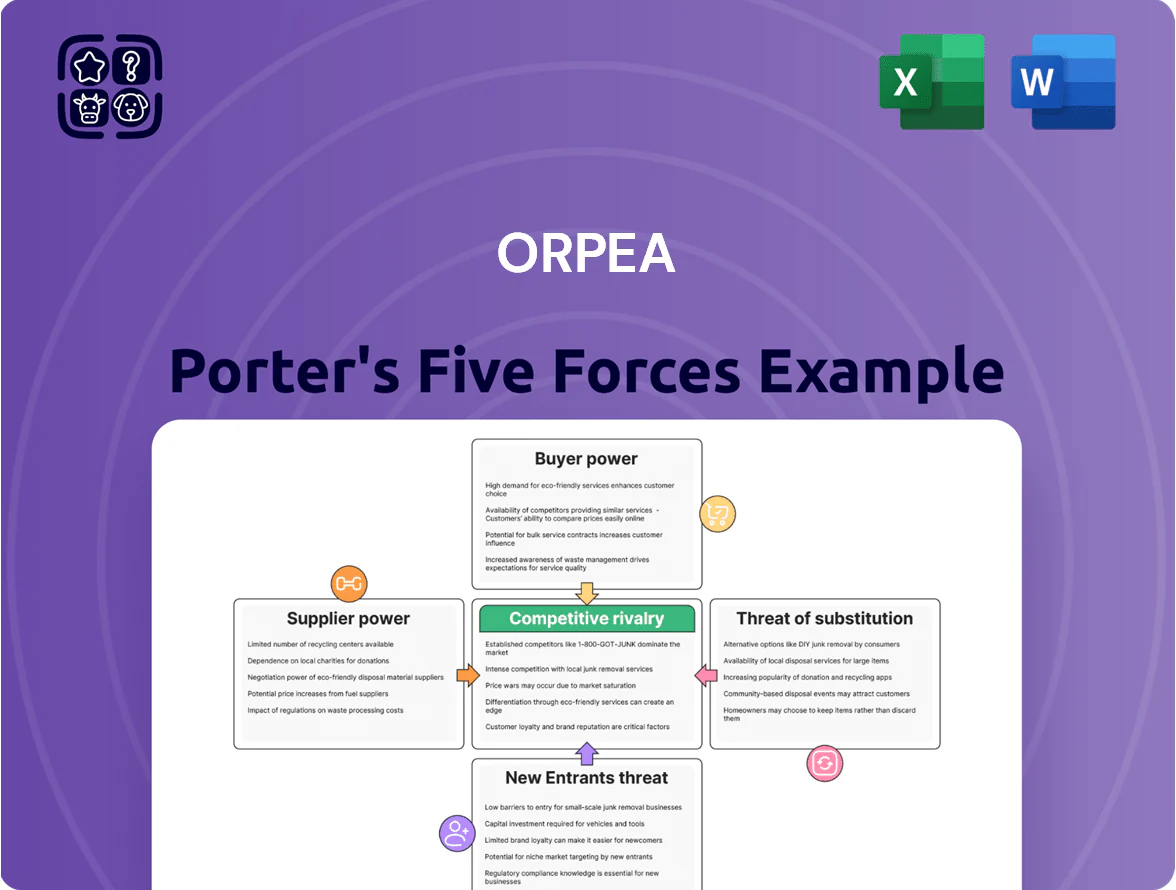

Orpea Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Unlock the full Porter's Five Forces Analysis to explore Orpea’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of specialized medical and nursing staff

Primary suppliers for Orpea are skilled nurses and caregivers; their bargaining power is high due to chronic global shortages in geriatric care. As of late 2025, nurse vacancy rates in Western Europe averaged ~12–14%, forcing Orpea to raise wages by roughly 8–11% and invest in benefits to meet mandated staffing ratios. Labor costs now account for about 55–60% of operating expenses, constraining margin compression.

Real estate developers and landlords

Orpea depends on developers and REITs for sites; by 2024 around 40% of its estate was leased, raising supplier leverage during renewals.

The asset-light shift lowers capital burden but healthcare-specific layouts limit relocations, so landlords can demand higher rents or stricter terms.

