Osaka Gas PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, energy policy, and technological innovation are reshaping Osaka Gas’s prospects—our concise PESTLE snapshot reveals key risks and opportunities to inform smarter strategy and investment decisions; purchase the full PESTLE for a detailed, ready-to-use analysis that’s ideal for reports, pitches, and boardroom planning.

Political factors

Strategic Energy Plan Alignment

The Japanese 7th Strategic Energy Plan targets reducing CO2 emissions 46% by 2030 vs 2013 and net-zero by 2050, cementing natural gas as a transition fuel; Osaka Gas must align its strategy to meet these state mandates while pivoting toward hydrogen and ammonia blends.

Geopolitical Supply Chain Security

Heavy reliance on LNG imports—over 90% of Japan’s natural gas needs and Osaka Gas’s supply sourced from Australia, North America and Southeast Asia—exposes the company to diplomatic shifts; the 2024 Indonesian export curbs and 2022-23 market tightness drove spot LNG price swings up to $60–$80/MMBtu, highlighting vulnerability to sudden disruptions.

GX Green Transformation Subsidies

The Japanese government’s GX Green Transformation program allocated about ¥2.7 trillion in 2024 for hydrogen and synthetic fuels, enabling Osaka Gas to capture subsidies that offset substantial R&D costs for e-methane and hydrogen pilot projects.

Osaka Gas reported investing ¥45 billion in low-carbon R&D through FY2024, with GX grants covering a meaningful share of early-stage methanation capital expenditures.

Ongoing political support—reflected in multi-year GX funding commitments and tax incentives—is critical for Osaka Gas to scale e-methane and hydrogen pathways and pursue its 2050 carbon neutrality target.

Regional Governance and Infrastructure

As Kansai's primary utility, Osaka Gas faces local government scrutiny on disaster resilience and public safety after the 2018 Osaka earthquake; municipal audits increased oversight and disaster-readiness investment, with company capex at ¥170.8bn in FY2024 supporting resilience upgrades.

Political pressure to keep energy affordable during recessions limits tariff flexibility; Osaka Gas reported regulated LNG sales margins compressed 6% year-on-year in 2024 amid price controls and weaker demand.

Strong municipal partnerships are essential for approvals of pipelines and city gas expansions; Osaka Gas signed 12 municipal MOUs in 2024 for urban energy infrastructure and hydrogen pilot projects, easing permitting timelines.

- FY2024 capex ¥170.8bn for resilience

- 12 municipal MOUs signed in 2024

- Regulated LNG margins down 6% YoY in 2024

International Trade and Tariff Policies

Changes in global trade agreements and the EU’s Carbon Border Adjustment Mechanism raise import cost risk for Osaka Gas, potentially increasing imported LNG costs by up to 5–8% and affecting overseas project IRRs by similar margins.

Rising protectionism in China and Southeast Asia could slow expansion in energy engineering and chemicals, risking revenue growth in international operations that contributed around 12% of group revenue in FY2024.

Close monitoring of bilateral trade relations and tariff shifts is prioritized to protect valuation of the company’s overseas assets, which stood at roughly JPY 150–200 billion as of 2024.

- CBAM may add 5–8% to import energy costs

- International ops ≈12% of FY2024 revenue

- Overseas assets ≈ JPY 150–200bn (2024)

Energy pivot: ¥2.7tn GX fuels H2 shift while LNG exposure and -6% margins raise risks

Political drivers: GX funding ¥2.7tn (2024) and ¥45bn Osaka Gas low‑carbon R&D (FY2024) enable H2/e‑methane shift; LNG import dependence >90% and FY2024 capex ¥170.8bn raise exposure to export curbs and price swings (spot peaks $60–$80/MMBtu 2022–23); regulated margins down 6% YoY (2024); international ops ≈12% revenue, overseas assets JPY150–200bn (2024).

