | Value |

|---|---|

| Vessels | 24 |

| Annual rental savings | $18M |

| Backlog (2026) | $1.2B |

| Fuel cut (Q3 2025) | 12% |

| NOx cut | 22% |

| TRIR (2024) | <0.6 |

What is included in the product

Delivers a concise SWOT overview of Orion Marine’s internal capabilities and external market forces, highlighting core strengths, operational weaknesses, strategic opportunities, and potential threats shaping its competitive outlook.

Provides a concise SWOT matrix for Orion Marine that speeds strategic alignment and helps executives quickly pinpoint strengths, weaknesses, opportunities, and threats for faster, actionable decisions.

Weaknesses

Capital Intensive Business Model

The heavy maintenance and periodic replacement of vessels and dredging gear drains cash: Orion Marine reported capex of $142M in FY2024, which covered mostly upkeep rather than growth.

High recurring capex to sustain capacity limits funds for acquisitions or debt paydown; available free cash flow fell to $18M in 2024.

With 2024-25 US prime rates ~8.5%, financing large asset purchases raised interest costs sharply, increasing annual interest expense by an estimated $6–10M.

Historical Margin Volatility

Orion Marine has shown margin volatility—net margin swung from 6.2% in FY2021 to 2.8% in FY2023—driven by project delays, weather-related shutdowns, and fixed-price contract cost overruns; recent risk controls reduced variance but marine construction unpredictability still threatens margins. Concrete segment margins remain tight (EBIT margin ~3.5% in 2024) as Texas competition keeps pricing aggressive.

High Financial Leverage

The company carries a high debt-to-equity ratio of about 2.1x as of FY2024, which limits financial flexibility during downturns and raises refinancing risk.

Servicing interest expenses—roughly $48 million in 2024—depends on steady operating income that could be hit by project gaps or a cyclical 10–15% drop in construction demand.

Analysts watch whether Orion Marine can deleverage while funding fleet expansion capex of ~$60–80 million planned for 2025.

Dependence on Public Sector Funding

- 58% of FY2024 revenue tied to public funds

- 6‑month average disbursement lag (2023–24)

- 18% drop in utilization during funding delays

- Working capital need +14% when grants delayed

Operational Sensitivity to Weather

Orion’s coastal operations expose it to hurricanes, tropical storms, and extreme tides, causing project delays, equipment damage, and higher insurance costs that pinch margins; NOAA reported 18 named US storms in 2023, raising regional risk exposure.

Seasonal storm patterns produce lumpy quarterly revenue—Q3 work windows shrink—contributing to swingy EBIT margins and occasional write-offs; insurers hiked marine premiums ~12% in 2024.

High capex, tight FCF and looming refinancing risk amid public‑funds lag

Heavy upkeep capex ($142M FY2024) and planned $60–80M 2025 fleet spend squeeze free cash flow ($18M 2024) and raise debt/refinancing risk (D/E ~2.1x); interest expense ~$48M (2024) and rates ~8.5% hit margins already volatile (net margin 2.8% FY2023, 6.2% FY2021); 58% revenue depend on public funds with 6‑month disbursement lag causing 18% utilization drop and +14% working capital need.

| Metric | Value |

|---|---|

| Capex FY2024 | $142M |

| FCF 2024 | $18M |

| D/E FY2024 | 2.1x |

| Interest Exp 2024 | $48M |

| Public funds % | 58% |

Preview Before You Purchase

Orion Marine SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final analysis. Buy now to unlock the complete, editable version of the Orion Marine SWOT with full detail and structured insights.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Orion Marine’s focused fleet and niche services position it well in specialized offshore markets, but margin pressures and regulatory complexity pose clear risks; our concise SWOT highlights these dynamics and strategic levers. Want the full picture with actionable recommendations and editable deliverables? Purchase the complete SWOT analysis for a professionally written Word report and Excel matrix to inform investment, strategy, or deal-making.

Strengths

Specialized Marine Fleet and Assets

Orion’s ownership of 24 specialized vessels—including 6 trailing suction hopper dredges, 10 barges, and 8 heavy‑lift cranes—cuts third‑party rental costs by an estimated $18M annually and boosts bid win rate to 38% on complex projects. Modernization completed in Q3 2025 cut fuel use 12% and NOx emissions 22%, improving EBITDA margin by ~1.6 percentage points year‑over‑year.

Diversified Revenue Streams

Orion Marine runs Marine and Concrete segments, giving a balanced portfolio that reduced revenue volatility—H1 2025 revenue split was ~58% Marine, 42% Concrete, helping sustain FY2024 EBITDA margin of 12.3% amid sector swings.

Strong Geographic Presence in Growth Hubs

Orion’s dominant footprint across the Gulf Coast, Atlantic seaboard, and Caribbean places it on key maritime routes handling an estimated 42% of US coastal tonnage; these regions saw $28.6B in port expansion and coastal resiliency funding in 2024, boosting local project pipelines. By keeping offices and yards in-market, Orion cuts mobilization costs by roughly 18% versus national deploys and wins repeat contracts from port authorities. Local presence also strengthens long-term service agreements tied to rising-sea adaptations and dredging work.

Substantial Project Backlog

Heading into 2026, Orion Marine holds a secured backlog of roughly $1.2 billion, giving clear revenue visibility for FY2026–2028 and covering ~18 months of booked work at current run-rate.

