Oshkosh Porter's Five Forces Analysis

From Overview to Strategy Blueprint

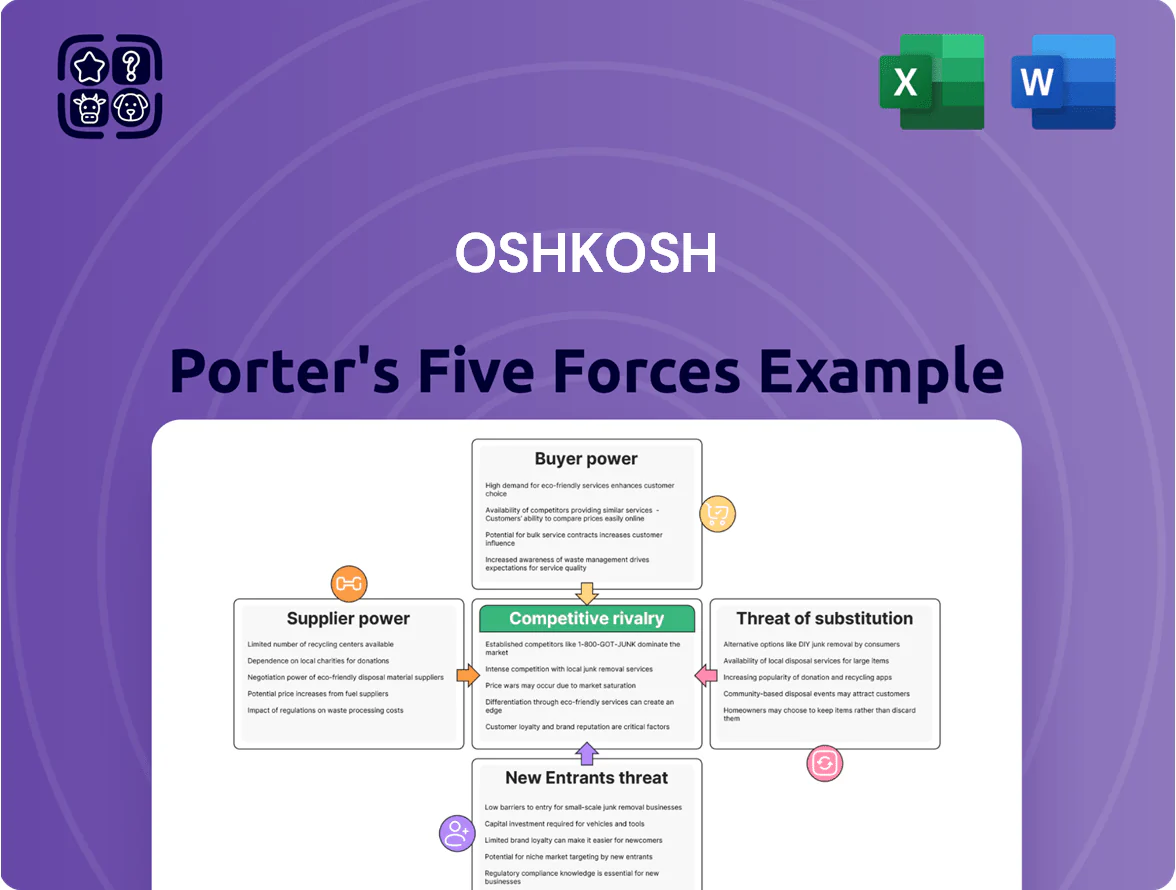

Oshkosh faces moderate supplier power, high buyer expectations, and significant rivalry from defense and commercial vehicle peers, while barriers to entry remain substantial due to scale and certification demands.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Oshkosh’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in Raw Material and Commodity Pricing

Oshkosh relies heavily on steel, aluminum, and advanced composites for specialty vehicles and access equipment; raw-materials made up about 38% of COGS in 2024. Global steel and aluminum price swings—steel up ~15% and aluminum up ~12% year‑over‑year in 2022–24 due to trade policies and Russia tensions—raise production costs and squeeze margins.