| Metric | 2024 |

|---|---|

| GX funding | ¥2.7tn |

| Osaka Gas R&D | ¥45bn |

| Capex | ¥170.8bn |

| Regulated margin change | -6% YoY |

| Intl revenue share | ≈12% |

| Overseas assets | JPY150–200bn |

What is included in the product

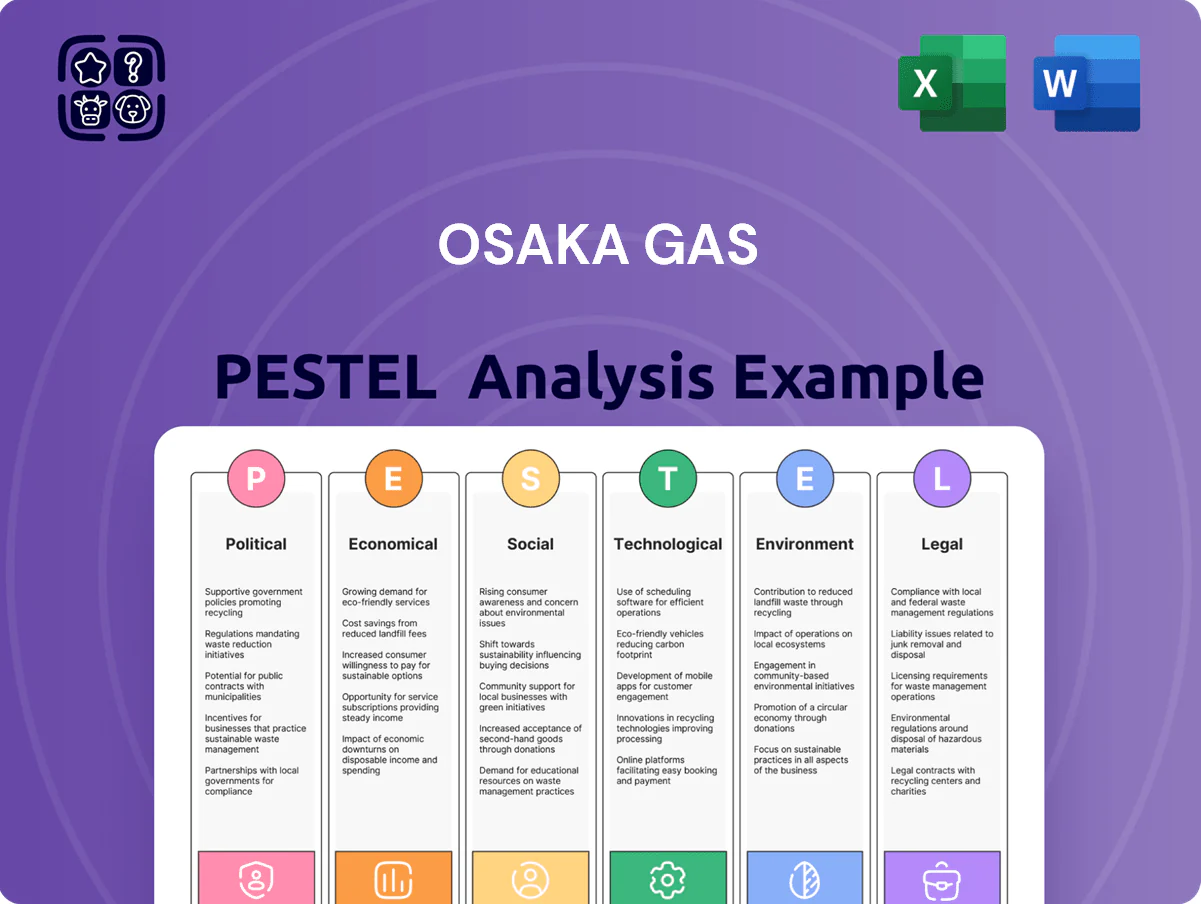

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—uniquely impact Osaka Gas, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary of Osaka Gas that’s ready to drop into presentations or strategy packs, simplifying external risk discussions and enabling quick team alignment during planning sessions.

