Ormat Technologies Porter's Five Forces Analysis

Don't Miss the Bigger Picture

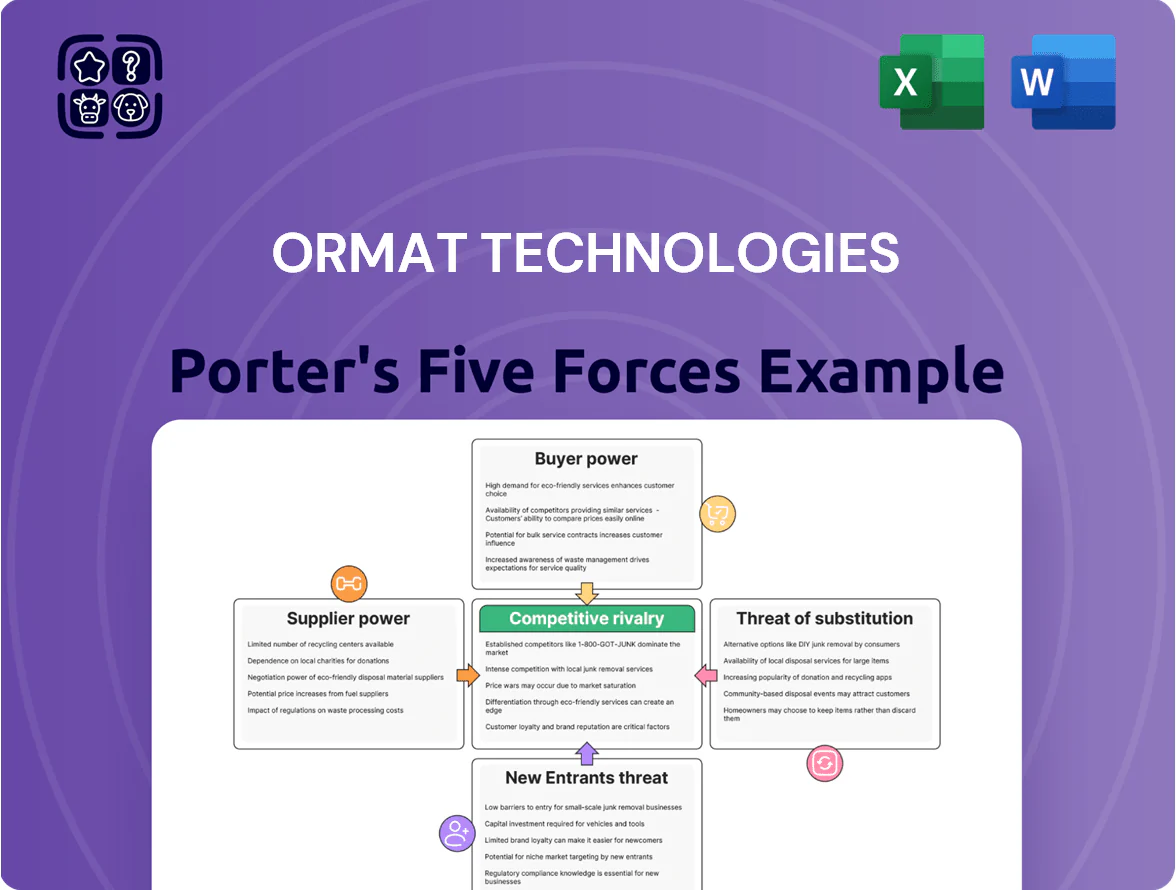

Ormat Technologies faces moderate competitive rivalry with niche geothermal expertise, regulatory tailwinds, and capital-intensive barriers that limit new entrants while supplier and buyer power vary by project scale; substitute threats (solar, storage) are rising but still complementary in many markets. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ormat Technologies’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Geothermal Equipment Components

Ormat's vertical integration—manufacturing turbines and heat exchangers in-house—cuts dependence on external tech suppliers and lowers supplier bargaining power, supporting a 2024 gross margin of ~31% (FY2024 revenue $1.03bn).

