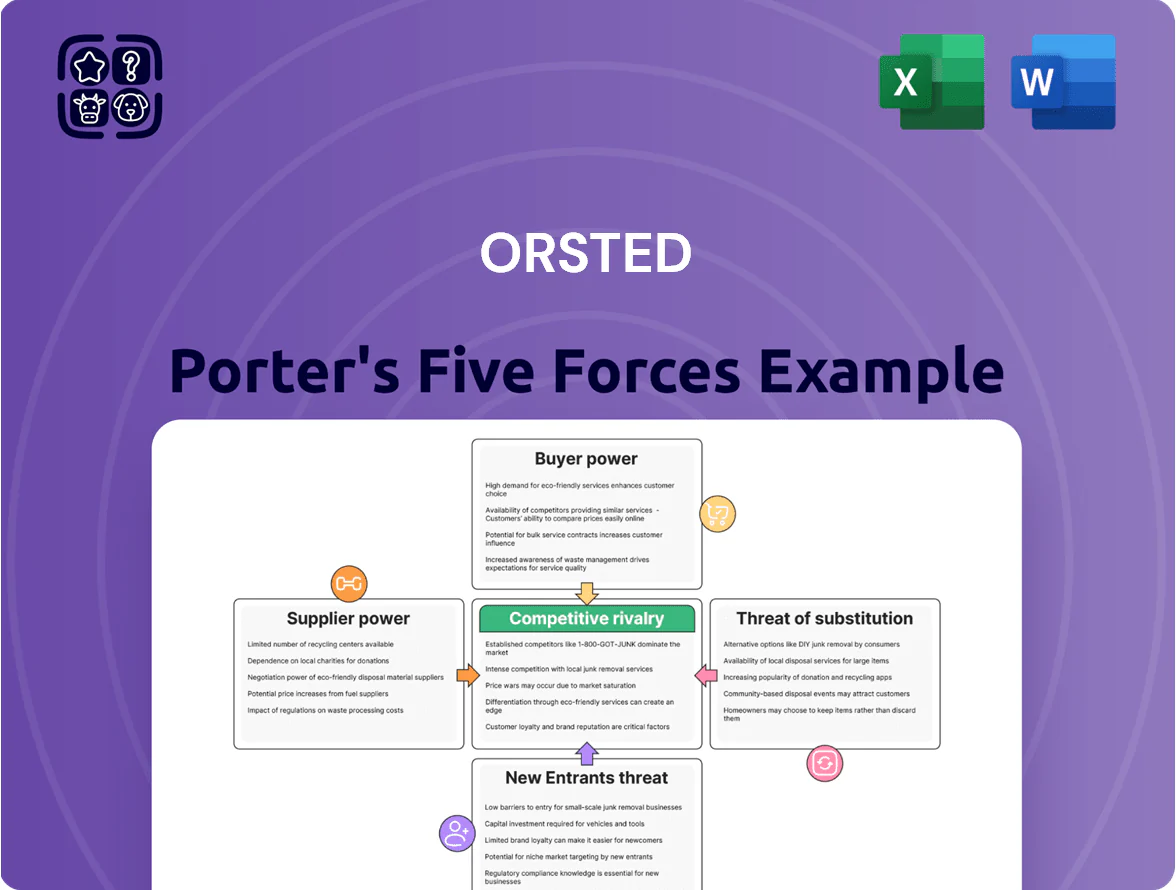

Orsted Porter's Five Forces Analysis

Don't Miss the Bigger Picture

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Orsted’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of specialized turbine manufacturers

The offshore wind market is concentrated among Siemens Gamesa, Vestas, and GE, which together supplied over 70% of global offshore turbine capacity in 2024, giving them strong pricing and delivery leverage over Orsted.

The firms’ specialized 10–15+ MW nacelles and blade designs are critical for Orsted’s large projects, forcing reliance on long-term contracts and capacity reservations to secure supply.

By late 2025, only a handful of confirmed 15+ MW turbine deliveries exist (estimated <20 GW pipeline globally), raising Orsted’s dependency and exposure to lead-time and price risk.

Raw material price volatility

Steel, copper, and rare earths drive 35–50% of turbine and solar balance-of-system costs; a 20% steel price rise in 2024 raised onshore wind CAPEX by ~4–6%, so suppliers can materially cut Orsted’s margins.

Suppliers passed through cost spikes in 2022–24; with late-2025 geopolitical shifts, Orsted faces higher capital-expenditure uncertainty and must hedge or secure long-term contracts to limit supplier leverage.

Specialized vessel and logistics constraints

The global fleet of Wind Turbine Installation Vessels (WTIVs) able to lift 2,000+ tonnes and install 15+ MW turbines is under 30 units in 2025, so owners command day rates often €200–€400k and multi-year charters; peak offshore installation activity raises rates ~25% y/y in 2024–25. Orsted must book vessels 2–4 years ahead, creating strong supplier bargaining power and exposure to high fixed logistics costs.