Economic factors

Currency Exchange Rate Volatility

As a major LNG importer billing costs tied to US dollars, Osaka Gas faces rising procurement expenses when the yen weakens; yen fell about 12% vs USD from 2021–2024, pushing import costs higher and compressing margins that cannot be fully passed to consumers due to regulated tariffs. Persistent depreciation in 2024 raised import bills by an estimated ¥40–60 billion, prompting Osaka Gas to deploy hedging instruments—FX forwards, options, and natural gas-linked contracts—to stabilize EBITDA exposure to currency swings.

Global LNG Market Price Dynamics

Fluctuations in global LNG prices—Henry Hub equivalents and JKM rising 40% in 2023 to average about $16/MMBtu and settling near $11–13/MMBtu in 2024—directly raise Osaka Gas cost of sales, shrinking margins during winter peaks. High 2022–24 spot spikes increased wholesale costs versus contract rates, pressuring EBITDA. Osaka Gas mitigates exposure via long-term contracts (roughly 60–70% of volumes) plus spot purchases to stabilize procurement costs.

Interest Rate Environment in Japan

Rising BOJ rates since 2022 have pushed 10-year JGB yields from near 0% to about 0.8% in early 2026, raising corporate borrowing costs; for Osaka Gas this increases debt servicing on capital-intensive renewables and network upgrades.

With FY2025 capex guidance near JPY 120bn and renewable project IRRs sensitive to financing spreads, higher rates materially affect project feasibility.

Management must time debt issuance and consider mix of bonds, project finance and equity to optimize WACC.

Industrial Production in the Kansai Region

The Kansai manufacturing sector, representing about 12% of Japan’s industrial output, underpins strong industrial gas demand for Osaka Gas; Osaka and Hyogo hosting major steel and chemical plants consume significant volumes, with Kansai industrial production index up 1.2% year-on-year in 2024.

Factory offshoring and prolonged domestic stagnation threaten core revenues—Japan’s manufacturing employment fell 0.8% in 2023—while regional revitalization projects like Osaka’s 2025 expo-related investments (¥800 billion estimated) and semiconductor/EV supply-chain growth offer upside for energy sales and engineering services.

- Kansai accounts for ~12% of Japan industrial output; 2024 IP index +1.2% YoY

- Manufacturing jobs -0.8% in 2023, risk to gas demand

- ¥800B regional investments (2025 projects) may boost sales

- Semiconductor/EV supply-chain expansion = engineering service opportunities

Inflation and Consumer Spending Power

Rising inflation in Japan—CPI at 3.1% year‑on‑year in 2024—raises labor and material costs for Osaka Gas while eroding household real income; real wages fell 0.5% in 2024, pressuring consumer spending.

Although residential gas is essential, prolonged cost pressure could drive reduced consumption or shifts to high‑efficiency appliances and electrification, with household gas consumption down ~1.2% in 2024.

Osaka Gas must calibrate pricing and promotions to stay competitive versus electricity and renewables amid rising energy price sensitivity.

- 2024 CPI 3.1% y/y; real wages -0.5%

- Household gas use -1.2% in 2024

- Need pricing flexibility vs electricity/renewables

Yen slump lifts import costs ¥40–60bn; LNG falls to $11–13, capex ¥120bn

Yen depreciation (~12% vs USD 2021–24) raised import costs by an estimated ¥40–60bn in 2024; LNG spot averaged $11–13/MMBtu in 2024 after $16 in 2023; BOJ-driven 10y JGB ~0.8% by early 2026 raises funding costs; FY2025 capex ~¥120bn; Kansai IP +1.2% YoY 2024, manufacturing jobs -0.8% in 2023; CPI 3.1% in 2024, real wages -0.5%, household gas use -1.2% 2024.

| Metric | Value |

|---|---|

| Yen vs USD (2021–24) | -12% |

| Import cost impact 2024 | ¥40–60bn |

| LNG spot 2024 | $11–13/MMBtu |

| FY2025 capex | ¥120bn |

Same Document Delivered

Osaka Gas PESTLE Analysis

The preview shown here is the exact Osaka Gas PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, energy policy, and technological innovation are reshaping Osaka Gas’s prospects—our concise PESTLE snapshot reveals key risks and opportunities to inform smarter strategy and investment decisions; purchase the full PESTLE for a detailed, ready-to-use analysis that’s ideal for reports, pitches, and boardroom planning.