Rising construction costs—EU average +12% in 2023—and higher borrowing rates (ECB policy rate 3.75% end-2024) strengthen owners’ bargaining power.

Pharmaceutical and medical equipment providers

Suppliers of specialized devices, diagnostics, and drugs hold moderate power over Orpea because their products are essential; in 2024 Orpea bought €1.2bn of medical supplies, letting scale secure volume discounts but not full price control.

Many life‑saving drugs and advanced rehab tools have few substitutes, so switching is hard; regulatory constraints (EU MDR, national drug approvals) further limit moves to lower‑cost, unverified suppliers.

Energy and utility providers

Energy needs for Orpea’s care homes are high—heating, cooling, and medical gear can account for 12–18% of operating costs; in 2024 European industrial electricity prices averaged ~€0.18/kWh, up ~35% vs 2020, and volatility persisted into 2025.

Orpea faces weak bargaining power vs local utility monopolies, creating fixed-cost pressure that is hard to cut without capex: on-site solar+storage payback often exceeds 8–12 years for large campuses.

Food service and facility management vendors

- High dependency: few certified vendors raise switching costs

- Risk metric: 62% cite vendor reliability (2024)

- Cost trade-off: lower price vs reputational risk

- Mitigation: multi-vendor contracts, SLAs, contingency stocks

Supplier squeeze: rising wages, leased estates and €1.2bn supply costs bite margins

Suppliers exert above‑average power: labor shortages (nurse vacancy ~12–14% in W. Europe) pushed Orpea to raise wages ~8–11%, making labor 55–60% of costs; landlords hold leverage with ~40% leased estate; medical suppliers are moderately powerful (Orpea bought €1.2bn supplies in 2024); utilities and outsourced services add fixed-cost and switching risks.

| Item | 2024–25 |

|---|---|

| Nurse vacancy W. Europe | 12–14% |

| Wage uplift | +8–11% |

| Labor share | 55–60% ops |

| Leased estate | ~40% |

| Medical supplies spend | €1.2bn (2024) |

| Energy price EU avg | ~€0.18/kWh (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Orpea that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and disruptive risks—designed for easy incorporation into investor reports, strategy decks, or academic work.

Compact Porter's Five Forces for Orpea—clear single-sheet view to speed strategic decisions and spot regulatory, supplier, and reputational pressures at a glance.

Customers Bargaining Power

State and social security reimbursement bodies

In countries like France and Germany, national health insurers and social security bodies set reimbursement rates and occupancy subsidies, giving them immense bargaining power over Orpea; in France public payers cover ~60–70% of long-term care funding and reimbursed tariffs rose <2% annually 2019–2024 while labor costs climbed ~20% (2019–2024), squeezing margins.

Individual residents and their families

Wealthier private-pay residents exert strong bargaining power: in France and Germany roughly 20–30% of clients are private-pay, and premium providers compete on service and pricing, pushing Orpea to match higher standards and margins.

After the 2020–2022 scandals, 68% of families say transparency is a deal-breaker, raising demands for accountability and contract clarity.

Online reviews and national quality ratings (e.g., France’s 2024 HAS indicators) let customers compare care; facilities losing one-star equivalents can see occupancy drops of 5–10% within 12 months.

Insurance companies and private health funds

Private insurers and health funds bargain hard, using member pools to secure bulk rates—France’s complementary insurers covered ~77% of rehab stays in 2023, pushing average price discounts of 8–15% versus list rates.

As Orpea grew post-acute revenue to ~€420m in 2024, dependence on institutional payers rose, concentrating pricing risk.

Payers enforce clinical pathways and audits; failing audits can drop Orpea from preferred lists and cut occupancy by double-digit points.

Low switching costs for prospective residents

While relocating a resident is emotionally and physically hard, the pre-admission choice is fiercely competitive: 74% of French families surveyed in 2024 compared three or more facilities by location, price, and services before signing, per INSEE-linked sector data.

This transparency and price visibility mean Orpea must sustain high clinical, staffing, and amenity standards to win new admissions in a market with ~12% annual turnover of open beds.

Here’s the quick math: 3x options reviewed × 12% bed churn raises marketing and quality costs by an estimated 150–220 basis points of revenue.