Grid connection and infrastructure providers

Escalating labor costs for technical expertise

Supply squeeze leaves Ørsted exposed: scarce turbines, costly HVDC, rising CAPEX risk

Supplier concentration (Siemens Gamesa, Vestas, GE >70% 2024) plus scarce 15+ MW turbines (<20 GW pipeline 2025), <30 WTIVs, HVDC cable costs $3–5m/km (2024) and 24+ month lead times give Ørsted low switching power, higher CAPEX risk, and need for long-term contracts to protect margins.

| Metric | Value |

|---|---|

| Turbine suppliers share (2024) | >70% |

| 15+ MW pipeline (2025) | <20 GW |

| WTIVs ≥2,000t (2025) | <30 units |

| HVDC cost (2024) | $3–5m/km |

| HVDC lead time | 24+ months |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and rivalry specific to Ørsted, highlighting disruptive threats, pricing influence, and strategic protections that shape its profitability and market position.

A concise, one-sheet Porter's Five Forces view for Ørsted—clarifies competitive pressure and regulatory risk fast, ready to drop into investor decks or strategy memos.

Customers Bargaining Power

Government-led auction and tender systems

National governments award Orsted’s large-scale contracts via auctions and tenders, giving them strong bargaining power over price and subsidy terms; for example, UK Contracts for Difference (CfD) awarded in 2023 cleared at £37.35/MWh for offshore wind, constraining revenue upside.

Because CfDs and Power Purchase Agreements (PPAs) set floors, ceilings, and subsidy levels, Orsted often bids into thin margins to secure 15–20 year revenue visibility on projects like Hornsea 2 and 3.

Corporate Power Purchase Agreements (PPAs)

Wholesale market price sensitivity

A portion of Orsted’s 2024 revenue—about 18% of DKK 78.5bn (≈US$11.7bn)—comes from selling power into volatile wholesale markets where hourly prices swung 40–60% year-on-year in some European zones in 2024.

Large utilities and retailers switch hourly to the cheapest source, so Orsted faces high buyer price sensitivity and switching power in the merchant segment.

Because electricity is commoditized, Orsted has limited pricing control in merchant sales, exposing margins to spot-price volatility; hedges covered roughly 70% of 2025 output as of Dec 2024.

Public and political scrutiny on energy bills

As a major energy provider, Orsted faces indirect customer power via political pressure: in 2023–2025 many EU states introduced or debated price caps and windfall taxes after wholesale price spikes—UK windfall tax raised £5bn in 2022–23—so governments can compel revenue limits or levies to protect households.

This political pressure effectively gives the public collective bargaining power that shapes Orsted’s regulatory risks and returns, raising policy uncertainty and potential margin compression.

- 2023–25: EU/UK price-cap and windfall moves

- UK windfall tax ~£5bn (2022–23)

- Raises regulatory risk, potential margin squeeze

Low switching costs for green energy certificates

Businesses can swap Renewable Energy Certificates (RECs) between developers with almost no cost, so Orsted competes mainly on price for that identical environmental attribute per MWh.

In 2024 US REC prices ranged broadly—state-specific vintage RECs as low as $1–$5/MWh while voluntary market RECs averaged about $2–$4/MWh—giving buyers strong leverage to seek lowest-cost suppliers.

Buyers squeeze Ørsted: low CfDs/PPAs, high hedges cap upside

Buyers—governments via CfDs (eg UK 2023 CfD £37.35/MWh), large corporates (≈28 GW PPAs in 2023), utilities/retailers and REC traders—hold strong bargaining power through auctions, long-tenor PPAs, low switching costs, and REC fungibility, compressing Orsted’s project IRRs; about 18% of 2024 revenue (DKK 78.5bn) from volatile wholesale markets and ~70% hedge cover for 2025 limit upside.

| Metric | Value |

|---|---|

| UK CfD (2023) | £37.35/MWh |

| Corporate PPAs (2023) | ~28 GW |

| Orsted 2024 revenue from power | 18% of DKK 78.5bn |

| 2025 hedge cover | ~70% |

Full Version Awaits

Orsted Porter's Five Forces Analysis

This preview shows the exact Orsted Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the part of the full, professionally written file you’ll get—fully formatted and ready for download and use the moment you buy. You're looking at the actual deliverable; once you complete your purchase, you’ll get instant access to this same file. No mockups, no samples—the preview equals the final, ready-to-use analysis.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Orsted’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of specialized turbine manufacturers

The offshore wind market is concentrated among Siemens Gamesa, Vestas, and GE, which together supplied over 70% of global offshore turbine capacity in 2024, giving them strong pricing and delivery leverage over Orsted.

The firms’ specialized 10–15+ MW nacelles and blade designs are critical for Orsted’s large projects, forcing reliance on long-term contracts and capacity reservations to secure supply.

By late 2025, only a handful of confirmed 15+ MW turbine deliveries exist (estimated <20 GW pipeline globally), raising Orsted’s dependency and exposure to lead-time and price risk.

Raw material price volatility

Steel, copper, and rare earths drive 35–50% of turbine and solar balance-of-system costs; a 20% steel price rise in 2024 raised onshore wind CAPEX by ~4–6%, so suppliers can materially cut Orsted’s margins.