Political factors

Strategic Energy Plan Alignment

The Japanese 7th Strategic Energy Plan targets reducing CO2 emissions 46% by 2030 vs 2013 and net-zero by 2050, cementing natural gas as a transition fuel; Osaka Gas must align its strategy to meet these state mandates while pivoting toward hydrogen and ammonia blends.

Geopolitical Supply Chain Security

Heavy reliance on LNG imports—over 90% of Japan’s natural gas needs and Osaka Gas’s supply sourced from Australia, North America and Southeast Asia—exposes the company to diplomatic shifts; the 2024 Indonesian export curbs and 2022-23 market tightness drove spot LNG price swings up to $60–$80/MMBtu, highlighting vulnerability to sudden disruptions.

GX Green Transformation Subsidies

The Japanese government’s GX Green Transformation program allocated about ¥2.7 trillion in 2024 for hydrogen and synthetic fuels, enabling Osaka Gas to capture subsidies that offset substantial R&D costs for e-methane and hydrogen pilot projects.

Osaka Gas reported investing ¥45 billion in low-carbon R&D through FY2024, with GX grants covering a meaningful share of early-stage methanation capital expenditures.

Ongoing political support—reflected in multi-year GX funding commitments and tax incentives—is critical for Osaka Gas to scale e-methane and hydrogen pathways and pursue its 2050 carbon neutrality target.

Regional Governance and Infrastructure

As Kansai's primary utility, Osaka Gas faces local government scrutiny on disaster resilience and public safety after the 2018 Osaka earthquake; municipal audits increased oversight and disaster-readiness investment, with company capex at ¥170.8bn in FY2024 supporting resilience upgrades.

Political pressure to keep energy affordable during recessions limits tariff flexibility; Osaka Gas reported regulated LNG sales margins compressed 6% year-on-year in 2024 amid price controls and weaker demand.

Strong municipal partnerships are essential for approvals of pipelines and city gas expansions; Osaka Gas signed 12 municipal MOUs in 2024 for urban energy infrastructure and hydrogen pilot projects, easing permitting timelines.

- FY2024 capex ¥170.8bn for resilience

- 12 municipal MOUs signed in 2024

- Regulated LNG margins down 6% YoY in 2024

International Trade and Tariff Policies

Changes in global trade agreements and the EU’s Carbon Border Adjustment Mechanism raise import cost risk for Osaka Gas, potentially increasing imported LNG costs by up to 5–8% and affecting overseas project IRRs by similar margins.

Rising protectionism in China and Southeast Asia could slow expansion in energy engineering and chemicals, risking revenue growth in international operations that contributed around 12% of group revenue in FY2024.

Close monitoring of bilateral trade relations and tariff shifts is prioritized to protect valuation of the company’s overseas assets, which stood at roughly JPY 150–200 billion as of 2024.

- CBAM may add 5–8% to import energy costs

- International ops ≈12% of FY2024 revenue

- Overseas assets ≈ JPY 150–200bn (2024)

Energy pivot: ¥2.7tn GX fuels H2 shift while LNG exposure and -6% margins raise risks

Political drivers: GX funding ¥2.7tn (2024) and ¥45bn Osaka Gas low‑carbon R&D (FY2024) enable H2/e‑methane shift; LNG import dependence >90% and FY2024 capex ¥170.8bn raise exposure to export curbs and price swings (spot peaks $60–$80/MMBtu 2022–23); regulated margins down 6% YoY (2024); international ops ≈12% revenue, overseas assets JPY150–200bn (2024).

| Metric | 2024 |

|---|---|

| GX funding | ¥2.7tn |

| Osaka Gas R&D | ¥45bn |

| Capex | ¥170.8bn |

| Regulated margin change | -6% YoY |

| Intl revenue share | ≈12% |

| Overseas assets | JPY150–200bn |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—uniquely impact Osaka Gas, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary of Osaka Gas that’s ready to drop into presentations or strategy packs, simplifying external risk discussions and enabling quick team alignment during planning sessions.