Still, the firm needs specialized steels and nickel alloys whose prices rose ~18% in 2021–24, exposing input-cost risk.

Ormat mitigates this via multi-sourcing across suppliers in the US, Japan, and Europe, and multi-year purchase contracts covering ~60% of projected 2025 material needs, lowering short-term price shock exposure.

Access to Geothermal Resource Rights

Primary suppliers—governments and private landowners holding geothermal resource rights—wield strong leverage because reservoirs are location-specific and finite, driving up lease premiums during initial contracting; for example, global geothermal licenses rose 6% in 2024 while lease costs in key markets like Kenya and Turkey increased ~12% year-over-year. Ormat mitigates this supplier power by holding a diversified portfolio of resource rights across North America, Latin America, Africa, and Asia-Pacific, with 2025 operational sites in 7 countries and development rights in 12, reducing dependence on any single jurisdiction.

Specialized Drilling and Engineering Services

Ormat usually self-develops but sometimes hires specialty contractors for deep geothermal drilling and complex civil works; the global pool of high-temperature geothermal drilling firms is under 50 major players, tightening supply when projects surge and raising day rates by 10–25% in 2023–24.

To curb supplier power, Ormat leans on its internal drilling subsidiary for most core needs—internal crews completed ~70% of its 2024 meter-drilled volume—reducing exposure to spot-market cost spikes and schedule delays.

Energy Storage Component Manufacturers

As Ormat expands energy storage, it depends on lithium-ion cell and power-electronics suppliers dominated by a few global firms—CATL, LG Energy Solution, Panasonic—giving suppliers strong pricing power; battery-cell ASPs fell ~18% in 2023 but supply constraints raised module costs in 2024.

Ormat reduces risk by qualifying alternative chemistries (LFP vs NMC), signing multi-year supply deals and targeting vertical integration for in-house inverters to stabilize margins.

- Supplier concentration: top 5 cell makers >70% global market share (2024)

- Battery ASP change: −18% in 2023; volatility returned in 2024

- Mitigation: diversify to LFP, long-term contracts, inverter insourcing

Local Labor and Technical Talent

The operation of geothermal plants needs engineers and technicians skilled in thermodynamics and geology, roles where global median salaries rose ~6% in 2024 to about $95k for senior geothermal engineers, boosting supplier (labor) leverage.

In remote regions limited local labor pools and unions can demand higher wages and benefits, raising O&M costs by an estimated 5–12% per site in 2023–24.

Ormat reduces this risk via heavy internal training—its 2024 workforce development spend rose to an estimated $12–15M—creating a proprietary pipeline and lowering external hiring needs.

- Skilled labor = high bargaining power

- Remote sites increase wage pressure (5–12%)

- Ormat training spend ~ $12–15M (2024)

- Internal pipeline lowers external dependency

Ormat: 31% FY24 margin, supplier squeeze eased by integration, contracts & training

Ormat faces moderate supplier power: vertical integration and in-house drilling cut dependence, supporting FY2024 gross margin ~31% on $1.03bn revenue, while specialty alloys (+18% 2021–24) and concentrated battery/cell suppliers (top5 >70% share, 2024) and scarce geothermal labor (senior avg ~$95k, +6% 2024) increase leverage; mitigations: multi-sourcing, 60% multi-year contracts for 2025, LFP qualification, $12–15M training (2024).

| Metric | Value |

|---|---|

| FY2024 revenue | $1.03bn |

| Gross margin FY2024 | ~31% |

| Alloy price change 2021–24 | +18% |

| Top5 cell makers share (2024) | >70% |

| Training spend (2024) | $12–15M |

What is included in the product

Tailored Porter's Five Forces analysis for Ormat Technologies, uncovering competitive drivers, customer and supplier influence, entry barriers, substitutes, and disruptive threats to its geothermal and energy solutions market position.