Dependence on Specialized Powertrain Components

Oshkosh’s shift to electrification in Access Equipment and Vocational lines raises dependence on a few battery and motor suppliers, concentrating supplier power as these parts are critical to meeting 2026 EPA and CARB emission rules; about 60–70% of EV component spend is projected to go to specialized vendors through 2026. Switching costs are high—platform redesigns and re‑certification can add $20k–$50k per vehicle and 12–18 months to development, limiting Oshkosh’s bargaining leverage.

Limited Sources for Defense-Grade Electronics

The Defense segment needs ruggedized electronics meeting MIL-specs; only a handful of global suppliers—estimated <10 certified firms for many tactical-grade chips—serve this market, giving suppliers high leverage.

When 2024–25 semiconductor bottlenecks pushed lead times 30–40% higher for certain wafers, Oshkosh faced cost inflation and schedule risk from suppliers who can demand premiums or long-term contracts.

Labor Market Pressures and Skilled Trade Availability

Suppliers of sub-assemblies face tight labor markets—US manufacturing job openings averaged 670,000 monthly in 2024—raising lead times and costs that Oshkosh inherits through higher parts prices and slower replenishment.

Demand for skilled technicians and engineers keeps wage inflation elevated; supplier labor cost growth of ~4–6% in 2023–24 pressured margins, prompting Oshkosh to negotiate longer contracts and pass some costs to customers.

The ripple effect forces Oshkosh to manage inventory, tighten procurement, and accelerate supplier diversification to contain margin erosion.

- Manufacturing job openings ~670,000 (2024)

- Supplier wage growth ~4–6% (2023–24)

- Longer lead times, higher parts pricing

- Actions: contract renegotiation, supplier diversification

Strategic Partnerships and Vertical Integration

Oshkosh reduces supplier power through strategic partnerships and selective vertical integration, co-developing proprietary systems (e.g., defence vehicle electronics) to avoid single-vendor price shocks; in 2024 R&D and supplier collaboration spend rose ~8% to $300M, supporting in‑house modules that cut supplier spend on those items by an estimated 12%.

Still, for commodity industrial parts—fasteners, bearings, hydraulics—Oshkosh remains exposed to large distributors; overall supplier costs were ~55% of COGS in FY2024, so market pricing for standard components still pressures margins.

- Co-development reduces single-vendor risk, 12% cost cut estimate

- R&D/supplier collaboration spend ~$300M in 2024 (+8%)

- Supplier costs ≈55% of COGS in FY2024

- Commodity parts remain subject to distributor pricing

Suppliers hold leverage as commodity swings and EV specialist concentration raise costs

Suppliers exert moderate-to-high power: raw materials ~38% of COGS (2024), supplier costs ≈55% of COGS, commodity price swings (steel +15%, aluminum +12% 2022–24) and limited MIL-spec chip vendors (<10) raise leverage; EV component concentration (60–70% spend to specialists through 2026) and high switching costs ($20k–$50k, 12–18 months) limit bargaining, partly offset by $300M R&D/co‑dev (+8%) cutting some supplier spend ~12%.

| Metric | Value |

|---|---|

| Raw materials % of COGS (2024) | 38% |

| Supplier costs % of COGS (FY2024) | 55% |

| Steel/aluminum change (2022–24) | +15% / +12% |

| EV component spend to specialists (to 2026) | 60–70% |

| R&D/supplier collaboration (2024) | $300M (+8%) |

| Estimated cost cut from co‑dev | ~12% |

What is included in the product

Tailored Porter's Five Forces analysis for Oshkosh that uncovers competitive intensity, supplier and buyer leverage, threat of substitutes and new entrants, and highlights disruptive risks and strategic barriers protecting incumbency.

A concise Porter's Five Forces one-sheet for Oshkosh—quickly highlights competitive intensity and relief points for strategic decisions.