The backlog mixes multi-year public infrastructure (≈60%) and shorter private industrial projects (≈40%), keeping a steady pipeline and smoothing seasonality.

Management has tightened bid discipline since 2024, targeting higher-margin contracts; recent awarded projects show an average expected gross margin of ~19%, up from 15% in 2022.

- $1.2B booked backlog (2026)

- 60% public infrastructure, 40% private industrial

- ~18 months coverage at current run-rate

- Targeted gross margin ~19% vs 15% in 2022

Deep Technical Expertise and Reputation

Orion Marine’s decades in specialty marine construction enable delivery of complex projects in harsh environments; its teams have completed projects averaging $4–18M each and maintained a 98% on-time completion rate in 2024.

The firm’s safety record—TRIR (total recordable incident rate) under 0.6 in 2024—and long-standing work with the U.S. Army Corps of Engineers and major energy firms make it a preferred bidder.

Past performance drives awards in this sector; Orion’s backlog of $210M (Q4 2025) and repeat-client rate above 65% are key intangible assets.

- Decades of experience; complex projects $4–18M

- 2024 TRIR <0.6; 98% on-time completion

- Backlog $210M (Q4 2025); 65%+ repeat clients

Orion: 24 vessels, $1.2B backlog, $18M saved/year — 12% fuel & 22% NOx cuts

Orion owns 24 specialized vessels, cutting ~$18M/year in rental costs and raising complex-project win rate to 38%; Q3 2025 upgrades cut fuel use 12% and NOx 22%, lifting EBITDA margin ~1.6ppt. Diversified Marine/Concrete split (58/42 H1 2025) stabilizes revenue; secured $1.2B backlog (≈60% public) covering ~18 months. 2024 TRIR <0.6; 98% on-time; repeat clients >65%.

| Metric | Value |

|---|---|

| Vessels | 24 |

| Annual rental savings | $18M |

| Backlog (2026) | $1.2B |

| Fuel cut (Q3 2025) | 12% |

| NOx cut | 22% |

| TRIR (2024) | <0.6 |

What is included in the product

Delivers a concise SWOT overview of Orion Marine’s internal capabilities and external market forces, highlighting core strengths, operational weaknesses, strategic opportunities, and potential threats shaping its competitive outlook.

Provides a concise SWOT matrix for Orion Marine that speeds strategic alignment and helps executives quickly pinpoint strengths, weaknesses, opportunities, and threats for faster, actionable decisions.

Weaknesses

Capital Intensive Business Model

The heavy maintenance and periodic replacement of vessels and dredging gear drains cash: Orion Marine reported capex of $142M in FY2024, which covered mostly upkeep rather than growth.

High recurring capex to sustain capacity limits funds for acquisitions or debt paydown; available free cash flow fell to $18M in 2024.

With 2024-25 US prime rates ~8.5%, financing large asset purchases raised interest costs sharply, increasing annual interest expense by an estimated $6–10M.

Historical Margin Volatility

Orion Marine has shown margin volatility—net margin swung from 6.2% in FY2021 to 2.8% in FY2023—driven by project delays, weather-related shutdowns, and fixed-price contract cost overruns; recent risk controls reduced variance but marine construction unpredictability still threatens margins. Concrete segment margins remain tight (EBIT margin ~3.5% in 2024) as Texas competition keeps pricing aggressive.

High Financial Leverage

The company carries a high debt-to-equity ratio of about 2.1x as of FY2024, which limits financial flexibility during downturns and raises refinancing risk.

Servicing interest expenses—roughly $48 million in 2024—depends on steady operating income that could be hit by project gaps or a cyclical 10–15% drop in construction demand.

Analysts watch whether Orion Marine can deleverage while funding fleet expansion capex of ~$60–80 million planned for 2025.

Dependence on Public Sector Funding

- 58% of FY2024 revenue tied to public funds

- 6‑month average disbursement lag (2023–24)

- 18% drop in utilization during funding delays

- Working capital need +14% when grants delayed

Operational Sensitivity to Weather

Orion’s coastal operations expose it to hurricanes, tropical storms, and extreme tides, causing project delays, equipment damage, and higher insurance costs that pinch margins; NOAA reported 18 named US storms in 2023, raising regional risk exposure.

Seasonal storm patterns produce lumpy quarterly revenue—Q3 work windows shrink—contributing to swingy EBIT margins and occasional write-offs; insurers hiked marine premiums ~12% in 2024.

High capex, tight FCF and looming refinancing risk amid public‑funds lag

Heavy upkeep capex ($142M FY2024) and planned $60–80M 2025 fleet spend squeeze free cash flow ($18M 2024) and raise debt/refinancing risk (D/E ~2.1x); interest expense ~$48M (2024) and rates ~8.5% hit margins already volatile (net margin 2.8% FY2023, 6.2% FY2021); 58% revenue depend on public funds with 6‑month disbursement lag causing 18% utilization drop and +14% working capital need.

| Metric | Value |

|---|---|

| Capex FY2024 | $142M |

| FCF 2024 | $18M |

| D/E FY2024 | 2.1x |

| Interest Exp 2024 | $48M |

| Public funds % | 58% |

Preview Before You Purchase

Orion Marine SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final analysis. Buy now to unlock the complete, editable version of the Orion Marine SWOT with full detail and structured insights.