- High pre-admission comparison: 74% compared ≥3 facilities

- Market churn pressure: ~12% annual open-bed turnover

- Cost impact: quality/marketing +150–220 bps of revenue

Influence of advocacy groups and patient unions

Patient rights orgs and elderly advocacy groups shape legislation and public opinion, indirectly cutting Orpea’s pricing autonomy after 2022 scandals that led to a 15% French revenue hit in 2023 for reputation remediation.

The groups lobby for tighter quality and pricing rules; EU inquiries and fines since 2022 raise compliance costs and limit margin expansion.

Their mobilization power—media campaigns and class actions—elevates switching and regulatory risk for Orpea, pressuring service fees and investor sentiment.

- Advocacy-driven regulation reduces pricing flexibility

- 2022–2023 scandals cost ~15% French revenue

- Media/class actions raise compliance and legal costs

- Public mobilization increases switching and funding risk

Insurers squeeze tariffs; ratings shift occupancy ±10%—€420m institutional risk

Payers (public insurers cover ~60–70% in France) and private insurers force tariffs and bulk discounts (8–15%), while private-pay clients (20–30%) demand premium services; post-2020 scandals transparency needs (68% families) and quality ratings (HAS 2024) drive 5–10% occupancy swings, raising marketing/quality costs ~150–220 bps and concentrating pricing risk as institutional revenue reached ~€420m (2024).

| Metric | Value (2024) |

|---|---|

| Public funding share (FR) | 60–70% |

| Private-pay share | 20–30% |

| Occupancy drop after rating loss | 5–10% |

| Marketing/quality cost | +150–220 bps |

| Institutional revenue | €420m |

Full Version Awaits

Orpea Porter's Five Forces Analysis

This preview shows the exact Orpea Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready to download with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Unlock the full Porter's Five Forces Analysis to explore Orpea’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of specialized medical and nursing staff

Primary suppliers for Orpea are skilled nurses and caregivers; their bargaining power is high due to chronic global shortages in geriatric care. As of late 2025, nurse vacancy rates in Western Europe averaged ~12–14%, forcing Orpea to raise wages by roughly 8–11% and invest in benefits to meet mandated staffing ratios. Labor costs now account for about 55–60% of operating expenses, constraining margin compression.

Real estate developers and landlords

Orpea depends on developers and REITs for sites; by 2024 around 40% of its estate was leased, raising supplier leverage during renewals.

The asset-light shift lowers capital burden but healthcare-specific layouts limit relocations, so landlords can demand higher rents or stricter terms.

Rising construction costs—EU average +12% in 2023—and higher borrowing rates (ECB policy rate 3.75% end-2024) strengthen owners’ bargaining power.

Pharmaceutical and medical equipment providers

Suppliers of specialized devices, diagnostics, and drugs hold moderate power over Orpea because their products are essential; in 2024 Orpea bought €1.2bn of medical supplies, letting scale secure volume discounts but not full price control.

Many life‑saving drugs and advanced rehab tools have few substitutes, so switching is hard; regulatory constraints (EU MDR, national drug approvals) further limit moves to lower‑cost, unverified suppliers.

Energy and utility providers

Energy needs for Orpea’s care homes are high—heating, cooling, and medical gear can account for 12–18% of operating costs; in 2024 European industrial electricity prices averaged ~€0.18/kWh, up ~35% vs 2020, and volatility persisted into 2025.

Orpea faces weak bargaining power vs local utility monopolies, creating fixed-cost pressure that is hard to cut without capex: on-site solar+storage payback often exceeds 8–12 years for large campuses.

Food service and facility management vendors

- High dependency: few certified vendors raise switching costs

- Risk metric: 62% cite vendor reliability (2024)

- Cost trade-off: lower price vs reputational risk

- Mitigation: multi-vendor contracts, SLAs, contingency stocks

Supplier squeeze: rising wages, leased estates and €1.2bn supply costs bite margins

Suppliers exert above‑average power: labor shortages (nurse vacancy ~12–14% in W. Europe) pushed Orpea to raise wages ~8–11%, making labor 55–60% of costs; landlords hold leverage with ~40% leased estate; medical suppliers are moderately powerful (Orpea bought €1.2bn supplies in 2024); utilities and outsourced services add fixed-cost and switching risks.

| Item | 2024–25 |

|---|---|

| Nurse vacancy W. Europe | 12–14% |

| Wage uplift | +8–11% |

| Labor share | 55–60% ops |

| Leased estate | ~40% |

| Medical supplies spend | €1.2bn (2024) |

| Energy price EU avg | ~€0.18/kWh (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Orpea that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and disruptive risks—designed for easy incorporation into investor reports, strategy decks, or academic work.