A concise Porter's Five Forces summary for Ormat Technologies—ideal for fast strategic decisions and investor briefings, with a clean layout ready to drop into decks and adapt to new market data.

Customers Bargaining Power

Concentration of Utility Off-takers

A significant share of Ormat Technologies revenue comes from a few large utilities—Southern California Edison and NV Energy accounted for about 28% of total revenue in 2024, giving these off-takers strong bargaining leverage due to purchase scale and influence on project financing.

That buyer power pressures pricing and contract terms, but is partly offset by utilities’ need to meet state renewable portfolio standards—California and Nevada mandates drove 2024 geothermal/renewable procurement, supporting long-term PPA demand.

Long-term Power Purchase Agreements

Long-term Power Purchase Agreements (PPAs) of 15–25 years lock in pricing and sharply reduce customers’ short-term bargaining power against Ormat Technologies, limiting renegotiation until contract expiry. During contract life, customers face switching costs and supply security concerns, so price pressure is low; historically Ormat reported 2024 contracted revenue of about $520 million, reflecting stable PPA-backed cash flows. However, in initial negotiations buyers can push prices using benchmarks—US utility-scale solar LCOE fell to ~$30/MWh in 2024—giving customers leverage before signing.

Availability of Alternative Renewable Energy

Utilities can buy solar, wind, or battery storage instead of geothermal, and by 2025 US utility-scale solar and wind LCOE averaged $24–32/MWh vs geothermal around $50–90/MWh, giving buyers leverage to press for lower prices and flexible terms.

That competition increases contract negotiation power, especially as battery storage deployments hit 30 GW US capacity in 2024, enabling firming of intermittent renewables.

Ormat stresses geothermal’s baseload reliability — ~90–95% capacity factor vs 25–35% for wind and 10–25% for solar — to justify premium pricing and long-term contracts.

Government and Regulatory Influence

- State buyers driven by mandates and budgets

- Policy/subsidy shifts lower prices, delay PPAs

- Ormat in 20+ countries by 2025 diversifies risk

Direct Equipment and Service Clients

Direct equipment clients can pit providers for price and specs, pressuring margins; Ormat sold $477m in product revenue in 2024, showing exposure to this dynamic.

Ormat’s reliability record and integrated one-stop-shop model—services plus equipment—boost retention: 2024 service revenue hit $305m, helping offset pricing pressure.

- Product revenue 2024: $477m

- Service revenue 2024: $305m

- Clients can play vendors off each other

- Integrated model raises switching costs

Customers Hold Leverage: Large Buyers, Cheaper Renewables, but Diversification Shields Revenue

Customers hold moderate-to-high bargaining power: top utilities (SCE, NV Energy) made ~28% of 2024 revenue, pressuring price and terms, but 15–25y PPAs (contracted revenue ~$520M in 2024) limit short-term renegotiation; competing LCOEs (solar/wind $24–32/MWh vs geothermal $50–90/MWh in 2025) give buyers leverage; diversification to 20+ countries and service revenue $305M cushions pressure.

| Metric | Value |

|---|---|

| Top-2 share 2024 | ~28% |

| Contracted rev 2024 | $520M |

| Product rev 2024 | $477M |

| Service rev 2024 | $305M |

| US RES LCOE 2025 | $24–32/MWh |

| Geothermal LCOE 2025 | $50–90/MWh |

| Countries of ops 2025 | 20+ |

Full Version Awaits

Ormat Technologies Porter's Five Forces Analysis

This preview shows the exact Ormat Technologies Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, ready for download and use upon payment, and contains the complete, professionally written assessment of competitive rivalry, supplier and buyer power, threats of substitutes, and barriers to entry.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Ormat Technologies faces moderate competitive rivalry with niche geothermal expertise, regulatory tailwinds, and capital-intensive barriers that limit new entrants while supplier and buyer power vary by project scale; substitute threats (solar, storage) are rising but still complementary in many markets. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ormat Technologies’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Geothermal Equipment Components

Ormat's vertical integration—manufacturing turbines and heat exchangers in-house—cuts dependence on external tech suppliers and lowers supplier bargaining power, supporting a 2024 gross margin of ~31% (FY2024 revenue $1.03bn).