Customers Bargaining Power

Concentration of Government and Defense Contracts

A significant share of Oshkosh Corporation’s revenue comes from the U.S. Department of Defense and U.S. Postal Service; in FY2024 defense-related sales were about 36% of total revenue (~$3.2bn of $8.9bn), giving these buyers outsized bargaining power.

These agencies set technical specs, strict delivery schedules, and price ceilings, squeezing margins and shifting compliance costs to Oshkosh.

The loss of one major contract can cut utilization sharply; a single program cancellation historically trimmed segment EBITDA by double-digit percentage points within a year.

Influence of Large Equipment Rental Companies

In Access Equipment, a few large renters—United Rentals (2025 revenue $12.8B) and Sunbelt (Ahern Rentals/ARI combined significant share)—buy high volumes, giving them strong price and financing leverage over Oshkosh; they often secure discounts north of 10% on fleet purchases. Their order flow tracks construction cycles, and late‑2025 cooling saw rental utilization drop ~3–4%, letting buyers delay or cancel orders and press for looser payment terms.

Municipal Budget Constraints in Fire and Emergency

Fire departments and municipal governments, funded primarily by local property and sales tax, are the main buyers in Oshkosh’s Fire & Emergency segment; 2023 US municipal revenue growth slowed to 1.8%, tightening budgets and buying power. Competitive bidding rules push suppliers to compete on price and on long-term service contracts, pressuring margins. Pierce maintains strong brand loyalty, but 2024 austerity moves saw 27% of respondents request lower-cost or value-focused configurations. Municipal demand shifts mean Oshkosh must balance price, uptime, and lifecycle service costs.

Increasing Demand for Total Cost of Ownership Transparency

Modern fleet buyers focus on total cost of ownership (TCO) not sticker price, so Oshkosh must show fuel use, maintenance intervals, and 5-year resale values to justify premium pricing; 2024 fleet studies show TCO drives 68% of purchase decisions in municipal fleets.

Buyers use TCO data to demand discounts, longer warranties, and service packages, and pressure rises as competitors roll out electric models with 30–50% lower fuel and maintenance projections over 10 years.

- 68% of municipal purchases driven by TCO (2024 study)

- Electric alternatives claim 30–50% lower TCO over 10 years

- Oshkosh must supply fuel, maintenance, resale data to protect margins

Low Switching Costs in Certain Vocational Markets

In refuse collection and concrete mixer markets, customers face low switching costs, so price or service slips let buyers shift brands quickly; Oshkosh’s durable gear helps retain clients, but competitors like Mack, Volvo, and Terex keep options open.

This dynamic kept Vocational OEM ASPs under pressure in 2024—industry truck ASPs fell ~2–3% YoY—forcing Oshkosh to push incremental tech and service contracts to protect margins.

- Low switching costs enable quick brand moves

- Oshkosh durability = retention advantage

- Strong competitors keep pricing tight

- 2024 ASPs down ~2–3% YoY; fuels product/service focus

Buyers Squeeze Margins: DoD/USPS 36% Revenue, Renters >10% Discounts, ASPs -2–3%

Buyers hold high power: DoD/USPS = 36% of FY2024 revenue (~$3.2B of $8.9B), large renters (United Rentals $12.8B 2025) extract >10% fleet discounts, municipal budgets slow (2023 growth 1.8%) and 68% of municipal buys driven by TCO (2024); ASPs down ~2–3% YoY (2024) press service/warranty sales.

| Metric | Value |

|---|---|

| DoD/USPS share FY2024 | 36% (~$3.2B) |

| Renters discount | >10% |

| Municipal TCO influence | 68% (2024) |

| Industry ASP change 2024 | -2–3% YoY |

What You See Is What You Get

Oshkosh Porter's Five Forces Analysis

This preview shows the exact Oshkosh Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for download.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Oshkosh faces moderate supplier power, high buyer expectations, and significant rivalry from defense and commercial vehicle peers, while barriers to entry remain substantial due to scale and certification demands.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Oshkosh’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in Raw Material and Commodity Pricing

Oshkosh relies heavily on steel, aluminum, and advanced composites for specialty vehicles and access equipment; raw-materials made up about 38% of COGS in 2024. Global steel and aluminum price swings—steel up ~15% and aluminum up ~12% year‑over‑year in 2022–24 due to trade policies and Russia tensions—raise production costs and squeeze margins.

