OTP Bank Business Model Canvas

OTP Bank Business Model Canvas: Strategic Blueprint for Investors & Strategists

Unlock the full strategic blueprint behind OTP Bank's business model—this concise Business Model Canvas exposes how OTP creates customer value, leverages partnerships, and monetizes services across retail and corporate banking; ideal for investors, strategists, and consultants seeking actionable insights.

Partnerships

Strategic Insurance Alliances

OTP Bank partners long-term with Groupama to sell life, property and casualty insurance via 1,500+ OTP branches and digital channels across 10 CEE markets, driving cross-sell: insurance contributed ~8% of non-interest income in 2024 and helped lift bancassurance revenue by €120m in 2023–24.

Technology and Fintech Collaborators

OTP Bank partners with fintechs and software vendors to speed its digital transformation, integrating payment rails, AI-driven credit risk models, and upgraded cybersecurity; by 2024 OTP reported 28% of transactions processed via digital channels and €1.2bn in IT spend over 2022–24 to support scale.

Payment Network Providers

Visa and Mastercard let OTP Bank issue globally accepted debit and credit cards, processing ~90% of international card volumes; they supply network rails for domestic and cross-border transactions and co-develop security standards like 3D Secure and tokenization for mobile wallets.

Regional Regulatory and Government Bodies

OTP Bank maintains active ties with central banks and financial regulators across its 11 CEE markets, ensuring compliance with evolving fiscal laws and securing operating licenses; in 2024 OTP reported regulatory capital (CET1) at 14.8%, supporting participation in government lending schemes and economic programs.

These transparent relationships enable access to state-backed credit lines during volatility—OTP tapped €350m in public-sector facilities in 2023—and help the bank adapt quickly to legislative shifts, preserving market trust and license stability.

- Operates in 11 CEE countries

- CET1 ratio 14.8% (2024)

- €350m public facilities tapped (2023)

- Supports government lending and development programs

- Crucial during regional volatility and law changes

Corporate and SME Ecosystem Partners

OTP Bank partners with business associations and chambers to run joint workshops, SME lending programs, and entrepreneur financial literacy initiatives, reaching over 12,000 SMEs in Hungary and CEE in 2024 and contributing to a 6% rise in commercial loan originations year-on-year.

Embedding in local ecosystems improves deal flow for high-quality corporate borrowers and lets OTP tailor products to regional sectors, supporting a 3.5% reduction in SME default rates where programs operate.

- 12,000+ SMEs engaged (2024)

- 6% YoY increase in commercial loan originations

- 3.5% lower SME default rate in program regions

- Activities: workshops, specialized lending, financial literacy

OTP partners drive €120m bancassurance uplift, 28% digital, CET1 14.8% — 12k+ SMEs

OTP’s key partners (Groupama, Visa/Mastercard, fintechs, regulators, chambers) drive bancassurance €120m uplift (2023–24), 28% digital transactions (2024), CET1 14.8% (2024), €350m public facilities tapped (2023), 12,000+ SMEs engaged (2024) and 6% YoY loan growth.

| Partner | Metric | Value |

|---|---|---|

| Groupama | Bancassurance uplift | €120m (2023–24) |

| Digital/Fintech | Digital txns | 28% (2024) |

| Regulators | CET1 | 14.8% (2024) |

| Public facilities | Tapped | €350m (2023) |

| SME programs | SMEs reached | 12,000+ (2024) |

| SME programs | Loan origination growth | 6% YoY (2024) |

What is included in the product

A concise, pre-written Business Model Canvas for OTP Bank detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and governance, reflecting real-world operations and strategic priorities.

High-level, editable Business Model Canvas for OTP Bank that condenses its banking strategy into a one-page snapshot—ideal for boardrooms, quick comparisons, and collaborative adaptation to relieve the pain of building structured financial models from scratch.

Activities

Core Banking and Lending Operations

OTP Bank manages deposits and issues mortgages, consumer loans, and corporate lending, with total loans of EUR 28.6bn and customer deposits of EUR 34.1bn as of FY 2024; core lending drives net interest income and fee margins.

Digital Banking Development and Maintenance

OTP Bank invests heavily in continuous improvement of its mobile and internet banking—R&D and IT capex reached HUF 42.3bn (≈€110m) in 2024—to shift transactions from branches to digital channels and cut costs. This includes agile software development, UX design, and enterprise-grade cybersecurity (SOC, MFA, end-to-end encryption) to retain younger users and support a 2024 digital adoption rate of ~68% among retail clients.

Regional Market Integration and M&A

OTP’s core activity is acquiring and integrating smaller banks across Central and Eastern Europe; since 2016 it closed over 10 deals, adding ~3.5 million customers and raising group assets by ~25% to €64.2bn by end-2024.

Integration focuses on IT standardization, product alignment, and cultural onboarding to cut costs ~12% per unit and achieve faster cross-sell, supporting rapid geographic scale-up.

Risk Management and Compliance

OTP Bank continuously monitors market, credit, and operational risks to protect capital and deposits, using AML protocols and IFRS compliance; in 2024 its group loan loss provisions covered 62% of non-performing loans, showing active loss absorption.

Dedicated risk teams apply advanced analytics to predict defaults and stress results—OTP reported a CET1 ratio of 14.8% in 2024—preserving reputation and avoiding fines through a strong compliance culture.

- Loan loss provisions: coverage 62% of NPLs (2024)

- CET1 ratio: 14.8% (2024)

- AML, IFRS adherence: mandatory across subsidiaries

- Advanced analytics: PD/LGD models for stress testing

Customer Advisory and Wealth Management

OTP Bank offers tailored advisory and wealth management to HNWIs and corporates, including portfolio management, brokerage, and retirement planning by specialist advisors; these services drove about 18% of 2024 fee income in the Group’s private banking segment (OTP Group FY2024 report).

Focus on long-term, high-touch relationships boosts retention and cross-sell, with private banking AUM ≈ EUR 12.3bn in 2024 and fee margins ~0.65%.

- Services: portfolio mgmt, brokerage, retirement planning

- Clients: HNWIs, corporates, specialist advisors

- 2024 figures: AUM EUR 12.3bn; fee income ~18%

- Strategy: high-touch, long-term relationships

OTP Bank: €64.2bn assets, €28.6bn loans, €34.1bn deposits, €110m digital push, 14.8% CET1

OTP Bank issues loans (EUR 28.6bn) and gathers deposits (EUR 34.1bn), invests HUF 42.3bn (~€110m) in digital R&D (68% retail digital adoption), acquires CEE banks (assets €64.2bn, +25% since 2016), maintains CET1 14.8% and NPL coverage 62%, and manages private banking AUM €12.3bn (fee income 18%).

| Metric | 2024 |

|---|---|

| Loans | €28.6bn |

| Deposits | €34.1bn |

| Digital R&D capex | HUF42.3bn (~€110m) |

| Digital adoption | 68% |

| Group assets | €64.2bn |

| CET1 | 14.8% |

| NPL coverage | 62% |

| Private AUM | €12.3bn |

Preview Before You Purchase

Business Model Canvas

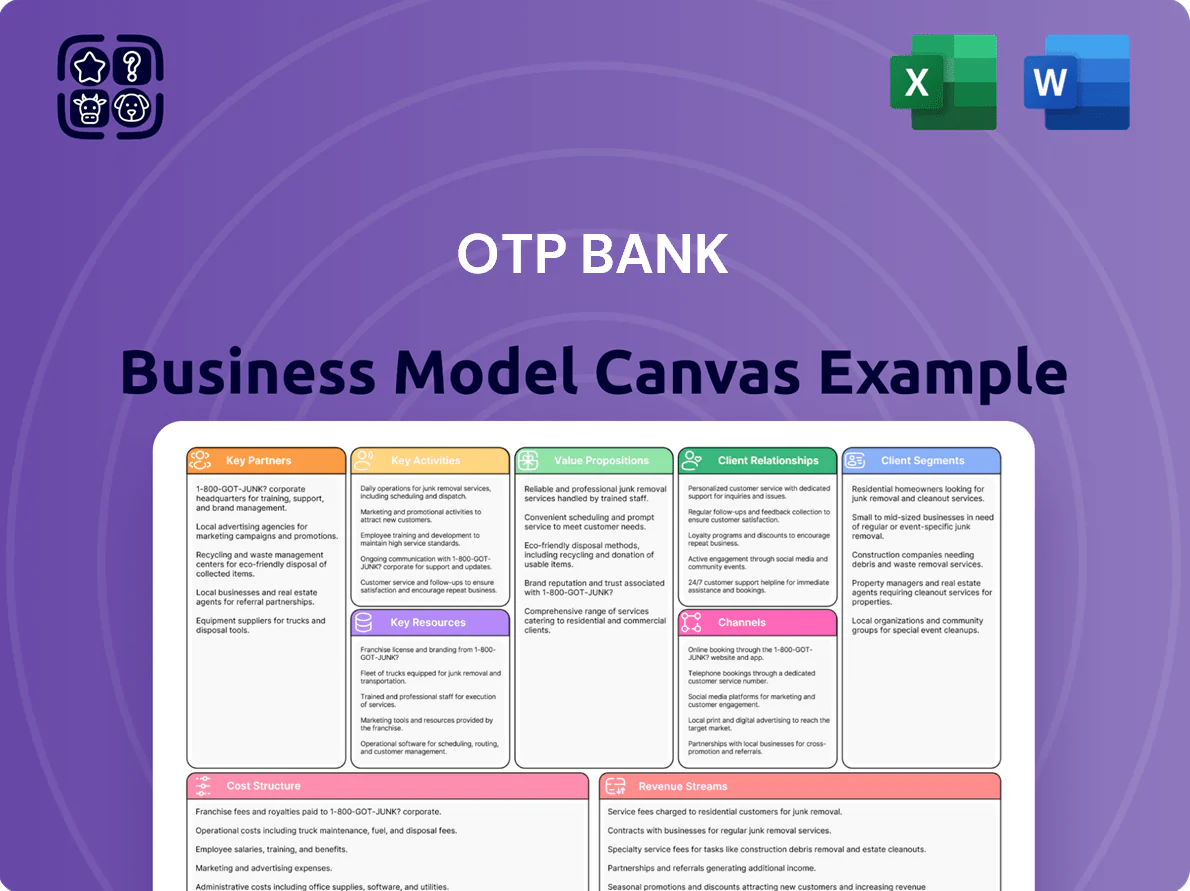

The document you’re previewing is the actual OTP Bank Business Model Canvas you’ll receive—no mockup or sample—so when you purchase, you’ll download this exact, fully formatted file ready for editing and presentation in Word and Excel.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

OTP Bank Business Model Canvas: Strategic Blueprint for Investors & Strategists

Unlock the full strategic blueprint behind OTP Bank's business model—this concise Business Model Canvas exposes how OTP creates customer value, leverages partnerships, and monetizes services across retail and corporate banking; ideal for investors, strategists, and consultants seeking actionable insights.

Partnerships

Strategic Insurance Alliances

OTP Bank partners long-term with Groupama to sell life, property and casualty insurance via 1,500+ OTP branches and digital channels across 10 CEE markets, driving cross-sell: insurance contributed ~8% of non-interest income in 2024 and helped lift bancassurance revenue by €120m in 2023–24.

Technology and Fintech Collaborators

OTP Bank partners with fintechs and software vendors to speed its digital transformation, integrating payment rails, AI-driven credit risk models, and upgraded cybersecurity; by 2024 OTP reported 28% of transactions processed via digital channels and €1.2bn in IT spend over 2022–24 to support scale.

Payment Network Providers

Visa and Mastercard let OTP Bank issue globally accepted debit and credit cards, processing ~90% of international card volumes; they supply network rails for domestic and cross-border transactions and co-develop security standards like 3D Secure and tokenization for mobile wallets.

Regional Regulatory and Government Bodies

OTP Bank maintains active ties with central banks and financial regulators across its 11 CEE markets, ensuring compliance with evolving fiscal laws and securing operating licenses; in 2024 OTP reported regulatory capital (CET1) at 14.8%, supporting participation in government lending schemes and economic programs.

These transparent relationships enable access to state-backed credit lines during volatility—OTP tapped €350m in public-sector facilities in 2023—and help the bank adapt quickly to legislative shifts, preserving market trust and license stability.

- Operates in 11 CEE countries

- CET1 ratio 14.8% (2024)

- €350m public facilities tapped (2023)

- Supports government lending and development programs

- Crucial during regional volatility and law changes

Corporate and SME Ecosystem Partners

OTP Bank partners with business associations and chambers to run joint workshops, SME lending programs, and entrepreneur financial literacy initiatives, reaching over 12,000 SMEs in Hungary and CEE in 2024 and contributing to a 6% rise in commercial loan originations year-on-year.

Embedding in local ecosystems improves deal flow for high-quality corporate borrowers and lets OTP tailor products to regional sectors, supporting a 3.5% reduction in SME default rates where programs operate.

- 12,000+ SMEs engaged (2024)

- 6% YoY increase in commercial loan originations

- 3.5% lower SME default rate in program regions

- Activities: workshops, specialized lending, financial literacy

OTP partners drive €120m bancassurance uplift, 28% digital, CET1 14.8% — 12k+ SMEs

OTP’s key partners (Groupama, Visa/Mastercard, fintechs, regulators, chambers) drive bancassurance €120m uplift (2023–24), 28% digital transactions (2024), CET1 14.8% (2024), €350m public facilities tapped (2023), 12,000+ SMEs engaged (2024) and 6% YoY loan growth.

| Partner | Metric | Value |

|---|---|---|

| Groupama | Bancassurance uplift | €120m (2023–24) |

| Digital/Fintech | Digital txns | 28% (2024) |

| Regulators | CET1 | 14.8% (2024) |

| Public facilities | Tapped | €350m (2023) |

| SME programs | SMEs reached | 12,000+ (2024) |

| SME programs | Loan origination growth | 6% YoY (2024) |

What is included in the product

A concise, pre-written Business Model Canvas for OTP Bank detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and governance, reflecting real-world operations and strategic priorities.

High-level, editable Business Model Canvas for OTP Bank that condenses its banking strategy into a one-page snapshot—ideal for boardrooms, quick comparisons, and collaborative adaptation to relieve the pain of building structured financial models from scratch.

Activities

Core Banking and Lending Operations

OTP Bank manages deposits and issues mortgages, consumer loans, and corporate lending, with total loans of EUR 28.6bn and customer deposits of EUR 34.1bn as of FY 2024; core lending drives net interest income and fee margins.

Digital Banking Development and Maintenance

OTP Bank invests heavily in continuous improvement of its mobile and internet banking—R&D and IT capex reached HUF 42.3bn (≈€110m) in 2024—to shift transactions from branches to digital channels and cut costs. This includes agile software development, UX design, and enterprise-grade cybersecurity (SOC, MFA, end-to-end encryption) to retain younger users and support a 2024 digital adoption rate of ~68% among retail clients.

Regional Market Integration and M&A

OTP’s core activity is acquiring and integrating smaller banks across Central and Eastern Europe; since 2016 it closed over 10 deals, adding ~3.5 million customers and raising group assets by ~25% to €64.2bn by end-2024.

Integration focuses on IT standardization, product alignment, and cultural onboarding to cut costs ~12% per unit and achieve faster cross-sell, supporting rapid geographic scale-up.

Risk Management and Compliance

OTP Bank continuously monitors market, credit, and operational risks to protect capital and deposits, using AML protocols and IFRS compliance; in 2024 its group loan loss provisions covered 62% of non-performing loans, showing active loss absorption.

Dedicated risk teams apply advanced analytics to predict defaults and stress results—OTP reported a CET1 ratio of 14.8% in 2024—preserving reputation and avoiding fines through a strong compliance culture.

- Loan loss provisions: coverage 62% of NPLs (2024)

- CET1 ratio: 14.8% (2024)

- AML, IFRS adherence: mandatory across subsidiaries

- Advanced analytics: PD/LGD models for stress testing

Customer Advisory and Wealth Management

OTP Bank offers tailored advisory and wealth management to HNWIs and corporates, including portfolio management, brokerage, and retirement planning by specialist advisors; these services drove about 18% of 2024 fee income in the Group’s private banking segment (OTP Group FY2024 report).

Focus on long-term, high-touch relationships boosts retention and cross-sell, with private banking AUM ≈ EUR 12.3bn in 2024 and fee margins ~0.65%.

- Services: portfolio mgmt, brokerage, retirement planning

- Clients: HNWIs, corporates, specialist advisors

- 2024 figures: AUM EUR 12.3bn; fee income ~18%

- Strategy: high-touch, long-term relationships

OTP Bank: €64.2bn assets, €28.6bn loans, €34.1bn deposits, €110m digital push, 14.8% CET1

OTP Bank issues loans (EUR 28.6bn) and gathers deposits (EUR 34.1bn), invests HUF 42.3bn (~€110m) in digital R&D (68% retail digital adoption), acquires CEE banks (assets €64.2bn, +25% since 2016), maintains CET1 14.8% and NPL coverage 62%, and manages private banking AUM €12.3bn (fee income 18%).

| Metric | 2024 |

|---|---|

| Loans | €28.6bn |

| Deposits | €34.1bn |

| Digital R&D capex | HUF42.3bn (~€110m) |

| Digital adoption | 68% |

| Group assets | €64.2bn |

| CET1 | 14.8% |

| NPL coverage | 62% |

| Private AUM | €12.3bn |

Preview Before You Purchase

Business Model Canvas

The document you’re previewing is the actual OTP Bank Business Model Canvas you’ll receive—no mockup or sample—so when you purchase, you’ll download this exact, fully formatted file ready for editing and presentation in Word and Excel.