Still, the firm needs specialized steels and nickel alloys whose prices rose ~18% in 2021–24, exposing input-cost risk.

Ormat mitigates this via multi-sourcing across suppliers in the US, Japan, and Europe, and multi-year purchase contracts covering ~60% of projected 2025 material needs, lowering short-term price shock exposure.

Access to Geothermal Resource Rights

Primary suppliers—governments and private landowners holding geothermal resource rights—wield strong leverage because reservoirs are location-specific and finite, driving up lease premiums during initial contracting; for example, global geothermal licenses rose 6% in 2024 while lease costs in key markets like Kenya and Turkey increased ~12% year-over-year. Ormat mitigates this supplier power by holding a diversified portfolio of resource rights across North America, Latin America, Africa, and Asia-Pacific, with 2025 operational sites in 7 countries and development rights in 12, reducing dependence on any single jurisdiction.

Specialized Drilling and Engineering Services

Ormat usually self-develops but sometimes hires specialty contractors for deep geothermal drilling and complex civil works; the global pool of high-temperature geothermal drilling firms is under 50 major players, tightening supply when projects surge and raising day rates by 10–25% in 2023–24.

To curb supplier power, Ormat leans on its internal drilling subsidiary for most core needs—internal crews completed ~70% of its 2024 meter-drilled volume—reducing exposure to spot-market cost spikes and schedule delays.

Energy Storage Component Manufacturers

As Ormat expands energy storage, it depends on lithium-ion cell and power-electronics suppliers dominated by a few global firms—CATL, LG Energy Solution, Panasonic—giving suppliers strong pricing power; battery-cell ASPs fell ~18% in 2023 but supply constraints raised module costs in 2024.

Ormat reduces risk by qualifying alternative chemistries (LFP vs NMC), signing multi-year supply deals and targeting vertical integration for in-house inverters to stabilize margins.

- Supplier concentration: top 5 cell makers >70% global market share (2024)

- Battery ASP change: −18% in 2023; volatility returned in 2024

- Mitigation: diversify to LFP, long-term contracts, inverter insourcing

Local Labor and Technical Talent

The operation of geothermal plants needs engineers and technicians skilled in thermodynamics and geology, roles where global median salaries rose ~6% in 2024 to about $95k for senior geothermal engineers, boosting supplier (labor) leverage.

In remote regions limited local labor pools and unions can demand higher wages and benefits, raising O&M costs by an estimated 5–12% per site in 2023–24.

Ormat reduces this risk via heavy internal training—its 2024 workforce development spend rose to an estimated $12–15M—creating a proprietary pipeline and lowering external hiring needs.

- Skilled labor = high bargaining power

- Remote sites increase wage pressure (5–12%)

- Ormat training spend ~ $12–15M (2024)

- Internal pipeline lowers external dependency

Ormat: 31% FY24 margin, supplier squeeze eased by integration, contracts & training

Ormat faces moderate supplier power: vertical integration and in-house drilling cut dependence, supporting FY2024 gross margin ~31% on $1.03bn revenue, while specialty alloys (+18% 2021–24) and concentrated battery/cell suppliers (top5 >70% share, 2024) and scarce geothermal labor (senior avg ~$95k, +6% 2024) increase leverage; mitigations: multi-sourcing, 60% multi-year contracts for 2025, LFP qualification, $12–15M training (2024).

| Metric | Value |

|---|---|

| FY2024 revenue | $1.03bn |

| Gross margin FY2024 | ~31% |

| Alloy price change 2021–24 | +18% |

| Top5 cell makers share (2024) | >70% |

| Training spend (2024) | $12–15M |

What is included in the product

Tailored Porter's Five Forces analysis for Ormat Technologies, uncovering competitive drivers, customer and supplier influence, entry barriers, substitutes, and disruptive threats to its geothermal and energy solutions market position.