Dependence on Specialized Powertrain Components

Oshkosh’s shift to electrification in Access Equipment and Vocational lines raises dependence on a few battery and motor suppliers, concentrating supplier power as these parts are critical to meeting 2026 EPA and CARB emission rules; about 60–70% of EV component spend is projected to go to specialized vendors through 2026. Switching costs are high—platform redesigns and re‑certification can add $20k–$50k per vehicle and 12–18 months to development, limiting Oshkosh’s bargaining leverage.

Limited Sources for Defense-Grade Electronics

The Defense segment needs ruggedized electronics meeting MIL-specs; only a handful of global suppliers—estimated <10 certified firms for many tactical-grade chips—serve this market, giving suppliers high leverage.

When 2024–25 semiconductor bottlenecks pushed lead times 30–40% higher for certain wafers, Oshkosh faced cost inflation and schedule risk from suppliers who can demand premiums or long-term contracts.

Labor Market Pressures and Skilled Trade Availability

Suppliers of sub-assemblies face tight labor markets—US manufacturing job openings averaged 670,000 monthly in 2024—raising lead times and costs that Oshkosh inherits through higher parts prices and slower replenishment.

Demand for skilled technicians and engineers keeps wage inflation elevated; supplier labor cost growth of ~4–6% in 2023–24 pressured margins, prompting Oshkosh to negotiate longer contracts and pass some costs to customers.

The ripple effect forces Oshkosh to manage inventory, tighten procurement, and accelerate supplier diversification to contain margin erosion.

- Manufacturing job openings ~670,000 (2024)

- Supplier wage growth ~4–6% (2023–24)

- Longer lead times, higher parts pricing

- Actions: contract renegotiation, supplier diversification

Strategic Partnerships and Vertical Integration

Oshkosh reduces supplier power through strategic partnerships and selective vertical integration, co-developing proprietary systems (e.g., defence vehicle electronics) to avoid single-vendor price shocks; in 2024 R&D and supplier collaboration spend rose ~8% to $300M, supporting in‑house modules that cut supplier spend on those items by an estimated 12%.

Still, for commodity industrial parts—fasteners, bearings, hydraulics—Oshkosh remains exposed to large distributors; overall supplier costs were ~55% of COGS in FY2024, so market pricing for standard components still pressures margins.

- Co-development reduces single-vendor risk, 12% cost cut estimate

- R&D/supplier collaboration spend ~$300M in 2024 (+8%)

- Supplier costs ≈55% of COGS in FY2024

- Commodity parts remain subject to distributor pricing

Suppliers hold leverage as commodity swings and EV specialist concentration raise costs

Suppliers exert moderate-to-high power: raw materials ~38% of COGS (2024), supplier costs ≈55% of COGS, commodity price swings (steel +15%, aluminum +12% 2022–24) and limited MIL-spec chip vendors (<10) raise leverage; EV component concentration (60–70% spend to specialists through 2026) and high switching costs ($20k–$50k, 12–18 months) limit bargaining, partly offset by $300M R&D/co‑dev (+8%) cutting some supplier spend ~12%.

| Metric | Value |

|---|---|

| Raw materials % of COGS (2024) | 38% |

| Supplier costs % of COGS (FY2024) | 55% |

| Steel/aluminum change (2022–24) | +15% / +12% |

| EV component spend to specialists (to 2026) | 60–70% |

| R&D/supplier collaboration (2024) | $300M (+8%) |

| Estimated cost cut from co‑dev | ~12% |

What is included in the product

Tailored Porter's Five Forces analysis for Oshkosh that uncovers competitive intensity, supplier and buyer leverage, threat of substitutes and new entrants, and highlights disruptive risks and strategic barriers protecting incumbency.