Suppliers passed through cost spikes in 2022–24; with late-2025 geopolitical shifts, Orsted faces higher capital-expenditure uncertainty and must hedge or secure long-term contracts to limit supplier leverage.

Specialized vessel and logistics constraints

The global fleet of Wind Turbine Installation Vessels (WTIVs) able to lift 2,000+ tonnes and install 15+ MW turbines is under 30 units in 2025, so owners command day rates often €200–€400k and multi-year charters; peak offshore installation activity raises rates ~25% y/y in 2024–25. Orsted must book vessels 2–4 years ahead, creating strong supplier bargaining power and exposure to high fixed logistics costs.

Grid connection and infrastructure providers

Escalating labor costs for technical expertise

Supply squeeze leaves Ørsted exposed: scarce turbines, costly HVDC, rising CAPEX risk

Supplier concentration (Siemens Gamesa, Vestas, GE >70% 2024) plus scarce 15+ MW turbines (<20 GW pipeline 2025), <30 WTIVs, HVDC cable costs $3–5m/km (2024) and 24+ month lead times give Ørsted low switching power, higher CAPEX risk, and need for long-term contracts to protect margins.

| Metric | Value |

|---|---|

| Turbine suppliers share (2024) | >70% |

| 15+ MW pipeline (2025) | <20 GW |

| WTIVs ≥2,000t (2025) | <30 units |

| HVDC cost (2024) | $3–5m/km |

| HVDC lead time | 24+ months |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and rivalry specific to Ørsted, highlighting disruptive threats, pricing influence, and strategic protections that shape its profitability and market position.

A concise, one-sheet Porter's Five Forces view for Ørsted—clarifies competitive pressure and regulatory risk fast, ready to drop into investor decks or strategy memos.

Customers Bargaining Power

Government-led auction and tender systems

National governments award Orsted’s large-scale contracts via auctions and tenders, giving them strong bargaining power over price and subsidy terms; for example, UK Contracts for Difference (CfD) awarded in 2023 cleared at £37.35/MWh for offshore wind, constraining revenue upside.

Because CfDs and Power Purchase Agreements (PPAs) set floors, ceilings, and subsidy levels, Orsted often bids into thin margins to secure 15–20 year revenue visibility on projects like Hornsea 2 and 3.

Corporate Power Purchase Agreements (PPAs)

Wholesale market price sensitivity

A portion of Orsted’s 2024 revenue—about 18% of DKK 78.5bn (≈US$11.7bn)—comes from selling power into volatile wholesale markets where hourly prices swung 40–60% year-on-year in some European zones in 2024.

Large utilities and retailers switch hourly to the cheapest source, so Orsted faces high buyer price sensitivity and switching power in the merchant segment.

Because electricity is commoditized, Orsted has limited pricing control in merchant sales, exposing margins to spot-price volatility; hedges covered roughly 70% of 2025 output as of Dec 2024.

Public and political scrutiny on energy bills

As a major energy provider, Orsted faces indirect customer power via political pressure: in 2023–2025 many EU states introduced or debated price caps and windfall taxes after wholesale price spikes—UK windfall tax raised £5bn in 2022–23—so governments can compel revenue limits or levies to protect households.

This political pressure effectively gives the public collective bargaining power that shapes Orsted’s regulatory risks and returns, raising policy uncertainty and potential margin compression.

- 2023–25: EU/UK price-cap and windfall moves

- UK windfall tax ~£5bn (2022–23)

- Raises regulatory risk, potential margin squeeze

Low switching costs for green energy certificates

Businesses can swap Renewable Energy Certificates (RECs) between developers with almost no cost, so Orsted competes mainly on price for that identical environmental attribute per MWh.

In 2024 US REC prices ranged broadly—state-specific vintage RECs as low as $1–$5/MWh while voluntary market RECs averaged about $2–$4/MWh—giving buyers strong leverage to seek lowest-cost suppliers.

Buyers squeeze Ørsted: low CfDs/PPAs, high hedges cap upside

Buyers—governments via CfDs (eg UK 2023 CfD £37.35/MWh), large corporates (≈28 GW PPAs in 2023), utilities/retailers and REC traders—hold strong bargaining power through auctions, long-tenor PPAs, low switching costs, and REC fungibility, compressing Orsted’s project IRRs; about 18% of 2024 revenue (DKK 78.5bn) from volatile wholesale markets and ~70% hedge cover for 2025 limit upside.

| Metric | Value |

|---|---|

| UK CfD (2023) | £37.35/MWh |

| Corporate PPAs (2023) | ~28 GW |

| Orsted 2024 revenue from power | 18% of DKK 78.5bn |

| 2025 hedge cover | ~70% |

Full Version Awaits

Orsted Porter's Five Forces Analysis

This preview shows the exact Orsted Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the part of the full, professionally written file you’ll get—fully formatted and ready for download and use the moment you buy. You're looking at the actual deliverable; once you complete your purchase, you’ll get instant access to this same file. No mockups, no samples—the preview equals the final, ready-to-use analysis.