A concise Porter's Five Forces summary for Ormat Technologies—ideal for fast strategic decisions and investor briefings, with a clean layout ready to drop into decks and adapt to new market data.

Customers Bargaining Power

Concentration of Utility Off-takers

A significant share of Ormat Technologies revenue comes from a few large utilities—Southern California Edison and NV Energy accounted for about 28% of total revenue in 2024, giving these off-takers strong bargaining leverage due to purchase scale and influence on project financing.

That buyer power pressures pricing and contract terms, but is partly offset by utilities’ need to meet state renewable portfolio standards—California and Nevada mandates drove 2024 geothermal/renewable procurement, supporting long-term PPA demand.

Long-term Power Purchase Agreements

Long-term Power Purchase Agreements (PPAs) of 15–25 years lock in pricing and sharply reduce customers’ short-term bargaining power against Ormat Technologies, limiting renegotiation until contract expiry. During contract life, customers face switching costs and supply security concerns, so price pressure is low; historically Ormat reported 2024 contracted revenue of about $520 million, reflecting stable PPA-backed cash flows. However, in initial negotiations buyers can push prices using benchmarks—US utility-scale solar LCOE fell to ~$30/MWh in 2024—giving customers leverage before signing.

Availability of Alternative Renewable Energy

Utilities can buy solar, wind, or battery storage instead of geothermal, and by 2025 US utility-scale solar and wind LCOE averaged $24–32/MWh vs geothermal around $50–90/MWh, giving buyers leverage to press for lower prices and flexible terms.

That competition increases contract negotiation power, especially as battery storage deployments hit 30 GW US capacity in 2024, enabling firming of intermittent renewables.

Ormat stresses geothermal’s baseload reliability — ~90–95% capacity factor vs 25–35% for wind and 10–25% for solar — to justify premium pricing and long-term contracts.

Government and Regulatory Influence

- State buyers driven by mandates and budgets

- Policy/subsidy shifts lower prices, delay PPAs

- Ormat in 20+ countries by 2025 diversifies risk

Direct Equipment and Service Clients

Direct equipment clients can pit providers for price and specs, pressuring margins; Ormat sold $477m in product revenue in 2024, showing exposure to this dynamic.

Ormat’s reliability record and integrated one-stop-shop model—services plus equipment—boost retention: 2024 service revenue hit $305m, helping offset pricing pressure.

- Product revenue 2024: $477m

- Service revenue 2024: $305m

- Clients can play vendors off each other

- Integrated model raises switching costs

Customers Hold Leverage: Large Buyers, Cheaper Renewables, but Diversification Shields Revenue

Customers hold moderate-to-high bargaining power: top utilities (SCE, NV Energy) made ~28% of 2024 revenue, pressuring price and terms, but 15–25y PPAs (contracted revenue ~$520M in 2024) limit short-term renegotiation; competing LCOEs (solar/wind $24–32/MWh vs geothermal $50–90/MWh in 2025) give buyers leverage; diversification to 20+ countries and service revenue $305M cushions pressure.

| Metric | Value |

|---|---|

| Top-2 share 2024 | ~28% |

| Contracted rev 2024 | $520M |

| Product rev 2024 | $477M |

| Service rev 2024 | $305M |

| US RES LCOE 2025 | $24–32/MWh |

| Geothermal LCOE 2025 | $50–90/MWh |

| Countries of ops 2025 | 20+ |

Full Version Awaits

Ormat Technologies Porter's Five Forces Analysis

This preview shows the exact Ormat Technologies Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, ready for download and use upon payment, and contains the complete, professionally written assessment of competitive rivalry, supplier and buyer power, threats of substitutes, and barriers to entry.