A concise Porter's Five Forces one-sheet for Oshkosh—quickly highlights competitive intensity and relief points for strategic decisions.

Customers Bargaining Power

Concentration of Government and Defense Contracts

A significant share of Oshkosh Corporation’s revenue comes from the U.S. Department of Defense and U.S. Postal Service; in FY2024 defense-related sales were about 36% of total revenue (~$3.2bn of $8.9bn), giving these buyers outsized bargaining power.

These agencies set technical specs, strict delivery schedules, and price ceilings, squeezing margins and shifting compliance costs to Oshkosh.

The loss of one major contract can cut utilization sharply; a single program cancellation historically trimmed segment EBITDA by double-digit percentage points within a year.

Influence of Large Equipment Rental Companies

In Access Equipment, a few large renters—United Rentals (2025 revenue $12.8B) and Sunbelt (Ahern Rentals/ARI combined significant share)—buy high volumes, giving them strong price and financing leverage over Oshkosh; they often secure discounts north of 10% on fleet purchases. Their order flow tracks construction cycles, and late‑2025 cooling saw rental utilization drop ~3–4%, letting buyers delay or cancel orders and press for looser payment terms.

Municipal Budget Constraints in Fire and Emergency

Fire departments and municipal governments, funded primarily by local property and sales tax, are the main buyers in Oshkosh’s Fire & Emergency segment; 2023 US municipal revenue growth slowed to 1.8%, tightening budgets and buying power. Competitive bidding rules push suppliers to compete on price and on long-term service contracts, pressuring margins. Pierce maintains strong brand loyalty, but 2024 austerity moves saw 27% of respondents request lower-cost or value-focused configurations. Municipal demand shifts mean Oshkosh must balance price, uptime, and lifecycle service costs.

Increasing Demand for Total Cost of Ownership Transparency

Modern fleet buyers focus on total cost of ownership (TCO) not sticker price, so Oshkosh must show fuel use, maintenance intervals, and 5-year resale values to justify premium pricing; 2024 fleet studies show TCO drives 68% of purchase decisions in municipal fleets.

Buyers use TCO data to demand discounts, longer warranties, and service packages, and pressure rises as competitors roll out electric models with 30–50% lower fuel and maintenance projections over 10 years.

- 68% of municipal purchases driven by TCO (2024 study)

- Electric alternatives claim 30–50% lower TCO over 10 years

- Oshkosh must supply fuel, maintenance, resale data to protect margins

Low Switching Costs in Certain Vocational Markets

In refuse collection and concrete mixer markets, customers face low switching costs, so price or service slips let buyers shift brands quickly; Oshkosh’s durable gear helps retain clients, but competitors like Mack, Volvo, and Terex keep options open.

This dynamic kept Vocational OEM ASPs under pressure in 2024—industry truck ASPs fell ~2–3% YoY—forcing Oshkosh to push incremental tech and service contracts to protect margins.

- Low switching costs enable quick brand moves

- Oshkosh durability = retention advantage

- Strong competitors keep pricing tight

- 2024 ASPs down ~2–3% YoY; fuels product/service focus

Buyers Squeeze Margins: DoD/USPS 36% Revenue, Renters >10% Discounts, ASPs -2–3%

Buyers hold high power: DoD/USPS = 36% of FY2024 revenue (~$3.2B of $8.9B), large renters (United Rentals $12.8B 2025) extract >10% fleet discounts, municipal budgets slow (2023 growth 1.8%) and 68% of municipal buys driven by TCO (2024); ASPs down ~2–3% YoY (2024) press service/warranty sales.

| Metric | Value |

|---|---|

| DoD/USPS share FY2024 | 36% (~$3.2B) |

| Renters discount | >10% |

| Municipal TCO influence | 68% (2024) |

| Industry ASP change 2024 | -2–3% YoY |

What You See Is What You Get

Oshkosh Porter's Five Forces Analysis

This preview shows the exact Oshkosh Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for download.