Compact Porter's Five Forces for Orpea—clear single-sheet view to speed strategic decisions and spot regulatory, supplier, and reputational pressures at a glance.

Customers Bargaining Power

State and social security reimbursement bodies

In countries like France and Germany, national health insurers and social security bodies set reimbursement rates and occupancy subsidies, giving them immense bargaining power over Orpea; in France public payers cover ~60–70% of long-term care funding and reimbursed tariffs rose <2% annually 2019–2024 while labor costs climbed ~20% (2019–2024), squeezing margins.

Individual residents and their families

Wealthier private-pay residents exert strong bargaining power: in France and Germany roughly 20–30% of clients are private-pay, and premium providers compete on service and pricing, pushing Orpea to match higher standards and margins.

After the 2020–2022 scandals, 68% of families say transparency is a deal-breaker, raising demands for accountability and contract clarity.

Online reviews and national quality ratings (e.g., France’s 2024 HAS indicators) let customers compare care; facilities losing one-star equivalents can see occupancy drops of 5–10% within 12 months.

Insurance companies and private health funds

Private insurers and health funds bargain hard, using member pools to secure bulk rates—France’s complementary insurers covered ~77% of rehab stays in 2023, pushing average price discounts of 8–15% versus list rates.

As Orpea grew post-acute revenue to ~€420m in 2024, dependence on institutional payers rose, concentrating pricing risk.

Payers enforce clinical pathways and audits; failing audits can drop Orpea from preferred lists and cut occupancy by double-digit points.

Low switching costs for prospective residents

While relocating a resident is emotionally and physically hard, the pre-admission choice is fiercely competitive: 74% of French families surveyed in 2024 compared three or more facilities by location, price, and services before signing, per INSEE-linked sector data.

This transparency and price visibility mean Orpea must sustain high clinical, staffing, and amenity standards to win new admissions in a market with ~12% annual turnover of open beds.

Here’s the quick math: 3x options reviewed × 12% bed churn raises marketing and quality costs by an estimated 150–220 basis points of revenue.

- High pre-admission comparison: 74% compared ≥3 facilities

- Market churn pressure: ~12% annual open-bed turnover

- Cost impact: quality/marketing +150–220 bps of revenue

Influence of advocacy groups and patient unions

Patient rights orgs and elderly advocacy groups shape legislation and public opinion, indirectly cutting Orpea’s pricing autonomy after 2022 scandals that led to a 15% French revenue hit in 2023 for reputation remediation.

The groups lobby for tighter quality and pricing rules; EU inquiries and fines since 2022 raise compliance costs and limit margin expansion.

Their mobilization power—media campaigns and class actions—elevates switching and regulatory risk for Orpea, pressuring service fees and investor sentiment.

- Advocacy-driven regulation reduces pricing flexibility

- 2022–2023 scandals cost ~15% French revenue

- Media/class actions raise compliance and legal costs

- Public mobilization increases switching and funding risk

Insurers squeeze tariffs; ratings shift occupancy ±10%—€420m institutional risk

Payers (public insurers cover ~60–70% in France) and private insurers force tariffs and bulk discounts (8–15%), while private-pay clients (20–30%) demand premium services; post-2020 scandals transparency needs (68% families) and quality ratings (HAS 2024) drive 5–10% occupancy swings, raising marketing/quality costs ~150–220 bps and concentrating pricing risk as institutional revenue reached ~€420m (2024).

| Metric | Value (2024) |

|---|---|

| Public funding share (FR) | 60–70% |

| Private-pay share | 20–30% |

| Occupancy drop after rating loss | 5–10% |

| Marketing/quality cost | +150–220 bps |

| Institutional revenue | €420m |

Full Version Awaits

Orpea Porter's Five Forces Analysis

This preview shows the exact Orpea Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready to download with no placeholders or samples.