Economic factors

Currency Exchange Rate Volatility

As a major LNG importer billing costs tied to US dollars, Osaka Gas faces rising procurement expenses when the yen weakens; yen fell about 12% vs USD from 2021–2024, pushing import costs higher and compressing margins that cannot be fully passed to consumers due to regulated tariffs. Persistent depreciation in 2024 raised import bills by an estimated ¥40–60 billion, prompting Osaka Gas to deploy hedging instruments—FX forwards, options, and natural gas-linked contracts—to stabilize EBITDA exposure to currency swings.

Global LNG Market Price Dynamics

Fluctuations in global LNG prices—Henry Hub equivalents and JKM rising 40% in 2023 to average about $16/MMBtu and settling near $11–13/MMBtu in 2024—directly raise Osaka Gas cost of sales, shrinking margins during winter peaks. High 2022–24 spot spikes increased wholesale costs versus contract rates, pressuring EBITDA. Osaka Gas mitigates exposure via long-term contracts (roughly 60–70% of volumes) plus spot purchases to stabilize procurement costs.

Interest Rate Environment in Japan

Rising BOJ rates since 2022 have pushed 10-year JGB yields from near 0% to about 0.8% in early 2026, raising corporate borrowing costs; for Osaka Gas this increases debt servicing on capital-intensive renewables and network upgrades.

With FY2025 capex guidance near JPY 120bn and renewable project IRRs sensitive to financing spreads, higher rates materially affect project feasibility.

Management must time debt issuance and consider mix of bonds, project finance and equity to optimize WACC.

Industrial Production in the Kansai Region

The Kansai manufacturing sector, representing about 12% of Japan’s industrial output, underpins strong industrial gas demand for Osaka Gas; Osaka and Hyogo hosting major steel and chemical plants consume significant volumes, with Kansai industrial production index up 1.2% year-on-year in 2024.

Factory offshoring and prolonged domestic stagnation threaten core revenues—Japan’s manufacturing employment fell 0.8% in 2023—while regional revitalization projects like Osaka’s 2025 expo-related investments (¥800 billion estimated) and semiconductor/EV supply-chain growth offer upside for energy sales and engineering services.

- Kansai accounts for ~12% of Japan industrial output; 2024 IP index +1.2% YoY

- Manufacturing jobs -0.8% in 2023, risk to gas demand

- ¥800B regional investments (2025 projects) may boost sales

- Semiconductor/EV supply-chain expansion = engineering service opportunities

Inflation and Consumer Spending Power

Rising inflation in Japan—CPI at 3.1% year‑on‑year in 2024—raises labor and material costs for Osaka Gas while eroding household real income; real wages fell 0.5% in 2024, pressuring consumer spending.

Although residential gas is essential, prolonged cost pressure could drive reduced consumption or shifts to high‑efficiency appliances and electrification, with household gas consumption down ~1.2% in 2024.

Osaka Gas must calibrate pricing and promotions to stay competitive versus electricity and renewables amid rising energy price sensitivity.

- 2024 CPI 3.1% y/y; real wages -0.5%

- Household gas use -1.2% in 2024

- Need pricing flexibility vs electricity/renewables

Yen slump lifts import costs ¥40–60bn; LNG falls to $11–13, capex ¥120bn

Yen depreciation (~12% vs USD 2021–24) raised import costs by an estimated ¥40–60bn in 2024; LNG spot averaged $11–13/MMBtu in 2024 after $16 in 2023; BOJ-driven 10y JGB ~0.8% by early 2026 raises funding costs; FY2025 capex ~¥120bn; Kansai IP +1.2% YoY 2024, manufacturing jobs -0.8% in 2023; CPI 3.1% in 2024, real wages -0.5%, household gas use -1.2% 2024.

| Metric | Value |

|---|---|

| Yen vs USD (2021–24) | -12% |

| Import cost impact 2024 | ¥40–60bn |

| LNG spot 2024 | $11–13/MMBtu |

| FY2025 capex | ¥120bn |

Same Document Delivered

Osaka Gas PESTLE Analysis

The preview shown here is the exact Osaka Gas PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers.